Asia Pacific Electric Vehicle Market

Market Size in USD Million

CAGR :

%

USD

242.26 Million

USD

1,371.66 Million

2025

2033

USD

242.26 Million

USD

1,371.66 Million

2025

2033

| 2026 –2033 | |

| USD 242.26 Million | |

| USD 1,371.66 Million | |

| % | |

|

Asia-Pacific Electric Vehicle Market Size

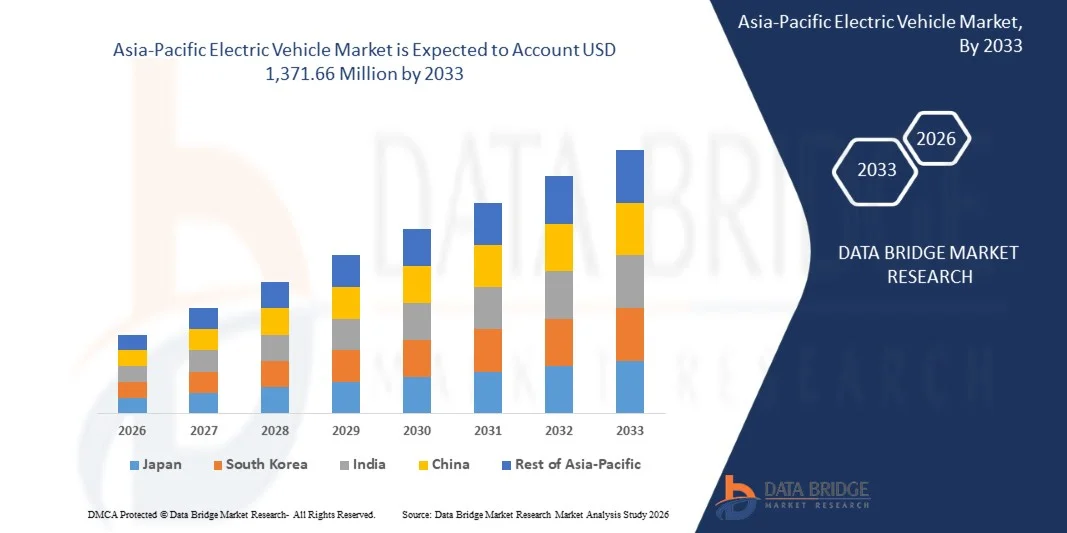

- The Asia-Pacific electric vehicle market size was valued at USD 242.26 million in 2025 and is expected to reach USD 1,371.66 million by 2033, at a CAGR of 24.20% during the forecast period

- The market growth is largely fuelled by the increasing government initiatives and subsidies promoting electric mobility, along with stringent emission regulations aimed at reducing carbon footprint across major economies

- Rising consumer awareness regarding environmental sustainability, coupled with advancements in battery technology and expanding charging infrastructure, is further accelerating the adoption of electric vehicles across the region

Asia-Pacific Electric Vehicle Market Analysis

- The market is witnessing rapid growth due to strong policy support, increasing investments by automakers, and the growing shift toward sustainable transportation solutions, which are driving large-scale adoption of electric vehicles across urban and semi-urban areas

- Increasing fuel prices, rapid urbanization, and rising demand for energy-efficient mobility solutions are further supporting market expansion, while continuous innovation in EV components and ecosystem development is enhancing overall market competitiveness

- China electric vehicle market captured the largest revenue share in 2025 within Asia-Pacific, fueled by strong government incentives, extensive charging infrastructure, and the presence of leading EV manufacturers. Consumers are increasingly adopting electric vehicles due to supportive policies such as subsidies, tax exemptions, and license plate benefits in major cities

- Japan is expected to witness the highest compound annual growth rate (CAGR) in the Asia-Pacific electric vehicle market due to increasing investments in advanced mobility technologies, strong focus on carbon neutrality, rapid development of next-generation battery systems, and expanding adoption of hybrid and electric vehicles across the automotive sector

- The Battery Cells & Packs segment held the largest market revenue share in 2025 driven by the increasing demand for high-performance batteries that determine vehicle range, efficiency, and overall cost structure. Continuous advancements in lithium-ion and next-generation battery technologies, along with large-scale investments in battery manufacturing facilities, are further strengthening the dominance of this segment across the region

Report Scope and Asia-Pacific Electric Vehicle Market Segmentation

|

Attributes |

Asia-Pacific Electric Vehicle Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

• BYD Company Ltd. (China) |

|

Market Opportunities |

• Expansion Of Public Charging Infrastructure |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Asia-Pacific Electric Vehicle Market Trends

“Rising Adoption of Sustainable and Low-Emission Mobility Solutions”

• The increasing focus on reducing carbon emissions and promoting environmentally friendly transportation is significantly shaping the Asia-Pacific electric vehicle market, as consumers and governments are actively shifting toward clean mobility alternatives. Electric vehicles are gaining strong traction due to their ability to reduce greenhouse gas emissions, lower dependency on fossil fuels, and support sustainability goals. This trend is strengthening adoption across passenger and commercial vehicle segments, encouraging automakers to expand their EV portfolios and invest in advanced technologies

• Increasing awareness regarding environmental protection, coupled with rising fuel prices and urban pollution concerns, has accelerated the demand for electric vehicles across major economies such as China, India, and Japan. Consumers are increasingly preferring energy-efficient mobility solutions, prompting governments to introduce subsidies, tax incentives, and favorable policies. This has also led to collaborations between automotive manufacturers, battery producers, and charging infrastructure providers to enhance the EV ecosystem

• Sustainability and electrification trends are influencing purchasing decisions, with manufacturers focusing on innovation, battery efficiency, and extended driving range. These factors are helping companies differentiate their offerings in a competitive market while building consumer trust and accelerating adoption rates. Companies are also emphasizing eco-friendly production practices and lifecycle sustainability to strengthen their market positioning and appeal to environmentally conscious consumers

• For instance, in 2024, BYD in China and Tata Motors in India expanded their electric vehicle portfolios by introducing new affordable EV models targeting urban consumers. These launches were aligned with rising consumer demand for cost-effective and sustainable transportation solutions, supported by expanding charging infrastructure and government incentives. The vehicles were also marketed as eco-friendly alternatives, enhancing brand loyalty and increasing EV penetration in the region

• While demand for electric vehicles is growing rapidly, sustained market expansion depends on advancements in battery technology, cost reduction, and the development of robust charging infrastructure. Manufacturers are also focusing on improving vehicle range, charging speed, and overall performance to ensure competitiveness with conventional vehicles and support long-term adoption across diverse consumer segments

Asia-Pacific Electric Vehicle Market Dynamics

Driver

“Increasing Government Support and Electrification Initiatives”

• Strong government support through subsidies, tax benefits, and regulatory mandates is a major driver for the Asia-Pacific electric vehicle market. Governments across the region are promoting EV adoption to reduce emissions, enhance energy security, and support sustainable development goals. These initiatives are encouraging manufacturers to scale production and invest in local EV manufacturing facilities

• Expanding applications across passenger vehicles, commercial fleets, and public transportation are significantly influencing market growth. Electric vehicles offer lower operating costs, reduced maintenance, and improved energy efficiency, making them an attractive alternative to internal combustion engine vehicles. The increasing integration of EVs in ride-sharing, logistics, and public transit systems further reinforces this trend

• Automotive manufacturers and technology providers are actively promoting EV adoption through product innovation, partnerships, and infrastructure development. These efforts are supported by the growing demand for clean mobility solutions and are fostering collaborations across the value chain, including battery manufacturing, software integration, and charging networks

• For instance, in 2023, Hyundai in South Korea and SAIC Motor in China increased investments in EV production and battery development to expand their electric vehicle offerings. This expansion was driven by rising demand for electric mobility and supportive government policies, resulting in improved production capacity and enhanced market competitiveness. Both companies also emphasized innovation and sustainability to strengthen their brand presence

• Although strong policy support and electrification trends drive growth, widespread adoption depends on reducing vehicle costs, improving battery efficiency, and expanding charging infrastructure. Continuous investment in research and development, along with public-private partnerships, will be essential to sustain long-term market growth and meet increasing demand

Restraint/Challenge

“High Initial Cost and Infrastructure Limitations”

• The relatively high upfront cost of electric vehicles compared to conventional vehicles remains a significant challenge, limiting adoption among price-sensitive consumers. High battery costs and manufacturing expenses contribute to the elevated pricing of EVs. In addition, limited economies of scale in certain markets can further impact affordability and slow down mass adoption

• Consumer awareness and acceptance vary across the region, particularly in developing countries where EV infrastructure is still evolving. Limited understanding of long-term cost benefits and performance capabilities can hinder adoption. This also results in slower penetration in rural and semi-urban areas where charging infrastructure is less developed

• Infrastructure challenges, including insufficient charging stations and grid limitations, also impact market growth. The need for widespread and reliable charging networks increases operational complexity and requires substantial investment. Companies and governments must focus on building fast-charging networks, improving grid capacity, and ensuring accessibility to support EV adoption

• For instance, in 2024, emerging markets such as Indonesia and Vietnam reported slower EV adoption due to limited charging infrastructure and higher vehicle costs compared to traditional vehicles. Range anxiety and lack of standardized charging solutions were additional barriers. These factors also influenced consumer hesitation and impacted overall EV sales growth in these regions

• Overcoming these challenges will require cost optimization, infrastructure expansion, and increased consumer awareness initiatives. Collaboration between governments, automakers, and energy providers will be critical to developing a robust EV ecosystem. Furthermore, advancements in battery technology, charging solutions, and localized manufacturing will play a key role in improving affordability and accelerating market adoption

Asia-Pacific Electric Vehicle Market Scope

The market is segmented on the basis of component, propulsion type, charging station type, class, power train, and vehicle type.

• By Component

On the basis of component, the Asia-Pacific electric vehicle market is segmented into Battery Cells & Packs, On-Board Charger, Infotainment System, and Others. The Battery Cells & Packs segment held the largest market revenue share in 2025 driven by the increasing demand for high-performance batteries that determine vehicle range, efficiency, and overall cost structure. Continuous advancements in lithium-ion and next-generation battery technologies, along with large-scale investments in battery manufacturing facilities, are further strengthening the dominance of this segment across the region.

The Infotainment System segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising consumer preference for connected vehicles and advanced in-car digital experiences. Modern EVs increasingly integrate smart dashboards, navigation systems, and AI-based interfaces, enhancing user convenience and driving demand for sophisticated infotainment solutions.

• By Propulsion Type

On the basis of propulsion type, the market is segmented into Plug-In Hybrid Electric Vehicles (PHEVs), Battery Electric Vehicles (BEVs), Hybrid Electric Vehicles (HEVs), and Fuel Cell Electric Vehicles (FCEVs). The Battery Electric Vehicles (BEVs) segment accounted for the largest market share in 2025 due to zero-emission benefits, strong government incentives, and expanding charging infrastructure across major countries. BEVs are gaining widespread adoption as they eliminate fuel dependency and align with sustainability goals.

The Fuel Cell Electric Vehicles (FCEVs) segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing investments in hydrogen infrastructure and the potential for longer driving ranges with faster refueling. Growing interest in clean hydrogen energy is encouraging governments and manufacturers to explore FCEV deployment, particularly for commercial and long-distance transportation.

• By Charging Station Type

On the basis of charging station type, the market is segmented into Normal Charging and Super Charging. The Normal Charging segment held the largest market share in 2025 owing to its widespread availability, cost-effectiveness, and suitability for residential and workplace charging applications. Most EV users rely on standard charging solutions for overnight charging, making it a dominant segment.

The Super Charging segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for rapid charging solutions that significantly reduce charging time. Expansion of fast-charging networks along highways and urban centers is enhancing EV convenience and supporting long-distance travel adoption.

• By Class

On the basis of class, the market is segmented into Mid-Priced and Luxury. The Mid-Priced segment dominated the market in 2025 due to its affordability and increasing availability of cost-effective electric vehicle models targeting mass-market consumers. Government subsidies and rising middle-class income levels are further supporting the growth of this segment.

The Luxury segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for premium electric vehicles equipped with advanced features, superior performance, and enhanced comfort. High-income consumers are increasingly adopting luxury EVs as a status symbol combined with sustainability.

• By Power Train

On the basis of power train, the market is segmented into Parallel Hybrid, Series Hybrid, and Combined Hybrid. The Parallel Hybrid segment held the largest market share in 2025 driven by its ability to offer improved fuel efficiency while maintaining performance, making it a preferred choice among consumers transitioning from conventional vehicles.

The Combined Hybrid segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its flexibility in utilizing both series and parallel configurations, enhancing efficiency and performance. Technological advancements are enabling automakers to optimize hybrid systems for better energy utilization and reduced emissions.

• By Vehicle Type

On the basis of vehicle type, the market is segmented into Passenger Cars, Two Wheelers, and Commercial Vehicles. The Passenger Cars segment dominated the market in 2025 driven by increasing consumer adoption, urbanization, and strong government support for personal electric mobility. The availability of diverse EV models across price ranges is further accelerating segment growth.

The Two Wheelers segment is expected to witness the fastest growth rate from 2026 to 2033, driven by high demand in densely populated countries such as India and China, where two-wheelers are a primary mode of transportation. Lower cost, ease of charging, and favorable government policies are significantly boosting the adoption of electric two-wheelers across the region.

Asia-Pacific Electric Vehicle Market Regional Analysis

- China electric vehicle market captured the largest revenue share in 2025 within Asia-Pacific, fueled by strong government incentives, extensive charging infrastructure, and the presence of leading EV manufacturers. Consumers are increasingly adopting electric vehicles due to supportive policies such as subsidies, tax exemptions, and license plate benefits in major cities

- The country’s well-established battery manufacturing ecosystem and large-scale production capabilities further accelerate market growth

- Moreover, continuous innovation in battery technology and increasing investments in autonomous and connected vehicle technologies are significantly contributing to the market's expansion

Japan Electric Vehicle Market Insight

The Japan electric vehicle market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing investments in next-generation mobility solutions and strong government initiatives to achieve carbon neutrality. Consumers are gradually shifting towards hybrid and battery electric vehicles due to rising environmental awareness and fuel efficiency concerns. The presence of advanced automotive manufacturers and ongoing research in solid-state battery technology further strengthens the market outlook. In addition, the expansion of charging infrastructure and integration of smart mobility solutions are playing a crucial role in accelerating electric vehicle adoption across the country.

Asia-Pacific Electric Vehicle Market Share

The Asia-Pacific electric vehicle industry is primarily led by well-established companies, including:

• BYD Company Ltd. (China)

• NIO Inc. (China)

• XPeng Inc. (China)

• Li Auto Inc. (China)

• Geely Automobile Holdings Ltd. (China)

• Great Wall Motor Company Limited (China)

• SAIC Motor Corporation Limited (China)

• Changan Automobile Co., Ltd. (China)

• Tata Motors Limited (India)

• Mahindra & Mahindra Ltd. (India)

• Hyundai Motor Company (South Korea)

• Kia Corporation (South Korea)

• Toyota Motor Corporation (Japan)

• Honda Motor Co., Ltd. (Japan)

• Nissan Motor Co., Ltd. (Japan)

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.