Asia Pacific Chemical Surface Treatment Market

Market Size in USD Million

USD

421.63 Million

USD

746.38 Million

2025

2033

USD

421.63 Million

USD

746.38 Million

2025

2033

| 2026 - 2033 | |

| USD 421.63 Million | |

| USD 746.38 Million | |

| % | |

|

Asia-Pacific Chemical Surface Treatment Market Overview

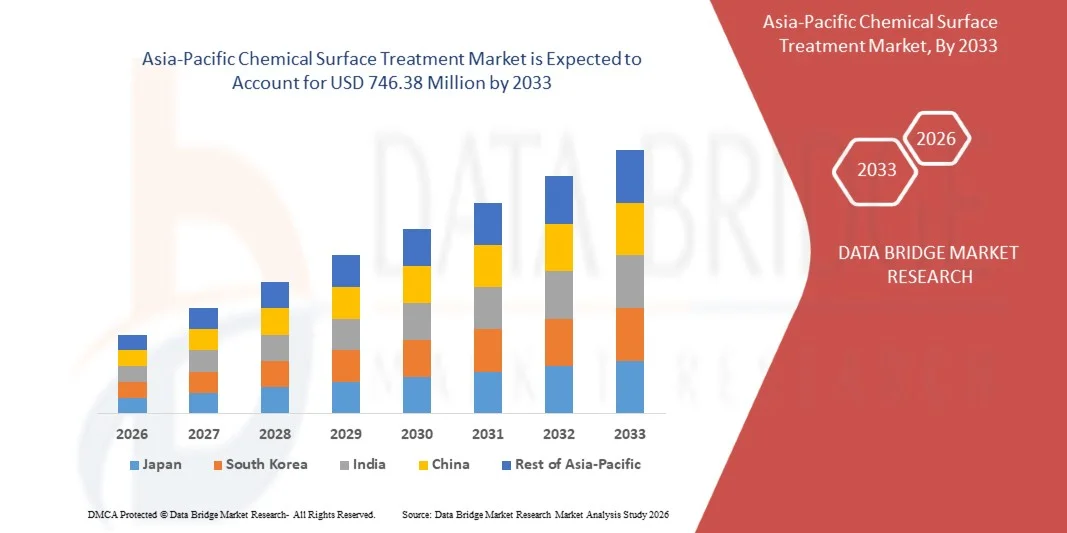

As per Data Bridge Market Research analysis the Asia-Pacific chemical surface treatment market was valued at USD 421.63 Million in 2025 and is projected to reach USD 746.38 Million by 2033, growing at a CAGR of 7.40% from 2026 to 2033. The market is experiencing consistent growth driven by strong industrialization across China, India, Japan, and Southeast Asia, rising demand from automotive and electronics manufacturing, and increasing use of advanced corrosion protection and surface finishing solutions. Expanding metal processing industries, rapid growth in electric vehicle production, and continuous infrastructure development are further supporting market growth across the region.

The increasing focus on improving product durability, enhancing corrosion resistance, and meeting stringent environmental regulations is significantly driving adoption of chemical surface treatment solutions across multiple end-use industries. Manufacturers are increasingly shifting toward eco-friendly, low-VOC, and high-performance formulations to comply with tightening regulatory frameworks and sustainability goals. In addition, rising investments in advanced manufacturing technologies and growing demand for high-quality surface finishing in export-oriented industries are further accelerating market penetration across Asia-Pacific.

Key Market Trends & Insights

- China dominated the Asia-Pacific chemical surface treatment market with the largest revenue share of 45% in 2025, supported by its massive industrial manufacturing base, strong presence of automotive and electronics production clusters, and large-scale metal processing industries

- The metals segment led the market with a 78.4% share in 2025, driven by extensive use in automotive, construction, electronics, and heavy machinery industries across the region

- India is expected to be the fastest-growing country at a CAGR of 8.6% from 2026 to 2033, fueled by rapid industrialization, expanding automotive production, and strong growth in electronics manufacturing under government-led initiatives

- Corrosion Inhibitors are the fastest-growing application type, projected to register a CAGR of 13.2% from 2026 to 2033, supported by increasing need to extend asset life in marine, oil & gas, and infrastructure applications

- The plating chemicals segment dominated the product category with a 36.8% revenue share in 2025, led by strong demand from electronics manufacturing, automotive component finishing, and industrial machinery production across China, Japan, and South Korea

- Transportation accounted for 31.7% of the market in 2025, preferred by strong demand from automotive manufacturing hubs in China, Japan, South Korea, and India

- The Conversion Coating segment is the fastest-growing product category, with a CAGR of 12.6% from 2026 to 2033, driven by rising demand for lightweight materials protection in automotive and aerospace applications

Market Size & Forecast

- Global Market Value (2025): USD 421.63 Million

- Expected Market Value (2033): USD 746.38 Million

- Forecast CAGR (2026–2033): 7.40%

- Leading Country in 2025: China

- Fastest Growing Country: India

Report Scope and Asia-Pacific Chemical Surface Treatment Market Segmentation

|

Attributes |

Chemical Surface Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific |

|

Key Market Players |

· Element Solutions Inc (U.S.) · NOF Corporation (Japan) · Atotech (Germany) · Henkel AG & Co. KGaA (Germany) · Chemetall, Inc. (Germany) · Nihon Parkerizing Co., Ltd. (Japan) · PPG Industries, Inc. (U.S.) · Nippon Paint Holdings Co., Ltd. (Japan) · Solvay (Belgium) · OC Oerlikon Management AG (Switzerland) · McGean-Rohco Inc. (U.S.) · JCU CORPORATION (Japan) · Platform Specialty Products Corporation (U.S.) · Quaker Chemical Corporation (U.S.) |

|

Market Opportunities |

· EV Manufacturing Driving Advanced Surface Treatment Demand · Growth in Nano-Based and Smart Coating Technologies · Expansion of Industrial Base in Southeast Asia |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Asia-Pacific Chemical Surface Treatment Market Trends

Trend: Eco-Friendly Low-VOC Surface Treatment Adoption

Asia-Pacific chemical surface treatment market is witnessing a strong shift toward eco-friendly, low-VOC, and chromium-free formulations driven by tightening environmental regulations and sustainability targets. Automotive, electronics, and metal processing industries are increasingly replacing conventional hazardous chemistries with compliant surface treatment solutions to meet export standards and green manufacturing requirements. Demand is particularly strong in China, Japan, and South Korea, where industrial modernization programs are accelerating adoption of cleaner technologies.

Companies such as Henkel, through its BONDERITE solutions, and BASF’s Chemetall brand are actively expanding low-emission surface treatment portfolios across Asia-Pacific manufacturing hubs to support regulatory compliance and sustainable production.

Asia-Pacific Chemical Surface Treatment Market Dynamics

Key Market Driver: Rapid Industrialization in Automotive and Electronics Sectors

The rapid expansion of automotive manufacturing, electric vehicle production, and electronics assembly across Asia-Pacific is significantly driving demand for chemical surface treatment solutions. These industries require high-performance coatings for corrosion resistance, adhesion improvement, and durability enhancement in mass production environments. Growing industrial output in China, India, Vietnam, and Thailand further strengthens consumption of plating chemicals, conversion coatings, and pre-treatment solutions.

Major manufacturers such as Atotech (MKS Instruments), Nippon Paint Holdings, and PPG Industries are expanding production and supply capabilities in Asia-Pacific to cater to rising demand from automotive OEMs and electronics manufacturing clusters.

Key Restraint/Challenge: Strict Environmental Regulations Increasing Compliance Costs

Stringent environmental regulations on hazardous chemicals, wastewater discharge, and volatile organic compounds are increasing compliance costs for surface treatment chemical manufacturers across Asia-Pacific. Regulatory frameworks in China, Japan, and South Korea are pushing companies to invest in cleaner production technologies and reformulate traditional chemical processes, raising operational complexity. Small and mid-sized manufacturers face challenges in upgrading infrastructure to meet evolving environmental standards.

For instance, regulatory tightening under China’s environmental protection policies has forced several industrial chemical producers to shift toward chromium-free and water-based surface treatment solutions, increasing R&D and production costs across the value chain.

Key Market Opportunity: Growth in Nano-Based and Smart Coating Technologies

Advancements in nano-coatings, self-healing surfaces, and smart corrosion protection systems are creating significant growth opportunities in the Asia-Pacific chemical surface treatment market. These technologies offer enhanced durability, reduced maintenance costs, and improved performance for high-value applications in aerospace, automotive, and electronics industries. Increasing R&D investments are accelerating commercialization of next-generation surface treatment chemistries.

Companies such as Solvay and NOF Corporation are actively developing advanced nano-structured surface treatment solutions, while regional collaborations with electronics and automotive manufacturers are accelerating adoption of smart coating technologies across Asia-Pacific industrial sectors.

Asia-Pacific Chemical Surface Treatment Market Scope

The chemical surface treatment market is segmented on the basis of product, base, application, and end user.

- By Product

On the basis of product, the Asia-Pacific Chemical Surface Treatment market is segmented into plating chemicals, conversion coating, activating agents, paint strippers, cleaners, metal working fluids, and others. The Plating Chemicals segment dominated the market with the largest share of 36.8% in 2025, driven by strong demand from electronics manufacturing, automotive component finishing, and industrial machinery production across China, Japan, and South Korea. High usage of electroplating and electroless plating processes in corrosion resistance and surface durability applications further strengthens segment leadership. Rapid industrial output and export-oriented manufacturing ecosystems continue to support large-scale consumption. Continuous investments in high-performance coating chemistries reinforce its dominant position.

The Conversion Coating segment is projected to register the fastest growth at a CAGR of 12.6% from 2026 to 2033, driven by rising demand for lightweight materials protection in automotive and aerospace applications. Increasing adoption of eco-friendly, low-VOC surface treatment solutions is accelerating substitution of traditional coating methods. Expanding electric vehicle production is further boosting demand for advanced surface preparation technologies. Strong regulatory focus on reducing hazardous chemical usage is pushing manufacturers toward conversion-based processes. Growing industrial modernization across India and Southeast Asia is further supporting segment expansion.

- By Base

On the basis of base, the Asia-Pacific Chemical Surface Treatment market is segmented into metals, plastics, wood, and other materials. The Metals segment dominated the market with a share of 78.4% in 2025, driven by extensive use in automotive, construction, electronics, and heavy machinery industries across the region. High requirement for corrosion resistance, surface hardness, and improved adhesion in metal components significantly strengthens adoption. Large-scale steel and aluminum processing industries in China, India, and Japan further reinforce demand. Continuous industrial expansion and infrastructure development sustain the dominance of this segment.

The Plastics segment is projected to register the fastest growth at a CAGR of 11.8% from 2026 to 2033, driven by increasing use of engineered plastics in automotive interiors, consumer electronics, and medical devices. Rising demand for lightweight and durable materials is accelerating surface treatment adoption to improve coating adhesion and performance. Expanding electronics manufacturing across Southeast Asia is further boosting usage. Advancements in plasma and chemical etching technologies are improving treatment efficiency for plastics. Growing substitution of metals with high-performance polymers continues to support strong segment growth.

- By Application

On the basis of application, the Asia-Pacific Chemical Surface Treatment market is segmented into metals coloring, corrosion inhibitors, post treatment, pre-treatment cleaners, pre-treatment conditioners, decorative, plating, and others. The Pre-treatment Cleaners segment dominated the market with a share of 29.5% in 2025, driven by its essential role in ensuring surface readiness across metal fabrication and manufacturing industries. Strong demand from automotive and electronics sectors for defect-free coating adhesion reinforces segment leadership. Increasing industrial quality standards across China and Japan further supports adoption. High-volume usage in mass production environments strengthens its dominant position. Continuous expansion of manufacturing output sustains long-term demand.

The Corrosion Inhibitors segment is projected to register the fastest growth at a CAGR of 13.2% from 2026 to 2033, driven by increasing need to extend asset life in marine, oil & gas, and infrastructure applications. Rising exposure of industrial equipment to harsh environmental conditions is accelerating protective chemical usage. Expanding offshore and coastal industrial projects in Southeast Asia are further supporting adoption. Technological advancements in nano-based and smart inhibitor formulations are improving efficiency. Growing focus on maintenance cost reduction across heavy industries continues to drive segment expansion.

- By End-User

On the basis of end-user, the Asia-Pacific Chemical Surface Treatment market is segmented into building and construction, transportation, aerospace and defence, non-ferrous metal, household appliances, general industry, industrial machinery, electronics, paints and coatings, and others. The Transportation segment dominated the market with a share of 31.7% in 2025, driven by strong demand from automotive manufacturing hubs in China, Japan, South Korea, and India. High usage of surface treatment chemicals for corrosion resistance, durability enhancement, and aesthetic finishing supports segment leadership. Rapid expansion of electric vehicle production further strengthens consumption of advanced surface treatment solutions. Strong export-oriented automotive supply chains reinforce large-scale adoption. Continuous innovation in lightweight vehicle materials sustains dominance.

The Aerospace and Defence segment is projected to register the fastest growth at a CAGR of 13.5% from 2026 to 2033, driven by increasing aircraft production and defense modernization programs across Asia-Pacific economies. Rising demand for high-performance coatings and advanced surface protection in extreme operating conditions is accelerating adoption. Expanding investments in indigenous aerospace manufacturing in India and China further support growth. Stringent safety and durability standards are pushing use of specialized treatment chemicals. Continuous technological advancements in corrosion-resistant and high-temperature coatings reinforce segment expansion.

Asia-Pacific Chemical Surface Treatment Market Regional Analysis

China dominated the chemical surface treatment market and accounted for the largest revenue share of 45% in 2025, driven by its massive industrial manufacturing base, strong presence of automotive and electronics production clusters, and large-scale metal processing industries. High consumption of surface treatment chemicals across automotive components, consumer electronics, and heavy machinery significantly reinforces its leadership position. Government-backed industrial modernization programs and strict environmental compliance standards are further pushing adoption of advanced, eco-friendly surface treatment solutions. The presence of major domestic chemical manufacturers, combined with strong export-oriented production networks, continues to strengthen China’s dominant position across the region. Expanding investments in smart manufacturing and high-performance coatings further consolidate market penetration.

Japan Chemical Surface Treatment Market Insight

The Japan market is anticipated to grow steadily from 2026 to 2033, supported by its highly advanced manufacturing ecosystem and strong focus on precision engineering in automotive, aerospace, and electronics sectors. Increasing demand for high-performance, corrosion-resistant, and environmentally compliant surface treatment chemicals is driving consistent adoption across industrial applications. Japanese manufacturers are prioritizing low-emission and high-durability formulations in line with stringent environmental regulations. Continuous R&D investments in nano-coatings and advanced conversion technologies are further enhancing product efficiency. Strong collaboration between chemical producers and end-use industries ensures stable and technology-driven market expansion.

India Chemical Surface Treatment Market Insight

India is projected to register the fastest CAGR of 8.6% in the Asia-Pacific Chemical Surface Treatment market during 2026–2033, driven by rapid industrialization, expanding automotive production, and strong growth in electronics manufacturing under government-led initiatives. Rising infrastructure development and increasing demand for corrosion protection in construction and transportation sectors are significantly boosting chemical consumption. Growing awareness of surface quality enhancement and increasing adoption of modern manufacturing techniques are accelerating market penetration. Expanding presence of global chemical companies and rapid growth of domestic production capabilities are improving supply accessibility. Strong policy support for “Make in India” initiatives and rising exports further reinforce India’s position as the fastest-growing market in the region.

Asia-Pacific Chemical Surface Treatment Market Share

The chemical surface treatment industry is primarily led by well-established companies, including:

- Element Solutions Inc (U.S.)

- NOF Corporation (Japan)

- Atotech (Germany)

- Henkel AG & Co. KGaA (Germany)

- Chemetall, Inc. (Germany)

- Nihon Parkerizing Co., Ltd. (Japan)

- PPG Industries, Inc. (U.S.)

- Nippon Paint Holdings Co., Ltd. (Japan)

- Solvay (Belgium)

- OC Oerlikon Management AG (Switzerland)

- McGean-Rohco Inc. (U.S.)

- JCU CORPORATION (Japan)

- Platform Specialty Products Corporation (U.S.)

- Quaker Chemical Corporation (U.S.)

Latest Developments in Asia-Pacific Chemical Surface Treatment Market

- In March 2025, Henkel expanded its surface treatment portfolio in Asia-Pacific by launching an upgraded range of low-VOC conversion coating and pre-treatment solutions under its BONDERITE brand across China and India. This development strengthens Henkel’s positioning in environmentally compliant surface treatment technologies, supporting rising demand from automotive and electronics manufacturers. The expansion enhances supply chain responsiveness and improves adoption of sustainable chemical formulations in the region’s fast-growing industrial base

- In September 2024, PPG Industries commissioned a new advanced surface treatment and coatings innovation center in Singapore focused on high-performance chemical solutions for aerospace and industrial applications. This investment enhances the company’s R&D capabilities in corrosion-resistant and lightweight material treatments, accelerating product customization for Asia-Pacific manufacturers. The facility is expected to strengthen regional innovation pipelines and improve commercialization of next-generation surface treatment chemistries

- In May 2023, Nippon Paint Holdings expanded its industrial coatings and surface treatment chemical production capacity in Vietnam to support growing demand from automotive component and electronics manufacturing hubs in Southeast Asia. This expansion improves regional supply availability and reduces dependency on imports for high-performance surface treatment solutions. It also strengthens the company’s competitiveness in fast-growing ASEAN industrial markets by enabling faster delivery and localized formulation development

- In November 2022, BASF inaugurated its largest surface treatment site under the Chemetall brand in Pinghu City, Zhejiang Province, China. This facility spans 60,000 square meters and significantly enhances production capacity to meet rising regional demand for high-performance surface treatment chemicals. The expansion strengthens BASF’s ability to serve automotive, electronics, and industrial manufacturing sectors while improving supply chain efficiency across Asia-Pacific markets

- In July 2022, DIC Corporation completed the acquisition of Guangdong TOD New Materials Co. Ltd, a Chinese chemical coating resin manufacturer based in Guangdong Province. This acquisition supports backward integration by strengthening DIC’s raw material control and enhancing its surface treatment chemical portfolio. It improves cost efficiency, supply chain stability, and competitive positioning in China’s rapidly expanding coatings and surface treatment market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Asia Pacific Chemical Surface Treatment Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Asia Pacific Chemical Surface Treatment Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Asia Pacific Chemical Surface Treatment Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.