Asia Pacific Compostable Packaging Market

Market Size in USD Billion

USD

2.11 Billion

USD

7.99 Billion

2024

2032

USD

2.11 Billion

USD

7.99 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.11 Billion | |

| USD 7.99 Billion | |

| % | |

|

Compostable Packaging Market Size

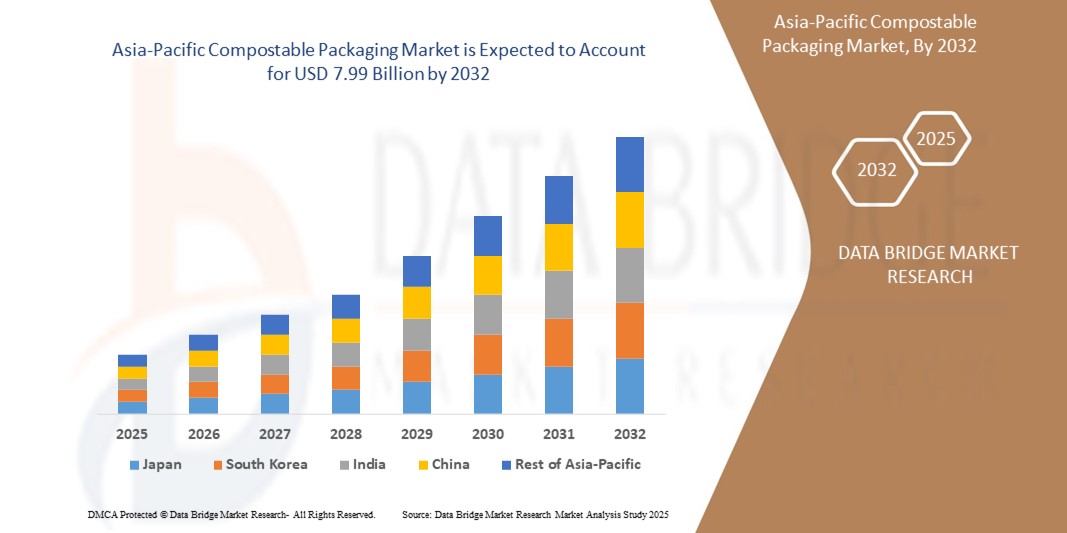

- The Asia-Pacific compostable packaging market size was valued at USD 2.11 billion in 2024 and is expected to reach USD 7.99 billion by 2032, at a CAGR of 18.10% during the forecast period

- The market growth is largely fueled by increasing environmental awareness and stringent government regulations aimed at reducing plastic waste, prompting industries and consumers to shift toward eco-friendly and compostable packaging alternatives

- Furthermore, the rapid expansion of the food delivery and e-commerce sectors, especially in emerging economies, is driving demand for sustainable packaging solutions that are both functional and biodegradable, significantly accelerating market adoption

Compostable Packaging Market Analysis

- Compostable packaging, designed to naturally decompose into non-toxic components, is gaining significant traction across industries due to rising environmental concerns, government regulations on single-use plastics, and the growing demand for sustainable alternatives in both consumer and industrial packaging applications

- The escalating demand for compostable packaging is primarily fueled by increased environmental awareness among consumers, expanding e-commerce and food delivery services, and a rising preference for biodegradable and eco-friendly packaging materials over conventional plastics

- China dominated the compostable packaging market with the largest revenue share in 2024, driven by large-scale manufacturing capabilities, proactive plastic ban policies, and high demand from the food and beverage sector focused on sustainability

- India is expected to be the fastest-growing market for compostable packaging during the forecast period, owing to increasing government initiatives such as the nationwide ban on single-use plastics, growing start-up activity in sustainable packaging, and rising urban consumer demand for eco-friendly products

- The Food & Beverages segment held the largest market share in 2024, due to its extensive consumption of single-use packaging, rising demand for sustainable alternatives in food delivery and takeaway services, and strong regulatory push for eco-friendly materials

Report Scope and Compostable Packaging Market Segmentation

|

Attributes |

Compostable Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Compostable Packaging Market Trends

“Rising Innovation in Biopolymer Materials and Composting Infrastructure”

- A significant and accelerating trend in the Asia-Pacific compostable packaging market is the rapid advancement in biopolymer innovation—particularly materials such as PLA (Polylactic Acid), PHA (Polyhydroxyalkanoates), and starch blends—that offer enhanced durability, compostability, and versatility across packaging applications. These innovations are helping bridge the performance gap between traditional plastics and compostable alternatives, enabling broader adoption in food & beverage, healthcare, and retail sectors

- For instance, NatureWorks LLC has expanded its Ingeo™ PLA biopolymer offerings tailored for high-heat resistance and superior clarity, making them ideal for food packaging applications such as clamshells and cold beverage cups. Similarly, Futamura Group's NatureFlex™ films are seeing increased uptake due to their high barrier properties and compostability certifications suitable for industrial and home composting

- Alongside material innovation, the development of composting infrastructure—including municipal composting programs, decentralized compost bins, and partnerships between governments and packaging firms—is transforming how consumers and businesses handle compostable waste. Countries such as Japan and Australia are leading pilot programs to integrate curbside composting and food-safe compostable materials in public waste systems

- Another emerging trend is the branding and marketing shift towards sustainability, where packaging design not only reflects eco-credentials (such as compostability logos and minimalist printing) but also appeals to environmentally conscious consumers. Brands are increasingly using compostable packaging as a tool for green positioning, particularly in urban markets across India, China, and Southeast Asia

Compostable Packaging Market Dynamics

Driver

“Government Bans and Corporate Commitments to Sustainability”

- The growing number of government-imposed bans and restrictions on single-use plastics across countries such as India, China, and Indonesia is a major driver accelerating the shift toward compostable packaging. These regulations are creating strong market incentives for both local and multinational companies to invest in alternative packaging solutions

- For instance, India’s nationwide ban on single-use plastic items (effective from July 2022) and China’s phased plastic ban policy that mandates biodegradable alternatives in key cities are significantly driving compostable product demand in retail, hospitality, and food services.

- In addition to regulatory pressure, corporate sustainability commitments are influencing packaging innovation. Companies such as Unilever, Nestlé, and PepsiCo have pledged to transition to 100% recyclable, compostable, or reusable packaging by 2025–2030, thereby pushing packaging suppliers to innovate rapidly and scale up compostable solution

- These trends are supported by rising environmental consciousness among consumers and investments in industrial composting infrastructure, making it easier for end-users to adopt and dispose of compostable packaging responsibly

Restraint/Challenge

“Lack of Composting Infrastructure and High Cost of Materials”

- Despite strong momentum, one of the most significant challenges in the Asia-Pacific compostable packaging market is the lack of adequate composting infrastructure, especially in developing nations. Compostable materials require specific conditions for proper degradation, and without access to certified composting facilities, their environmental benefits cannot be fully realized

- For instance, many urban centers in Southeast Asia and South Asia still lack municipal compost collection systems, leading to compostable packaging often ending up in landfills where it decomposes improperly. This not only undermines environmental impact but also discourages consumers and businesses from adopting such materials at scale

- Additionally, the relatively high cost of compostable materials such as PLA or PHA compared to conventional plastics limits widespread adoption—particularly among small and medium-sized enterprises (SMEs) and budget-conscious sectors. While costs are expected to decline with scale and innovation, price sensitivity remains a barrier in price-competitive markets such as India, Vietnam, and the Philippines

- Overcoming these challenges will require a combination of public-private investments in composting systems, government subsidies or incentives, and increased consumer awareness on proper disposal practices. Furthermore, the development of locally sourced, cost-effective compostable materials will be key to improving affordability and scaling adoption across diverse market segments

Compostable Packaging Market Scope

The market is segmented on the basis of product type, material, packaging layer, distribution channel, and end-user.

• By Product Type

On the basis of product type, the Asia-Pacific compostable packaging market is segmented into bags, trays, cups, plates, films, lids, straws, cutlery, bowls, clamshells, pouches & sachets, and others. The bags segment held the largest market revenue share in 2024, primarily due to their widespread application in grocery, retail, and food delivery sectors. The surge in bans on conventional plastic carry bags across countries such as India, Thailand, and Australia has led to significant demand for compostable alternatives. Compostable bags are valued for their biodegradability, regulatory compliance, and consumer appeal, especially in eco-conscious urban markets.

The clamshells segment is expected to witness the fastest CAGR from 2025 to 2032. Their popularity is rising rapidly in ready-to-eat food packaging and takeaway services due to convenience, sturdiness, and compostability. Innovations in heat-resistant PLA-based and paper-based clamshell packaging are further contributing to this segment’s momentum.

• By Material

Based on material, the market is segmented into plastic, paper & paperboard, and others. The plastic segment dominated the market in 2024, largely driven by the extensive use of bioplastics such as PLA and starch-based polymers, which mimic the flexibility and strength of conventional plastics while offering compostable properties. PLA’s cost-effectiveness and ease of processing make it a preferred choice for mass production, especially in single-use food service applications.

The paper & paperboard segment is anticipated to grow at the highest CAGR during the forecast period. The natural biodegradability, recyclability, and aesthetic appeal of paper packaging have driven its increased usage, especially for eco-friendly branding in the personal care and F&B sectors.

• By Packaging Layer

On the basis of packaging layer, the market is segmented into primary packaging, secondary packaging, and tertiary packaging. The primary packaging segment accounted for the largest market revenue share in 2024, owing to its direct contact with products in the food, medical, and retail sectors. This includes compostable trays, cups, and pouches that maintain freshness and ensure food safety while complying with plastic reduction mandates.

The secondary packaging segment is expected to register the fastest growth during the forecast period, as brands increasingly shift to sustainable outer packaging for shipping, presentation, and branding purposes. Compostable corrugated board and molded pulp solutions are gaining traction in electronics and consumer goods.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into B2B, supermarkets/hypermarkets, departmental stores, convenience stores, specialty stores, e-commerce, and others. The B2B segment held the largest share in 2024, as food chains, hospitality firms, and packaging wholesalers procure compostable packaging in bulk for operational use and resale. Partnerships between packaging manufacturers and restaurant chains, especially in urban markets of Japan and Singapore, are driving this segment.

The e-commerce segment is anticipated to witness the highest CAGR from 2025 to 2032. The growing trend of eco-friendly online shopping platforms and availability of customizable compostable packaging options through digital channels are enhancing accessibility and awareness among SMEs and startups.

• By End-User

By end-user, the market is segmented into food & beverages, medical, automotive, electrical & electronics, agriculture, textile goods, personal & home care, chemical, and others. The food & beverages segment held the dominant share in 2024, supported by the demand for eco-friendly alternatives for disposable tableware, containers, and takeaway packaging. Regulatory pressure on food service outlets and rising consumer preference for sustainable dining have fueled growth across countries such as Australia, South Korea, and India.

The personal & home care segment is expected to grow at the fastest rate during the forecast period, as cosmetic and wellness brands embrace sustainable packaging to align with their green marketing strategies. Compostable sachets and jars made from bio-based materials are gaining popularity among environmentally conscious consumers.

Asia-Pacific Compostable Packaging Market Regional Analysis

- China dominated the compostable packaging market with the largest revenue share in 2024, driven by large-scale manufacturing capabilities, proactive plastic ban policies, and high demand from the food and beverage sector focused on sustainability

- Manufacturers are increasingly partnering with food and beverage chains to supply customized compostable solutions that meet both environmental and branding goals. Technological advancements in biopolymer processing and packaging automation further boost scalability.

- Market growth is also fueled by increasing investments in green packaging startups and supportive policies under initiatives such as “Made in China 2025” focusing on environmental innovation.

China Compostable Packaging Market Insight

China held the largest share of the Asia-Pacific compostable packaging market in 2024, supported by aggressive anti-plastic legislation, rapid urbanization, and the surge in online food delivery services. Companies are leveraging domestic bioplastic production capacities, particularly PLA and bagasse, to meet demand. Strategic government mandates, such as the National Development and Reform Commission’s 2020 ban on non-degradable plastic bags in major cities, have accelerated adoption across sectors.

India Compostable Packaging Market Insight

India is expected to witness the fastest growth rate in the region during the forecast period, owing to a combination of policy mandates, rising environmental awareness, and increased startup activity in sustainable packaging. States such as Maharashtra, Tamil Nadu, and Kerala have implemented strict plastic bans, encouraging the use of paper-based and biodegradable packaging in retail, food services, and FMCG. Domestic innovations in agro-waste-based packaging and collaborations with local municipalities for composting infrastructure are expected to further propel market penetration.

Japan Compostable Packaging Market Insight

Japan is a key market for premium compostable packaging solutions, particularly in the personal care, electronics, and food sectors. High consumer consciousness about environmental impact, coupled with the government’s Plastic Resource Circulation Strategy, is pushing brands to adopt fiber-based and compostable plastic alternatives. Innovations in molded pulp packaging and the use of biodegradable films in electronics and gift packaging are shaping Japan’s eco-friendly packaging landscape.

Australia Compostable Packaging Market Insight

Australia is steadily emerging as a strong adopter of compostable packaging due to national targets such as the 2025 National Packaging Targets, which aim for 100% of packaging to be reusable, recyclable, or compostable. Major supermarket chains and QSRs are leading initiatives by replacing single-use plastics with compostable alternatives. The country’s robust composting infrastructure and consumer preference for environmentally responsible brands support ongoing growth, especially in fresh food and retail packaging.

Compostable Packaging Market Share

The compostable packaging industry is primarily led by well-established companies, including:

- International Paper (U.S.)

- Mondi (UK)

- BASF SE (Germany)

- Be Green Packaging HQ (U.S.)

- Futamura Group (Japan)

- WestRock Company (U.S.)

- BIOPAK (Australia)

- Amcor plc (Switzerland)

- Wuxi Topteam Co. Ltd (China)

- NatureWorks LLC (U.S.)

- Ecolifellc.com (U.S.)

- Lithey Inc. (India)

- Biotec Pvt. Ltd (India)

- Avani Eco (Indonesia)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Asia Pacific Compostable Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Asia Pacific Compostable Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Asia Pacific Compostable Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.