الألومنيوم هو العنصر المعدني الأكثر شيوعًا، إذ يُشكل أكثر من 8% من كتلة قشرة الأرض، وهو معدن خفيف الوزن، أبيض فضي اللون، غير مغناطيسي، ومرن. كما أنه أكثر المعادن غير الحديدية استخدامًا. تشمل تطبيقاته الأسقف، وعزل الرقائق المعدنية، والنوافذ، والكسوة، والأبواب، وواجهات المتاجر، والدرابزين، والأدوات المعمارية. كما يُعدّ استخدامًا شائعًا للألمنيوم في ألواح العتبات والأرضيات التجارية.

يمكنكم الاطلاع على التقرير الكامل عبر الرابط التالي: https://www.databridgemarketresearch.com/reports/saudi-arabia-aluminum-market

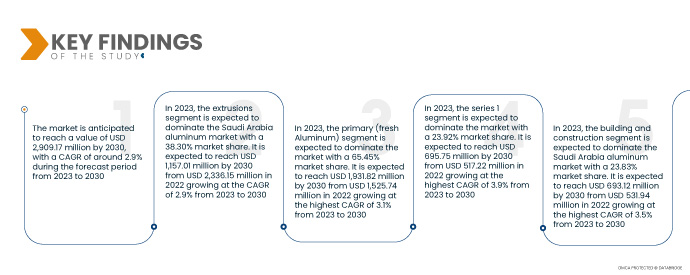

تحلل شركة Data Bridge Market Research أن سوق الألمنيوم في المملكة العربية السعودية من المتوقع أن ينمو بمعدل نمو سنوي مركب نسبته 2.9٪ من عام 2023 إلى عام 2030 ومن المتوقع أن يصل إلى 2،909.17 مليون دولار أمريكي بحلول عام 2030.

النتائج الرئيسية للدراسة

من المتوقع أن تؤدي سياسات إزالة الكربون والتحول إلى عالم أكثر استدامة إلى دفع نمو السوق

نظراً لارتفاع انبعاثات ثاني أكسيد الكربون في المملكة العربية السعودية سنوياً، فقد التزمت المملكة بتجاوز صافي انبعاثات الكربون الصفرية بحلول عام 2060. وتستثمر المملكة بشكل كبير في مصادر الطاقة المتجددة، مع سعيها في الوقت نفسه إلى تقليل هدر الطاقة وزيادة كفاءتها. إضافةً إلى ذلك، تستثمر المملكة العربية السعودية في مشاريع البنية التحتية الخضراء، وتبحث عن سبل لتخزين ونقل الطاقة. وتُظهر هذه المبادرات التزام المملكة العربية السعودية بمكافحة تغير المناخ، وتقديم نموذج يُحتذى به لمستقبل أكثر استدامة.

يساهم قطاع الألمنيوم في المملكة العربية السعودية بنسبة ضئيلة في انبعاثات ثاني أكسيد الكربون في البلاد. يستهلك قطاع الألمنيوم الرئيسي أكثر من 900 تيراواط ساعة من الطاقة سنويًا، وينبعث منه 1.1 جيجا طن من غازات الاحتباس الحراري. لو كان الألمنيوم الأولي دولةً لحلّ خامس أكبر مستهلك للكهرباء في العالم. كما تُطلق ملايين الأطنان من غازات الاحتباس الحراري، مثل غازات الكربون المشبع بالفلور وثاني أكسيد الكبريت وأكاسيد النيتروز والمركبات المتطايرة، أثناء تصنيع الألمنيوم الأولي، إلى جانب ثاني أكسيد الكربون. بالإضافة إلى ذلك، يجب تخزين 175 مليون طن من نفايات الطين الأحمر الكاوي الخطرة الناتجة عن تكرير الألومينا للمصاهر سنويًا. مع تشديد القيود البيئية عالميًا، تتسارع جهود إزالة الكربون في الشرق الأوسط.

سيتوجب على القطاع الخاص توفير الجزء الأكبر من خطة إزالة الكربون، لكنها ستعتمد على الأسس التي وضعتها الحكومة. ويعمل القطاع الصناعي في القطاع الخاص بنشاط على دمج عناصر الاستدامة في خططه المؤسسية والتجارية لضمان تطبيق تدابير استدامة فعّالة على امتداد سلسلة القيمة الصناعية. تدعم الحكومة السعودية نمو الأعمال المستدامة من خلال إرساء أفضل الممارسات، وإطلاق مشاريع تركز على الابتكار، وتشجيع تبادل المعلومات. ونتيجةً لذلك، من المتوقع أن ينمو السوق بفضل التزام المصنّعين بإزالة الكربون والانتقال إلى لوائح عالمية أكثر استدامة، مما يُتوقع أن يُحفّز نمو السوق.

نطاق التقرير وتقسيم السوق

مقياس التقرير

|

تفاصيل

|

فترة التنبؤ

|

من 2023 إلى 2030

|

سنة الأساس

|

2022

|

السنوات التاريخية

|

2021 (قابلة للتخصيص حتى 2015-2020)

|

الوحدات الكمية

|

الإيرادات بالملايين من الدولارات الأمريكية، والحجم بالآلاف من الأطنان

|

القطاعات المغطاة

|

حسب الفئة (الصب، البثق، التشكيل، المنتجات المدرفلة المسطحة، والأصباغ والمساحيق)، المصدر (أولي (ألومنيوم طازج) وثانوي (ألومنيوم مُعاد تدويره))، السلسلة (السلسلة 1، السلسلة 2، السلسلة 3، السلسلة 4، السلسلة 5، السلسلة 6، السلسلة 7، والسلسلة 8)، المستخدم النهائي (السيارات، الصناعة، التغليف، البناء والتشييد، الكهرباء والإلكترونيات، الفضاء، الأجهزة المنزلية، الأدوات الهندسية، التغليف، وغيرها)

|

المناطق المغطاة

|

المملكة العربية السعودية

|

الجهات الفاعلة في السوق المغطاة

|

مجموعة التيسير شركة تالكو الصناعية (المملكة العربية السعودية)، شركة ألكوا (معادن) (الولايات المتحدة)، ألوبكو (المملكة العربية السعودية)، معادن أبورا (المملكة العربية السعودية)، ألما (المملكة العربية السعودية)، والصالح (المملكة العربية السعودية) وغيرها.

|

نقاط البيانات التي يغطيها التقرير

|

بالإضافة إلى الرؤى حول سيناريوهات السوق مثل القيمة السوقية ومعدل النمو والتجزئة والتغطية الجغرافية واللاعبين الرئيسيين، تتضمن تقارير السوق التي تم تنظيمها بواسطة Data Bridge Market Research أيضًا تحليلًا متعمقًا من الخبراء والإنتاج والقدرة التمثيلية الجغرافية للشركة وتخطيطات الشبكة للموزعين والشركاء وتحليل اتجاهات الأسعار التفصيلية والمحدثة وتحليل العجز في سلسلة التوريد والطلب.

|

تحليل القطاعات

يتم تقسيم السوق إلى أربعة قطاعات بارزة بناءً على الفئة والمصدر والسلسلة والمستخدم النهائي.

- بناءً على الفئة، يتم تقسيم السوق إلى الصب، والبثق، والتزوير، والمنتجات المدرفلة المسطحة، والأصباغ والمساحيق.

ومن المتوقع أن تهيمن صناعة البثق على سوق الألمنيوم في المملكة العربية السعودية في عام 2023 .

ومن المتوقع أن تهيمن قطاعات البثق على سوق الألمنيوم في المملكة العربية السعودية في عام 2023، وذلك بفضل خفة وزنها وقوتها ومقاومتها للتآكل وسرعة طرحها في السوق واستدامتها وموصلاتها الممتازة وعدم قابليتها للاشتعال وعدم سميتها وغيرها.

- بناءً على المصدر، يُقسّم السوق إلى قسمين: أولي (ألومنيوم طازج) وثانوي (ألومنيوم مُعاد تدويره). في عام ٢٠٢٣، من المتوقع أن يُهيمن قطاع أولي (ألومنيوم طازج) على السوق بحصة سوقية تبلغ ٦٥.٤٥٪، نظرًا لاستخدامه الواسع في التطبيقات الكهربائية والرقائق والتغليف. بالإضافة إلى ذلك، يُمكن خلطه بعناصر أخرى لزيادة قوته.

- على أساس السلسلة، يتم تقسيم السوق إلى السلسلة 1، والسلسلة 2، والسلسلة 3، والسلسلة 4، والسلسلة 5، والسلسلة 6، والسلسلة 7، والسلسلة 8. في عام 2023، من المتوقع أن تهيمن شريحة السلسلة 1 على السوق بحصة سوقية تبلغ 23.92٪ حيث يتم استخدامها في تطبيقات مثل المعدات الكيميائية والألواح والألواح والرقائق وأدوات المائدة المعدنية وغيرها.

- على أساس المستخدم النهائي، يتم تقسيم السوق إلى السيارات، والصناعة، والبناء والتشييد، والكهرباء والإلكترونيات، والفضاء، والأجهزة المنزلية ، وأدوات الهندسة، والتعبئة والتغليف، وغيرها.

ومن المتوقع أن يهيمن قطاع البناء والتشييد للاستخدام النهائي على سوق الألمنيوم في المملكة العربية السعودية في عام 2023.

ومن المتوقع أن يهيمن قطاع البناء والتشييد على السوق في عام 2023 بحصة سوقية تبلغ 23.83% بسبب قدرته على التكيف وخفته وقدرته على تحمل التكاليف وقدرته على توفير المتانة والدعم الإضافيين.

اللاعبون الرئيسيون

تعترف شركة داتا بريدج لأبحاث السوق بالشركات التالية باعتبارها اللاعبين الرئيسيين في سوق الألمنيوم في المملكة العربية السعودية والتي تشمل مجموعة التيسير، شركة تالكو الصناعية (المملكة العربية السعودية)، شركة ألكوا (معادن) (الولايات المتحدة)، ألوبكو (المملكة العربية السعودية)، معادن أبورا (المملكة العربية السعودية)، ألما (المملكة العربية السعودية)، والصالح (المملكة العربية السعودية).

تطوير السوق

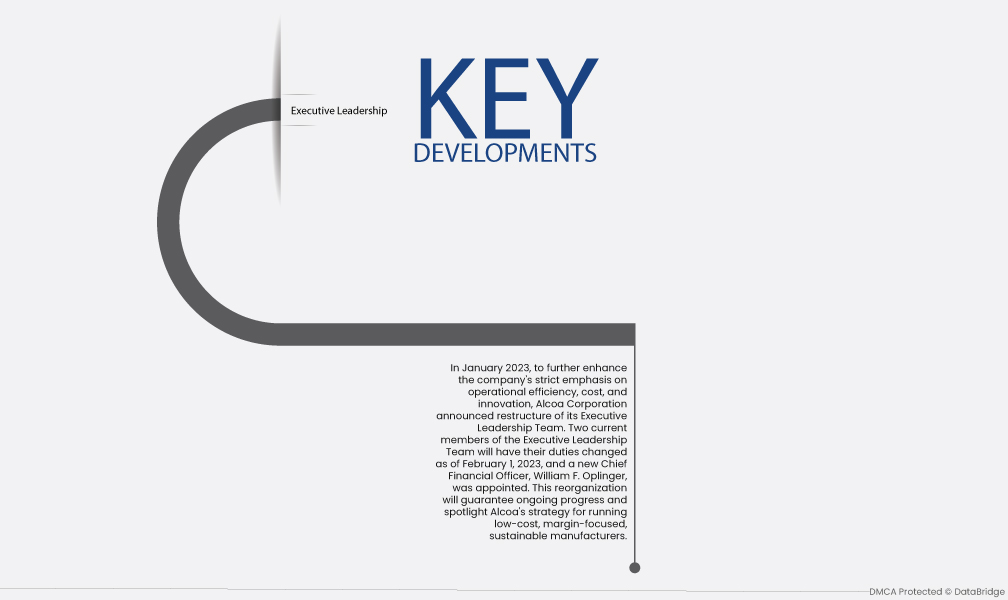

- في يناير 2023، ولتعزيز تركيز الشركة على الكفاءة التشغيلية والتكلفة والابتكار، أعلنت شركة ألكوا عن إعادة هيكلة فريقها القيادي التنفيذي. وسيتم تغيير مهام عضوين حاليين في فريق القيادة التنفيذية اعتبارًا من 1 فبراير 2023، كما تم تعيين ويليام إف. أوبلينجر مديرًا ماليًا جديدًا. تضمن عملية إعادة الهيكلة هذه استمرار التقدم وتسلط الضوء على استراتيجية ألكوا لإدارة شركات تصنيع مستدامة منخفضة التكلفة، تركز على هامش الربح.

لمزيد من المعلومات التفصيلية حول تقرير سوق الألمنيوم في المملكة العربية السعودية، انقر هنا - https://www.databridgemarketresearch.com/reports/saudi-arabia-aluminum-market