Asia Pacific Automotive Interior Materials Market

Market Size in USD Billion

USD

1.56 Billion

USD

2.04 Billion

2025

2033

USD

1.56 Billion

USD

2.04 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.56 Billion | |

| USD 2.04 Billion | |

| % | |

|

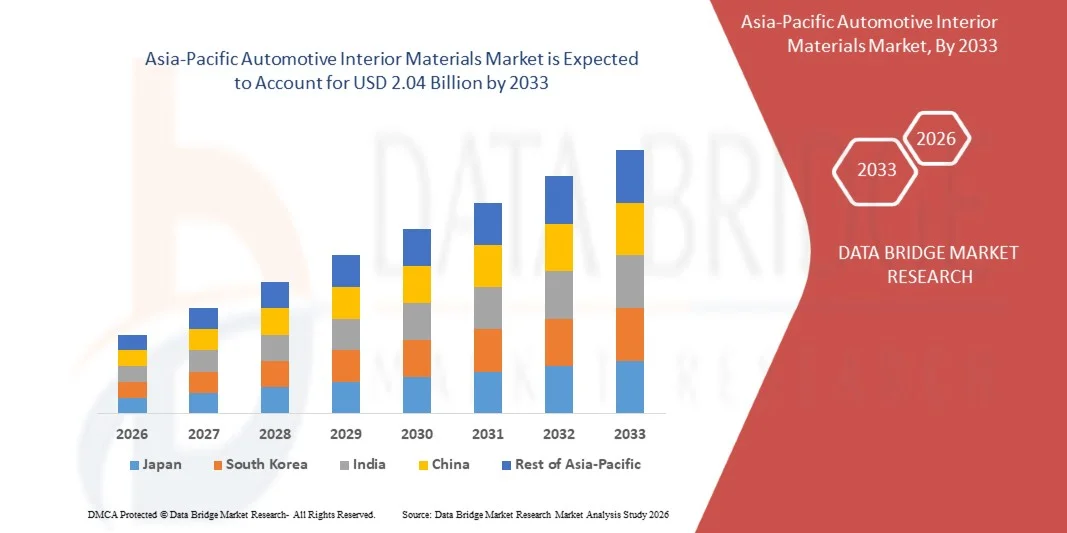

Asia-Pacific Automotive Interior Materials Market Size

- The Asia-Pacific automotive interior materials market size was valued at USD 1.56 Billion in 2025 and is expected to reach USD 2.04 Billion by 2033, at a CAGR of 3.45% during the forecast period

- The market growth is largely fuelled by the increasing demand for enhanced vehicle aesthetics, comfort, and premium interior finishes across passenger and commercial vehicles

- Rising adoption of lightweight and sustainable materials to improve fuel efficiency and meet environmental regulations is further accelerating market expansion

Asia-Pacific Automotive Interior Materials Market Analysis

- The market is witnessing strong growth due to continuous innovation in material technologies, including bio-based polymers, synthetic leather, and advanced composites, aimed at improving durability and sustainability

- Increasing production of electric vehicles is driving demand for specialized interior materials that offer improved thermal management, lightweight properties, and enhanced design flexibility

- China dominated the automotive interior materials market with the largest revenue share in 2025, driven by high vehicle production volumes and strong manufacturing capabilities

- Japan is expected to witness the highest compound annual growth rate (CAGR) in the Asia-Pacific automotive interior materials market due to strong focus on technological innovation, increasing adoption of lightweight and sustainable interior materials, and growing demand for high-quality and premium vehicle interiors

- The plastic segment held the largest market revenue share in 2025 driven by its cost-effectiveness, lightweight properties, and versatility in manufacturing various interior components such as dashboards, trims, and panels. Plastics also offer durability, corrosion resistance, and ease of molding into complex shapes, making them highly suitable for large-scale automotive production. In addition, increasing focus on recyclable and bio-based plastics is further supporting segment growth by aligning with sustainability goals

Report Scope and Asia-Pacific Automotive Interior Materials Market Segmentation

|

Attributes |

Asia-Pacific Automotive Interior Materials Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

• Toyota Boshoku Corporation (Japan) |

|

Market Opportunities |

• Increasing Adoption Of Sustainable And Bio-Based Interior Materials |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia-Pacific Automotive Interior Materials Market Trends

“Increasing Demand For Premium And Sustainable Interior Solutions”

• The growing consumer preference for enhanced comfort, aesthetics, and sustainability is significantly shaping the automotive interior materials market, as automakers increasingly focus on delivering high-quality and eco-friendly cabin experiences. Advanced materials such as synthetic leather, bio-based polymers, and recycled fabrics are gaining traction due to their ability to provide durability, lightweight properties, and improved visual appeal while aligning with sustainability goals. This trend is encouraging manufacturers to innovate with new material compositions and finishes that meet evolving consumer expectations

• Increasing awareness regarding environmental impact and regulatory compliance has accelerated the adoption of sustainable and low-emission interior materials across passenger and commercial vehicles. Automakers are actively incorporating recyclable and low-VOC materials in seats, dashboards, door panels, and trims to enhance cabin air quality and reduce carbon footprint. This shift is also driving collaboration between material suppliers and automotive OEMs to develop high-performance, eco-friendly solutions

• Premiumization trends are influencing purchasing decisions, with consumers demanding advanced features such as soft-touch surfaces, ambient lighting compatibility, noise reduction materials, and enhanced ergonomics. These factors are helping manufacturers differentiate their offerings in a competitive market while improving overall vehicle value proposition and brand positioning

• For instance, in 2024, Toyota and BMW expanded their use of sustainable interior materials, including recycled plastics and bio-based upholstery, in new vehicle models. These developments were introduced to meet rising consumer demand for eco-friendly and premium interiors while strengthening brand perception and customer loyalty

• While demand for advanced interior materials is growing, sustained market expansion depends on continuous innovation, cost optimization, and maintaining performance standards comparable to traditional materials. Manufacturers are focusing on improving material durability, scalability, and supply chain efficiency to support long-term growth

Asia-Pacific Automotive Interior Materials Market Dynamics

Driver

“Growing Preference For Premium, Lightweight, And Sustainable Materials”

• Rising demand for high-quality, comfortable, and visually appealing interiors is a major driver for the automotive interior materials market. Automakers are increasingly adopting lightweight and sustainable materials to enhance fuel efficiency and meet environmental regulations while improving overall vehicle performance and design flexibility

• Expanding applications across seats, dashboards, door panels, headliners, and carpets are influencing market growth. Advanced materials help improve durability, thermal insulation, and acoustic performance, enabling manufacturers to deliver superior in-cabin experiences and meet consumer expectations

• Automotive manufacturers are actively promoting innovative interior solutions through product development, branding strategies, and sustainability initiatives. These efforts are supported by increasing consumer preference for technologically advanced and environmentally responsible vehicles, encouraging collaborations between OEMs and material suppliers

• For instance, in 2023, Ford Motor Company and Hyundai Motor Company increased the integration of recycled and bio-based materials in vehicle interiors. This expansion was driven by rising demand for sustainable mobility solutions and improved interior quality, supporting product differentiation and brand value enhancement

• Although demand for premium and sustainable materials is rising, broader adoption depends on cost efficiency, material availability, and scalable manufacturing processes. Investment in advanced material technologies and supply chain optimization will be critical for long-term growth

Restraint/Challenge

“High Cost And Performance Trade-Offs Of Advanced Materials”

• The relatively high cost of advanced and sustainable interior materials compared to conventional options remains a key challenge, limiting adoption among cost-sensitive manufacturers. Premium materials such as synthetic leather, composites, and bio-based polymers often involve higher production and processing costs, impacting overall vehicle pricing

• Performance limitations and durability concerns associated with certain eco-friendly materials can restrict their widespread use in demanding automotive applications. Manufacturers must ensure that these materials meet safety, longevity, and quality standards without compromising functionality

• Supply chain complexities and availability of raw materials also impact market growth, as sourcing sustainable and certified materials requires strict compliance and reliable supplier networks. Fluctuations in raw material supply can lead to production delays and increased operational costs

• For instance, in 2024, suppliers working with brands such as Tesla and Volkswagen reported challenges related to sourcing and scaling sustainable materials for mass production. Higher costs and performance validation requirements created barriers to rapid adoption, affecting production timelines and cost structures

• Addressing these challenges will require continuous innovation, cost-effective manufacturing techniques, and improved material performance. Strengthening supplier networks and investing in research and development will be essential to ensure long-term market competitiveness and adoption

Asia-Pacific Automotive Interior Materials Market Scope

The market is segmented on the basis of material type, application, vehicle type, and end-user.

• By Material Type

On the basis of material type, the automotive interior materials market is segmented into Plastic, Composites, Fabrics, Leather, and Others. The plastic segment held the largest market revenue share in 2025 driven by its cost-effectiveness, lightweight properties, and versatility in manufacturing various interior components such as dashboards, trims, and panels. Plastics also offer durability, corrosion resistance, and ease of molding into complex shapes, making them highly suitable for large-scale automotive production. In addition, increasing focus on recyclable and bio-based plastics is further supporting segment growth by aligning with sustainability goals.

The leather segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for premium and luxury vehicle interiors. Leather materials enhance comfort, aesthetics, and perceived vehicle value, making them increasingly popular in high-end and mid-range vehicles. Advancements in synthetic and vegan leather alternatives are also contributing to growth by offering cost-effective and eco-friendly options. Furthermore, increasing consumer preference for customized and high-quality interiors is accelerating adoption.

• By Application

On the basis of application, the automotive interior materials market is segmented into Consoles and Dashboards, Doors, Seats, Steering Wheels, and Floor Carpet. The seats segment accounted for the largest market share in 2025 due to high material consumption and the need for comfort, durability, and ergonomic design. Seat materials such as fabrics, leather, and foams play a crucial role in enhancing passenger comfort, safety, and long-term usability. In addition, innovations in smart seating systems and temperature-controlled materials are further driving segment demand.

The dashboards segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing integration of advanced technologies such as infotainment systems, digital displays, and touch-sensitive controls. This is encouraging the use of high-quality, durable, and visually appealing materials to support both functionality and aesthetics. Growing demand for connected and autonomous vehicles is also contributing to the evolution of dashboard materials and design complexity.

• By Vehicle Type

On the basis of vehicle type, the automotive interior materials market is segmented into Passenger Vehicle, Light Commercial Vehicle, and Heavy Commercial Vehicle. The passenger vehicle segment dominated the market in 2025 driven by high production volumes and increasing consumer demand for comfort, premium features, and advanced interior designs. Rising disposable income and shifting consumer preferences toward enhanced in-cabin experience are further supporting segment growth.

The light commercial vehicle segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rapid expansion of e-commerce, logistics, and urban delivery services. This growth is increasing the demand for durable and cost-effective interior materials that can withstand frequent usage and operational wear. In addition, fleet operators are focusing on ergonomic and easy-to-maintain interiors, which is boosting material innovation in this segment.

• By End-user

On the basis of end-user, the automotive interior materials market is segmented into OEM and Aftermarket. The OEM segment held the largest market share in 2025 driven by strong integration of advanced materials during vehicle manufacturing and increasing focus on product differentiation by automakers. OEMs are also investing in sustainable and lightweight materials to meet regulatory requirements and improve vehicle efficiency.

The aftermarket segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising consumer interest in vehicle customization, interior upgrades, and replacement of worn-out components. Increasing availability of premium and innovative materials, along with growing automotive service networks, is further supporting demand. In addition, the trend of vehicle personalization is encouraging consumers to invest in high-quality interior enhancements.

Asia-Pacific Automotive Interior Materials Market Regional Analysis

• China dominated the automotive interior materials market with the largest revenue share in 2025, driven by high vehicle production volumes and strong manufacturing capabilities

• Consumers in the country are increasingly demanding improved interior quality, comfort, and advanced features, encouraging manufacturers to adopt innovative and cost-effective materials

• This dominance is further supported by rapid urbanization, expanding middle-class population, and rising demand for electric vehicles, strengthening China’s market position

Japan Automotive Interior Materials Market Insight

The Japan automotive interior materials market is expected to witness the fastest growth rate from 2026 to 2033, fueled by strong focus on technological innovation and high-quality vehicle interiors. Consumers are increasingly prioritizing comfort, safety, and premium design in automotive interiors. The growing adoption of advanced materials, including lightweight and sustainable options, is further supporting market growth. In addition, continuous investment in research and development and increasing demand for next-generation vehicles are significantly contributing to market expansion

Asia-Pacific Automotive Interior Materials Market Share

The Asia-Pacific automotive interior materials industry is primarily led by well-established companies, including:

• Toyota Boshoku Corporation (Japan)

• Faurecia Japan (Japan)

• Techtex (Japan)

• Grammer Japan (Japan)

• Johnson Controls Japan (Japan)

• Hyundai Mobis (South Korea)

• Hyundai Glovis (South Korea)

• Kosei Co., Ltd. (Japan)

• Nihon Plast Co., Ltd. (Japan)

• Seiren Co., Ltd. (Japan)

• Sumitomo Riko Company Limited (Japan)

• Tachi-S Co., Ltd. (Japan)

• Tokai Rika Co., Ltd. (Japan)

• Mitsui Kinzoku ACT Corporation (Japan)

• Showa Corporation (Japan)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Asia Pacific Automotive Interior Materials Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Asia Pacific Automotive Interior Materials Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Asia Pacific Automotive Interior Materials Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.