Asia Pacific Cloud Storage Market

Market Size in USD Billion

USD

25.68 Billion

USD

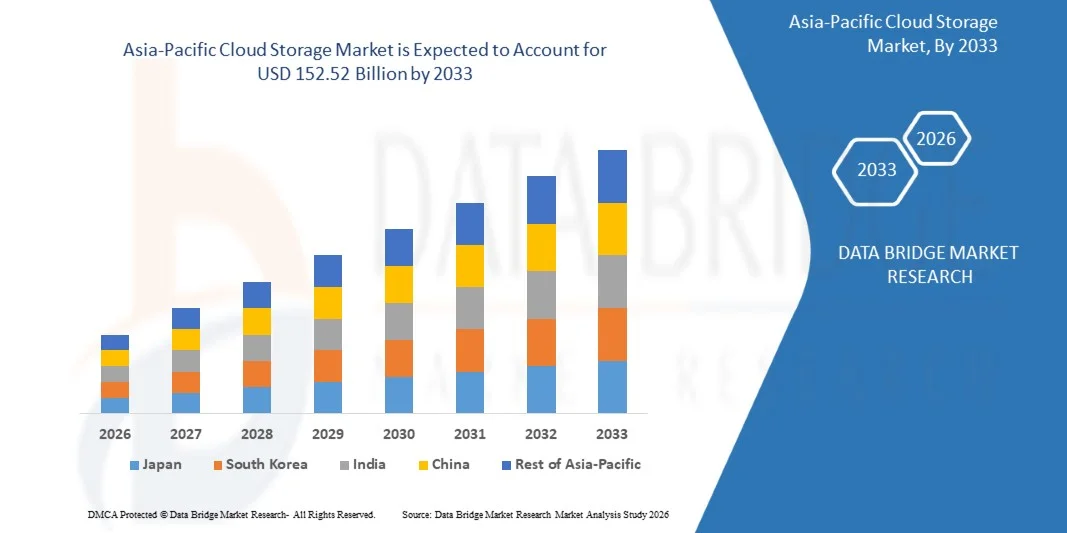

152.52 Billion

2025

2033

USD

25.68 Billion

USD

152.52 Billion

2025

2033

| 2026 - 2033 | |

| USD 25.68 Billion | |

| USD 152.52 Billion | |

| % | |

|

Asia-Pacific Cloud Storage Market Overview

The Asia-Pacific cloud storage market was valued at USD 25.68 billion in 2025 and is projected to reach USD 152.52 billion by 2033, growing at a CAGR of 24.94% from 2026 to 2033. The market is witnessing rapid expansion driven by accelerating digital transformation across enterprises, rising adoption of hybrid and multi-cloud environments, and increasing demand for scalable and cost-efficient data storage solutions.

The growth of the market is further supported by the exponential increase in data generation from smartphones, IoT devices, and enterprise applications, along with strong investments in cloud infrastructure by regional technology providers. In addition, the shift toward remote work models, growing e-commerce penetration, and government-led digitalization initiatives across emerging economies are significantly boosting the adoption of cloud storage services across the Asia-Pacific region.

Key Market Trends & Insights

- China dominated the Asia-Pacific cloud storage market with the largest revenue share of approximately 32.7% in 2025, supported by large-scale data center expansion, strong government-backed digital infrastructure programs, and rapid growth of cloud adoption across e-commerce, fintech, and industrial internet platforms.

- Japan is expected to be the fastest-growing region in the Asia-Pacific cloud storage market, recording a CAGR of 26.8% from 2026 to 2033. Growth is driven by increasing adoption of hybrid cloud models, rising enterprise digital transformation initiatives, and strong demand for secure and compliant data storage systems across manufacturing, automotive, and healthcare sectors.

- The Public Cloud Deployment segment held the largest market revenue share of approximately 58.4% in 2025 driven by strong adoption among SMEs and large enterprises due to lower infrastructure costs, high scalability, and faster deployment capabilities. Major industries such as e-commerce, BFSI, and media rely heavily on public cloud platforms for real-time data access and elastic storage capacity. Public cloud providers across Asia-Pacific are also expanding regional data center footprints to improve latency and ensure data localization compliance across key markets.

- The Hybrid Cloud Deployment segment is projected to register the fastest growth at a CAGR of 27.6% from 2026 to 2033, driven by increasing demand for data security, regulatory compliance, and flexible workload management across enterprises operating in multiple jurisdictions. Organizations are increasingly adopting hybrid models to balance cost efficiency with data sovereignty requirements, particularly in regulated industries such as banking and healthcare. The rising integration of edge computing with hybrid cloud architectures is further enhancing real-time data processing capabilities across distributed enterprise environments. Growing enterprise focus on disaster recovery and business continuity planning is also accelerating hybrid cloud adoption across Asia-Pacific.

- The Large Enterprise segment held the dominant market revenue share of approximately 65.7% in 2025 driven by high-volume data storage needs, advanced digital transformation initiatives, and widespread adoption of multi-cloud architectures across global enterprises operating in Asia-Pacific. These organizations generate and process massive datasets from customer transactions, analytics platforms, and enterprise applications. Large enterprises are also leading adopters of AI-driven storage optimization and automated data lifecycle management solutions.

- The Small Enterprise segment is projected to register the fastest growth at a CAGR of 26.9% from 2026 to 2033, driven by increasing affordability of cloud solutions, rising SaaS adoption, and government-led digitalization programs supporting SME cloud migration across emerging economies such as India, Vietnam, and Indonesia. Small businesses are rapidly shifting toward subscription-based cloud storage models to reduce upfront infrastructure investment. The expansion of digital payment systems and online business platforms is further accelerating cloud storage penetration among SMEs.

- The Banking, Financial Services and Insurance segment held the largest market share of approximately 24.1% in 2025 driven by strong demand for secure data storage, real-time transaction processing, and regulatory compliance requirements across digital banking ecosystems in Asia-Pacific. BFSI institutions are increasingly adopting cloud-native storage for fraud detection, risk analysis, and customer data management. Rising fintech adoption and digital banking expansion are further strengthening cloud storage demand in this segment.

- The Telecommunication segment accounted for approximately 18.6% share, supported by rapid 5G deployment and growing data traffic management needs across network infrastructure operators. Telecom companies are increasingly leveraging cloud storage for managing subscriber data, network analytics, and content delivery optimization. Expansion of 5G-enabled services is significantly increasing data storage requirements across Asia-Pacific telecom operators.

- The Software segment held the dominant market revenue share of approximately 70.2% in 2025 driven by strong demand for cloud storage platforms, data management solutions, and AI-enabled storage optimization tools across enterprises in Asia-Pacific. Software solutions are increasingly integrated with analytics, cybersecurity, and automation capabilities to enhance performance and data governance. Continuous innovation in cloud-native applications is further strengthening software dominance in the market.

- The Services segment accounted for approximately 29.8% share in 2025 and is projected to register steady growth, driven by increasing demand for cloud migration services, managed storage services, and ongoing maintenance and support requirements across enterprise cloud ecosystems. Organizations are increasingly relying on third-party service providers for seamless migration, integration, and optimization of cloud infrastructure. Rising complexity of multi-cloud environments is further boosting demand for professional and managed services across Asia-Pacific.

Market Size & Forecast

- Market Value (2025): USD 25.68 Billion

- Expected Market Value (2033): USD 152.52 Billion

- Forecast CAGR (2026–2033): 24.94%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Asia-Pacific Cloud Storage Market Segmentation

|

Attributes |

Asia-Pacific Cloud Storage Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

• Amazon Web Services, Inc. (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Asia-Pacific Cloud Storage Market Trends

Trend: Growth In Hybrid Cloud Adoption And Distributed Storage Architectures

Increasing demand for scalable, flexible, and cost-efficient data management solutions across enterprises, government institutions, and digital-native businesses is accelerating the shift from traditional on-premise storage systems to hybrid and multi-cloud environments. Conventional centralized storage infrastructure often faces limitations in scalability, latency, and disaster recovery, encouraging organizations to adopt distributed cloud storage models with improved redundancy and accessibility.

In modern enterprise environments, companies are increasingly integrating hybrid cloud storage systems, For instance combining private data centers with public cloud platforms to optimize workload distribution, enhance data security, and reduce operational costs while maintaining compliance with regional data governance regulations. In the e-commerce and fintech sectors, cloud-native storage architectures are being used to manage large-scale transactional data and customer analytics in real time, improving operational efficiency and decision-making speed.

The rapid expansion of artificial intelligence, IoT devices, and high-resolution media content is also driving exponential data generation, significantly increasing demand for scalable cloud storage infrastructure capable of handling unstructured and semi-structured data. In addition, government-led digital transformation initiatives across Asia-Pacific countries such as India, China, and Singapore are supporting large-scale cloud migration programs to improve public service delivery and data accessibility. Growing industry adoption of edge-cloud integration in 2025 across telecom and manufacturing sectors is enabling faster data processing at the network edge, reducing latency by up to 30–40% in real-time applications across distributed systems.

Global Asia-Pacific Cloud Storage Market Dynamics

Key Market Driver: Rapid Digital Transformation And Exponential Data Growth

Enterprises across Asia-Pacific are experiencing rapid digitalization driven by cloud-first strategies, increasing internet penetration, and widespread adoption of data-intensive applications such as AI, IoT, and big data analytics. Traditional storage infrastructure is becoming insufficient due to limited scalability, higher maintenance costs, and slower data access speeds, accelerating the shift toward cloud-based storage ecosystems.

Organizations in sectors such as banking, retail, healthcare, and manufacturing are increasingly deploying cloud storage platforms, For instance to manage real-time transaction data, electronic health records, and supply chain analytics, enabling improved operational efficiency and data-driven decision-making. In countries such as India and China, national digital programs are significantly increasing cloud adoption among SMEs and public sector organizations, improving digital infrastructure accessibility.

The rapid expansion of streaming platforms, social media usage, and AI-powered applications is also generating massive volumes of structured and unstructured data, requiring highly scalable and resilient storage systems. In addition, hyperscale cloud providers are expanding regional data center investments across Asia-Pacific, with major infrastructure expansions in Singapore, Japan, and India in 2024–2025, improving latency and data sovereignty compliance for enterprise users. Real-world deployments across financial institutions in Southeast Asia have demonstrated cloud migration benefits, including up to 25–35% reduction in IT infrastructure costs and improved disaster recovery capabilities.

Key Market Restraint/Challenge: Data Security Concerns And Regulatory Compliance Complexity

Despite strong adoption growth, concerns around data security, privacy breaches, and regulatory compliance continue to restrain the expansion of cloud storage solutions across Asia-Pacific. Organizations handling sensitive financial, healthcare, and government data face challenges related to cross-border data transfers, encryption standards, and compliance with evolving data protection laws.

Enterprises remain cautious about vendor lock-in risks and potential cyber threats such as ransomware attacks and unauthorized data access, which can lead to operational disruptions and financial losses. In addition, varying data localization regulations across countries such as India, China, and Australia create complexity in designing unified cloud storage strategies for multinational organizations.

Industry reports indicate that cybersecurity incidents targeting cloud environments in Asia-Pacific increased significantly in 2024, with data breach-related costs averaging several million USD per incident for large enterprises, highlighting the financial risks associated with inadequate cloud security frameworks.

Key Market Opportunity: Expansion Of Hybrid Cloud And AI-Driven Storage Optimization

The growing need for flexible, intelligent, and cost-optimized data management solutions is creating strong opportunities for hybrid cloud storage and AI-powered storage optimization technologies across Asia-Pacific. Enterprises are increasingly seeking architectures that combine public cloud scalability with private cloud security to balance performance, compliance, and cost efficiency.

Companies are actively deploying hybrid cloud storage systems, For instance in industries such as telecommunications and healthcare, to enable secure data sharing while maintaining control over sensitive information and ensuring regulatory compliance. In addition, AI-driven storage management tools are being used to automatically optimize data placement, reduce storage costs, and improve retrieval speeds based on usage patterns and workload demands.

The rapid growth of edge computing, 5G networks, and smart city initiatives is further enhancing demand for distributed cloud storage systems capable of processing data closer to the source. Major cloud providers expanded AI-integrated storage offerings in 2025 across Asia-Pacific markets, enabling predictive storage scaling and improving data retrieval efficiency by up to 20–30% in enterprise workloads across high-density computing environments.

Asia-Pacific Cloud Storage Market Scope

The market is segmented on the basis of model, type, functionality, offering, and end-use application.

• By Deployment

On the basis of deployment, the Asia-Pacific cloud storage market is segmented into Public Cloud Deployment, Private Cloud Deployment, and Hybrid Cloud Deployment. The Public Cloud Deployment segment held the largest market revenue share of approximately 58.4% in 2025 driven by strong adoption among SMEs and large enterprises due to lower infrastructure costs, high scalability, and faster deployment capabilities. Major industries such as e-commerce, BFSI, and media rely heavily on public cloud platforms for real-time data access and elastic storage capacity. Public cloud providers across Asia-Pacific are also expanding regional data center footprints to improve latency and ensure data localization compliance across key markets.

The Hybrid Cloud Deployment segment is projected to register the fastest growth at a CAGR of 27.6% from 2026 to 2033, driven by increasing demand for data security, regulatory compliance, and flexible workload management across enterprises operating in multiple jurisdictions. Organizations are increasingly adopting hybrid models to balance cost efficiency with data sovereignty requirements, particularly in regulated industries such as banking and healthcare. The rising integration of edge computing with hybrid cloud architectures is further enhancing real-time data processing capabilities across distributed enterprise environments. Growing enterprise focus on disaster recovery and business continuity planning is also accelerating hybrid cloud adoption across Asia-Pacific.

• By Organization Size

On the basis of organization size, the market is segmented into Large Enterprise and Small Enterprise. The Large Enterprise segment held the dominant market revenue share of approximately 65.7% in 2025 driven by high-volume data storage needs, advanced digital transformation initiatives, and widespread adoption of multi-cloud architectures across global enterprises operating in Asia-Pacific. These organizations generate and process massive datasets from customer transactions, analytics platforms, and enterprise applications. Large enterprises are also leading adopters of AI-driven storage optimization and automated data lifecycle management solutions.

The Small Enterprise segment is projected to register the fastest growth at a CAGR of 26.9% from 2026 to 2033, driven by increasing affordability of cloud solutions, rising SaaS adoption, and government-led digitalization programs supporting SME cloud migration across emerging economies such as India, Vietnam, and Indonesia. Small businesses are rapidly shifting toward subscription-based cloud storage models to reduce upfront infrastructure investment. The expansion of digital payment systems and online business platforms is further accelerating cloud storage penetration among SMEs.

• By End User

On the basis of end user, the market is segmented into Banking, Financial Services and Insurance, Telecommunication, Consumer Goods and Retail, Media and Entertainment, Healthcare and Life Science, Government, and Other. The Banking, Financial Services and Insurance segment held the largest market share of approximately 24.1% in 2025 driven by strong demand for secure data storage, real-time transaction processing, and regulatory compliance requirements across digital banking ecosystems in Asia-Pacific. BFSI institutions are increasingly adopting cloud-native storage for fraud detection, risk analysis, and customer data management. Rising fintech adoption and digital banking expansion are further strengthening cloud storage demand in this segment.

The Telecommunication segment accounted for approximately 18.6% share, supported by rapid 5G deployment and growing data traffic management needs across network infrastructure operators. Telecom companies are increasingly leveraging cloud storage for managing subscriber data, network analytics, and content delivery optimization. Expansion of 5G-enabled services is significantly increasing data storage requirements across Asia-Pacific telecom operators.

• By Component

On the basis of component, the market is segmented into Software and Services. The Software segment held the dominant market revenue share of approximately 70.2% in 2025 driven by strong demand for cloud storage platforms, data management solutions, and AI-enabled storage optimization tools across enterprises in Asia-Pacific. Software solutions are increasingly integrated with analytics, cybersecurity, and automation capabilities to enhance performance and data governance. Continuous innovation in cloud-native applications is further strengthening software dominance in the market.

The Services segment accounted for approximately 29.8% share in 2025 and is projected to register steady growth, driven by increasing demand for cloud migration services, managed storage services, and ongoing maintenance and support requirements across enterprise cloud ecosystems. Organizations are increasingly relying on third-party service providers for seamless migration, integration, and optimization of cloud infrastructure. Rising complexity of multi-cloud environments is further boosting demand for professional and managed services across Asia-Pacific.

Asia-Pacific Cloud Storage Market Regional Analysis

China Cloud Storage Market Insight

China dominated the cloud storage market with the largest revenue share of approximately 32.7% in 2025, driven by rapid digitalization, massive data generation, and strong government-backed cloud infrastructure expansion. The country’s leadership in e-commerce, fintech, and smart city initiatives is significantly increasing demand for scalable cloud storage solutions. Major domestic cloud providers are aggressively expanding data center capacity to support growing enterprise and consumer workloads. In addition, strong investments in AI, 5G networks, and industrial internet platforms are further accelerating cloud storage adoption across both public and private sectors.

Japan Cloud Storage Market Insight

Japan is the fastest-growing region in the cloud storage market, projected to register a CAGR of 26.8% from 2026 to 2033, driven by increasing adoption of hybrid cloud models, rising enterprise digital transformation, and strong demand for secure data management solutions. The country’s advanced manufacturing and automotive sectors are rapidly integrating cloud storage to support IoT connectivity, smart factory operations, and predictive analytics. Growing investments in data sovereignty-compliant cloud infrastructure and partnerships with global hyperscale providers are further supporting market expansion. In addition, rising adoption of AI-driven enterprise applications and disaster-resilient cloud architectures is significantly boosting demand across Japan’s digital ecosystem.

Asia-Pacific Cloud Storage Market Share

The Asia-Pacific Cloud Storage industry is primarily led by well-established companies, including:

• Amazon Web Services, Inc. (U.S.)

• Apple Inc. (U.S.)

• IBM (U.S.)

• Microsoft Corporation (U.S.)

• Oracle (U.S.)

• Salesforce (U.S.)

• VMware, Inc. (U.S.)

• RACKSPACE TECHNOLOGY (U.S.)

• HP Development Company, L.P. (U.S.)

• Google LLC (U.S.)

• FUJITSU (Japan)

• Dell Inc. (U.S.)

• Cisco Systems, Inc. (U.S.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.