Apac Infusion Pump System Accessories Software Market

Market Size in USD Billion

CAGR :

%

USD

3.46 Billion

USD

8.50 Billion

2025

2033

USD

3.46 Billion

USD

8.50 Billion

2025

2033

| 2026 –2033 | |

| USD 3.46 Billion | |

| USD 8.50 Billion | |

| % | |

|

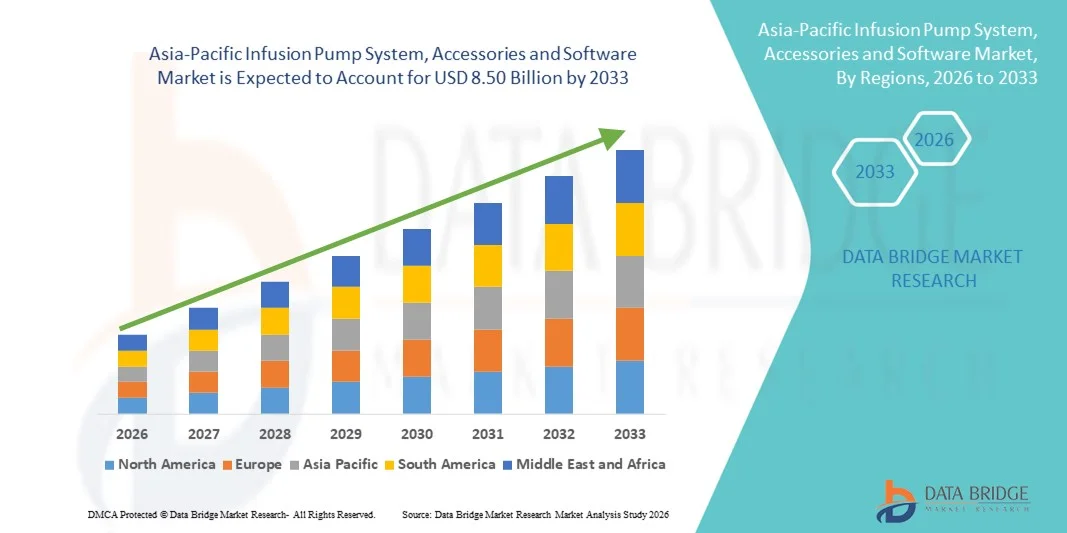

Asia-Pacific Infusion Pump System, Accessories and Software Market Size

- The Asia-Pacific infusion pump system, accessories and software market size was valued at USD 3.46 billion in 2025 and is expected to reach USD 8.50 billion by 2033, at a CAGR of 11.9% during the forecast period

- The market growth is largely driven by increasing adoption of advanced infusion technologies, growing hospital infrastructure, and rising prevalence of chronic diseases, fueling demand for accurate and automated drug delivery systems

- Furthermore, expanding healthcare IT integration, rising investments in smart hospital solutions, and demand for improved patient safety and monitoring are positioning infusion pumps and associated software as essential components in modern clinical care. These combined factors are accelerating market uptake, thereby significantly boosting the industry’s growth

Asia-Pacific Infusion Pump System, Accessories and Software Market Analysis

- Infusion Pump System, Accessories and Software Market, including infusion pump systems, accessories, and software, provides precise and automated drug delivery, becoming critical components of modern healthcare infrastructure in hospitals, clinics, and home care settings due to their accuracy, safety features, and integration with hospital information systems

- The rising demand for infusion pumps is primarily driven by the growing prevalence of chronic diseases, increasing hospital admissions, and the need for reliable and efficient intravenous therapy, coupled with healthcare digitalization and patient monitoring initiatives

- Japan dominated the Asia-Pacific infusion pump system, accessories and software market in 2025 with the largest revenue share of 34.7%, supported by advanced hospital infrastructure, high adoption of smart medical devices, and strong presence of established medical device manufacturers

- China is expected to be the fastest-growing country in the Asia-Pacific infusion pump system, accessories and software market during the forecast period, fueled by expanding hospital infrastructure, government initiatives to modernize healthcare, and increasing adoption of advanced medical devices in both urban and rural hospitals

- The syringe pump segment dominated the Asia-Pacific infusion pump system, accessories and software market with a market share of 38.5% in 2025, driven by its precision in delivering small-volume medications, ease of use in intensive care units, and compatibility with a wide range of therapies

Report Scope and Asia-Pacific Infusion Pump System, Accessories and Software Market Segmentation

|

Attributes |

Asia-Pacific Infusion Pump System, Accessories and Software Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Infusion Pump System, Accessories and Software Market Trends

Advancements in Smart and Connected Infusion Technology

- A significant and accelerating trend in the Asia-Pacific infusion pump system, accessories, and software market is the integration of smart connectivity and IoT-enabled features, allowing real-time monitoring, data analytics, and remote control of infusion therapies

- For instance, the B. Braun Space Infusion Pump can be connected to hospital networks to monitor multiple patients simultaneously, enabling clinicians to adjust infusion parameters remotely. Similarly, Mindray’s BeneFusion pump series offers centralized monitoring and alerts through integrated hospital software platforms

- Smart infusion pumps leverage AI and predictive analytics to optimize drug delivery, detect anomalies, and suggest dosage adjustments, improving patient safety and reducing errors. For instance, some Hospira Plum A+ pumps utilize intelligent alerts to notify caregivers of occlusions or dosage deviations

- Integration with hospital information systems facilitates seamless documentation, automated reporting, and centralized control, allowing healthcare staff to manage multiple infusion devices from a single interface, improving operational efficiency

- This trend towards connected, data-driven, and automated infusion systems is redefining clinical workflows, prompting manufacturers such as Terumo to develop IoT-enabled pumps with features such as automatic alarm notifications and remote monitoring capabilities

- The demand for smart, connected, and interoperable infusion solutions is growing rapidly across hospitals, clinics, and home healthcare settings, as healthcare providers increasingly prioritize patient safety, efficiency, and integrated therapy management

- Integration with electronic medical records (EMR) and cloud-based platforms is enhancing data analytics capabilities, enabling healthcare providers to track therapy outcomes, optimize resource allocation, and improve clinical decision-making

Asia-Pacific Infusion Pump System, Accessories and Software Market Dynamics

Driver

Increasing Healthcare Infrastructure Expansion and Chronic Disease Management

- The rapid growth of healthcare infrastructure, coupled with rising prevalence of chronic diseases requiring continuous intravenous therapy, is a major driver for the Asia-Pacific infusion pump market

- For instance, in March 2025, Mindray launched an initiative to supply advanced infusion pumps to tier-2 and tier-3 hospitals in India and China, improving therapy accuracy and patient monitoring

- Growing hospital admissions and the need for reliable drug delivery systems are pushing healthcare providers to adopt advanced infusion pumps that minimize errors and optimize therapy outcomes

- In addition, the shift toward digital hospital solutions and electronic health records is making infusion pumps with integrated software and connectivity essential for efficient clinical workflows

- The convenience of automated drug delivery, real-time monitoring, and remote control capabilities is propelling the adoption of infusion pump systems in both acute care and home healthcare settings, with manufacturers offering user-friendly and scalable solutions

- Government initiatives and funding to modernize healthcare facilities in countries such as China, India, and Australia are further accelerating adoption of advanced infusion technologies

- Rising awareness and training programs for healthcare professionals on safe and efficient infusion practices are boosting confidence in adopting smart infusion systems

Restraint/Challenge

Device Safety Concerns and Regulatory Compliance Hurdles

- Concerns regarding device malfunctions, software errors, and regulatory compliance issues pose significant challenges to broader market adoption, as infusion pumps require strict adherence to safety and quality standards

- For instance, reported software glitches in some infusion pump models have led to dosage errors, making healthcare providers cautious about widespread deployment

- Addressing these concerns through rigorous device testing, robust software validation, and compliance with national and international medical device regulations is essential for building trust among hospitals and clinicians

- In addition, the relatively high cost of advanced infusion pump systems and associated software can limit adoption in budget-constrained hospitals or home healthcare settings, despite their clinical benefits

- While prices are gradually stabilizing, the perceived premium of smart infusion systems, combined with stringent regulatory requirements, can hinder rapid uptake; overcoming these challenges through affordable, compliant, and reliable solutions is crucial for sustained market growth

- Limited technical expertise and maintenance capabilities in smaller hospitals or rural clinics can impede proper usage and reliability of advanced infusion pumps

- Interoperability issues between infusion pump software and existing hospital IT systems can create operational challenges, delaying widespread adoption until standardized integration solutions are implemented

Asia-Pacific Infusion Pump System, Accessories and Software Market Scope

The market is segmented on the basis of product type, application, type, usage, infusion method, infusion type, operation type, end user, and distribution channel.

- By Product Type

On the basis of product type, the Asia-Pacific infusion pump market is segmented into infusion pump systems, infusion pump accessories, and infusion pump management softwares. The Infusion Pump Systems segment dominated the market with the largest revenue share in 2025, driven by the critical role these systems play in delivering accurate medication dosages across hospitals, clinics, and home healthcare. Hospitals prefer these systems for patient safety, particularly in ICUs, oncology, and pediatric wards. Technological advancements such as smart pumps, multi-channel systems, and IoT integration further enhance monitoring and workflow efficiency. Rising prevalence of chronic diseases and investments in modern healthcare infrastructure are boosting the segment. Its established presence in both developed and emerging Asia-Pacific healthcare markets ensures steady adoption.

The Infusion Pump Management Softwares segment is expected to witness the fastest growth from 2026 to 2033, fueled by increasing adoption of digital health solutions and smart hospital initiatives. These software solutions enable centralized monitoring, dose error reduction, and remote management of multiple pumps. Integration with hospital EMR/EHR systems improves workflow efficiency and reduces manual errors. Hospitals increasingly adopt these solutions to optimize drug administration protocols and enhance patient safety. The segment is particularly popular in large-scale, multi-ward hospitals and high-volume facilities.

- By Application

On the basis of application, the market is segmented into general infusion, pain and anesthesia management, insulin infusion, enteral infusion, chemotherapy, pediatrics/neonatology, hematology, gastroenterology, and others. The General Infusion segment dominated the market in 2025, holding the largest revenue share due to its broad applicability in delivering fluids, electrolytes, and medications in hospitals. ICUs, emergency wards, and post-operative units heavily rely on general infusion pumps. The segment benefits from clinician familiarity and the large installed base of compatible devices. Its widespread use across hospitals ensures consistent revenue generation. Rising patient admissions and expansion of healthcare infrastructure further strengthen this segment.

The Chemotherapy segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by rising cancer prevalence in countries such as China, India, and Japan. Oncology wards require precise, controlled delivery of cytotoxic drugs, making infusion pumps essential. Advanced pumps reduce dosage errors and improve patient safety. Increasing investments in cancer care infrastructure and government support for oncology treatment accelerate segment growth. Hospitals adopt these systems for both inpatient and outpatient chemotherapy administration.

- By Type

On the basis of type, the market is segmented into traditional infusion pumps and specialty infusion pumps. The Traditional Infusion Pumps segment dominated the market in 2025, owing to their reliability, cost-effectiveness, and widespread adoption across hospitals and clinics. These pumps are extensively used in general infusion, pain management, and pediatric care. Clinicians prefer traditional pumps for their simplicity, ease of use, and compatibility with standard accessories. Hospitals of all sizes deploy these pumps for routine therapies. The segment’s familiarity among clinicians and proven performance ensures sustained demand. Consistent adoption in both public and private healthcare facilities maintains dominance.

The Specialty Infusion Pumps segment is projected to witness the fastest growth from 2026 to 2033, fueled by rising adoption in oncology, pediatrics, and critical care. Specialty pumps include smart pumps, syringe pumps, multi-channel pumps, and devices integrated with software for remote monitoring. These pumps are preferred in high-risk therapies where precise dosing is critical. Growth is supported by rising prevalence of chronic diseases and hospital investments in advanced care technologies. Technological innovation and increased focus on patient safety further drive adoption.

- By Usage

On the basis of usage, the market is segmented into disposable and reusable. The Reusable segment dominated the market in 2025, holding the largest revenue share due to its cost-effectiveness and long-term use in hospitals and clinics. Reusable pumps are compatible with multiple accessories and suitable for a variety of therapies. Hospitals prioritize these systems for high-volume wards and critical care units. Long-term operational cost savings contribute to dominance. Ease of maintenance, reliability, and consistent performance further strengthen adoption. The segment is particularly popular in large-scale healthcare facilities.

The Disposable segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by infection control measures, ease of use, and adoption in home healthcare. Single-use pumps reduce cross-contamination risks, which has become increasingly critical post-pandemic. Rising telemedicine, outpatient care, and home infusion therapy boost demand. Disposables are preferred in hospice and home care settings. Hospitals increasingly integrate disposable devices for safer patient outcomes. Growth is also supported by regulatory initiatives promoting single-use medical devices.

- By Infusion Method

On the basis of infusion method, The market is segmented into intravenous, arterial, subcutaneous, and epidural. The Intravenous (IV) segment dominated in 2025, due to its universal application across hospitals, including ICUs, surgical wards, and oncology units. IV infusion is standard for delivering fluids, electrolytes, and medications. Its dominance is supported by clinician familiarity and the large installed base of IV-compatible pumps. Hospitals prioritize IV pumps for both general and critical care. Continuous and intermittent IV therapies further reinforce demand. The segment generates consistent revenue across multiple care settings.

The Subcutaneous infusion segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing adoption in home healthcare and chronic disease management, including insulin delivery. Wearable infusion devices and remote monitoring systems enhance patient convenience and compliance. Adoption is increasing in outpatient and home care settings. Integration with patient monitoring software improves therapy accuracy. Rising prevalence of diabetes and other chronic conditions further accelerates segment growth.

- By Infusion Type

On the basis of infusion type, the market is segmented into continuous infusion and intermittent infusion. The Continuous Infusion segment dominated in 2025, due to its critical role in ICUs, oncology, and anesthesia management. Continuous infusion maintains stable drug plasma levels, reduces errors, and improves patient outcomes. Hospitals rely on these pumps for long-duration therapies. Advanced smart pumps enhance precision and monitoring capabilities. Its widespread adoption in hospitals ensures sustained revenue generation. Clinician familiarity and proven performance maintain dominance.

The Intermittent Infusion segment is expected to grow at the fastest CAGR from 2026 to 2033,, driven by adoption in home healthcare, pain management, and outpatient therapy. Flexible dosing schedules and reduced drug wastage attract hospitals and patients. Telemedicine and home care adoption further support growth. Intermittent pumps integrate with remote monitoring software. They are preferred in outpatient therapy and chronic disease management. Rising home-based healthcare adoption fuels rapid segment growth.

- By Operation Type

On the basis of operation type, the market is segmented into syringe pump, elastomeric pump, peristaltic pump, multi-channel pump, and smart pump. The Syringe Pump segment dominated in 2025 with a market share of 38.5%, favored for precise, low-volume drug delivery in neonatal, pediatric, and critical care settings. It is reliable, easy to operate, and compatible with multiple therapies. Hospitals use syringe pumps for both continuous and intermittent infusions. Widespread adoption in ICUs ensures steady revenue. Clinician familiarity and operational simplicity maintain dominance. The segment remains a preferred choice in high-risk therapy units.

The Smart Pump segment is projected to witness the fastest growth from 2026 to 2033, driven by AI integration, wireless connectivity, and compatibility with hospital EMR systems. Smart pumps improve patient safety, reduce dosage errors, and enable remote monitoring. They are increasingly adopted in oncology, critical care, and home healthcare. Hospitals invest in smart pumps to optimize workflow efficiency and enhance patient outcomes. Rising digital health initiatives and government support further accelerate adoption.

- By End User

On the basis of end user, the market is segmented into hospitals and clinics, home healthcare, ambulatory and surgical centers, and others. The Hospitals and Clinics segment dominated the market in 2025, holding the largest revenue share due to high patient volumes and the need for precise, continuous, and intermittent medication delivery. Hospitals prioritize infusion pumps for ICUs, oncology, pediatrics, and post-operative wards. Their demand is supported by the integration of smart pumps with hospital EMR/EHR systems and the adoption of advanced software for dose management. Hospitals benefit from improved workflow efficiency, reduced human error, and enhanced patient safety through modern infusion solutions. The segment remains dominant across both public and private healthcare facilities.

The Home Healthcare segment is expected to witness the fastest growth from 2026 to 2033, driven by rising chronic disease prevalence, telemedicine adoption, and increased preference for outpatient and at-home infusion therapy. Home-based care solutions, such as portable infusion pumps and subcutaneous devices, allow patients to manage therapies such as insulin delivery or pain management conveniently. Smart, connected devices enable remote monitoring by healthcare professionals, reducing hospital visits. Government initiatives promoting home healthcare and reimbursement schemes further accelerate segment adoption. Increasing patient awareness of home infusion benefits fuels rapid growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and retail sales. The Direct Tender segment dominated the market in 2025, holding the largest revenue share due to bulk procurement by hospitals, clinics, and healthcare institutions. Direct tenders allow healthcare facilities to purchase infusion pumps, accessories, and software at negotiated prices, ensuring cost-effectiveness and long-term supply reliability. Large-scale tenders often include service agreements, training, and maintenance support, which strengthens adoption in hospitals. This channel is particularly preferred in government hospitals and large private healthcare chains. High-volume demand and long-term contracts reinforce its dominance.

The Retail Sales segment is expected to witness the fastest growth from 2026 to 2033, fueled by rising home healthcare adoption, outpatient infusion therapy, and small clinics seeking standalone purchases. Retail availability enables patients and smaller care centers to access infusion devices, accessories, and supporting software easily. Increasing e-commerce adoption and partnerships between manufacturers and distributors expand market reach. The segment is gaining traction due to convenience, affordability, and growing awareness of home-based infusion therapies. Rising consumer preference for self-administered infusion solutions accelerates growth in retail channels.

Asia-Pacific Infusion Pump System, Accessories and Software Market Regional Analysis

- Japan dominated the Asia-Pacific infusion pump system, accessories and software market in 2025 with the largest revenue share of 34.7%, supported by advanced hospital infrastructure, high adoption of smart medical devices, and strong presence of established medical device manufacturers

- Hospitals and clinics in Japan increasingly prioritize patient safety, real-time monitoring, and integration with hospital information systems, making smart and connected infusion pumps an essential component of modern healthcare delivery

- This widespread adoption is further supported by government initiatives to modernize healthcare facilities, increasing investments in smart hospital solutions, and rising awareness among healthcare providers about the benefits of advanced infusion technologies, establishing infusion pumps as a preferred solution in both acute care and home healthcare settings

The China Infusion Pump System, Accessories and Software Market Insight

The China infusion pump market is expected to grow at a rapid CAGR during the forecast period, driven by expanding hospital infrastructure, increasing prevalence of chronic diseases, and rising adoption of smart and connected medical devices. Government initiatives to modernize healthcare facilities and promote digital health solutions are further boosting demand. Moreover, growing awareness among clinicians about patient safety, accurate dosing, and automated therapy management is accelerating market adoption across public and private hospitals, specialty clinics, and home healthcare settings. Investments in local manufacturing and affordable infusion pump solutions are also helping to widen accessibility across urban and semi-urban regions.

Japan Infusion Pump System, Accessories and Software Market Insight

The Japan infusion pump market is gaining momentum due to advanced hospital infrastructure, high adoption of connected medical devices, and a strong focus on patient safety and workflow efficiency. The increasing number of smart hospitals, integration with IoT-enabled systems, and demand for precise, automated drug delivery solutions are fueling growth. In addition, Japan’s rapidly aging population is driving demand for user-friendly, safe, and reliable infusion systems in both residential and clinical settings. Hospitals are also investing in integrated hospital information systems that allow centralized monitoring of multiple infusion devices, improving operational efficiency and reducing medication errors.

India Infusion Pump System, Accessories and Software Market Insight

The India infusion pump market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by rapid expansion of healthcare facilities, rising prevalence of chronic and critical illnesses, and growing adoption of smart medical devices. India’s push towards smart hospitals, telemedicine-enabled home healthcare, and domestic manufacturing of cost-effective infusion pumps is boosting market growth. Increasing awareness among healthcare providers about patient safety, dosage accuracy, and workflow automation is further accelerating adoption. The market is also benefiting from government programs aimed at improving rural healthcare infrastructure, expanding access to advanced infusion therapy across tier-2 and tier-3 cities.

South Korea Infusion Pump System, Accessories and Software Market Insight

The South Korea infusion pump market is poised for steady growth, fueled by technologically advanced hospital infrastructure, high healthcare expenditure, and rising adoption of automated and connected infusion devices. Government initiatives promoting digital healthcare, smart hospital programs, and integration of medical devices with electronic medical records are supporting market expansion. Moreover, South Korea’s emphasis on patient safety, precision therapy, and efficiency in clinical workflows is driving widespread adoption of infusion pumps across hospitals, specialty clinics, and home care settings. The growing trend of remote patient monitoring and telemedicine is also encouraging the use of portable and IoT-enabled infusion systems, enhancing patient convenience and clinical efficiency.

Asia-Pacific Infusion Pump System, Accessories and Software Market Share

The Asia-Pacific Infusion Pump System, Accessories and Software industry is primarily led by well-established companies, including:

- Shenzhen Mindray Bio Medical Electronics Co., Ltd. (China)

- Baxter (U.S.)

- B. Braun SE (Germany)

- Fresenius Kabi AG (Germany)

- BD (U.S.)

- Medtronic (Ireland)

- ICU Medical, Inc. (U.S.)

- Smiths Medical (U.K.)

- Nipro Corporation (Japan)

- Moog Inc. (U.S.)

- AngioDynamics, Inc. (U.S.)

- Teleflex Incorporated (U.S.)

- ZOLL Medical Corporation (U.S.)

- Micrel Medical Devices (Italy)

- Halyard Health (U.S.)

- Zyno Medical (U.S.)

- Shenzhen ENMIND Technology Co., Ltd. (China)

- Polymedicure Ltd. (India)

- KD Scientific Inc. (U.S.)

What are the Recent Developments in Asia-Pacific Infusion Pump System, Accessories and Software Market?

- In August 2025, Terumo India launched the Terufusion™ Advanced Infusion Systems in India, comprising a smart syringe pump, smart volumetric pump, and integrated pump monitoring software to enhance precision, patient safety, and ICU workflow efficiency, responding to rising critical care needs across Indian hospitals

- In April 2025, ICU Medical introduced a new category of precision IV pumps — the Plum Solo™ and updated Plum Duo™ precision infusion pumps with advanced LifeShield™ infusion safety software expanding its IV Performance Platform to deliver ±3% accuracy and improved clinical data reliability for infusion therapy. This development represents a significant advancement in infusion device technology that healthcare systems

- In February 2023, Mindray introduced the BeneFusion i Series and u Series infusion systems, offering high‑precision, customizable infusion technology designed to improve medication delivery accuracy and clinical safety across diverse care environments in the Asia‑Pacific region

- In October 2021, EOFlow Co., Ltd. formed a joint venture with Changsha Sinocare in China to support local production and distribution of the EOPatch wearable insulin infusion pump, targeting China’s expanding diabetes care market with innovative drug delivery solutions

- In February 2021, Mindray introduced the new BeneFusion e Series infusion systems, marketed as delivering improved efficiency for IV therapy with features catering to a range of clinical settings, expanding the company’s infusion product portfolio in Asian markets such as India and China

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.