Global Battery Materials Market

Tamanho do mercado em biliões de dólares

CAGR :

%

USD

61.86 Billion

USD

141.22 Billion

2025

2033

USD

61.86 Billion

USD

141.22 Billion

2025

2033

| 2026 –2033 | |

| USD 61.86 Billion | |

| USD 141.22 Billion | |

| % | |

|

Segmentação de Mercado de Materiais de Bateria Global, Por Tipo de Material (Catódio, Anodo, Eletrolítico, Separador e Outros), Tipo de Bateria (Lítio-Ião, Ácido de Chumbo, Hidrido de Metal de Nickel (NiMH), Cádmio de Nickel (Ni-Cd) e Outros), Aplicação (Dispositivos Portáveis, Automotivo, Itens Eletrônicos, Armazenamento de Energia e Outros) - Tendências e Previsão da Indústria para 2033

Tamanho do mercado de materiais da bateria

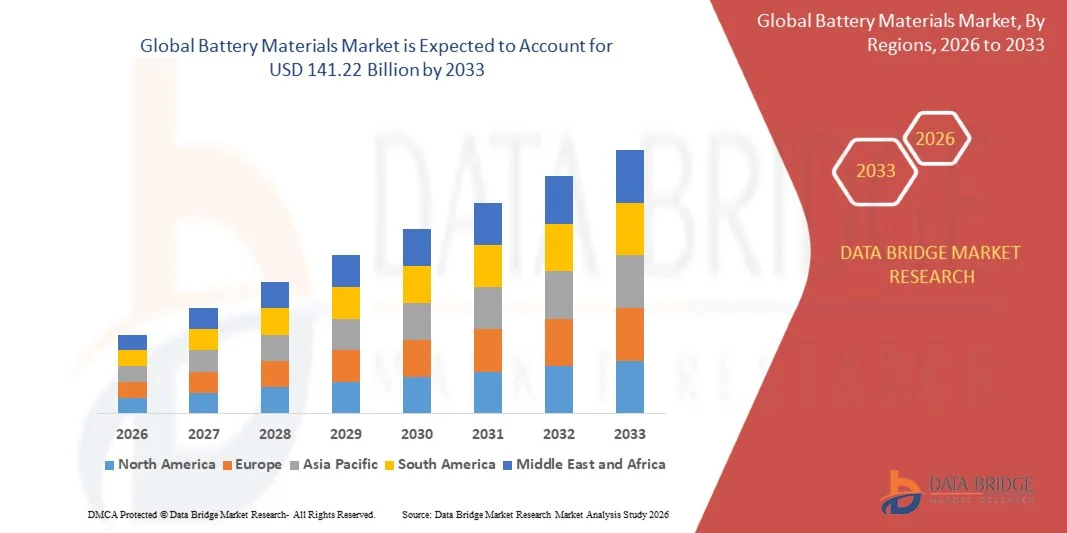

- A dimensão global do mercado de materiais para bateria foi avaliada em61,86 mil milhões de USD em 2025e espera-se alcançarUSD 141,22 mil milhões até 2033, em umaCAGR de 10,87%durante o período de previsão

- O crescimento do mercado é amplamente alimentado pela rápida adoção de veículos elétricos, sistemas de armazenamento de energia renovável e dispositivos eletrônicos portáteis, que estão impulsionando forte demanda por materiais de bateria de alto desempenho, como cátodos, ânodos e eletrólitos

- Além disso, o aumento dos investimentos em tecnologias de bateria de última geração, incluindo cátodos de níquel, ânodos de silício e eletrólitos de estado sólido, estão aumentando a densidade energética, durabilidade e segurança, acelerando a adoção e produção de materiais avançados de bateria, aumentando significativamente o crescimento da indústria.

Análise do Mercado de Materiais de Bateria

- Materiais de bateria, incluindo cátodo, anodo, eletrólito e componentes separadores, são fundamentais para o desempenho, eficiência e longevidade de iões de lítio, à base de níquel e outras baterias químicas usadas em aplicações automotivas, eletrônicas e de armazenamento de energia

- A crescente demanda por materiais de bateria é principalmente alimentada pela mudança global para a mobilidade elétrica, aumentando a penetração da eletrônica de consumo e crescente foco na integração de energias renováveis, juntamente com crescentes investimentos em pesquisa e desenvolvimento para melhorar o desempenho e sustentabilidade do material

- Ásia-Pacífico domina o mercado de materiais de bateria em 2025, devido à rápida adoção de veículos elétricos, ampliação da produção de eletrônicos de consumo, e uma forte presença de hubs de fabricação de material de bateria

- Espera-se que a América do Norte seja a região de crescimento mais rápido no mercado de materiais de bateria durante o período de previsão devido ao aumento da adoção de EV, expansão de sistemas de armazenamento de energia renovável e demanda robusta por lítio-ion e baterias avançadas

- O segmento Lítio-Ion dominou o mercado com uma quota de mercado de 55,5% em 2025, devido à sua alta densidade energética, longa vida útil e versatilidade em aplicações de eletrônicos de consumo, veículos elétricos e armazenamento de energia. O segmento beneficia de um forte investimento em pesquisa e produção por fabricantes de baterias chave, permitindo melhorias contínuas de desempenho e reduções de custos. Baterias de íon de lítio são favorecidas em dispositivos portáteis e setores automotivos devido ao seu design leve e capacidade de carregamento rápido

Denunciar Escopo e Segmentação de Mercado de Materiais de Bateria

| Atributos | Materiais da bateria Principais perspectivas do mercado |

| Segmentos Cobertos |

|

| Países abrangidos | América do Norte

Europa

Ásia- Pacífico

Médio Oriente e África

América do Sul

|

| Jogadores do mercado chave |

|

| Oportunidades de Mercado |

|

| Informações sobre o Valor Adicionado | Além dos insights sobre cenários de mercado, como valor de mercado, taxa de crescimento, segmentação, cobertura geográfica e principais atores, os relatórios de mercado curados pela Data Bridge Market Research também incluem análise de importação, visão geral da capacidade de produção, análise do consumo de produção, análise de tendências de preços, cenário de mudança climática, análise da cadeia de suprimentos, análise da cadeia de valor, visão geral da matéria-prima/consumíveis, critérios de seleção de fornecedores, Análise de PESTLE, Análise de Porter e quadro regulatório. |

Tendências do mercado de materiais de bateria

“Demanda crescente para materiais de bateria de alta densidade energética”

- Uma tendência significativa no mercado de materiais de bateria é a crescente demanda por materiais de alta densidade energética que podem melhorar o desempenho, longevidade e segurança das baterias usadas em veículos elétricos, eletrônicos de consumo e sistemas de armazenamento de energia. Fabricantes e usuários finais estão priorizando materiais que permitem maiores intervalos de condução, carregamento mais rápido e saídas de energia mais altas, impulsionando inovação em tecnologias catódicas, anodas e eletrólitos

- Por exemplo, a CATL está investindo em materiais catódicos NMC ricos em níquel para aumentar a densidade energética em baterias de veículos elétricos, reforçando o desempenho e a competitividade de seu portfólio de baterias EV. Tais materiais são essenciais para satisfazer as expectativas crescentes dos consumidores de baterias de alta capacidade e de longa duração

- A adoção de ânodos avançados à base de silício está aumentando rapidamente, pois permitem maiores capacidades e ciclos de carga mais rápidos, posicionando esses materiais como facilitadores críticos de baterias de iões de lítio de última geração

- Os fabricantes de baterias estão focando em eletrólitos de alta tensão e alta estabilidade que melhoram a eficiência da bateria e o gerenciamento térmico, especialmente em condições extremas de operação

- O setor de energia renovável está impulsionando a procura de soluções de armazenamento de energia que exigem baterias com maior densidade energética para armazenar eletricidade da geração solar e eólica. Isso está incentivando a adoção em larga escala de materiais avançados para aplicações de armazenamento em escala de grade

- A pesquisa e o desenvolvimento em produtos químicos de bateria sólidos e híbridos estão aumentando, apoiados por investimentos de líderes globais como BASF e Umicore, com o objetivo de produzir materiais mais seguros, mais energéticos e duradouros para veículos elétricos e aplicações de armazenamento industrial

Dinâmica do Mercado de Materiais de Bateria

Controlador

“Adoção de veículos elétricos e sistemas de armazenamento de energia”

- A crescente mudança global para mobilidade elétrica e armazenamento de energia renovável está impulsionando a demanda sem precedentes por materiais de bateria de alto desempenho. Esta tendência é apoiada por regulamentos mais rigorosos em matéria de emissões, incentivos governamentais e preferência crescente dos consumidores por soluções sustentáveis de transporte e energia

- Por exemplo, as Gigafactories da Tesla dependem fortemente de materiais avançados de cátodo e anodo fornecidos por empresas como Panasonic e CATL para escalar a produção de baterias EV, permitindo maiores intervalos de condução e capacidades de carregamento mais rápidas. A colaboração estratégica entre montadoras e fornecedores de material de bateria está acelerando a inovação e adoção em todo o setor

- Eletrificação crescente em transportes públicos e frotas comerciais está aumentando a demanda por pacotes de bateria de grande formato que exigem composições de materiais otimizados. Materiais de bateria que fornecem alta densidade de energia e estabilidade térmica são cruciais para atender a esses requisitos operacionais

- O aumento da implantação de sistemas de armazenamento de energia estacionários para aplicações residenciais, comerciais e de utilidades está estimulando ainda mais a demanda por materiais avançados de bateria. Materiais que permitem uma longa vida útil e confiabilidade sob ciclos contínuos de descarga de carga são particularmente valorizados neste segmento

- A integração de materiais de bateria em tecnologias emergentes, como baterias de estado sólido, EVs híbridos e eletrônicos portáteis reforça o driver de mercado, já que os fabricantes buscam soluções que melhorem a eficiência, reduzam o custo e aumentem as taxas de adoção

Restrição/Desafio

“Dependência da cadeia de suprimentos em matérias-primas críticas”

- O mercado de materiais para baterias enfrenta desafios significativos devido à dependência de matérias-primas críticas como lítio, cobalto, níquel e grafite, que estão geograficamente concentradas e sujeitas à volatilidade dos preços. Esta dependência cria riscos de abastecimento e potenciais estrangulamentos na produção de baterias em larga escala

- Por exemplo, Umicore e Zhejiang Huayou Cobalt experimentaram restrições na cadeia de suprimentos impactando a disponibilidade de cobalto para materiais catódicos. Tais interrupções podem aumentar os custos e atrasar os prazos de produção para os fabricantes de baterias

- A extração e o processamento dessas matérias-primas requerem investimento substancial em capital, conformidade regulatória e gestão ambiental, que aumentam a complexidade operacional. Os fabricantes devem navegar por desafios geopolíticos, comerciais e ambientais, garantindo um fornecimento estável de materiais de alta qualidade

- Alta concorrência para matérias-primas entre fabricantes de baterias, fabricantes de EV e empresas eletrônicas podem aumentar os preços e criar incerteza no mercado, impactando margens de lucro e escalabilidade da produção de baterias

- O mercado continua a encontrar restrições relacionadas à reciclagem e reutilização de materiais críticos. Enquanto empresas como a BASF estão avançando tecnologias de reciclagem de baterias, escalar essas soluções para atender à demanda global continua sendo um desafio, aumentando a pressão sobre a cadeia de suprimentos e disponibilidade de materiais

Âmbito de mercado dos materiais da bateria

O mercado é segmentado com base no tipo de material, tipo de bateria e aplicação.

- Por Tipo de Material

Com base no tipo de material, o mercado de materiais de bateria é segmentado em cátodo, anodo, eletrólito, separador, entre outros. O segmento catódico dominou o mercado com a maior participação de receita em 2025, impulsionado pelo seu papel crítico na determinação da densidade de energia da bateria, vida útil e desempenho global. Os fabricantes costumam priorizar materiais cátodo de alta qualidade para baterias de iões de lítio devido ao seu impacto direto na eficiência e segurança da bateria. O mercado vê forte demanda por cátodos avançados como fabricantes de automóveis e eletrônicos buscam soluções de armazenamento de energia de maior duração e maior capacidade. Os materiais catódicos, como o óxido de cobalto de níquel de lítio (NMC) e o fosfato de ferro de lítio (LFP) são amplamente adotados em veículos elétricos e eletrônicos de consumo, cimentando ainda mais o domínio do mercado. Otimização de custos e melhores métodos de produção também aceleraram a adoção na fabricação de baterias em larga escala.

Espera-se que o segmento de anodo testemunhe o crescimento mais rápido de 2026 para 2033, alimentado pelo aumento da pesquisa em anodos híbridos de silício e grafite-silício que aumentam a capacidade da bateria e ciclos de carga. Por exemplo, empresas como a BTR New Energy Materials estão investindo em tecnologias de anodo de última geração para suportar a crescente demanda por baterias de iões de lítio de alto desempenho. A crescente eletrificação do transporte e expansão da eletrônica portátil acionam a necessidade de soluções avançadas de anodo, posicionando este segmento para um crescimento robusto no período de previsão.

- Por Tipo de Bateria

Com base no tipo de bateria, o mercado é segmentado em lítio-ion, chumbo-ácido, níquel-hidreto metálico (NiMH), níquel-cádmio (Ni-Cd), entre outros. O segmento de íon-lítio dominou o mercado com a maior parcela de receita de 55,5% em 2025, impulsionada por sua alta densidade energética, longa vida útil e versatilidade em aplicações de eletrônicos de consumo, veículos elétricos e armazenamento de energia. O segmento beneficia de um forte investimento em pesquisa e produção por fabricantes de baterias chave, permitindo melhorias contínuas de desempenho e reduções de custos. Baterias de íon de lítio são favorecidas em dispositivos portáteis e setores automotivos devido ao seu design leve e capacidade de carregamento rápido. Recursos de segurança aprimorados e sistemas de gerenciamento de baterias em evolução reforçaram ainda mais o domínio do mercado. A adoção crescente de sistemas de armazenamento de energia renovável também apoia a implantação generalizada de tecnologia de lítio-ion.

Espera-se que o segmento de chumbo-ácido testemunhe o crescimento mais rápido de 2026 para 2033, impulsionado pela demanda contínua em baterias de arranque automotivo e armazenamento de energia estacionária. Por exemplo, a Exide Technologies continua inovando em soluções de chumbo-ácido para aplicações industriais e de energia de backup. Os baixos custos de produção do segmento, a reciclagem e a cadeia de abastecimento estabelecida contribuem para o seu potencial de crescimento, particularmente em economias emergentes, onde a eficiência de custo é crítica.

- Por Aplicação

Com base na aplicação, o mercado de materiais de bateria é segmentado em dispositivos portáteis, automotivos, itens eletrônicos, armazenamentos de energia, entre outros. O segmento automotivo dominou o mercado com a maior participação de receita em 2025, impulsionada pela rápida expansão da produção de veículos elétricos e incentivos governamentais que apoiam a adoção da EV. Baterias automotivas exigem materiais de alto desempenho para alcançar maiores faixas de condução, carregamento mais rápido e maior segurança, conduzindo investimentos substanciais em tecnologias de catodo, anodo e eletrólito. Os principais fabricantes de EV, como Tesla e BYD, estão investindo fortemente em produtos químicos avançados e cadeias de suprimentos para garantir materiais de alta qualidade, fortalecendo o domínio do segmento automotivo. O crescente foco na eletrificação de veículos em toda a Europa, América do Norte e Ásia-Pacífico acelera ainda mais o crescimento do mercado.

Espera-se que o segmento de dispositivos portáteis testemunhe o crescimento mais rápido de 2026 para 2033, alimentado pela crescente demanda por smartphones, tablets, laptops e eletrônicos wearable. Por exemplo, a Samsung SDI continua a expandir suas soluções de material de bateria para baterias compactas de iões de lítio de alta capacidade em eletrônicos de consumo. A necessidade de baterias leves, eficientes e de longa duração em aplicações portáteis impulsiona a rápida adoção de materiais avançados de cátodo e ânodo, suportando um forte crescimento neste segmento.

Análise regional do mercado de materiais de bateria

- Asia-Pacific dominou o mercado de materiais de bateria com a maior parte de receita em 2025, impulsionado pela rápida adoção de veículos elétricos, expansão da produção de eletrônicos de consumo, e uma forte presença de hubs de fabricação de materiais de bateria

- O cenário de produção rentável da região, o aumento dos investimentos em iões de lítio e a produção avançada de material de bateria e o aumento das exportações de componentes de bateria de alta qualidade estão acelerando a expansão do mercado

- A disponibilidade de mão-de-obra qualificada, incentivos governamentais favoráveis para projetos de EV e armazenamento de energia e a rápida industrialização em economias em desenvolvimento estão contribuindo para o aumento do consumo de materiais de bateria em setores automotivos, eletrônicos e de armazenamento de energia

China Bateria Materiais Visão do mercado

A China teve a maior participação no mercado de materiais para baterias Ásia-Pacífico em 2025, devido à sua posição como líder global na produção de baterias de iões de lítio e adoção de EV. A forte base industrial do país, a extensa cadeia de suprimentos de matérias-primas para baterias e as políticas governamentais de apoio à energia limpa e à fabricação de EV são os principais fatores de crescimento. A demanda também é reforçada por investimentos contínuos em instalações de produção de catódicos, anodos e eletrólitos para mercados nacionais e internacionais.

Índia Bateria Materiais Visão do Mercado

A Índia está assistindo ao crescimento mais rápido na região Ásia-Pacífico, alimentado pela rápida expansão da adoção de EV, aumento da fabricação de eletrônicos e aumento dos investimentos em infraestrutura de materiais de bateria. Iniciativas governamentais como a Missão Nacional de Mobilidade Elétrica e incentivos à produção doméstica de baterias estão reforçando a demanda por materiais de bateria de alta qualidade. Além disso, o crescimento da I&D em produtos químicos avançados em bateria e o aumento do potencial de exportação de componentes de iões de lítio contribuem para uma expansão robusta do mercado.

Europe Battery Materials Market Insight

O mercado europeu de materiais para baterias está em constante expansão, apoiado por quadros regulatórios rigorosos, a crescente procura de baterias EV de alto desempenho e os crescentes investimentos em soluções sustentáveis de armazenamento de energia. A região enfatiza a conformidade ambiental, design avançado de bateria e fornecimento de materiais de alta qualidade, especialmente para aplicações de armazenamento de energia automotiva e industrial. O crescente enfoque nas práticas de economia circular, incluindo a reciclagem de baterias, está a aumentar ainda mais o crescimento do mercado.

Alemanha Battery Materials Market Insight

O mercado de materiais de bateria da Alemanha é impulsionado pela sua liderança na fabricação de EV, forte patrimônio da indústria química e de materiais e modelo de produção orientado para a exportação. O país tem redes de P&D bem estabelecidas e colaboração entre instituições acadêmicas e fabricantes de materiais de bateria, promovendo inovação contínua em tecnologias de catodo, anodo e eletrólito. A demanda é particularmente forte para uso em baterias de iões de lítio de alta capacidade e aplicações emergentes de baterias de estado sólido.

U.K. Battery Materials Market Insight

O mercado do Reino Unido é suportado por um setor de energia automotiva e limpa maduro, crescentes esforços para localizar cadeias de fornecimento de baterias EV pós-Brexit e crescente demanda por materiais de bateria de alto desempenho. Com foco crescente em I&D, colaboração industrial-acadêmica e investimentos em materiais de bateria da próxima geração, o Reino Unido continua a desempenhar um papel significativo no cenário europeu de materiais de bateria.

América do Norte Bateria Materiais Visão do mercado

A América do Norte é projetada para crescer no CAGR mais rápido de 2026 para 2033, impulsionado pelo aumento da adoção de EV, expansão de sistemas de armazenamento de energia renovável, e demanda robusta para lítio-ion e baterias avançadas. Forte foco na inovação tecnológica, incentivos governamentais para energia limpa e parcerias entre OEMs automotivos e fabricantes de materiais de bateria estão aumentando a demanda. Além disso, o reabastecimento da produção de baterias e os investimentos estratégicos no fornecimento de materiais estão apoiando a expansão do mercado.

U.S. Battery Materials Market Insight

Os EUA representaram a maior parte do mercado da América do Norte em 2025, apoiada pelo seu extenso mercado EV, forte infraestrutura de P&D e investimento significativo na produção de material de bateria. A ênfase do país na sustentabilidade, conformidade regulatória e inovação está incentivando a adoção de materiais catódicos, anodos e eletrólitos de alta qualidade para aplicações de armazenamento automotivo e energético. Presença de fabricantes líderes de baterias e uma rede de distribuição madura solidificar ainda mais a posição líder dos EUA na região.

Partilha de Mercado de Materiais de Bateria

A indústria de materiais para bateria é liderada principalmente por empresas bem estabelecidas, incluindo:

- Materiais Umicore Cobalt & Specialty (CSM) (Bélgica)

- NEI Corporation (U.K.)

- Shanghai Shanshan Technology Co., Ltd. (China)

- Ningbo Ronbay New Energy Technology Co., Ltd. (China)

- Asahi Kasei Corporation (Japão)

- Hitachi Energy Ltd. (Suíça)

- CNGR Advanced Material Co., Ltd. (China)

- Zhejiang Huayou Cobalt Co., Ltd. (China)

- NIQUIA CORPORATION (Japão)

- Gotion High-Tech Co., Ltd (China)

- Mitsubishi Chemical Corporation (Japão)

- Kureha Corporation (Japão)

- BASF SE (Alemanha)

- Tokyo Chemical Industry Co Ltd (Japão)

- POSCO Future M Co., Ltd. (Coreia do Sul)

- INDÚSTRIAS DE TORAÇO, INC. (Japão)

Mais recentes desenvolvimentos no mercado global de materiais para baterias

- Em novembro de 2025, a LG Chem e a Sinopec celebraram um acordo estratégico de desenvolvimento conjunto para avançar os principais materiais catódicos e anodos para baterias de sódio. Esta colaboração tem por objectivo acelerar a comercialização da tecnologia de iões de sódio como alternativa ao lítio, que pode diversificar a paisagem dos materiais de bateria. Ao desenvolver materiais eficientes e de alto desempenho de íons de sódio, espera-se que a parceria amplie as capacidades de produção, reduza a dependência de lítio e crie novas oportunidades em armazenamento de energia e aplicações de veículos elétricos, potencialmente reformulando a dinâmica de demanda de materiais na indústria

- Em novembro de 2025, Nouveau Monde Graphite Inc. (NMG) atualizou seu acordo comercial multiano com a Panasonic Energy para promover a produção ativa de material anodo. A empresa planeja dedicar a capacidade de produção inicial em operações da Fase-2 e garantiu acordos de compra vinculativos para volumes futuros. Este desenvolvimento reforça a segurança da cadeia de suprimentos para materiais de anodos críticos, suporta a escala de produção para atender à crescente demanda de EV e armazenamento de energia, e permite materiais de maior qualidade e mais consistentes, reforçando a competitividade dos fabricantes de baterias globalmente

- Em dezembro de 2024, a China Contemporary Amperex Technology Co. Limited (CATL) começou a fornecer suporte financeiro a seus fornecedores de materiais e equipamentos de bateria para impulsionar a inovação tecnológica e fortalecer sua cadeia de suprimentos. Esta iniciativa foi projetada para aliviar a pressão em meio à intensa concorrência de preços EV e garantir o fornecimento de material ininterrupta. Ao apoiar fornecedores a montante, a CATL está incentivando o desenvolvimento mais rápido de materiais avançados de cátodo, ânodo e eletrólito, melhorando a eficiência de produção e reduzindo os custos, o que aumenta sua liderança de mercado em materiais globais de baterias

- Em junho de 2024, Asahi Kasei obteve prova de conceito para baterias de lítio-ion usando seu eletrólito condutor de alta iônica proprietário. A nova tecnologia melhora a durabilidade da bateria em altas temperaturas e a potência a baixas temperaturas, permitindo pacotes de bateria menores e menores custos. Este avanço aborda diretamente os principais desafios de desempenho e densidade de energia dos LIBs atuais, apoiando a adoção mais ampla em aplicações de armazenamento automotivo, portátil e de energia, e posicionando a empresa para fornecer materiais de bateria mais eficientes e competitivos no mercado

- Em abril de 2024, a BASF iniciou operações de sua refinaria de metal protótipo para reciclagem de baterias em Schwarzheide, Alemanha. Esta instalação centra-se na otimização de tecnologias de reciclagem inovadoras para baterias de iões de lítio em fim de vida e sucata de produção. Ao recuperar e reprocessamento de metais valiosos, como lítio, níquel e cobalto, a iniciativa da BASF contribui para a circularidade do material, reduz a dependência de matérias-primas virgens e suporta a produção de baterias sustentáveis, o que é fundamental para atender à crescente demanda em EVs e armazenamento de energia

SKU-

Obtenha acesso online ao relatório sobre a primeira nuvem de inteligência de mercado do mundo

- Painel interativo de análise de dados

- Painel de análise da empresa para oportunidades de elevado potencial de crescimento

- Acesso de analista de pesquisa para personalização e customização. consultas

- Análise da concorrência com painel interativo

- Últimas notícias, atualizações e atualizações Análise de tendências

- Aproveite o poder da análise de benchmark para um rastreio abrangente da concorrência

Metodologia de Investigação

A recolha de dados e a análise do ano base são feitas através de módulos de recolha de dados com amostras grandes. A etapa inclui a obtenção de informações de mercado ou dados relacionados através de diversas fontes e estratégias. Inclui examinar e planear antecipadamente todos os dados adquiridos no passado. Da mesma forma, envolve o exame de inconsistências de informação observadas em diferentes fontes de informação. Os dados de mercado são analisados e estimados utilizando modelos estatísticos e coerentes de mercado. Além disso, a análise da quota de mercado e a análise das principais tendências são os principais fatores de sucesso no relatório de mercado. Para saber mais, solicite uma chamada de analista ou abra a sua consulta.

A principal metodologia de investigação utilizada pela equipa de investigação do DBMR é a triangulação de dados que envolve a mineração de dados, a análise do impacto das variáveis de dados no mercado e a validação primária (especialista do setor). Os modelos de dados incluem grelha de posicionamento de fornecedores, análise da linha de tempo do mercado, visão geral e guia de mercado, grelha de posicionamento da empresa, análise de patentes, análise de preços, análise da quota de mercado da empresa, normas de medição, análise global versus regional e de participação dos fornecedores. Para saber mais sobre a metodologia de investigação, faça uma consulta para falar com os nossos especialistas do setor.

Personalização disponível

A Data Bridge Market Research é líder em investigação formativa avançada. Orgulhamo-nos de servir os nossos clientes novos e existentes com dados e análises que correspondem e atendem aos seus objetivos. O relatório pode ser personalizado para incluir análise de tendências de preços de marcas-alvo, compreensão do mercado para países adicionais (solicite a lista de países), dados de resultados de ensaios clínicos, revisão de literatura, mercado remodelado e análise de base de produtos . A análise de mercado dos concorrentes-alvo pode ser analisada desde análises baseadas em tecnologia até estratégias de carteira de mercado. Podemos adicionar quantos concorrentes necessitar de dados no formato e estilo de dados que procura. A nossa equipa de analistas também pode fornecer dados em tabelas dinâmicas de ficheiros Excel em bruto (livro de factos) ou pode ajudá-lo a criar apresentações a partir dos conjuntos de dados disponíveis no relatório.