Asia Pacific Aluminum Casting Market

Market Size in USD Billion

USD

46.73 Billion

USD

88.45 Billion

2024

2032

USD

46.73 Billion

USD

88.45 Billion

2024

2032

| 2025 - 2032 | |

| USD 46.73 Billion | |

| USD 88.45 Billion | |

| % | |

|

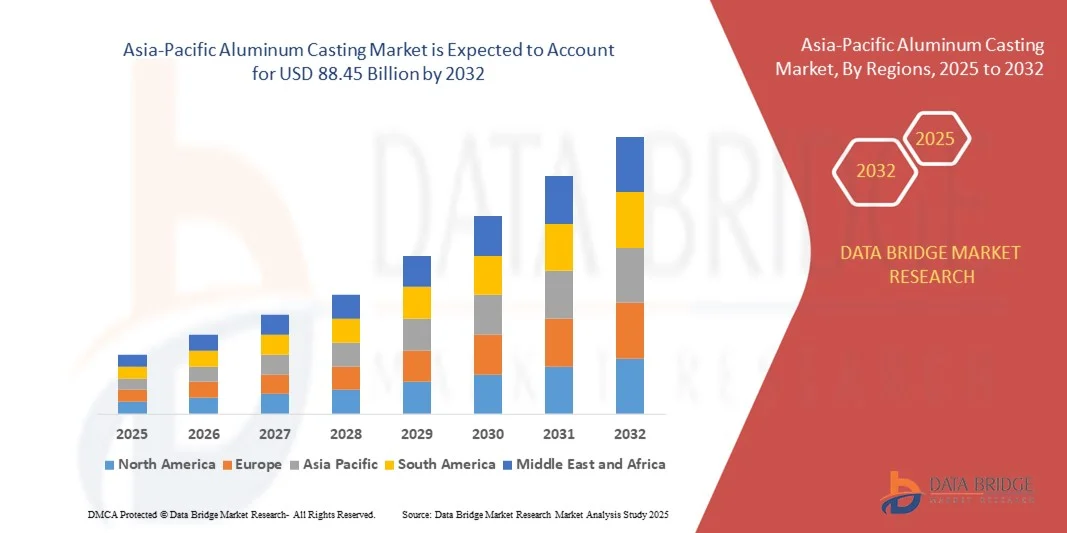

Asia-Pacific Aluminum Casting Market Size

- The Asia-Pacific Aluminum Casting Market size was valued at USD 46.73 billion in 2024 and is projected to reach USD 88.45 billion by 2032, growing at a CAGR of 8.30% during the forecast period.

- The market expansion is primarily driven by the rapid industrialization and increasing use of lightweight materials in the automotive, aerospace, and construction sectors, boosting demand for aluminum casting solutions.

- In addition, advancements in casting technologies, rising infrastructure investments, and a strong focus on energy efficiency are propelling the adoption of aluminum cast products, significantly accelerating the market’s overall growth.

Asia-Pacific Aluminum Casting Market Analysis

- Aluminum castings, providing lightweight, durable, and corrosion-resistant components, are increasingly essential across automotive, aerospace, construction, and industrial machinery sectors due to their strength-to-weight ratio, design flexibility, and energy efficiency benefits.

- The rising demand for aluminum casting is primarily driven by the automotive industry’s shift toward lightweight materials to improve fuel efficiency, growing aerospace production, and expanding infrastructure projects in emerging economies.

- China dominated the Asia-Pacific Aluminum Casting Market with the largest revenue share of 38.7% in 2024, supported by large-scale manufacturing facilities, strong domestic automotive production, and significant investments in industrial automation, with key players focusing on advanced casting technologies and high-precision components to meet growing demand.

- India is expected to be the fastest-growing region in the Asia-Pacific Aluminum Casting Market during the forecast period due to rapid industrialization, increasing automotive production, and rising infrastructure development.

- The expendable mold casting segment dominated the market with a revenue share of 57.4% in 2024, driven by its flexibility in producing complex and intricate components for automotive, aerospace, and industrial machinery applications

Report Scope and Asia-Pacific Aluminum Casting Market Segmentation

|

Attributes |

Aluminum Casting Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

• China Zhongwang Holdings (China) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia-Pacific Aluminum Casting Market Trends

Advancements in Lightweight and High-Performance Aluminum Casting

- A significant and accelerating trend in the Asia-Pacific Aluminum Casting Market is the adoption of advanced lightweight and high-performance aluminum alloys, designed to improve strength-to-weight ratios and enhance energy efficiency across automotive, aerospace, and industrial applications.

- For instance, automotive manufacturers are increasingly using high-pressure die-cast aluminum engine blocks and chassis components to reduce vehicle weight, improve fuel efficiency, and meet stricter emission standards. Similarly, aerospace companies are leveraging precision aluminum castings for structural components that require both durability and weight reduction.

- Technological innovations in casting processes, such as vacuum-assisted die casting, semi-solid casting, and additive manufacturing hybrid approaches, are enabling higher precision, reduced material waste, and improved mechanical properties. These advances allow manufacturers to produce complex geometries while maintaining performance and reliability.

- The integration of aluminum cast components into electric vehicles (EVs) and renewable energy infrastructure, such as wind turbine housings and solar panel frames, further underscores the material’s versatility and growing importance in sustainable industrial applications.

- This trend towards lightweight, high-performance, and technologically advanced aluminum castings is reshaping design and manufacturing expectations across multiple industries. Consequently, companies such as Constellium, Alcoa, and China Zhongwang are investing in R&D to develop innovative aluminum alloys and casting processes that meet evolving industry standards.

- The demand for aluminum cast components with superior mechanical properties and reduced weight is expanding rapidly across automotive, aerospace, construction, and industrial sectors, driven by stricter regulations, sustainability goals, and the need for performance optimization.

Asia-Pacific Aluminum Casting Market Dynamics

Driver

Growing Demand Driven by Automotive, Aerospace, and Industrial Expansion

- The increasing demand for lightweight, durable, and corrosion-resistant components across the automotive, aerospace, and industrial machinery sectors is a significant driver for the Asia-Pacific Aluminum Casting Market.

- For instance, in 2024, Hyundai Wia expanded its high-precision aluminum casting production for automotive engine and chassis components, responding to rising demand for fuel-efficient vehicles. Similar initiatives by key players are expected to accelerate market growth over the forecast period.

- As manufacturers aim to improve energy efficiency, reduce vehicle weight, and meet stricter environmental regulations, aluminum castings offer superior mechanical properties and design flexibility compared to traditional materials.

- Furthermore, the expansion of infrastructure projects, industrial machinery production, and renewable energy installations in emerging economies is driving the adoption of aluminum cast components due to their strength, lightweight nature, and longevity.

- The increasing use of aluminum in electric vehicles (EVs), aerospace structures, and industrial equipment, along with rising investments in precision casting technologies, is propelling market growth across both mature and emerging markets.

Restraint/Challenge

High Production Costs and Technical Complexity

- High initial production costs and technical complexities associated with advanced aluminum casting processes pose significant challenges to broader market adoption. Aluminum alloys require precise control during melting, casting, and post-processing, making the setup and maintenance of high-quality production lines capital-intensive.

- For instance, investment in vacuum-assisted die casting or semi-solid casting technologies can be cost-prohibitive for smaller manufacturers, limiting their ability to compete with larger, well-established players.

- Ensuring consistent quality, dimensional accuracy, and mechanical performance is critical, as defective castings can lead to product recalls or failures in automotive and aerospace applications. Companies such as Alcoa, Constellium, and China Zhongwang emphasize stringent quality control, process optimization, and advanced alloy development to mitigate these challenges.

- Additionally, fluctuations in raw material prices and energy costs can increase production expenses, further impacting market accessibility for smaller or price-sensitive manufacturers.

- Addressing these challenges through technological innovation, cost-efficient production methods, and strategic partnerships is vital for sustained growth and wider adoption of aluminum castings across diverse industries.

Asia-Pacific Aluminum Casting Market Scope

Asia Pacific aluminum casting market is segmented on the basis of process, source, application, and end-user.

- By Process

On the basis of process, the Asia-Pacific Aluminum Casting Market is segmented into expendable mold casting and non-expendable mold casting. The expendable mold casting segment dominated the market with a revenue share of 57.4% in 2024, driven by its flexibility in producing complex and intricate components for automotive, aerospace, and industrial machinery applications. This process allows for high-precision casting and accommodates varying production volumes, making it ideal for both mass production and specialized components.

Non-expendable mold casting is expected to witness the fastest CAGR of 18.9% from 2025 to 2032, owing to its ability to offer superior surface finish, dimensional accuracy, and reduced post-processing requirements. Increasing investments in high-precision casting technologies and growing demand for durable, lightweight components in emerging industries are fueling the adoption of non-expendable mold casting across the region.

- By Source

On the basis of source, the Asia-Pacific Aluminum Casting Market is segmented into primary (fresh aluminum) and secondary (recycled aluminum). The primary aluminum segment dominated the market with a 61.3% revenue share in 2024, driven by its high purity, consistent mechanical properties, and suitability for critical automotive and aerospace components. Primary aluminum ensures superior strength-to-weight ratios and reliability, making it the preferred choice for high-performance applications.

The secondary aluminum segment is expected to witness the fastest CAGR of 19.4% from 2025 to 2032, due to increasing environmental awareness, cost-effectiveness, and growing initiatives for sustainable manufacturing. Recycled aluminum usage is expanding rapidly in automotive, construction, and household appliance applications, driven by circular economy practices and regulations promoting reduced carbon footprints in the manufacturing sector.

- By Application

On the basis of application, the Asia-Pacific Aluminum Casting Market is segmented into intake manifolds, oil pan housings, structural parts, chassis parts, cylinder heads, engine blocks, transmissions, wheels and brakes, heat transfers, and others. The engine blocks segment dominated the market with a revenue share of 35.8% in 2024, propelled by the high demand for lightweight and thermally efficient components in automotive and commercial vehicles. Engine blocks made from aluminum alloys offer significant fuel efficiency gains and enhanced thermal management, supporting stringent emission regulations.

The wheels and brakes segment is expected to witness the fastest CAGR of 21.2% from 2025 to 2032, driven by the automotive industry’s shift toward lightweight castings for improved vehicle performance, safety, and energy efficiency. Increasing electric vehicle production and the demand for premium automotive components are further supporting this trend.

- By End-User

On the basis of end-user, the Asia-Pacific Aluminum Casting Market is segmented into automotive, building and construction, industrial, household appliances, aerospace, electronics and electrical, engineering tools, and others. The automotive segment dominated the market with a revenue share of 48.6% in 2024, fueled by the increasing production of passenger vehicles, commercial vehicles, and electric vehicles, which extensively utilize aluminum cast components for weight reduction and efficiency.

The industrial segment is expected to witness the fastest CAGR of 20.5% from 2025 to 2032, driven by rising demand for durable aluminum castings in machinery, renewable energy infrastructure, and manufacturing equipment. Expanding industrialization, increasing investments in smart factories, and growing adoption of precision aluminum components are supporting rapid growth in this sector.

Asia-Pacific Aluminum Casting Market Regional Analysis

- China dominated the Aluminum Casting Market with the largest revenue share of 38.7% in 2024, driven by rapid industrialization, expanding automotive and aerospace sectors, and increasing demand for lightweight, high-performance components.

- Manufacturers in the region prioritize aluminum castings for their strength-to-weight advantages, corrosion resistance, and cost-effectiveness, making them ideal for applications in vehicles, machinery, and infrastructure projects.

- This widespread adoption is further supported by growing urbanization, rising disposable incomes, and government initiatives promoting advanced manufacturing technologies, establishing Asia-Pacific as a key hub for aluminum casting production and innovation across both domestic and export markets.

China Aluminum Casting Market Insight

The China aluminum casting market accounted for the largest revenue share in Asia-Pacific in 2024, driven by the country’s rapidly growing automotive, electronics, and industrial machinery sectors. Rising urbanization, infrastructure development, and the expansion of electric vehicle production are key factors propelling demand. China’s strong manufacturing base, technological advancements in casting processes, and availability of cost-effective labor and raw materials enhance market growth. Furthermore, government initiatives supporting advanced manufacturing and sustainable production practices, including the use of recycled aluminum, are contributing to the widespread adoption of aluminum cast components in both domestic and export markets.

Japan Aluminum Casting Market Insight

The Japan aluminum casting market is experiencing steady growth due to the country’s emphasis on high-precision, lightweight components for automotive, aerospace, and electronics applications. Japan’s focus on energy efficiency, sustainability, and advanced manufacturing technologies is driving adoption of aluminum castings, particularly for engine blocks, structural parts, and electronic housings. The increasing number of smart and electric vehicles, coupled with automation in industrial production, further supports market expansion. Additionally, Japan’s aging population is influencing demand for durable and easy-to-use aluminum components across household appliances and mobility solutions.

India Aluminum Casting Market Insight

The India aluminum casting market is poised for robust growth during the forecast period, driven by rapid industrialization, rising automotive production, and expanding infrastructure projects. The country’s growing middle class and increasing disposable incomes are boosting demand for vehicles and consumer appliances, both of which utilize aluminum castings. India is also witnessing technological adoption in casting processes, such as high-pressure die casting and sand casting, which enhances efficiency and product quality. Government initiatives to promote domestic manufacturing and “Make in India” programs are further accelerating market growth in both domestic and export applications.

South Korea Aluminum Casting Market Insight

The South Korea aluminum casting market is witnessing steady growth, fueled by strong demand from the automotive, electronics, and industrial machinery sectors. South Korea’s focus on lightweight materials for fuel efficiency, coupled with technological advancements in aluminum casting processes, supports market expansion. The country’s emphasis on precision engineering and innovation in industrial components, along with the rise of electric vehicles and connected electronics, is driving adoption. Additionally, the presence of major domestic manufacturers and strategic collaborations with global players is enhancing South Korea’s competitiveness in the regional aluminum casting market.

Asia-Pacific Aluminum Casting Market Share

The Aluminum Casting industry is primarily led by well-established companies, including:

• China Zhongwang Holdings (China)

• Constellium (Netherlands)

• Hyundai Wia (South Korea)

• Gränges (Sweden)

• Alcoa Corporation (U.S.)

• Shandong Jinbao Aluminum Group (China)

• Sumitomo Light Metal Industries (Japan)

• UACJ Corporation (Japan)

• Novelis Inc. (U.S.)

• Hongqiao Group (China)

• AAC Technologies (China)

• Hefei Hongsheng Aluminum (China)

• India Foils Ltd. (India)

• Indal Aluminum (India)

• AMAG Austria Metall (Austria)

• Aluminium Bahrain (Alba) (Bahrain)

• Eckart GmbH (Germany)

• Metalcorp Group (UAE)

• Trimet Aluminium SE (Germany)

• Aleris Corporation (U.S.)

What are the Recent Developments in Asia-Pacific Aluminum Casting Market?

- In April 2023, China Zhongwang Holdings Ltd., a leading manufacturer of high-precision aluminum castings, launched a strategic expansion project in the Jiangsu province aimed at increasing production capacity for automotive and aerospace components. This initiative highlights the company’s commitment to leveraging advanced casting technologies and eco-friendly processes, strengthening its position in the rapidly growing Asia-Pacific aluminum casting market. By integrating cutting-edge manufacturing techniques, China Zhongwang aims to meet rising regional and global demand for lightweight, high-performance aluminum components.

- In March 2023, Hitech Castings India Pvt. Ltd. introduced a new line of aluminum engine blocks and chassis components tailored for electric and hybrid vehicles. The innovative product line focuses on reducing weight while maintaining structural integrity, addressing the increasing demand for fuel-efficient and sustainable automotive solutions. This advancement underscores Hitech Castings’ commitment to innovation and its role in driving growth within the Asia-Pacific aluminum casting market.

- In March 2023, Samsung Aerospace Components, South Korea, commissioned a state-of-the-art aluminum casting facility to supply structural and engine parts for aerospace applications. The facility incorporates precision casting technologies and automated quality control systems, highlighting Samsung’s dedication to producing high-performance aluminum components while reinforcing South Korea’s position as a key contributor to the Asia-Pacific aluminum casting market.

- In February 2023, Japan Aluminum Foundry Co., Ltd. announced a strategic partnership with leading automotive OEMs to manufacture intake manifolds, transmission housings, and structural parts. This collaboration focuses on improving vehicle performance and fuel efficiency through lightweight aluminum solutions, reflecting Japan’s continued emphasis on precision engineering and sustainable manufacturing in the Asia-Pacific aluminum casting sector.

- In January 2023, Indian Castings & Alloys Pvt. Ltd. unveiled a new facility producing aluminum wheels, engine blocks, and heat transfer components for automotive and industrial applications. Equipped with advanced casting technologies and stringent quality assurance protocols, the facility exemplifies the company’s dedication to innovation, operational efficiency, and reinforcing its footprint in the growing Asia-Pacific aluminum casting market.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Asia Pacific Aluminum Casting Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Asia Pacific Aluminum Casting Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Asia Pacific Aluminum Casting Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.