Asia Pacific Bio Implants Market

Market Size in USD Billion

USD

3.40 Billion

USD

6.62 Billion

2025

2033

USD

3.40 Billion

USD

6.62 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.40 Billion | |

| USD 6.62 Billion | |

| % | |

|

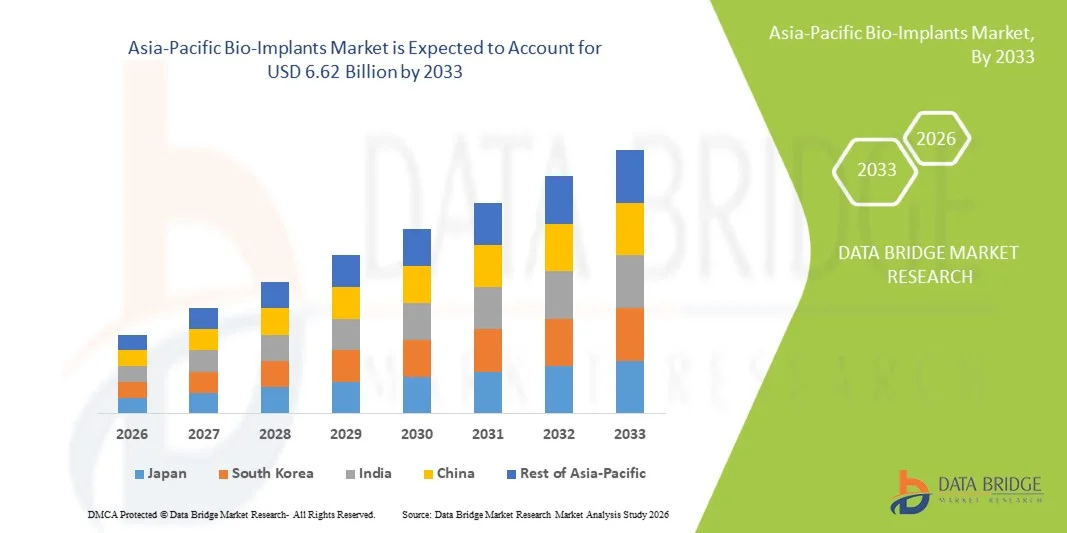

Asia-Pacific Bio-Implants Market Size

- The Asia-Pacific bio-implants market size was valued at USD 3.40 billion in 2025 and is expected to reach USD 6.62 billion by 2033, at a CAGR of 8.7% during the forecast period

- The market growth is largely driven by the increasing prevalence of orthopedic, cardiovascular, and dental disorders across the region, coupled with rising awareness about advanced medical treatment options and post-surgical recovery solutions

- Furthermore, growing healthcare infrastructure investments, rising geriatric population, and rapid adoption of advanced implantable devices are establishing bio-implants as an essential component of modern medical interventions. These converging factors are accelerating the uptake of bio-implant solutions, thereby significantly boosting the industry's growth in Asia-Pacific

Asia-Pacific Bio-Implants Market Analysis

- Bio-implants, including orthopedic, dental, cardiovascular, and neurostimulator implants, are increasingly vital components of modern medical treatment and surgical interventions in both hospitals and specialized clinics due to their ability to restore function, enhance patient outcomes, and integrate with advanced surgical technologies

- The escalating demand for bio-implants is primarily fueled by the rising prevalence of orthopedic disorders, cardiovascular diseases, and dental conditions, along with growing awareness of minimally invasive procedures and advanced implantable solutions

- Japan dominated the Asia-Pacific bio-implants market with the largest revenue share of 25.9% in 2025, characterized by advanced healthcare infrastructure, high adoption of medical technologies, and a strong presence of key industry player

- India is expected to be the fastest-growing country in the Asia-Pacific bio-implants market during the forecast period due to rising healthcare spending, expanding hospital networks, and greater accessibility of advanced implantable medical devices

- Orthopaedics and Trauma segment dominated the Asia-Pacific bio-implants market with a market share of 40% in 2025, driven by their critical role in fracture management, joint replacement procedures, and the region’s increasing incidence of bone-related disorders

Report Scope and Asia-Pacific Bio-Implants Market Segmentation

|

Attributes |

Asia-Pacific Bio-Implants Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Bio-Implants Market Trends

“Advancements in Minimally Invasive and AI-Enabled Surgical Implants”

- A significant and accelerating trend in the Asia-Pacific bio-implants market is the increasing adoption of minimally invasive surgical techniques and AI-assisted implant procedures, which are enhancing precision, reducing recovery time, and improving patient outcomes

- For instance, AI-assisted orthopedic implants can optimize implant positioning during joint replacement surgeries, improving alignment and long-term functionality. Similarly, robotic-assisted spinal implants are enabling more accurate screw placements with minimal tissue damage

- AI integration in implant planning allows surgeons to simulate procedures virtually, predict post-surgical outcomes, and tailor implants to patient-specific anatomy, enhancing the safety and effectiveness of treatments. Furthermore, implantable devices with smart sensor capabilities can monitor healing and provide real-time data to clinicians

- The seamless integration of bio-implants with advanced imaging, navigation, and robotic platforms allows centralized control over surgical procedures and post-operative monitoring, improving workflow efficiency and clinical decision-making

- This trend towards more intelligent, precise, and patient-customized implants is fundamentally reshaping expectations for surgical care. Consequently, companies such as Medtronic and Stryker are developing AI-enabled and sensor-integrated implants to optimize patient outcomes

- The demand for minimally invasive, AI-enhanced, and personalized bio-implant solutions is growing rapidly across hospitals and specialty clinics, as healthcare providers increasingly prioritize better recovery, safety, and long-term functionality

- Growing investments in R&D for smart implants with integrated biosensors and IoT connectivity are enabling continuous post-surgical monitoring and predictive health analytics, enhancing long-term patient care and driving market adoption

Asia-Pacific Bio-Implants Market Dynamics

Driver

“Rising Prevalence of Orthopedic, Dental, and Cardiovascular Disorders”

- The increasing incidence of bone fractures, joint disorders, cardiovascular diseases, and dental issues, coupled with rising awareness of advanced implantable treatments, is a significant driver of bio-implant demand in Asia-Pacific

- For instance, in March 2025, Stryker announced the launch of its AI-assisted knee replacement implant in India, aiming to enhance procedural accuracy and patient outcomes. Such innovations by leading companies are expected to accelerate market growth during the forecast period

- As populations age and the geriatric demographic expands, bio-implants provide critical solutions for mobility, cardiovascular health, and oral rehabilitation, offering compelling benefits over conventional treatment methods

- Furthermore, expanding healthcare infrastructure, government initiatives to improve surgical care accessibility, and increasing private hospital networks are making bio-implants more widely available across the region

- The availability of customized implants, digital surgical planning, and post-operative monitoring technologies are key factors driving adoption in hospitals, specialty clinics, and rehabilitation centers. The trend towards personalized patient care and minimally invasive interventions further contributes to market growth

- Rising awareness campaigns and educational programs targeting both healthcare professionals and patients are increasing acceptance and adoption of advanced implants across tier-2 and tier-3 cities in Asia-Pacific

- Government subsidies, insurance coverage expansion for implant procedures, and public-private partnerships in healthcare are further facilitating market penetration and driving sustained growth across the region

Restraint/Challenge

“High Costs and Regulatory Compliance Barriers”

- The high cost of advanced bio-implant devices, including AI-assisted and sensor-integrated implants, remains a key challenge to wider adoption in price-sensitive markets across Asia-Pacific

- For instance, premium orthopedic implants with navigation and robotic assistance are often unaffordable for smaller hospitals or mid-income patients, limiting market penetration in developing countries

- Stringent regulatory requirements, including approvals from national health authorities, clinical trials, and adherence to ISO and FDA standards, create barriers for new entrants and can delay product launches. In addition, variations in regulatory frameworks across countries complicate market entry

- While some cost-effective implant alternatives are emerging, the perceived high premium for technologically advanced bio-implants can still restrict adoption among healthcare providers with limited budgets

- Overcoming these challenges through improved cost-efficiency, faster regulatory approvals, local manufacturing, and clinician education will be vital for sustaining market growth in Asia-Pacific

- Lack of trained surgeons and clinical specialists capable of handling advanced implant procedures, particularly in rural and semi-urban regions, can slow adoption and limit market expansion

- Concerns regarding long-term implant safety, potential post-operative complications, and limited awareness about proper implant usage among patients can hinder confidence and delay widespread acceptance

Asia-Pacific Bio-Implants Market Scope

The market is segmented on the basis of product type, type of graft, material, mode of administration, and end-user.

- By Product Type

On the basis of product type, the Asia-Pacific bio-implants market is segmented into orthopaedics and trauma, pacing devices, stents and related implants, spinal implants, ophthalmic implants, structural cardiac implants, dental implants, neurostimulators implants, and prosthetic implants. Orthopaedics and Trauma dominated the market with the largest revenue share of 40% in 2025, driven by the rising prevalence of fractures, joint disorders, and bone-related injuries across the region. Hospitals and clinics prefer advanced implants such as plates, screws, and joint replacements for their proven effectiveness and long-term durability. The adoption of minimally invasive techniques and AI-assisted surgical planning further enhances procedural accuracy and patient recovery outcomes. Moreover, orthopaedic implants benefit from strong insurance coverage and government healthcare initiatives in countries such as Japan, China, and India. The segment also sees high adoption due to the aging population and increasing incidence of sports-related injuries. Customizable implants and growing awareness of early intervention further contribute to market leadership.

Dental Implants are anticipated to witness the fastest growth rate of 12% CAGR from 2026 to 2033, fueled by increasing awareness of oral health, cosmetic dentistry, and rising disposable incomes in urban Asia-Pacific regions. Dental implants restore functionality and aesthetics, offering a long-term solution for missing teeth. Technological advances such as 3D printing and digital planning allow patient-specific implants, enhancing outcomes. Clinics and hospitals are increasingly adopting modern implant systems integrated with guided surgery and AI planning. The growth is also supported by government programs promoting oral healthcare and insurance coverage expansion in developing countries.

- By Type

On the basis of type, the market is segmented into allograft, autograft, xenograft, and synthetic. Autograft dominated the market in 2025 due to its superior biocompatibility, lower risk of rejection, and faster integration with the patient’s own tissue. Surgeons prefer autografts for critical procedures such as spinal fusion and bone reconstruction. The segment’s dominance is supported by established surgical protocols and positive clinical outcomes. Availability of advanced harvesting techniques further encourages use in hospitals and specialized centers.

Synthetic grafts are expected to witness the fastest CAGR during 2026–2033, driven by advancements in biomaterials, polymers, and composites that mimic natural tissue properties. Synthetic implants reduce donor-site morbidity and allow customization for patient-specific anatomy. Growth is further supported by R&D investments in bioactive coatings, hydrogels, and 3D-printed implants. These grafts are increasingly adopted in both orthopaedic and dental applications, especially in regions with limited access to donor tissues.

- By Material

On the basis of material, the market is segmented into biomaterial metal, alloy, polymer, ceramics, and acrylic hydrogel. Alloy and Biomaterial Metal dominated the market in 2025 with a revenue share of 45%, favored for their mechanical strength, corrosion resistance, and reliability in load-bearing applications. Titanium and stainless steel implants are widely used in orthopaedic, dental, and spinal procedures. High adoption in hospitals is driven by proven clinical performance, regulatory approvals, and long-term safety records.

Polymer and Hydrogel-based implants are anticipated to witness the fastest growth rate during 2026–2033, driven by innovations in bioactive polymers, resorbable materials, and soft tissue-compatible hydrogels. These materials are increasingly used in dental, ophthalmic, and neurostimulator implants, offering advantages such as reduced inflammation and faster tissue integration. The growth is supported by technological developments in 3D printing and customization for patient-specific applications.

- By Mode of Administration

On the basis of administration, the market is segmented into surgical and non-surgical. Surgical implants dominated the market in 2025 due to their necessity for complex procedures such as joint replacements, cardiac stent placements, spinal fusion, and trauma management. The high adoption is supported by hospitals and surgical centers equipped with advanced operating rooms, robotics, and AI-guided systems. Surgical implants provide predictable outcomes and are often covered under insurance policies, further strengthening market dominance.

Non-surgical implants are expected to witness the fastest growth during 2026–2033, fueled by minimally invasive techniques, outpatient procedures, and demand for faster recovery times. Examples include certain cardiac pacing devices, neuromodulators, and injectable bone substitutes. The convenience, reduced hospitalization, and lower procedural risk drive adoption in clinics and ambulatory centers. Adoption is further supported by clinics and ambulatory surgical centers offering advanced non-surgical implant procedures.

- By End-User

On the basis of end-user, the market is segmented into clinics, hospitals, and ambulatory surgical centres (ASCs). Hospitals dominated the market in 2025 with a share of 50%, driven by the availability of advanced surgical facilities, trained specialists, and infrastructure capable of handling complex implant procedures. Hospitals are the preferred choice for high-risk surgeries, complex trauma cases, and multi-disciplinary procedures. The segment also benefits from insurance coverage and public health programs supporting advanced implant adoption.

Clinics and ASCs are expected to witness the fastest growth during 2026–2033, as outpatient procedures, minimally invasive surgeries, and smaller-scale implant interventions become more common. The trend is fueled by cost-effectiveness, shorter recovery times, and increasing adoption of portable and AI-assisted implant technologies suitable for decentralized healthcare delivery. Rising investments in primary care and specialty clinics further accelerate growth in these segments. Rising awareness of same-day implant procedures across Europe accelerates market expansion.

Asia-Pacific Bio-Implants Market Regional Analysis

- Japan dominated the Asia-Pacific bio-implants market with the largest revenue share of 25.9% in 2025, characterized by advanced healthcare infrastructure, high adoption of medical technologies, and a strong presence of key industry player

- Patients and healthcare providers in the region highly value the improved clinical outcomes, minimally invasive procedures, and long-term reliability offered by advanced bio-implants, including AI-assisted orthopedic, spinal, and dental implants

- This widespread adoption is further supported by strong government healthcare initiatives, expanding hospital networks, growing geriatric populations, and increasing awareness of implant-based treatments, establishing bio-implants as essential solutions in both hospitals and specialty clinics across the Asia-Pacific region

The China Bio-Implants Market Insight

The China bio-implants market is gaining momentum due to the country’s rapidly aging population, rising incidence of chronic diseases, and strong healthcare modernization programs. Advanced orthopedic, dental, and cardiovascular implants are increasingly adopted in hospitals and specialty clinics. The integration of AI-assisted surgical planning, 3D-printed patient-specific implants, and minimally invasive procedures is fueling growth. Moreover, expanding medical device manufacturing capabilities and government support for high-quality healthcare are enhancing the availability and affordability of bio-implants across urban and semi-urban regions.

Japan Bio-Implants Market Insight

The Japan bio-implants market is expanding steadily due to high healthcare standards, technological advancements, and the country’s focus on precision medicine. The adoption of AI-assisted, sensor-integrated, and minimally invasive implants is increasing, particularly in orthopedics, spinal procedures, and cardiac devices. Japan’s aging population drives demand for implants that improve mobility and quality of life. Hospitals and specialized clinics are integrating advanced imaging, robotic surgery, and digital planning to enhance surgical outcomes. Furthermore, strong regulatory frameworks and high patient awareness support market growth.

India Bio-Implants Market Insight

The India bio-implants market accounted for one of the largest revenue shares in Asia-Pacific in 2025, driven by rising healthcare expenditure, rapid urbanization, and growing awareness of advanced implantable treatments. Hospitals and specialty clinics are increasingly adopting orthopedic, dental, and cardiovascular implants to meet rising patient demand. Government initiatives toward universal healthcare, expansion of medical infrastructure, and support for private sector hospitals are further bolstering growth. In addition, domestic manufacturing of affordable implants, combined with increasing adoption of minimally invasive surgeries, is propelling the market in India across both urban and semi-urban areas.

South Korea Bio-Implants Market Insight

The South Korea bio-implants market is witnessing strong growth due to the country’s advanced healthcare infrastructure, high adoption of medical technology, and increasing patient demand for orthopedic, dental, and cardiovascular implants. Hospitals and specialty clinics are integrating robotic-assisted surgeries, AI-enabled planning, and minimally invasive procedures to improve patient outcomes. Rising geriatric population and higher healthcare spending are driving the need for long-lasting and technologically advanced implants. Furthermore, South Korea’s government initiatives to promote precision medicine and medical device innovation, along with strong domestic and international manufacturer presence, are boosting market expansion across urban and semi-urban regions.

Asia-Pacific Bio-Implants Market Share

The Asia-Pacific Bio-Implants industry is primarily led by well-established companies, including:

- Stryker (U.S.)

- Medtronic (U.S.)

- Boston Scientific Corporation (U.S.)

- Abbott (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Zimmer Biomet (U.S.)

- BioHorizons Implant Systems Incorporated (U.S.)

- Glidewell Dental (U.S.)

- Envista Holdings Corporation (U.S.)

- Implant Direct (U.S.)

- LifeNet Health, Inc. (U.S.)

- Integra LifeSciences Corporation (U.S.)

- Globus Medical, Inc. (U.S.)

- Orthofix Medical Inc. (U.S.)

- RTI Surgical Holdings, Inc. (U.S.)

- NuVasive, Inc. (U.S.)

- Cook Medical LLC (U.S.)

- Smith+Nephew (U.S.)

- CONMED Corporation (U.S.)

What are the Recent Developments in Asia-Pacific Bio-Implants Market?

- In October 2025, MedTech Innovator Asia Pacific announced the four finalists for its 7th annual accelerator program, highlighting breakthrough technologies in neuromodulation, surgical robotics, cardiac monitoring, and personalized implants from startups across the region, demonstrating Asia‑Pacific’s growing medtech innovation ecosystem and support for early‑stage implantable technologies

- In September 2025, Zimmer Biomet secured regulatory approval from Japan’s PMDA for the first orthopedic hip implants featuring infection‑preventing iodine surface technology, marking a significant breakthrough in joint replacement solutions that aim to reduce post‑surgical infections and improve long‑term patient outcomes in a region with an aging population

- In February 2025, Biotronik announced a strategic shift to strengthen its focus on active implantable devices and digital health solutions in the Asia‑Pacific region, including planned divestiture of its Vascular Intervention portfolio to Teleflex, aimed at accelerating investment into next‑generation implant technologies with AI‑enabled remote monitoring capabilities

- In January 2025, Stryker launched the Insignia Hip Stem in India, a 3D‑modelled hip implant designed for total hip and hemiarthroplasty procedures that leverages patient‑specific CT data to enhance surgical fit, precision, and outcomes, expanding advanced orthopedic implant options in the Asia‑Pacific region

- In September 2024, Regenity Biosciences received regulatory approval from China’s National Medical Products Administration for its novel crosslinked bioresorbable implantable collagen dental membrane, marking the company’s first dental product approval in China and enabling commercialization across oral surgical procedures such as guided bone regeneration in periodontal treatments

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.