يُعدّ تسريع طرح المنتجات في السوق ميزةً بالغة الأهمية تُسهّلها الملكية الفكرية لأشباه الموصلات، إذ تُوفّر وحدات وظيفية مُصمّمة ومُتحقّق منها مسبقًا، تندمج بسلاسة في التصاميم المُخصّصة. ومن خلال الاستفادة من الملكية الفكرية الحالية، يُمكن للمصممين تجنّب تعقيدات البدء من الصفر، مما يُبسّط تطوير مُكوّنات أشباه الموصلات المُعقّدة. وهذا يُقلّل من دورة التصميم ويُمكّن الشركات من الاستجابة السريعة لمتطلبات السوق من الأجهزة الإلكترونية المُتقدّمة. وتكمن أهمية ذلك في البقاء في الطليعة في ظلّ المنافسة الشديدة في مجال التكنولوجيا من خلال طرح مُنتجات مُبتكرة في السوق بسرعة.

يمكنك الوصول إلى التقرير الكامل على https://www.databridgemarketresearch.com/reports/north-america-semiconductor-ip-market

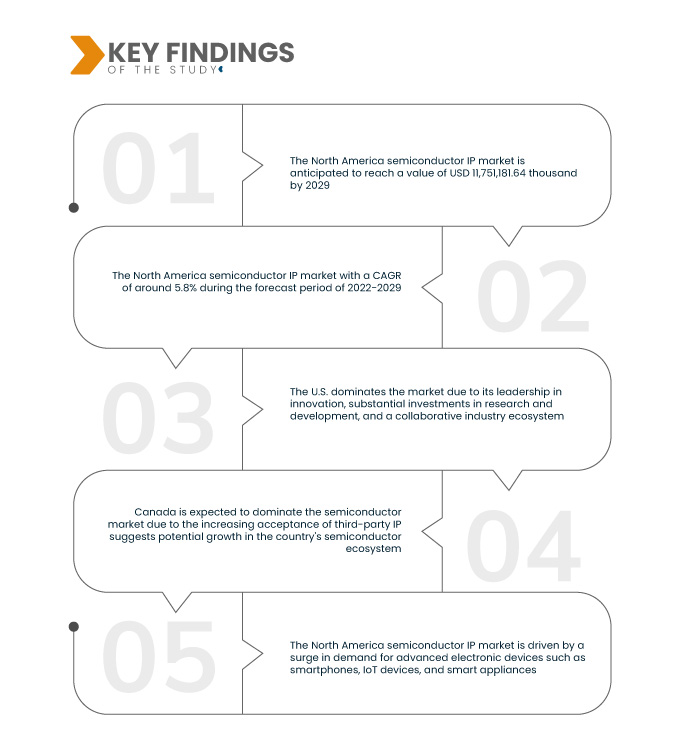

حلل بحث سوق داتا بريدج سوق الملكية الفكرية لأشباه الموصلات في أمريكا الشمالية، ومن المتوقع أن تصل قيمته إلى 1,751,181.64 ألف دولار أمريكي بحلول عام 2029، مقارنةً بـ 1,115,439 ألف دولار أمريكي في عام 2021، بمعدل نمو سنوي مركب قدره 5.8% خلال الفترة المتوقعة 2022-2029. ويُعدّ التعقيد المتزايد لتصاميم أشباه الموصلات في أمريكا الشمالية، مدفوعًا بالطلب على وظائف وأداء أفضل في الأجهزة الإلكترونية، محركًا رئيسيًا لسوق الملكية الفكرية لأشباه الموصلات.

النتائج الرئيسية للدراسة

من المتوقع أن يؤدي التركيز المتزايد على إلكترونيات السيارات إلى دفع معدل نمو السوق

برز التركيز المتزايد على إلكترونيات السيارات كمحرك رئيسي لسوق أشباه الموصلات في أمريكا الشمالية. وقد أدى التكامل السريع للمكونات الإلكترونية في صناعة السيارات، مدفوعًا باتجاهات جديدة مثل السيارات الكهربائية وأنظمة مساعدة السائق المتقدمة (ADAS)، إلى زيادة الطلب على حلول أشباه الموصلات المتخصصة في الملكية الفكرية. تلبي هذه الحلول المتطلبات الفريدة لتطبيقات السيارات، بما في ذلك الوظائف الحيوية للسلامة والاتصال داخل السيارة. ومع تزايد التقدم التكنولوجي في المركبات، يستجيب مزودو حلول الملكية الفكرية لأشباه الموصلات بابتكارات مصممة خصيصًا لقطاع السيارات، مما يساهم في نمو وديناميكية سوق أشباه الموصلات في أمريكا الشمالية.

نطاق التقرير وتقسيم السوق

مقياس التقرير

|

تفاصيل

|

فترة التنبؤ

|

من 2022 إلى 2029

|

سنة الأساس

|

2021

|

السنوات التاريخية

|

2020 (قابلة للتخصيص حتى 2014-2019)

|

الوحدات الكمية

|

الإيرادات بالألف دولار أمريكي، التسعير بالدولار الأمريكي، الحجم بالوحدات

|

القطاعات المغطاة

|

النوع (CPU SIP، Wired SIP، GPU SIP، Memory SIP، DSP SIP، Library SIP، Infrastructure SIP، Digital SIP، Analog SIP، Wireless SIP وغيرها)، النموذج (Soft Form، Hard Form)، مصدر IP (الترخيص، حقوق الملكية)، القناة (المصادر المباشرة، كتالوج الإنترنت)، المستخدم النهائي (السيارات، الاتصالات، الإلكترونيات الاستهلاكية ، الصناعية، الدفاعية، التجارية، الطبية، وغيرها)

|

الدول المغطاة

|

الولايات المتحدة وكندا والمكسيك في أمريكا الشمالية

|

الجهات الفاعلة في السوق المغطاة

|

Rambus.com (الولايات المتحدة)، Dolphin Design SAS (فرنسا)، Xilinx (الولايات المتحدة)، Arm Limited (شركة تابعة لمجموعة SoftBank Group Corp.) (المملكة المتحدة)، Cadence Design Systems, Inc. (الولايات المتحدة)، Siemens (ألمانيا)، eMemory Technology Inc. (تايوان)، Wave Computing, Inc. (الولايات المتحدة)، Lattice Semiconductor (الولايات المتحدة)، VeriSilicon (الصين)، Digital Core Design (بولندا)، Dream Chip Technologies GmbH (ألمانيا)، Achronix Semiconductor Corporation (الولايات المتحدة)، Faraday Technology Corporation (تايوان)، Synopsys, Inc. (الولايات المتحدة)، CEVA, Inc. (الولايات المتحدة)

|

نقاط البيانات التي يغطيها التقرير

|

بالإضافة إلى الرؤى حول سيناريوهات السوق مثل القيمة السوقية ومعدل النمو والتجزئة والتغطية الجغرافية واللاعبين الرئيسيين، تتضمن تقارير السوق التي تم تنظيمها بواسطة Data Bridge Market Research أيضًا تحليلًا متعمقًا من الخبراء والإنتاج والقدرة التمثيلية الجغرافية للشركة وتخطيطات الشبكة للموزعين والشركاء وتحليل اتجاهات الأسعار التفصيلية والمحدثة وتحليل العجز في سلسلة التوريد والطلب.

|

تحليل القطاعات:

يتم تقسيم سوق أشباه الموصلات IP في أمريكا الشمالية على أساس النوع والشكل ومصدر IP والقناة والمستخدم النهائي.

- على أساس النوع، يتم تقسيم سوق IP لأشباه الموصلات في أمريكا الشمالية إلى CPU SIP، وSIP السلكي، وGPU SIP، وSIP للذاكرة، وDSP SIP، وSIP للمكتبة، وSIP للبنية التحتية، وSIP الرقمي، وSIP التناظري، وSIP اللاسلكي، وغيرها.

- على أساس الشكل، يتم تقسيم سوق أشباه الموصلات الملكية الفكرية في أمريكا الشمالية إلى شكل ناعم وشكل صلب

- على أساس مصدر الملكية الفكرية، يتم تقسيم سوق الملكية الفكرية لأشباه الموصلات في أمريكا الشمالية إلى الترخيص، والملكية

- على أساس القناة، يتم تقسيم سوق الملكية الفكرية لأشباه الموصلات في أمريكا الشمالية إلى مصادر مباشرة وكتالوج الإنترنت

- على أساس المستخدم النهائي، يتم تقسيم سوق الملكية الفكرية لأشباه الموصلات في أمريكا الشمالية إلى السيارات والاتصالات والإلكترونيات الاستهلاكية والصناعية والدفاعية والتجارية والطبية وغيرها

اللاعبون الرئيسيون

تعترف شركة Data Bridge Market Research بالشركات التالية باعتبارها اللاعبين الرئيسيين في سوق الملكية الفكرية لأشباه الموصلات في أمريكا الشمالية: Rambus.com (الولايات المتحدة)، Dolphin Design SAS (فرنسا)، Xilinx (الولايات المتحدة)، Arm Limited (شركة تابعة لشركة SoftBank Group Corp.) (المملكة المتحدة)، Cadence Design Systems, Inc. (الولايات المتحدة)، Siemens (ألمانيا)، eMemory Technology Inc. (تايوان)، Wave Computing, Inc. (الولايات المتحدة).

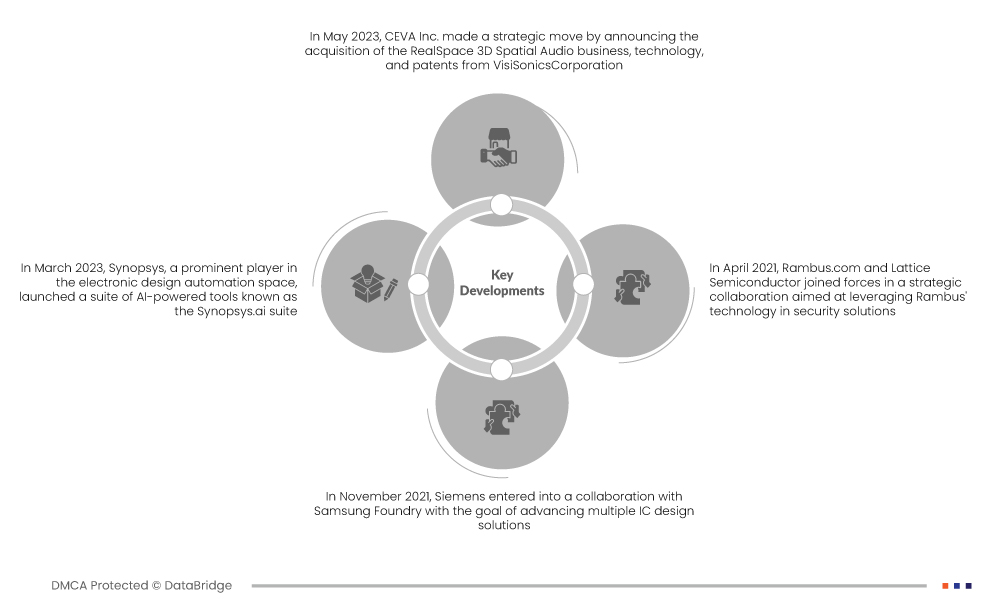

تطورات السوق

- في مايو 2023، اتخذت شركة CEVA Inc. خطوة استراتيجية بإعلانها الاستحواذ على أعمال وتقنيات وبراءات اختراع RealSpace 3D Spatial Audio من شركة VisiSonicsCorporation. وقد تميّز هذا الاستحواذ بدمج فريق البحث والتطوير الخاص بالصوت المكاني لشركة VisiSonics وبرمجياته في شركة CEVA، وهي شركة في ماريلاند تقع بالقرب من مركز البحث والتطوير الخاص بدمج أجهزة الاستشعار التابع لشركة CEVA. وقد ساهم إضافة قدرات الصوت المكاني لشركة VisiSonics في توسيع محفظة برامج CEVA التطبيقية للأنظمة المدمجة. وعززت هذه الخطوات مكانة CEVA في سوق الأجهزة القابلة للارتداء، حيث أصبح الصوت المكاني أساسيًا. وكان من المتوقع أن يساهم هذا الاستحواذ الاستراتيجي في نمو CEVA من خلال تعزيز قدراتها التكنولوجية وحضورها في السوق.

- في مارس 2023، أطلقت شركة سينوبسيس، الرائدة في مجال أتمتة تصميم الإلكترونيات، مجموعة من الأدوات المدعومة بالذكاء الاصطناعي تُعرف باسم مجموعة Synopsys.ai. غطت هذه المجموعة عملية تصميم الرقاقة بأكملها، من الهندسة المعمارية إلى التصنيع. تهدف مجموعة Synopsys.ai إلى إحداث ثورة في تصميم الرقاقة من خلال توفير إمكانية تقليل وقت التطوير بشكل كبير، وخفض التكاليف، وتحسين الأداء، وزيادة الإنتاجية. كانت هذه المجموعة من الأدوات قيّمة بشكل خاص لتصميمات الرقاقات التي تستهدف العقد المتقدمة مثل 5 نانومتر، و3 نانومتر، وفئة 2 نانومتر، وما فوقها. كان من المتوقع أن يُحدث نهج سينوبسيس المبتكر تغييرًا جذريًا في مجال أتمتة تصميم الإلكترونيات، واضعًا معايير جديدة للكفاءة والفعالية في هذه الصناعة.

- في نوفمبر 2021، تعاونت شركة سيمنز مع شركة سامسونج فاوندري لتطوير حلول تصميم متعددة للدوائر المتكاملة. تناول هذا التعاون جوانب أساسية في عملية التصميم، بما في ذلك التغليف، والتفريغ الكهروستاتيكي، والدوائر المتكاملة. وقد مكنت هذه الشراكة الاستراتيجية مع شركة سامسونج فاوندري شركة سيمنز من تسريع نمو المبيعات وزيادة الإيرادات. ومن خلال الاستفادة من خبرات كل منهما، سعى كل من سيمنز وسامسونج فاوندري إلى المساهمة في تطوير حلول تصميم الدوائر المتكاملة، وتعزيز الابتكار في صناعة أشباه الموصلات.

- في أبريل 2021، تعاونت Rambus.com مع Lattice Semiconductor في تعاون استراتيجي للاستفادة من تقنيات Rambus في حلول الأمن. كان من المتوقع أن يُحسّن هذا التعاون تقنية منتجات Rambus من خلال دمج حلول أمنية جديدة. كان من المتوقع أن يُمكّن دمج تقنيات Lattice Semiconductor شركة Rambus من تقديم حلول مُحسّنة وأكثر أمانًا لعملائها. من خلال البقاء في طليعة التطورات التكنولوجية، تهدف هذه الشراكة إلى جذب عملاء جدد وتسريع نمو إيرادات كل من Rambus.com وLattice Semiconductor.

التحليل الإقليمي

من الناحية الجغرافية، البلدان التي يغطيها تقرير سوق أشباه الموصلات الملكية الفكرية في أمريكا الشمالية هي الولايات المتحدة وكندا والمكسيك في أمريكا الشمالية.

وفقًا لتحليل Data Bridge Market Research:

الولايات المتحدة هي الدولة المهيمنة في سوق الملكية الفكرية لأشباه الموصلات في أمريكا الشمالية خلال الفترة المتوقعة 2022-2029

تُهيمن الولايات المتحدة على سوق أشباه الموصلات، مدفوعةً بمجموعة من العوامل. وقد مكّن التزامها بالابتكار واستثماراتها الكبيرة في البحث والتطوير الشركات الأمريكية من الحفاظ على ريادتها التكنولوجية. كما يُعزز النظام البيئي القوي والبيئة التعاونية قوة هذه الصناعة. ويلعب الطلب العالمي المتزايد على الأجهزة المتصلة، المدفوع باتجاهات مثل إنترنت الأشياء، وشبكات الجيل الخامس، والتقنيات الذكية، دورًا محوريًا. وتتمتع شركات أشباه الموصلات الأمريكية، مع شركات عملاقة مثل إنتل، وإنفيديا، وكوالكوم، وإيه إم دي، بمكانة ممتازة لتلبية هذا الطلب، مما يُسهم في هيمنة البلاد.

من المتوقع أن تكون كندا الدولة الأسرع نموًا في سوق الملكية الفكرية لأشباه الموصلات في أمريكا الشمالية للفترة المتوقعة 2022-2029

من المتوقع أن تهيمن كندا على السوق بفضل القبول المتزايد لحقوق الملكية الفكرية للجهات الخارجية. وتكمن قوة كندا في إطارها القانوني المتين لحماية الملكية الفكرية، ومنظومة ابتكار مزدهرة، وحكومتها التي تدعم البحث والتطوير. وإذا شهد قطاع التكنولوجيا نموًا كبيرًا، فسيؤدي ذلك إلى زيادة الطلب على حلول الملكية الفكرية للجهات الخارجية. كما أن السياسات الداعمة للأعمال، والتعاون العالمي، والشعب المتمكن من التكنولوجيا، وسهولة الحصول على التمويل، كلها عوامل تُسهم في تعزيز هيمنة كندا المحتملة على السوق.

لمزيد من المعلومات التفصيلية حول تقرير سوق أشباه الموصلات IP في أمريكا الشمالية ، انقر هنا - https://www.databridgemarketresearch.com/reports/north-america-semiconductor-ip-market