North America Wound Closure Devices Market

Tamanho do mercado em biliões de dólares

CAGR :

%

USD

15.18 Billion

USD

26.45 Billion

2024

2032

USD

15.18 Billion

USD

26.45 Billion

2024

2032

| 2025 –2032 | |

| USD 15.18 Billion | |

| USD 26.45 Billion | |

| % | |

|

North America Wound Closure Devices Market, By Device (Adhesives, Staples, Sutures, Mechanical Devices), Application (Burns, Ulcer, Surgical Wounds, Pressure Ulcers, Diabetic Ulcers, Arterial Ulcers), Type of Wound (Acute Wound, Chronic Wound), End User (Hospitals, Community Healthcare Service Providers, Ambulatory Surgical Centers, Home Care), Country (U.S., Canada, Mexico) Industry Trends and Forecast to 2032.

Wound Closure Devices Market Size

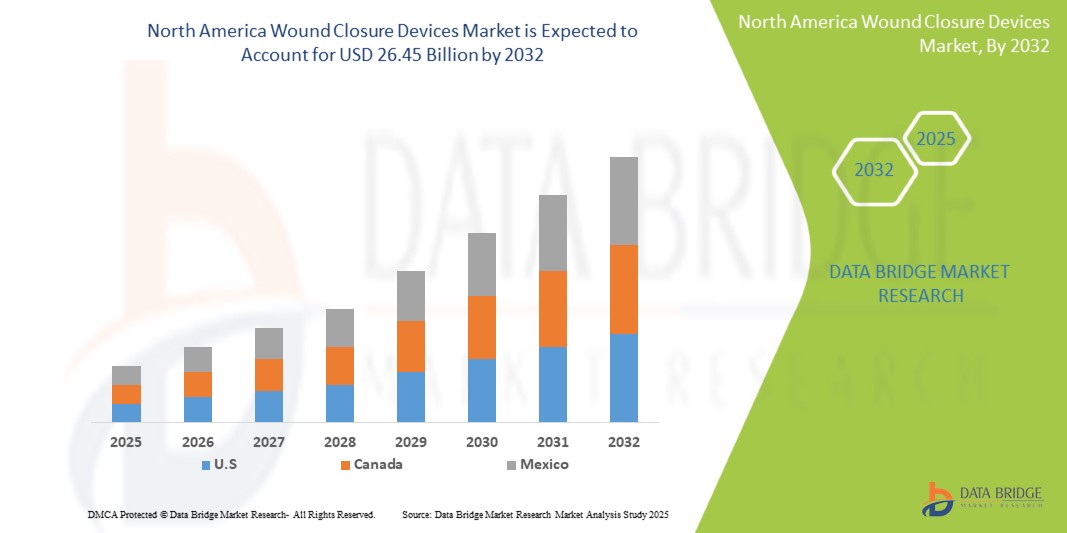

- The North America Wound Closure Devices Market size was valued atUSD 15.18 Billion in 2024and is expected to reachUSD 26.45 Billion by 2032, at aCAGR of 6.49%during the forecast period

- This growth is driven by factors such as the rising number of surgical procedures, increasing incidence of chronic wounds, and technological advancements in wound closure devices.

Wound Closure Devices Market Analysis

- Active wound care products play a critical role in enhancing the wound healing process by supporting cellular activity and tissue regeneration, particularly in chronic and non-healing wounds

- The demand for these products is driven by the increasing prevalence of chronic wounds, growing geriatric population, and rising awareness about advanced wound management solutions

- U.S. is expected to dominate the Active and Advanced Wound Care market due to its strong healthcare infrastructure, high healthcare expenditure, and increasing adoption of innovative wound care therapies

- U.S. is also projected to be the fastest-growing market during the forecast period due to the surge in diabetic foot ulcers, supportive reimbursement policies, and growing investments in wound care R&D

- The Advanced Dressings segment is expected to lead the market with a significant share due to their effectiveness in moisture retention, infection prevention, and acceleration of the healing process in complex wounds

Report Scope andWound Closure Devices Market Segmentation

|

Attributes |

Wound Closure Devices KeyMarket Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Wound Closure Devices Market Trends

“Rising Prevalence of Chronic and Surgical Wounds”

- The increasing incidence of chronic wounds, such as diabetic foot ulcers and pressure ulcers, is driving demand for effective closure devices to accelerate healing, minimize infection risk, and reduce hospital stays, especially among the aging population.

- Surgical procedures are rising due to a growing elderly population and lifestyle-related diseases. Post-surgical wound management is critical, and advanced closure devices are essential to support quick recovery and minimize complications like infections and dehiscence.

- Patients suffering from obesity or compromised immune systems face more complications in wound healing. This necessitates innovative closure solutions that offer superior sealing, minimal trauma, and improved outcomes, thereby fueling the adoption of advanced wound closure devices.

Wound Closure Devices Market Dynamics

Driver

Technological Advancements in Closure Techniques

- Emerging technologies such as absorbable staples, bioengineered adhesives, and antimicrobial sutures provide efficient, less invasive wound closure options. These innovations enhance clinical outcomes and patient comfort, encouraging wider use in both hospitals and outpatient settings.

- The integration of wound closure devices with digital monitoring tools enables real-time assessment of healing progress. This improves treatment strategies, reduces readmissions, and supports better decision-making among healthcare professionals, promoting adoption across North America.

- Minimally invasive surgical procedures are increasingly popular, necessitating equally advanced wound closure devices. These tools allow quicker recovery times, reduced scarring, and better cosmetic results, meeting rising patient and provider expectations for high-quality care.

For Instance,

Emerging technologies in wound closure, such as absorbable staples, bioengineered adhesives, and antimicrobial sutures, provide efficient, less invasive options, enhancing clinical outcomes and patient comfort. The integration of digital monitoring tools allows real-time healing assessments, promoting better decision-making and adoption of advanced closure devices in minimally invasive surgeries across North America.

Opportunity

“Rising Ambulatory Surgical Centers (ASCs) and Homecare Trends”

- With the shift toward cost-effective healthcare, Ambulatory Surgical Centers are on the rise. These facilities favor wound closure solutions that are quick to apply, easy to monitor, and adaptable to same-day procedures, offering growth potential for manufacturers.

- The expansion of home healthcare services allows for increased use of user-friendly wound closure devices. Devices like skin adhesives and adhesive strips, which require minimal medical supervision, are in demand among homecare patients across North America.

- Remote patient monitoring combined with easy-to-use closure technologies creates an opportunity for manufacturers to develop smart, self-applicable closure systems. These innovations align with the growing preference for decentralized and patient-centric healthcare delivery models.

For Instance,

- The rise of Ambulatory Surgical Centers (ASCs) is driving demand for quick and adaptable wound closure solutions suited for same-day procedures, presenting growth opportunities for manufacturers. Concurrently, home healthcare services favor user-friendly devices, like skin adhesives, while remote monitoring promotes the development of smart, self-applicable systems, aligning with decentralized healthcare trends.

Restraint/Challenge

“Regulatory Hurdles and Reimbursement Constraints”

- Strict regulatory pathways for approval of wound closure devices in the U.S. and Canada can delay market entry. Developers face rigorous testing and documentation requirements, increasing time-to-market and development costs.

- Reimbursement limitations for newer wound closure technologies restrict hospital and clinic adoption. Without adequate insurance coverage, healthcare providers may be reluctant to switch from traditional methods, hindering widespread deployment of innovative solutions.

- Navigating varying state-level reimbursement rules in the U.S. adds complexity for manufacturers. Inconsistent policies between regions impact market penetration and create operational challenges, especially for small and mid-sized device developers.

For Instance,

- Strict regulatory pathways in the U.S. and Canada delay market entry for wound closure devices due to rigorous testing and documentation requirements. Additionally, reimbursement limitations hinder the adoption of innovative technologies in hospitals and clinics. Varying state-level reimbursement rules further complicate market penetration for small and mid-sized manufacturers, impacting growth.

Wound Closure Devices Market Scope

The market is segmented on the basis By Device, Application, Type of Wound, End User.

|

Segmentation |

Sub-Segmentation |

|

By Device |

|

|

Application |

|

|

Type of Wound

|

|

|

End User |

|

In 2025, theAdhesives is projected to dominate the market with a largest share in application segment

The Adhesives segment is expected to dominate the Wound Closure Devices market with the largest share of 48.38% in 2024 due to increasing demand for non-invasive, easy-to-use wound closure solutions. As a critical component in both surgical and trauma care, advancements in adhesive strength, flexibility, and biocompatibility have significantly improved clinical outcomes and patient comfort. The rising volume of surgical procedures, growing preference for minimally invasive techniques, and increasing healthcare awareness further contribute to the segment’s market dominance.

TheStaples is expected to account for the largest share during the forecast period in technology market

In 2025, the Staples segment is expected to dominate the Wound Closure Devices market with the largest market share of 48.38% due to their efficiency, speed of application, and effectiveness in closing large or complex wounds. As a vital component in surgical wound management, advancements in stapler design, material safety, and precision delivery systems have improved procedural outcomes and reduced operative time. The increasing number of surgical interventions, rising demand for reliable closure methods, and growing adoption of technology-driven surgical tools further contribute to the segment’s market dominance.

Wound Closure Devices Market Regional Analysis

“U.S Holds the Largest Share and highest CAGR in theWound Closure DevicesMarket”

- U.S. dominates and highest CAGR the Wound Closure Devices market, driven by advanced healthcare infrastructure, high volume of surgical procedures, and strong presence of key market players

- The U.S. holds a significant share due to increased demand for minimally invasive wound closure solutions, rising incidence of chronic wounds, and growing preference for faster recovery options

- The availability of well-established reimbursement policies and growing investments in surgical innovation by leading medical device companies further strengthen the market

- In addition, the increasing shift toward outpatient surgeries, integration of smart wound care technologies, and the rising elderly population are fueling market expansion across the region

Wound Closure Devices Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Johnson & Johnson Services, Inc. (U.S.)

- Medtronic (Ireland)

- 3M (U.S.)

- Smith+Nephew (U.K.)

- B. Braun SE (Germany)

- Stryker (U.S.)

- Baxter (U.S.)

- Boston Scientific Corporation (U.S.)

- Frankenman International Ltd. (China)

- CooperSurgical Inc. (U.S.)

- Intuitive Surgical (U.S.)

- MANI, INC. (Japan)

- Artivion, Inc. (U.S.)

- CP Medical (Riverpoint Medical) (U.S.)

- CONMED Corporation (U.S.)

- Genesis Medtech (Singapore)

- Cardinal Health, Inc. (U.S.)

- Essity AB (Sweden)

- Medline Industries, LP (U.S.)

Latest Developments in North America Wound Closure Devices Market

- In June 2021, Ethicon Plus sutures were the first to be approved for use in the NHS by NICE Medical Technologies Guidance as they have been demonstrated to lower the possibility of surgical site infections (SSIs) by over 30%.

- In November 2020, Trubarb, a knotless tissue closure device launched by Healthium, is an efficacious triangular end stopper that removes the need for knotting as compared to a normal suture.

- In March 2020, LiquiBand Plus, developed by Advanced Medical Solutions Limited, was approved by the FDA to heal readily approximated skin margins of wounds after surgical incisions.

- In February 2020, Wego-Stainless Steel suture was approved by the FDA for applications such as abdominal wound closure, hernia repair, and sternal closure by Foosin Medical Supplies Inc., Ltd

SKU-

Obtenha acesso online ao relatório sobre a primeira nuvem de inteligência de mercado do mundo

- Painel interativo de análise de dados

- Painel de análise da empresa para oportunidades de elevado potencial de crescimento

- Acesso de analista de pesquisa para personalização e customização. consultas

- Análise da concorrência com painel interativo

- Últimas notícias, atualizações e atualizações Análise de tendências

- Aproveite o poder da análise de benchmark para um rastreio abrangente da concorrência

Metodologia de Investigação

A recolha de dados e a análise do ano base são feitas através de módulos de recolha de dados com amostras grandes. A etapa inclui a obtenção de informações de mercado ou dados relacionados através de diversas fontes e estratégias. Inclui examinar e planear antecipadamente todos os dados adquiridos no passado. Da mesma forma, envolve o exame de inconsistências de informação observadas em diferentes fontes de informação. Os dados de mercado são analisados e estimados utilizando modelos estatísticos e coerentes de mercado. Além disso, a análise da quota de mercado e a análise das principais tendências são os principais fatores de sucesso no relatório de mercado. Para saber mais, solicite uma chamada de analista ou abra a sua consulta.

A principal metodologia de investigação utilizada pela equipa de investigação do DBMR é a triangulação de dados que envolve a mineração de dados, a análise do impacto das variáveis de dados no mercado e a validação primária (especialista do setor). Os modelos de dados incluem grelha de posicionamento de fornecedores, análise da linha de tempo do mercado, visão geral e guia de mercado, grelha de posicionamento da empresa, análise de patentes, análise de preços, análise da quota de mercado da empresa, normas de medição, análise global versus regional e de participação dos fornecedores. Para saber mais sobre a metodologia de investigação, faça uma consulta para falar com os nossos especialistas do setor.

Personalização disponível

A Data Bridge Market Research é líder em investigação formativa avançada. Orgulhamo-nos de servir os nossos clientes novos e existentes com dados e análises que correspondem e atendem aos seus objetivos. O relatório pode ser personalizado para incluir análise de tendências de preços de marcas-alvo, compreensão do mercado para países adicionais (solicite a lista de países), dados de resultados de ensaios clínicos, revisão de literatura, mercado remodelado e análise de base de produtos . A análise de mercado dos concorrentes-alvo pode ser analisada desde análises baseadas em tecnologia até estratégias de carteira de mercado. Podemos adicionar quantos concorrentes necessitar de dados no formato e estilo de dados que procura. A nossa equipa de analistas também pode fornecer dados em tabelas dinâmicas de ficheiros Excel em bruto (livro de factos) ou pode ajudá-lo a criar apresentações a partir dos conjuntos de dados disponíveis no relatório.