Asia Pacific Electrostatic Chucks Market

Market Size in

21.68

30.10

2024

2032

21.68

30.10

2024

2032

| 2025 - 2032 | |

| USD 21.68 | |

| USD 30.10 | |

| % | |

|

Electrostatic Chucks Market Size

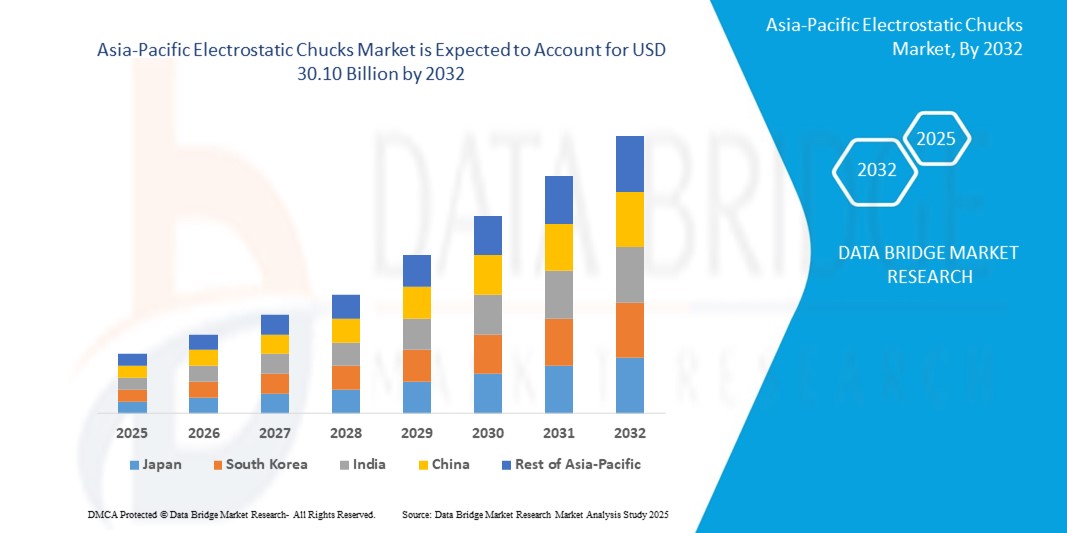

- The Asia Pacific Electrostatic Chucks Market size was valued at USD 21.68 billion in 2024 and is expected to reach USD 30.10billion by 2032, at a CAGR of 4.8% during the forecast period

- This growth is driven by the dominance of semiconductor manufacturing in countries like China, Japan, South Korea, and Taiwan, coupled with increasing demand for consumer electronics and advancements in renewable energy applications.

Electrostatic Chucks Market Analysis

- The Electrostatic Chucks market encompasses devices that use electrostatic forces to securely hold substrates, primarily silicon wafers, during semiconductor manufacturing processes such as photolithography, etching, and deposition, offering high precision and minimal contamination.

- The demand for ESCs is significantly driven by the Asia Pacific region’s leadership in semiconductor production, with the region accounting for 70% of global semiconductor output in 2024, and the growth of consumer electronics, with 1.5 billion smartphones shipped globally in 2024, largely manufactured in Asia Pacific.

- China is expected to dominate the Asia Pacific Electrostatic Chucks market due to its extensive semiconductor fabrication facilities and government initiatives like “Made in China 2025,” holding a 35.0% market share in 2025.

- South Korea is expected to be the fastest-growing country during the forecast period due to investments by major players like Samsung and SK Hynix in advanced semiconductor technologies.

- The Semiconductor LCD/CVD segment is expected to dominate the market with a market share of 60.0% in 2025 due to the critical role of ESCs in precise wafer processing for semiconductor production.

Report Scope and Electrostatic Chucks Market Segmentation

|

Attributes |

Electrostatic Chucks Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Electrostatic Chucks Market Trends

“Adoption of Advanced ESCs in EUV Lithography and 5G Applications”

- A prominent trend in the Asia Pacific Electrostatic Chucks market is the increasing adoption of advanced ESCs designed for extreme ultraviolet (EUV) lithography and 5G applications, which require high precision and thermal uniformity, with the EUV segment projected to grow at a CAGR of 6.0% during the forecast period.

- The Coulomb Type segment is estimated to hold the highest market share of 65.0% in 2025, owing to its superior electrostatic force and compatibility with advanced semiconductor processes like 3D NAND and 5G chip production.

- For instance, in 2024, a South Korean semiconductor manufacturer adopted Coulomb Type ESCs for EUV lithography, improving wafer handling efficiency by 12%.

- This trend is driving demand for innovative ESCs that support the region’s leadership in cutting-edge semiconductor technologies.

Electrostatic Chucks Market Dynamics

Driver

“Dominance of Semiconductor Manufacturing and Consumer Electronics”

- The Asia Pacific region’s dominance in semiconductor manufacturing, with countries like China, Japan, South Korea, and Taiwan producing 70% of global semiconductors, and the surge in consumer electronics production, with 1.5 billion smartphones shipped globally in 2024, are significantly contributing to the Electrostatic Chucks market growth.

- ESCs provide precise wafer handling, reducing contamination by 20% compared to mechanical chucks, critical for advanced processes like 300mm wafer production and EUV lithography.

- For instance, in 2024, TSMC in Taiwan integrated advanced ESCs in its 3nm chip production, enhancing yield by 15%.

- As the region continues to invest in semiconductor foundries and electronics, the demand for ESCs grows, ensuring high-precision manufacturing.

Opportunity

“Growing Demand for ESCs in Solar Panel Manufacturing”

- The increasing focus on renewable energy, with Asia Pacific aiming to produce 50% of global solar energy by 2030, offers significant opportunities for market growth by driving demand for ESCs in solar panel manufacturing.

- ESCs support precise handling in thin-film solar cell production, improving efficiency by 10% in photovoltaic manufacturing by 2025.

- For instance, in 2023, a Chinese solar panel manufacturer adopted ESCs for thin-film cell production, reducing defects by 15%.

- This opportunity drives market expansion by enabling scalable and efficient solutions for renewable energy applications.

Restraint/Challenge

“High Manufacturing and Maintenance Costs”

- High manufacturing costs, with 40% of manufacturers citing advanced materials like ceramics as a cost barrier in 2024, and maintenance expenses for ensuring ESC longevity in high-vacuum environments pose significant barriers to the market.

- These challenges require substantial investments in R&D and maintenance protocols, increasing costs for organizations.

For instance, in 2024, 30% of small Asian fabs reported high ESC maintenance costs as a barrier to adoption.

- These issues can hinder market growth, necessitating cost-effective and durable ESC solutions.

Electrostatic Chucks Market Scope

The market is segmented on the basis material, product, electrode, poles and application.

|

Segmentation |

Sub-Segmentation |

|

By Material |

|

|

By Product |

|

|

By Electrode |

|

|

By Poles

|

|

|

By Application |

|

In 2025, the Semiconductor LCD/CVD segment is projected to dominate the market with the largest share in the application segment

The Semiconductor LCD/CVD segment is expected to dominate the Electrostatic Chucks market in Europe with the largest share of 56.22% in 2025, driven by the increasing adoption of semiconductor fabrication and flat-panel display manufacturing technologies across the region. Electrostatic chucks are essential for accurately securing wafers during plasma etching, CVD, and lithography processes, ensuring precision and efficiency. The rise in demand for advanced nodes, EUV lithography, and OLED/LCD displays is fostering equipment upgrades and boosting the need for high-performance ESCs across major foundries and IDMs in Europe.

The Ceramics segment is expected to account for the largest share during the forecast period in the material segment

In 2025, the Ceramics segment is expected to dominate the European Electrostatic Chucks market with the largest market share of 51.31%, attributed to ceramics’ excellent thermal conductivity, electrical insulation, and mechanical strength—key properties for handling extreme environments in semiconductor processing. Ceramic ESCs are increasingly used in advanced etching and deposition tools due to their durability and compatibility with high-temperature plasma environments.

Electrostatic Chucks Market Country Analysis

“U.K. Holds the Largest Share in the Electrostatic Chucks Market”

- Japan dominates the Asia Pacific Electrostatic Chucks market, driven by its well-established semiconductor manufacturing industry, leadership in wafer processing equipment, and strong local supply chain integration.

- Major Japanese equipment manufacturers such as Tokyo Electron, ULVAC, and Shinko Electric are global leaders in producing electrostatic chucks for plasma etching, CVD, and lithography applications.

- The government’s aggressive support under initiatives like the Semiconductor and Digital Industry Strategy has attracted heavy investments in domestic chip production and tool development, further strengthening ESC demand.

- In 2024, Tokyo Electron announced expansions in its Yamanashi facility to meet the rising global demand for advanced wafer processing tools—key users of ESC technology—solidifying Japan’s leading role in the regional market..

“Germany is Projected to Register the Highest CAGR in the Electrostatic Chucks Market”

- China is expected to witness the highest growth rate in the Asia Pacific Electrostatic Chucks market, driven by its fast-expanding semiconductor fabrication capacity and government-backed initiatives such as “Made in China 2025” and the National IC Investment Fund.

- Leading Chinese chipmakers like SMIC, Hua Hong, and newer entrants are ramping up investments in 300mm fabs, which extensively rely on electrostatic chucks for front-end processing steps.

- In 2024, NAURA Technology Group and AMEC—China's leading semiconductor equipment firms—began exporting dry etching and deposition tools featuring domestically produced ESCs, boosting local supply chain self-sufficiency.

- The ongoing U.S.-China technology decoupling has accelerated domestic innovation and adoption of homegrown wafer handling systems, positioning China as a high-growth market for electrostatic chuck solutions..

Electrostatic Chucks Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- SHINKO ELECTRIC INDUSTRIES CO., LTD. (Japan)

- Applied Materials (U.S.)

- Kyocera Corporation (Japan)

- TOTO Ltd. (Japan)

- NTK CERATEC CO., LTD. (Japan)

- Sumitomo Osaka Cement Co., Ltd. (Japan)

- Creative Technology Corporation (Japan)

- Tsukuba Seiko Co., Ltd. (Japan)

- CoorsTek Inc. (U.S.)

- Entegris, Inc. (U.S.)

Latest Developments in Asia Pacific Electrostatic Chucks Market

- In March 2025, SHINKO Electric Industries Co., Ltd., a major player in electrostatic chuck technology, announced the opening of a new R&D center in Dresden, Germany, aimed at advancing wafer handling systems and electrostatic chuck designs for EUV lithography. This move supports Europe's growing semiconductor equipment ecosystem under the EU Chips Act initiative.

- In January 2025, Lam Research, a leading global semiconductor equipment supplier, expanded its presence in Villach, Austria, with investments focused on enhancing plasma etching and deposition tools. These tools integrate advanced ESC systems, which are critical for processing next-gen semiconductor wafers used in AI, automotive, and HPC applications.

- In November 2024, SEMITEC Corporation partnered with a European-based semiconductor OEM to supply ceramic-based bipolar electrostatic chucks for high-temperature plasma processing. The deal strengthens SEMITEC’s position in Europe and aligns with demand for robust ESCs compatible with SiC and GaN wafer processing.

- In October 2024, Applied Materials announced a collaboration with imec (Belgium) to co-develop next-generation electrostatic clamping technologies to support sub-3nm node semiconductor manufacturing. The partnership targets improvements in wafer flatness control and thermal uniformity, both critical to maintaining EUV lithography precision.

- In August 2024, Germany-based TRUMPF Hüttinger introduced an advanced RF power supply system optimized for electrostatic chucks used in plasma etchers and CVD equipment. The new system enhances power control and temperature stability during wafer processing, addressing challenges in high-aspect-ratio etching.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Asia Pacific Electrostatic Chucks Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Asia Pacific Electrostatic Chucks Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Asia Pacific Electrostatic Chucks Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.