Asia Pacific Balloon Catheter Market

Market Size in USD Million

USD

895.18 Million

USD

1,561.24 Million

2024

2032

USD

895.18 Million

USD

1,561.24 Million

2024

2032

Forecast Period |

2025 - 2032 |

Market Size (Base Year) |

USD 895.18 Million |

Market Size (Forecast Year) |

USD 1,561.24 Million |

CAGR |

% |

Major Markets Players |

|

Asia-Pacific Balloon Catheter Market Size

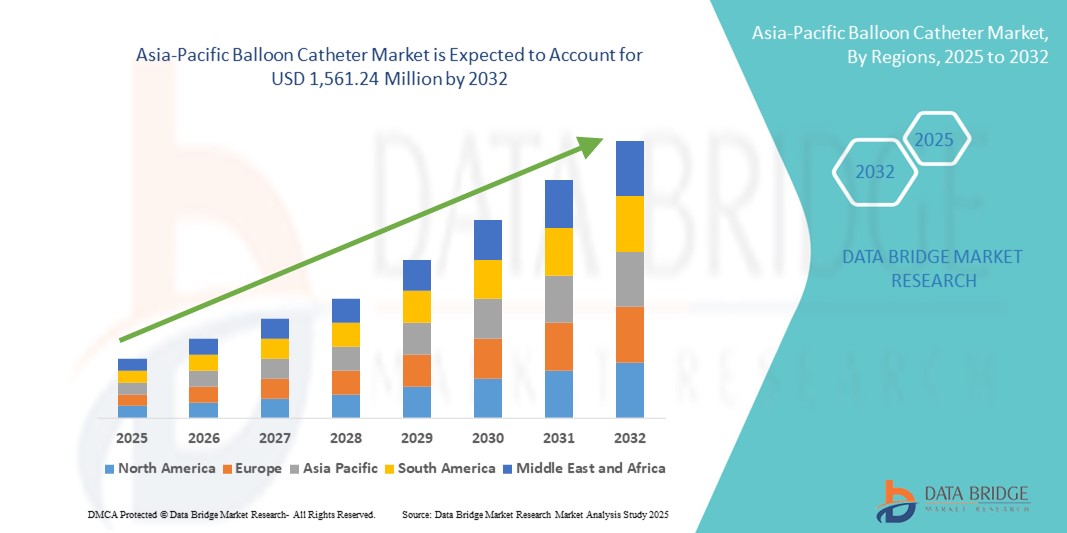

- The Asia-Pacific balloon catheter market size was valued at USD 895.18 million in 2024 and is expected to reach USD 1,561.24 million by 2032, at a CAGR of 7.20% during the forecast period

- The market growth is primarily driven by the rising prevalence of cardiovascular diseases, peripheral artery diseases, and urological conditions, alongside growing adoption of minimally invasive surgical procedures across emerging economies in the region

- Additionally, increased healthcare spending, expanding medical infrastructure, and a surge in geriatric population are prompting higher demand for advanced interventional tools like balloon catheters. These compounding factors are fostering robust growth in the Asia-Pacific market, making it a dynamic segment of the global balloon catheter industry

Asia-Pacific Balloon Catheter Market Analysis

- Balloon catheters, designed for minimally invasive procedures in cardiovascular and peripheral artery treatments, are becoming increasingly essential in Asia-Pacific’s clinical settings due to their precision, flexibility, and effectiveness in disease intervention across hospital and ambulatory care environments

- The escalating demand for balloon catheters is primarily fueled by the growing incidence of coronary artery disease, rising geriatric population, and the increasing shift toward less invasive procedures supported by advancing healthcare infrastructure in emerging economies

- China dominated the Asia-Pacific balloon catheter market with the largest revenue share of 35.6% in 2024, driven by rapid urban healthcare expansion, favorable regulatory support, and a growing number of interventional cardiology procedures, positioning the country as both a key consumer and manufacturer

- India is projected to be the fastest growing country in the Asia-Pacific balloon catheter market due to increasing healthcare accessibility, rising disposable incomes, and the growing prevalence of lifestyle-related chronic diseases

- The PTCA balloon catheter segment dominated the Asia-Pacific market with a market share of 45.7% in 2024, owing to its widespread use in angioplasty procedures and the region’s high burden of cardiovascular conditions

Report Scope and Asia-Pacific Balloon Catheter Market Segmentation

|

Attributes |

Asia-Pacific Balloon Catheter Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia-Pacific Balloon Catheter Market Trends

Shift Toward Minimally Invasive Interventions with Technological Advancements

- A key and accelerating trend in the Asia-Pacific balloon catheter market is the growing preference for minimally invasive procedures, supported by rapid technological advancements in catheter design and material innovation. This shift is reshaping treatment protocols in cardiovascular, urological, and peripheral vascular procedures across the region

- For instance, advancements in drug-eluting balloon (DEB) technology are enabling more targeted and efficient treatment of arterial blockages, especially in patients who are not ideal candidates for stenting. Companies such as Terumo and Medtronic are expanding their DEB portfolios across Asia-Pacific with improved drug delivery mechanisms and enhanced biocompatibility

- Innovations in high-pressure and scoring balloon catheters are addressing complex lesions and resistant plaques with higher precision, reducing procedural complications and improving patient outcomes

- Moreover, increased focus on using semi-compliant and non-compliant balloons for better vessel dilation control is gaining traction, particularly in complex angioplasty cases

- This trend is also complemented by a growing ecosystem of hybrid operating rooms and image-guided surgical tools across key Asia-Pacific economies, enhancing the accuracy and success of balloon catheter-based interventions

- The demand for technologically advanced balloon catheters is growing rapidly across hospitals and specialty centers, driven by clinicians’ preference for more precise, customizable, and safe treatment options especially in urban centers of China, India, and Japan

Asia-Pacific Balloon Catheter Market Dynamics

Driver

Rising Cardiovascular Disease Burden and Advancing Healthcare Infrastructure

- The rising prevalence of cardiovascular and peripheral artery diseases, combined with increasing adoption of minimally invasive treatment methods, is a major factor driving balloon catheter demand in Asia-Pacific

- For instance, in April 2024, Terumo Corporation expanded its local manufacturing capabilities in India, aiming to meet rising regional demand for coronary balloon catheters and related interventional devices. Such strategic moves by major players are propelling regional growth and accessibility

- Aging populations, changing lifestyles, and increasing rates of diabetes and hypertension are contributing to higher interventional cardiology volumes, particularly in China, Japan, and Southeast Asia

- Moreover, balloon catheters offer shorter recovery times, reduced procedural complications, and lower hospital stays compared to traditional surgeries—making them increasingly attractive to both patients and providers

- The growth of medical tourism, improved insurance coverage, and the establishment of specialized cardiac centers in emerging economies like Vietnam, Thailand, and Indonesia are further enhancing access to balloon catheter-based procedures, especially in the private healthcare segment

Restraint/Challenge

High Device Costs and Regulatory Compliance Barriers

- Despite rising demand, the high cost of advanced balloon catheter systems remains a key challenge, particularly for smaller healthcare facilities and price-sensitive markets within Asia-Pacific

- For instance, drug-eluting and specialty scoring or cutting balloon catheters often carry significantly higher price tags than traditional models, limiting widespread adoption in lower-income regions or rural areas

- Additionally, regulatory complexities and delays in product approvals can hinder market entry and expansion for international players. Countries such as China and India have stringent quality and clinical trial requirements, which can slow innovation deployment

- Furthermore, reimbursement limitations and a lack of skilled interventional cardiologists in underdeveloped areas may restrict patient access to advanced treatments

- Addressing these challenges through localized manufacturing, pricing strategies, clinical training programs, and faster regulatory harmonization will be critical for unlocking the full growth potential of the Asia-Pacific balloon catheter market

Asia-Pacific Balloon Catheter Market Scope

The market is segmented on the basis of type, product type, delivery platform, compliance, balloon material, balloon type, application, end user, and distribution channel.

- By Type

On the basis of type, the Asia-Pacific balloon catheter market is segmented into PTCA balloon catheters, CTO balloon catheters, and microcatheters. The PTCA balloon catheter segment dominated the market with the largest market revenue share of 45.7% in 2024, due to its widespread use in treating coronary artery disease and the rising volume of percutaneous coronary interventions across the region. PTCA catheters are favored for their reliability in angioplasty procedures, especially in hospitals with high interventional cardiology workloads.

The CTO balloon catheter segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by increasing adoption in complex coronary lesion management and technological advancements improving lesion crossing efficiency.

- By Product Type

On the basis of product type, the Asia-Pacific balloon catheter market is segmented into normal balloon catheter, drug eluting balloon catheter, cutting balloon catheter, stent graft balloon catheter, and scoring balloon catheter. The drug eluting balloon catheter segment held the largest market revenue share in 2024, driven by its effectiveness in preventing restenosis and reducing the need for permanent implants, particularly in small vessel disease and in-stent restenosis cases. Clinicians are increasingly adopting DEBs for their targeted drug delivery and favorable clinical outcomes.

The cutting balloon catheter segment is expected to witness the fastest CAGR from 2025 to 2032, as it gains traction in treating resistant and calcified plaques with greater precision and lesion preparation efficiency.

- By Delivery Platform

On the basis of delivery platform, the Asia-Pacific balloon catheter market is segmented into Rapid Exchange (RX) / Monorail balloon catheter, Over-The-Wire (OTW), and Fixed Wire (FW) balloon catheter. The Rapid Exchange (RX) balloon catheter segment dominated the market with the largest market revenue share in 2024, attributed to its procedural simplicity, single-operator usability, and faster device exchanges, especially in high-volume PCI centers.

The Over-The-Wire (OTW) segment is projected to witness the fastest growth during the forecast period, supported by its utility in complex procedures requiring enhanced pushability and wire support in long or tortuous lesions.

- By Compliance

On the basis of compliance, the Asia-Pacific balloon catheter market is segmented into non-compliant, semi-compliant, and compliant balloon catheters. The non-compliant balloon catheter segment held the largest market revenue share in 2024, due to its high-pressure dilation capabilities and ability to maintain shape under stress, making it suitable for post-dilatation and calcified lesions.

The semi-compliant segment is expected to register the fastest CAGR from 2025 to 2032, favored for its balance between flexibility and pressure response, making it adaptable to various lesion morphologies and commonly used in routine PCI procedures.

- By Balloon Material

On the basis of balloon material, the Asia-Pacific balloon catheter market is segmented into nylon, polyethylene terephthalate (PET), polyethylene (PE), silicone, polyolefin copolymer, and others. The polyethylene terephthalate (PET) segment held the largest market revenue share in 2024, driven by its superior strength, low compliance, and ability to maintain precise balloon dimensions under high pressure, particularly in complex coronary interventions.

The nylon segment is expected to grow at the fastest rate during forecast period, supported by its flexible handling characteristics and increasing adoption in semi-compliant balloon applications due to its enhanced deliverability and lower crossing profile.

- By Balloon Type

On the basis of balloon type, the Asia-Pacific balloon catheter market is segmented into high-pressure balloons and elastomeric balloons. The high-pressure balloon segment dominated the market with the largest market revenue share of 60% in 2024, due to its critical role in lesion preparation and post-stent expansion in complex coronary and peripheral procedures. High-pressure balloons are especially useful in treating heavily calcified or resistant blockages.

The elastomeric balloon segment is projected to grow at a steady pace during forecast period, driven by their flexible inflation profile, gentle vessel interaction, and usage in pediatric and neurovascular applications.

- By Application

On the basis of application, the Asia-Pacific balloon catheter market is segmented into coronary artery disease, peripheral artery disease, and others. The coronary artery disease segment dominated the market with the largest market revenue share of 55% in 2024, due to the high prevalence of heart disease, the increase in PCI procedures, and the widespread use of balloon catheters in diagnostic and therapeutic coronary interventions.

The peripheral artery disease segment is expected to witness the fastest growth, supported by growing awareness, better diagnosis, and the adoption of advanced balloon technologies for lower limb vascular therapies.

- By End User

On the basis of end user, the Asia-Pacific balloon catheter market is segmented into hospitals, specialty centers, ambulatory surgery centers, and others. The hospital segment dominated the market with the largest market revenue share of 60% in 2024, attributed to the concentration of advanced interventional equipment, skilled professionals, and high patient volumes in tertiary care and cardiac hospitals.

The specialty centers segment is anticipated to witness the fastest CAGR from 2025 to 2032, driven by the rising number of dedicated cardiovascular clinics and diagnostic centers offering cost-effective and specialized care, especially in urban and semi-urban areas.

- By Distribution Channel

On the basis of distribution channel, the Asia-Pacific balloon catheter market is segmented into direct tender, third party distribution, and others. The direct tender segment held the largest market revenue share in 2024, driven by bulk purchasing practices in government and large private hospitals, as well as contractual agreements with key manufacturers for consistent supply and cost control.

The third party distribution segment is expected to register the fastest growth rate during forecast period, supported by increasing penetration of distributors in smaller healthcare facilities, private clinics, and ambulatory surgery centers across emerging Asia-Pacific markets.

Asia-Pacific Balloon Catheter Market Regional Analysis

- China dominated the Asia-Pacific balloon catheter market with the largest revenue share of 35.6% in 2024, driven by rapid urban healthcare expansion, favorable regulatory support, and a growing number of interventional cardiology procedures, positioning the country as both a key consumer and manufacturer

- The country’s expanding hospital infrastructure, increasing number of catheterization labs, and the presence of leading domestic manufacturers offering cost-effective and technologically advanced balloon catheter solutions have significantly contributed to its dominance

- China’s focus on enhancing minimally invasive procedure capabilities and local production strengths further fuel its leading position in the regional market

The China Balloon Catheter Market Insight

China dominated the Asia-Pacific balloon catheter market with the largest revenue share in 2024, attributed to its large patient population, expanding healthcare infrastructure, and rising number of interventional cardiology procedures. Government investments in public health, along with a robust local manufacturing base and strong demand for technologically advanced medical devices, have significantly boosted market penetration. The growing adoption of high-pressure and drug-eluting balloon catheters, particularly in urban tertiary hospitals, is driving growth, supported by favorable reimbursement policies and clinical awareness.

India Balloon Catheter Market Insight

The India balloon catheter market is anticipated to grow at a notable CAGR during the forecast period, fueled by the increasing burden of coronary artery disease, growing healthcare investments, and expanding access to interventional treatments across urban and semi-urban areas. Rising public awareness, availability of cost-effective catheterization options, and increasing government focus on cardiovascular health under programs such as Ayushman Bharat are supporting market expansion. Additionally, the presence of domestic manufacturers offering affordable solutions is improving accessibility and supporting procedural volumes in both private and public hospitals.

Japan Balloon Catheter Market Insight

Japan’s balloon catheter market continues to advance steadily, supported by its aging population, advanced medical infrastructure, and high rate of cardiovascular diagnostics. The country demonstrates a strong preference for innovative and precision-based medical devices, including scoring and drug-eluting balloon catheters, especially in complex cases of peripheral and coronary artery disease. Integration of balloon catheter procedures into routine hospital care, along with a growing demand for minimally invasive and day-care interventional treatments, is bolstering market growth across major healthcare institutions.

South Korea Balloon Catheter Market Insight

The South Korea balloon catheter market is projected to expand at a promising CAGR during the forecast period, supported by the country’s highly developed healthcare infrastructure, strong focus on medical innovation, and growing incidence of lifestyle-related cardiovascular conditions. South Korea’s emphasis on early disease diagnosis and preventive healthcare has led to a rising number of interventional procedures utilizing balloon catheters. Additionally, the presence of leading local and international medical device companies, along with favorable reimbursement frameworks, is enhancing accessibility and driving market penetration across hospitals and ambulatory surgery centers.

Asia-Pacific Balloon Catheter Market Share

The Asia-Pacific Balloon Catheter industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Boston Scientific Corporation (U.S.)

- Abbott Laboratories (U.S.)

- BIOTRONIK SE & Co. KG (Germany)

- B. Braun SE (Germany)

- Terumo Corporation (Japan)

- Cordis Corporation (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Cook (U.S.)

- MicroPort Scientific Corporation (China)

- Lepu Medical Technology (Beijing) Co., Ltd. (China)

- Acrostak AG (Switzerland)

- Nipro Corporation (Japan)

- Balton Sp. z o.o. (Poland)

- Meril Life Sciences Pvt. Ltd. (India)

- iVascular S.L.U. (Spain)

- Hexacath France (France)

- AngioDynamics, Inc. (U.S.)

- Cardionovum GmbH (Germany)

- Alvimedica Medical Technologies Inc. (Turkey)

What are the Recent Developments in Asia-Pacific Balloon Catheter Market?

- In April 2024, Medtronic plc expanded its cardiovascular product offerings across Asia-Pacific by launching the latest generation of drug-coated balloon catheters in India and Southeast Asia. These devices are designed to improve outcomes in patients with peripheral artery disease (PAD), offering enhanced drug delivery efficiency and reduced restenosis rates. This regional launch reflects Medtronic’s strategy to localize advanced medical technologies, improve accessibility, and address growing cardiovascular health challenges in emerging Asian markets

- In March 2024, Boston Scientific Corporation announced the successful acquisition of a local Chinese catheter manufacturer to strengthen its supply chain and product customization capabilities for the Asia-Pacific region. This strategic move enables Boston Scientific to enhance its responsiveness to local clinical demands, accelerate innovation tailored to regional needs, and improve affordability through localized production, reinforcing its commitment to expanding its presence in China and beyond

- In March 2024, Terumo Corporation launched its next-generation scoring balloon catheter system in Japan and South Korea, focusing on treating complex coronary artery lesions. The product features enhanced trackability and lesion modification capabilities, addressing unmet needs in complex interventional cardiology. This development underscores Terumo's leadership in minimally invasive cardiovascular technologies and its ongoing investment in R&D to support regional cardiologists with precision tools

- In February 2024, B. Braun Melsungen AG initiated a strategic partnership with multiple healthcare providers in Thailand and Vietnam to implement training programs on advanced balloon catheter techniques. These collaborations aim to improve procedural outcomes by equipping interventionalists with the latest skills and product knowledge. This initiative highlights B. Braun’s dedication to capacity-building and supporting clinical excellence across developing markets in Asia-Pacific

- In January 2024, Abbott Laboratories expanded its distribution network across Australia and New Zealand, introducing a new line of semi-compliant balloon catheters for coronary angioplasty. These devices are designed to provide optimized lesion preparation and support complex PCI procedures. The move supports Abbott's strategy to scale its presence in developed Asia-Pacific markets while offering clinicians high-performance tools to meet evolving procedural demands

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.