Global Antiviral Api Market

Tamanho do mercado em biliões de dólares

CAGR :

%

USD

1.18 Billion

USD

2.33 Billion

2025

2033

USD

1.18 Billion

USD

2.33 Billion

2025

2033

| 2026 –2033 | |

| USD 1.18 Billion | |

| USD 2.33 Billion | |

| % | |

|

Segmentação Global de Mercado de API Antiviral, ByTipoAnálogos Nucleosídeos, Inibidores da Protease, Inibidores da Transcriptase Reversa Não Nucleosídeo (NNRTIs), Inibidores da Integrase e OutrosAplicaçãoHIV, Hepatite B & C, Influenza, COVID-19, Herpes e Outros), Usuário finalEmpresas Farmacêuticas, Organizações de Pesquisa de Contratos (OCR), Organizações de Desenvolvimento de Contratos e Manufacturing (CDMOs), Hospitais e Institutos de Pesquisa) - Tendências e Previsão da Indústria para 2033

Tamanho do Mercado da API Antiviral

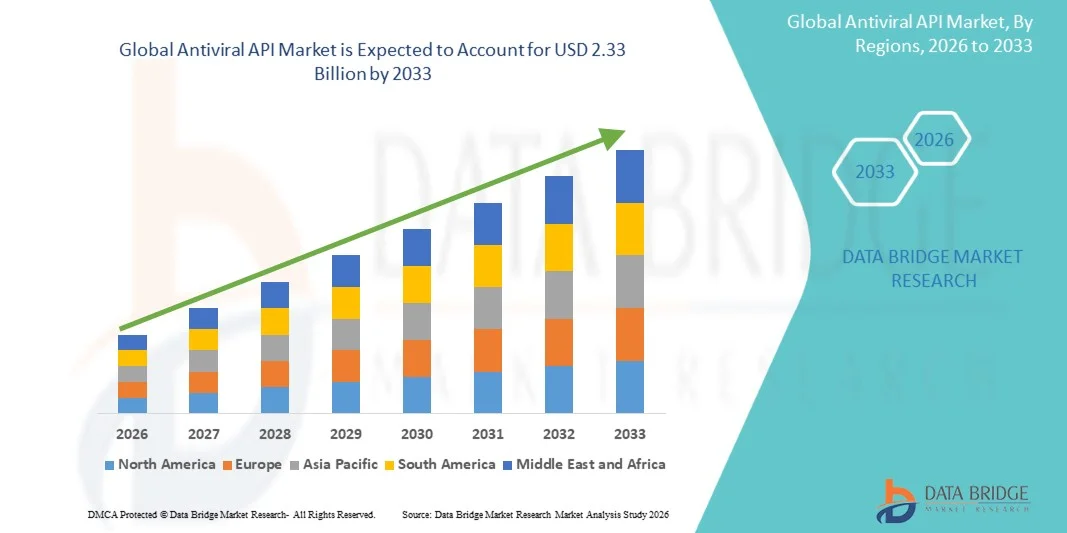

- O tamanho global do mercado de API antiviral foi avaliado em1,18 mil milhões de dólares em 2025e espera-se alcançarUSD 2,33 mil milhões até 2033, em umaCAGR de 8,90%durante o período de previsão

- O crescimento do mercado é amplamente impulsionado pelo aumento da prevalência de infecções virais, aumento da demanda por terapias antivirais eficazes e avanços tecnológicos contínuos no desenvolvimento de medicamentos antivirais, levando à maior adoção de ingredientes farmacêuticos antivirais ativos (APIs) na fabricação farmacêutica

- Além disso, o crescente investimento em P&D, a expansão das capacidades de produção farmacêutica e o crescente foco na preparação para pandemias e na medicina personalizada estão estabelecendo APIs antivirais como componentes essenciais de soluções terapêuticas modernas. Esses fatores convergentes estão acelerando a absorção de soluções de API antiviral, aumentando significativamente o crescimento da indústria

Análise de Mercado Antiviral API

- APIs antivirais, servindo como ingredientes farmacêuticos ativos em terapias para infecções virais como HIV, Hepatite, Influenza, COVID-19 e Herpes, são componentes cada vez mais vitais da fabricação farmacêutica moderna devido ao seu papel crítico no desenvolvimento eficaz de antivirais e resultados terapêuticos

- A crescente demanda por APIs antivirais é alimentada principalmente pela crescente prevalência de infecções virais, crescente foco na preparação pandêmica, aumento dos investimentos em I&D e expansão das capacidades de produção farmacêutica em todo o mundo, impulsionando a adoção de APIs antivirais de alta qualidade

- A América do Norte dominou o mercado de API antiviral com a maior parcela de receita de aproximadamente 39,2% em 2025, apoiada por infraestrutura farmacêutica avançada, quadros regulatórios fortes, alta demanda por terapias antivirais e presença de fabricantes farmacêuticos-chave, com os EUA contribuindo com a maioria da demanda regional

- Asia-Pacific é esperado para ser a região de crescimento mais rápido no mercado de API antiviral durante o período de previsão, impulsionado pelo aumento dos investimentos em saúde, ampliação das capacidades de fabricação de API na China e Índia, políticas governamentais de apoio e crescente demanda por medicamentos terapêuticos controlados

- O segmento HIV representou o maior percentual de receita de mercado de 41,2% em 2025, impulsionado pela demanda sustentada por terapia antirretroviral e inclusão nos programas nacionais de HIV.

Alcance do relatório e Segmentação do Mercado Antiviral API

| Atributos | Visão do mercado chave da API antiviral |

| Segmentos Cobertos |

|

| Países abrangidos | América do Norte

Europa

Ásia- Pacífico

Médio Oriente e África

América do Sul

|

| Jogadores do mercado chave |

|

| Oportunidades de Mercado |

|

| Informações sobre o Valor Adicionado | Além dos insights sobre cenários de mercado, como valor de mercado, taxa de crescimento, segmentação, cobertura geográfica e grandes atores, os relatórios de mercado curados pela Data Bridge Market Research também incluem análise de especialistas em profundidade, epidemiologia de pacientes, análise de pipelines, análise de preços e marco regulatório. |

Tendências do mercado de API antiviral

“Importância aumentada das terapias antivirais avançadas“

- Uma tendência significativa e acelerada no mercado global de API antiviral é o crescente desenvolvimento e produção de agentes antivirais de alta eficácia, incluindo terapias de amplo espectro e direcionadas, visando combater infecções virais emergentes em todo o mundo. Esta tendência reflecte a crescente procura de terapêutica de resposta rápida e de preparação para pandemias.

- Por exemplo, em março de 2023, a Gilead Sciences expandiu sua instalação de fabricação de API antiviral na Irlanda para aumentar a produção de compostos antivirais de amplo espectro investigativos, atendendo às necessidades globais de abastecimento

- Os fabricantes também estão focando em APIs biotecnológicas, como proteínas recombinantes e análogos nucleósidos, para melhorar a eficácia terapêutica, reduzir efeitos colaterais e apoiar formulações avançadas. Por exemplo, em julho de 2022, Merck lançou uma nova API antiviral baseada em nucleósidos para uso em tratamentos orais e injetáveis

- O mercado está vendo uma mudança para APIs antivirais compatíveis com GMP de alta pureza para atender aos requisitos regulatórios e garantir qualidade consistente do produto. Em 2021, Lonza atualizou sua instalação de produção suíça para produzir APIs antivirais de alta pureza, apoiando ensaios clínicos e fornecimento comercial

- Esta tendência para APIs antivirais mais eficientes, seguras e escaláveis está fundamentalmente reformulando as prioridades e estratégias de produção de P&D farmacêuticas

- A crescente ênfase nas terapias antivirais avançadas está impulsionando inovação, colaboração e investimentos em toda a indústria farmacêutica, uma vez que as empresas visam atender às demandas de saúde globais

Dinâmica de Mercado de API Antiviral

Controlador

“Crescimento da carga de doenças virais e preparação pandémica”

- A crescente prevalência de infecções virais em todo o mundo, incluindo HIV, hepatite, influenza e vírus zoonóticos emergentes, tem criado uma necessidade urgente de APIs antivirais de alta qualidade. Governos, instituições de saúde e empresas farmacêuticas estão priorizando o desenvolvimento da API antiviral para fortalecer a preparação e melhorar os resultados terapêuticos globalmente

- Por exemplo, em 2022, a OMS relatou surtos significativos de gripe no Sudeste Asiático, levando governos e fabricantes privados a aumentar a produção de APIs antivirais para estoques de emergência e disponibilidade de tratamento

- As empresas farmacêuticas estão cada vez mais investindo em novas APIs capazes de abordar cepas virais resistentes, terapias multidrogas e tempos de resposta terapêutica mais rápidos. Isso está impulsionando inovações em química antiviral, otimização de processos e métodos de produção biotecnológica

- A demanda por APIs antivirais prontas para pandemia não se limita aos países desenvolvidos; economias emergentes como Índia, Brasil e África do Sul também estão investindo em capacidades de produção locais para garantir auto-suficiência, que está acelerando ainda mais o crescimento do mercado

- Colaborações globais entre governos, instituições acadêmicas e empresas de biotecnologia estão facilitando o desenvolvimento, licenciamento e distribuição de APIs mais rápidas. Estas iniciativas visam garantir que os medicamentos antivirais de alta qualidade sejam acessíveis durante os surtos, reforçando a resiliência e a expansão do mercado.

- No geral, a combinação do aumento da prevalência de doenças virais, das prioridades globais de segurança da saúde e da inovação tecnológica na produção de APIs é um dos principais motores do mercado de APIs antivirais, tornando-se um dos segmentos mais dinâmicos na fabricação farmacêutica.

Restrição/Desafio

“Altos custos de produção e requisitos regulamentares rigorosos“

- A produção de APIs antivirais, especialmente compostos biotecnológicos derivados, como análogos de nucleósidos e proteínas recombinantes, envolve processos químicos complexos, equipamentos especializados e rigoroso controle de qualidade. Estes factores aumentam significativamente os custos de fabrico, o que pode impedir os pequenos operadores de entrarem no mercado

- Por exemplo, em maio de 2022, um fabricante indiano de API adiou o lançamento comercial de uma API antiviral recém-desenvolvida devido aos elevados custos necessários para atualizar suas instalações para cumprir rigorosas normas GMP e conformidade regulamentar internacional

- Além do investimento de capital, os fabricantes devem aderir a padrões rigorosos de segurança, pureza e consistência mandatados por agências reguladoras globais como o FDA, EMA e PMDA (Japão). Isso muitas vezes envolve validação multi-estágios, documentação extensa, e testes de qualidade repetidos, todos os quais adicionar às despesas operacionais

- Os altos custos de produção podem limitar a acessibilidade das APIs antivirais em países de baixa e média renda, retardando a adoção generalizada, apesar da crescente demanda terapêutica. Isto pode criar disparidades regionais no acesso a tratamentos antivirais críticos durante surtos

- Além disso, flutuar os preços das matérias-primas, depender de produtos químicos precursores específicos e cadeias de suprimentos complexas tornam a produção contínua de API desafiadora, especialmente durante emergências globais ou interrupções geopolíticas

- Globalmente, a combinação de requisitos de capital elevados, carga de conformidade regulamentar e processos de produção complexos continua a ser uma restrição significativa para o mercado de API Antiviral, impactando tanto os novos operadores como os fabricantes estabelecidos que procuram expandir a capacidade globalmente

Âmbito de mercado da API antiviral

O mercado é segmentado com base no tipo, aplicação e usuário final.

• Por tipo

Com base no tipo, o mercado Antiviral API é segmentado em Nucleoside Analogs, Protease Inibitors, Non-Nucleoside Reverse Transcriptase Inibitors (NNRTIs), Inibidores Integrase, e Outros. O segmento de Análises Nucleósidas dominou a maior parcela de receita de mercado de aproximadamente 38,6% em 2025, impulsionada pela sua eficácia bem estabelecida contra HIV, hepatite B & C e COVID-19. Essas APIs são amplamente utilizadas em terapias combinadas e são preferidas devido à atividade antiviral de amplo espectro, farmacocinética previsível e alta compatibilidade com outros agentes antivirais. A forte adoção por empresas farmacêuticas, hospitais e institutos de pesquisa, juntamente com investimentos contínuos em P&D e quadros regulatórios favoráveis, apoia a dominância. A disponibilidade de formulações genéricas, programas antivirais apoiados pelo governo e a demanda global de pacientes aumentam ainda mais a liderança no mercado. O aumento da capacidade de produção e as colaborações estratégicas entre os principais fabricantes continuam a fortalecer este segmento.

Espera-se que o segmento Inibidor Integrase testemunhe o CAGR mais rápido de 18,9% de 2026 a 2033, alimentado pelo aumento do uso na terapia anti-HIV e inclusão crescente em esquemas de combinação. Essas APIs são altamente eficazes no bloqueio da replicação viral, particularmente em cepas resistentes ao HIV. O segmento beneficia de ensaios clínicos em curso, financiamento do governo e adoção crescente em mercados emergentes. A expansão das drogas de pipeline, o aumento da demanda por terapias direcionadas e os investimentos globais em antivirais baseados em genes contribuem para uma rápida expansão do mercado. Aumentar a sensibilização dos prestadores de cuidados de saúde e dos doentes, bem como melhorar o acesso nas regiões em desenvolvimento, acelera ainda mais o crescimento.

• Por Aplicação

Com base na aplicação, o mercado de API Antiviral é segmentado em HIV, Hepatite B & C, Influenza, COVID-19, Herpes e Outros. O segmento HIV representou o maior percentual de receita de mercado de 41,2% em 2025, impulsionado pela demanda sustentada por terapia antirretroviral e inclusão nos programas nacionais de HIV. Terapêuticas combinadas usando análogos nucleósidos, inibidores da protease e NNRTIs fortalecem este segmento. Aumentar a conscientização, políticas favoráveis de reembolso e investimentos continuados das empresas farmacêuticas reforçam ainda mais a dominância. Forte desenvolvimento de dutos, alta conformidade com pacientes e a disponibilidade de centros de tratamento globalmente mantêm a liderança no mercado. O segmento se beneficia de parcerias globais e foco crescente em formulações antirretrovirais de longa duração.

O segmento COVID-19 é projetado para testemunhar o CAGR mais rápido de 22,4% de 2026 a 2033, alimentado pela alta demanda de APIs antivirais visando SARS-CoV-2, protocolos de tratamento de emergência e desenvolvimento de novos medicamentos. Ensaios clínicos em andamento, aprovações regulatórias aceleradas e investimentos em preparação para pandemias estão impulsionando o crescimento. A expansão da fabricação de contratos, o aumento da adoção hospitalar e a crescente necessidade de terapias combinadas contribuem para a rápida captação do mercado. O aumento da produção de medicamentos antivirais, o estoque governamental e as colaborações globais de pesquisa aumentam ainda mais o crescimento do mercado.

• Por Usuário Final

Com base no usuário final, o mercado de APIs antivirais é segmentado em empresas farmacêuticas, organizações de pesquisa de contratos (ORCs), organizações de desenvolvimento de contratos e fabricação (CDMOs), hospitais e institutos de pesquisa. As empresas farmacêuticas dominaram o mercado com uma parcela de receita de 45,7% em 2025, alavancando a produção interna, oleodutos fortes e redes globais de distribuição. Manufatura em larga escala, colaborações estratégicas e investimentos em P&D fortalecem a liderança. Incentivos governamentais, políticas de apoio e expansão em mercados emergentes consolidam ainda mais o domínio. O segmento se beneficia com o aumento da prevalência de doenças virais e maior acessibilidade dos pacientes aos antivirais avançados.

Espera-se que o segmento de CDMOs testemunhe o CAGR mais rápido de 20,1% de 2026 a 2033, impulsionado pela terceirização da produção de API antiviral, aumento da demanda por fabricação de contratos de alta qualidade e expansão da capacidade global de CDMO. As empresas farmacêuticas são cada vez mais parceiras de CDMOs para produção econômica, rápido aumento de escala e acesso a expertise especializada. Expansão em mercados emergentes, aumento de contratos e iniciativas governamentais de apoio aceleram ainda mais o crescimento. A crescente demanda por fabricação de precisão e soluções antivirais personalizadas também impulsiona a adoção de segmentos globalmente.

Análise Regional do Mercado Antiviral API

- A América do Norte dominou o mercado de API antiviral com a maior parcela de receita de aproximadamente 39,2% em 2025, apoiada por infraestrutura farmacêutica avançada, quadros regulatórios fortes, alta demanda por terapias antivirais e a presença de principais fabricantes farmacêuticos

- A região beneficia de investimentos robustos em I&D, uma cadeia de suprimentos tecnologicamente avançada e altos gastos em saúde, permitindo a produção e distribuição eficientes de APIs antivirais

- Colaborações estratégicas entre empresas de biotecnologia e farmacêutica, financiamento do governo e integração de tecnologias inovadoras de fabricação reforçam ainda mais a posição do mercado

U.S. Antiviral API Market Insight

O mercado de API antiviral dos EUA capturou a maior participação de receita na América do Norte em 2025, impulsionada pela rápida adoção de formulações antivirais inovadoras, pela crescente prevalência de doenças virais e pelo forte apoio do governo à pesquisa farmacêutica. A alta demanda por terapias antivirais avançadas em hospitais, institutos de pesquisa e empresas farmacêuticas impulsiona ainda mais o crescimento do mercado. Os EUA se beneficiam de uma base de fabricação farmacêutica bem estabelecida, infraestrutura de ensaios clínicos de ponta e lançamento contínuo de produtos. Além disso, o aumento das exportações de APIs antivirais e parcerias estratégicas com CDMOs reforça sua posição de liderança no mercado regional.

Europa Antiviral API Market Insight

Espera-se que o mercado europeu de API antiviral se expanda em um CAGR substancial durante o período de previsão, alimentado por supervisão regulatória rigorosa, aumento da demanda por terapias antivirais eficazes e ênfase na medicina de precisão. O Reino Unido dominou o mercado europeu com a maior quota de receita em 2025, apoiada por infra-estrutura de pesquisa clínica bem estabelecida, financiamento do governo para as ciências da vida, e forte adoção de terapias genéticas e celulares. Aumentar os investimentos das empresas farmacêuticas na produção de API antiviral, iniciativas de pesquisa avançadas e crescente foco na preparação de pandemias contribuem para a liderança do mercado.

Alemanha Antiviral API Market Insight

Espera-se que o mercado de API antiviral da Alemanha testemunhe o CAGR mais rápido de aproximadamente 15,8% de 2026 a 2033, impulsionado pelo aumento dos investimentos em biotecnologia e farmacêutica, expansão de ensaios clínicos e crescente demanda por APIs antivirais de alta qualidade. Forte foco na inovação, apoio regulatório para terapias avançadas e colaborações com CDMOs aceleram o crescimento. As iniciativas de medicina de precisão do país e a infraestrutura de pesquisa de alta qualidade tornam-no um polo atraente para o desenvolvimento de API antiviral.

Visão de mercado da API antiviral Ásia-Pacífico

Espera-se que o mercado de API antiviral Ásia-Pacífico seja a região de crescimento mais rápido, com um CAGR projetado de aproximadamente 24% de 2026 a 2033, impulsionado pelo aumento dos investimentos em saúde, expansão das capacidades de fabricação de APIs na China e Índia, políticas governamentais de apoio e crescente demanda por medicamentos terapêuticos controlados. A rápida urbanização, o crescimento das populações de classe média e o aumento da prevalência de doenças virais apoiam a expansão do mercado.

China Antiviral API Market Insight

O mercado de API antiviral da China representou a maior parte de receita de mercado da região em 2025, alimentada por capacidades de fabricação doméstica, políticas governamentais favoráveis e forte investimento em P&D por empresas farmacêuticas locais. A China tornou-se um centro chave para a produção de API antiviral, apoiado por ensaios clínicos em larga escala e fabricação econômica.

Índia Antiviral API Market Insight

Espera-se que o mercado de API antiviral da Índia testemunhe um crescimento robusto, apoiado pelo aumento da pesquisa clínica, aumento da terceirização da fabricação de API antiviral e iniciativas governamentais que promovam a biotecnologia e a inovação farmacêutica. Quadros regulamentares favoráveis, produção rentável e um crescente mercado de exportação farmacêutica aceleram ainda mais o crescimento.

Antiviral API Market Share

A indústria Antiviral API é liderada principalmente por empresas bem estabelecidas, incluindo:

- Ciências de Gileade (EUA)

- Pfizer Inc. (EUA)

- Merck & Co., Inc. (EUA)

- GSK (UK)

- Roche Holding AG (Suíça)

- Johnson & Johnson (EUA)

- AbbVie Inc. (EUA)

- Bristol- Myers Squibb (EUA)

- Teva Pharmaceutical Industries Ltd (Israel)

- Aurobindo Pharma (Índia)

- Cipla Ltd. (Índia)

- Hetero Labs Ltd. (Índia)

- Laboratórios do Dr. Reddy (Índia)

- Zhejiang Huahai Pharmaceutical (China)

- Grupo Farmacêutico da CSPC (China)

- Shanghai Fosun Pharmaceutical (China)

- Sun Pharmaceutical Industries Ltd. (Índia)

- Lupin Limited (Índia)

- Chugai Pharmaceutical Co., Ltd. (Japão)

- Boehringer Ingelheim (Alemanha)

Mais recentes desenvolvimentos no mercado global de API antiviral

- Em março de 2024, Cipla anunciou a aquisição de uma instalação de fabricação de API antiviral de médio porte na Índia para impulsionar a produção de API HCl valaciclovir e garantir o fornecimento de seu portfólio antiviral genérico. Esta aquisição ajuda a empresa a expandir a capacidade e melhorar a resiliência da cadeia de suprimentos para o tratamento de herpes e infecções virais relacionadas, refletindo crescente demanda e consolidação da fabricação no espaço API antiviral

- Em maio de 2024, Sandoz anunciou uma parceria estratégica com a Lupin para co-desenvolver e fabricar API valaciclovir para mercados globais, visando ampliar a produção e reduzir o tempo de chumbo para este ingrediente antiviral amplamente utilizado. A colaboração reforça o crescente foco da indústria na expansão da capacidade e melhoria do acesso a APIs antivirais essenciais

- Em junho de 2024, a Sun Pharmaceutical Industries lançou uma API HCl valaciclovir de alta pureza destinada aos mercados dos EUA e da UE, sinalizando uma mudança para ofertas especiais de API antiviral e atendendo aos padrões de qualidade exigidos pelos sistemas avançados de saúde. Este lançamento suporta uma maior disponibilidade de terapias antivirais para infecções virais, incluindo herpes

- Em dezembro de 2024, Zydus Cadila anunciou a aquisição de um fabricante especial de API para expandir sua capacidade de API antiviral, incluindo produção de API ganciclovir. Esta aquisição reforça a posição da Zydus no mercado de API antiviral e aumenta a sua capacidade de atender à procura global de tratamento do citomegalovírus e outras doenças virais

- Em fevereiro de 2025, Fresenius Kabi garantiu um grande contrato para fornecer API ganciclovir a uma rede hospitalar europeia, marcando uma expansão significativa de sua pegada comercial API antiviral e reforçando os elos da cadeia de suprimentos entre fabricantes e instituições de saúde

- Em março de 2025, a Cipla anunciou uma colaboração estratégica com a Hetero Labs para expandir a capacidade de fabricação de APIs entecavir e garantir o fornecimento global a longo prazo, refletindo esforços contínuos para fortalecer a produção de APIs antivirais chave para o tratamento da hepatite B

SKU-

Obtenha acesso online ao relatório sobre a primeira nuvem de inteligência de mercado do mundo

- Painel interativo de análise de dados

- Painel de análise da empresa para oportunidades de elevado potencial de crescimento

- Acesso de analista de pesquisa para personalização e customização. consultas

- Análise da concorrência com painel interativo

- Últimas notícias, atualizações e atualizações Análise de tendências

- Aproveite o poder da análise de benchmark para um rastreio abrangente da concorrência

Metodologia de Investigação

A recolha de dados e a análise do ano base são feitas através de módulos de recolha de dados com amostras grandes. A etapa inclui a obtenção de informações de mercado ou dados relacionados através de diversas fontes e estratégias. Inclui examinar e planear antecipadamente todos os dados adquiridos no passado. Da mesma forma, envolve o exame de inconsistências de informação observadas em diferentes fontes de informação. Os dados de mercado são analisados e estimados utilizando modelos estatísticos e coerentes de mercado. Além disso, a análise da quota de mercado e a análise das principais tendências são os principais fatores de sucesso no relatório de mercado. Para saber mais, solicite uma chamada de analista ou abra a sua consulta.

A principal metodologia de investigação utilizada pela equipa de investigação do DBMR é a triangulação de dados que envolve a mineração de dados, a análise do impacto das variáveis de dados no mercado e a validação primária (especialista do setor). Os modelos de dados incluem grelha de posicionamento de fornecedores, análise da linha de tempo do mercado, visão geral e guia de mercado, grelha de posicionamento da empresa, análise de patentes, análise de preços, análise da quota de mercado da empresa, normas de medição, análise global versus regional e de participação dos fornecedores. Para saber mais sobre a metodologia de investigação, faça uma consulta para falar com os nossos especialistas do setor.

Personalização disponível

A Data Bridge Market Research é líder em investigação formativa avançada. Orgulhamo-nos de servir os nossos clientes novos e existentes com dados e análises que correspondem e atendem aos seus objetivos. O relatório pode ser personalizado para incluir análise de tendências de preços de marcas-alvo, compreensão do mercado para países adicionais (solicite a lista de países), dados de resultados de ensaios clínicos, revisão de literatura, mercado remodelado e análise de base de produtos . A análise de mercado dos concorrentes-alvo pode ser analisada desde análises baseadas em tecnologia até estratégias de carteira de mercado. Podemos adicionar quantos concorrentes necessitar de dados no formato e estilo de dados que procura. A nossa equipa de analistas também pode fornecer dados em tabelas dinâmicas de ficheiros Excel em bruto (livro de factos) ou pode ajudá-lo a criar apresentações a partir dos conjuntos de dados disponíveis no relatório.