Asia Pacific Electrosurgery Equipment Market

Market Size in USD Billion

USD

1.20 Billion

USD

2.40 Billion

2025

2033

USD

1.20 Billion

USD

2.40 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.20 Billion | |

| USD 2.40 Billion | |

| % | |

|

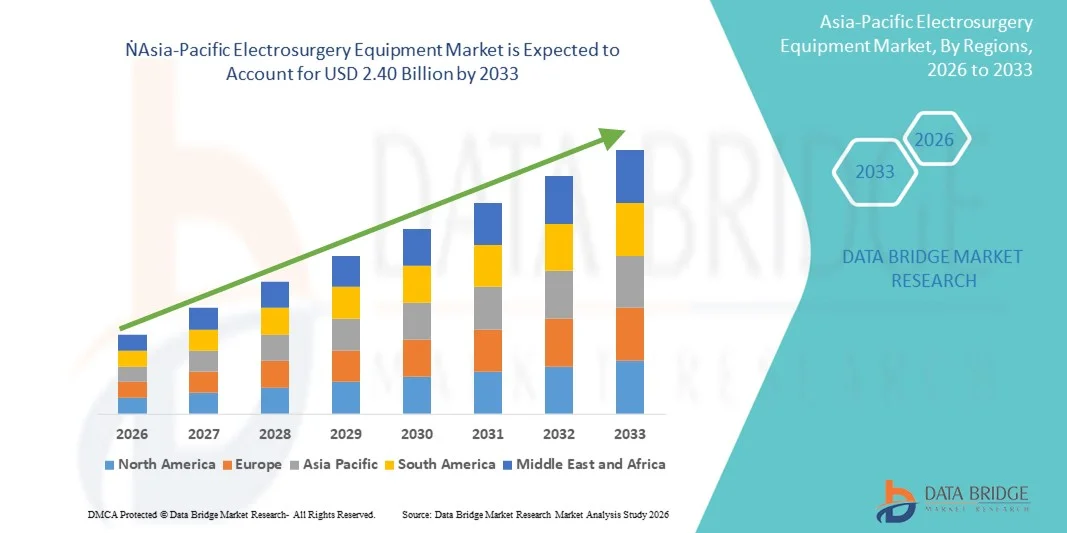

Asia-Pacific Electrosurgery Equipment Market Size

- The Asia-Pacific electrosurgery equipment market size was valued at USD 1.20 billion in 2025 and is expected to reach USD 2.40 billion by 2033, at a CAGR of 9.1% during the forecast period

- The market growth is largely fueled by the increasing adoption of minimally invasive surgical procedures, advancements in electrosurgical technologies, and the rising demand for improved surgical efficiency and precision in both hospital and outpatient settings

- Furthermore, growing awareness among healthcare professionals about the benefits of electrosurgery equipment, combined with increasing surgical volumes and the need for faster patient recovery, is accelerating the uptake of Electrosurgery Equipment solutions, thereby significantly boosting the industry's growth

Asia-Pacific Electrosurgery Equipment Market Analysis

- Electrosurgery equipment, offering advanced devices for cutting, coagulation, and tissue ablation, is increasingly vital in modern surgical procedures across hospitals and outpatient surgical centers due to enhanced precision, safety, and procedural efficiency

- The escalating demand for electrosurgery equipment is primarily fueled by the rising adoption of minimally invasive and laparoscopic surgeries, growing surgical volumes, and the need for faster patient recovery and improved outcomes

- China dominated the electrosurgery equipment market with the largest revenue share of 42.5% in 2025, characterized by rapid healthcare infrastructure expansion, strong government investments, and increasing adoption of advanced surgical technologies in both public and private hospitals. The country continues to experience substantial growth in surgical device installations, driven by rising procedural volumes and innovations from leading domestic and international manufacturers

- India is expected to be the fastest-growing region in the electrosurgery equipment market during the forecast period, projected to record a robust CAGR of 12.8% from 2026 to 2033, fueled by rising healthcare expenditure, expanding hospital networks, increasing awareness about minimally invasive surgeries, and government initiatives promoting advanced surgical care

- The Electrosurgical Instruments segment dominated the largest market revenue share of 45.6% in 2025, driven by their essential role in diverse surgical procedures across hospitals and specialty clinics. High adoption is due to precision, minimal blood loss, and reduced operative time

Report Scope and Electrosurgery Equipment Market Segmentation

|

Attributes |

Electrosurgery Equipment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Asia-Pacific Electrosurgery Equipment Market Trends

Growing Adoption of Minimally Invasive Surgical Procedures

- A significant and accelerating trend in the global Electrosurgery Equipment market is the increasing adoption of minimally invasive surgeries (MIS) across hospitals and surgical centers

- These procedures are driving demand for advanced electrosurgical devices that enable precise cutting, coagulation, and hemostasis, while reducing patient recovery time

- For instance, in March 2024, Medtronic launched its Valleylab FT10 electrosurgery system with enhanced feedback control, enabling surgeons to perform complex procedures with greater precision and reduced tissue damage

- This development highlights the growing emphasis on safety and procedural efficiency in the Electrosurgery Equipment market

- Integration with imaging systems and energy-based surgical tools is also becoming prevalent, allowing surgeons to combine electrosurgical devices with other advanced surgical modalities for improved outcomes

- The trend toward procedure-specific, ergonomic, and multifunctional devices is reshaping user expectations in the surgical domain

- Hospitals are increasingly prioritizing equipment that offers operational efficiency, reduced procedure time, and improved patient outcomes, further propelling market adoption

Asia-Pacific Electrosurgery Equipment Market Dynamics

Driver

Rising Surgical Procedures and Healthcare Infrastructure Development

- The increasing number of surgeries, especially in emerging economies, coupled with the expansion of healthcare infrastructure, is a key driver for the Electrosurgery Equipment market

- Rising prevalence of chronic diseases, oncology cases, and elective procedures contributes to the heightened demand for electrosurgical tools

- For instance, in August 2023, Johnson & Johnson announced the launch of the ValleyLab LS10 Energy Platform in India, targeting multi-specialty hospitals to enhance surgical precision and reduce complications. Such initiatives by major companies are expected to drive market growth significantly

- Enhanced training programs for surgeons and the growing adoption of advanced surgical techniques are also facilitating higher utilization of electrosurgical devices

- The focus on reducing operative times, minimizing complications, and supporting same-day discharge surgeries is boosting demand

- Overall, the combination of increasing surgical volumes, expanding hospital networks, and emphasis on procedural efficiency is accelerating the uptake of advanced Electrosurgery Equipment

Restraint/Challenge

High Costs and Regulatory Constraints

- The relatively high cost of advanced electrosurgical systems can be a barrier to adoption, particularly for smaller clinics or budget-constrained healthcare facilities in developing regions

- Many hospitals may delay replacing older devices due to budget limitations

- For instance, reports indicate that premium devices with multifunctional capabilities can cost 3–4 times more than standard units, discouraging smaller hospitals from upgrading their equipment

- Strict regulatory requirements and lengthy approval processes for medical devices pose additional challenges. Compliance with local health authorities and international standards such as FDA, CE marking, or ISO certifications increases time-to-market and operational costs for manufacturers

- Overcoming these challenges requires strategies such as offering cost-effective device variants, leasing programs, and regional regulatory expertise to support timely approvals

- Market growth depends on balancing affordability, compliance, and technological advancement to ensure widespread adoption of electrosurgical solutions

Asia-Pacific Electrosurgery Equipment Market Scope

The market is segmented on the basis of products, surgery, end-user, and distribution channel.

- By Products

On the basis of products, the Asia-Pacific Electrosurgery Equipment market is segmented into Electrosurgical Instruments, Electrosurgical Generators, Plasma and Smoke Management Systems, and Electrosurgical Accessories. The Electrosurgical Instruments segment dominated the largest market revenue share of 45.6% in 2025, driven by their essential role in diverse surgical procedures across hospitals and specialty clinics. High adoption is due to precision, minimal blood loss, and reduced operative time. Training programs and physician familiarity further enhance uptake. Continuous innovation in minimally invasive instruments supports sustained demand. Hospitals invest in high-quality instruments to improve patient outcomes. Integration with advanced generators increases efficiency. Emerging markets in APAC are expanding procurement. Cost-effective options for mid-tier hospitals also support adoption. Regulatory approvals improve trust. Rising surgical procedure volumes contribute to market leadership. Increasing healthcare expenditure strengthens segment dominance. Technological improvements, including ergonomic designs, enhance user preference.

The Plasma and Smoke Management Systems segment is expected to witness the fastest CAGR of 12.4% from 2026 to 2033, fueled by rising awareness of surgical smoke hazards and OR safety. Hospitals and surgical centers invest in smoke evacuation and plasma-based solutions. Compact, portable, and energy-efficient systems accelerate adoption. Government mandates and occupational health regulations drive demand. Integration with advanced electrosurgical generators improves workflow. Training programs for surgeons and OR staff enhance utilization. Growing numbers of minimally invasive surgeries increase demand. Technological innovations in filtration and plasma delivery systems support expansion. Urban hospitals in emerging APAC economies are early adopters. Rising adoption in elective surgeries promotes market growth. Telemedicine-assisted OR management further boosts usage.

- By Surgery

On the basis of surgery, the market is segmented into Gynaecological, Urology, Cardiovascular, General, Neurosurgery, Orthopaedic, Cosmetic, and Others. The General Surgery segment dominated the largest market revenue share of 41.8% in 2025, driven by the high volume of procedures such as laparoscopic, gastrointestinal, and emergency surgeries. Surgeons rely heavily on electrosurgical instruments for precision cutting and coagulation. Hospitals prioritize general surgery setups, resulting in widespread adoption. Government healthcare initiatives promoting surgical infrastructure expansion reinforce demand. Training and standardization of surgical protocols increase utilization. Integration with modern energy-based devices improves outcomes. Increasing hospital bed capacity drives demand. Surgeons’ preference for minimally invasive tools strengthens dominance. Rising procedure volume in China, India, and Japan supports leadership. Continuous product innovation enhances efficiency. Hospitals invest in comprehensive surgical suites. Electrosurgical solutions reduce operative time and patient recovery periods.

The Cosmetic Surgery segment is expected to witness the fastest CAGR of 13.2% from 2026 to 2033, driven by rising aesthetic awareness, increasing medical tourism, and higher disposable income. Surgeons prefer precise and minimally invasive equipment. Clinics and hospitals invest in advanced instruments tailored for cosmetic procedures. Technological innovations supporting rapid recovery and reduced scarring accelerate adoption. Social media influence and urbanization contribute to demand. Cosmetic centers expand procedure offerings with electrosurgical solutions. High demand for dermatological, facial, and body contouring procedures increases market potential. Training programs for cosmetic surgeons improve instrument utilization. Equipment manufacturers offer compact, versatile devices for outpatient use. Growth in private healthcare and specialty clinics promotes adoption. Rising investment in elective surgeries supports expansion. Emerging markets like Thailand and India contribute significantly to growth.

- By End-User

On the basis of end-user, the market is segmented into Hospitals, Specialty Clinics, Ambulatory Surgical Centres, and Others. The Hospitals segment dominated the largest market revenue share of 50.3% in 2025, due to centralized procurement, higher surgical volumes, and availability of trained surgical teams. Hospitals invest in electrosurgical generators and instruments to improve efficiency. Comprehensive surgical suites and multidisciplinary teams support adoption. Integration with hospital IT systems and OR management platforms increases utilization. Government funding for modern infrastructure boosts demand. Hospitals lead in implementing plasma and smoke management solutions. Preference for high-quality, reliable equipment ensures dominance. Expansion of tertiary care facilities in China, Japan, and India strengthens segment leadership. Training programs and clinical collaborations improve utilization. Regulatory compliance reinforces adoption. Hospitals prioritize bulk procurement and maintenance services.

The Ambulatory Surgical Centres segment is expected to witness the fastest CAGR of 12.8% from 2026 to 2033, fueled by the rise in outpatient procedures and cost-efficient care models. ASCs increasingly adopt compact electrosurgical devices. Growth in elective and minimally invasive surgeries in urban areas accelerates adoption. Government initiatives for outpatient care expansion promote growth. ASCs prefer versatile instruments that support multiple surgery types. Rising medical tourism in APAC encourages adoption. Technological advancements in lightweight and portable devices benefit ASCs. Smaller facilities adopt online procurement channels for efficiency. Increased training and awareness of staff enhance utilization. Collaboration with diagnostic and imaging centers improves workflow. Regulatory approvals for smaller devices further support market expansion.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Direct and Retail. The Direct segment dominated the largest market revenue share of 62.1% in 2025, as manufacturers prefer direct sales to hospitals and high-volume surgical centers for training, service, and warranty support. Direct distribution ensures control over product quality and after-sales service. Strong relationships with procurement teams enhance adoption. Regulatory compliance and installation support strengthen trust. Training programs for surgeons improve product utilization. Bulk purchasing agreements favor direct channels. Post-sale technical support reinforces loyalty. Bundled packages of instruments and generators improve efficiency. Hospitals prefer long-term contracts with manufacturers. Equipment upgrades and software updates support continuous adoption. Customization options enhance segment dominance.

The Retail segment is expected to witness the fastest CAGR of 11.9% from 2026 to 2033, supported by growing e-commerce adoption and smaller specialty clinics purchasing online. Simplified ordering, quick delivery, and competitive pricing drive retail growth. Emerging clinics in tier-2 and tier-3 cities increasingly rely on online channels. Availability of electrosurgical accessories through retail platforms accelerates adoption. Manufacturers are offering bundled kits and promotional packages to attract small buyers. Easy access to customer support and product tutorials enhances confidence in retail purchases. Growing awareness of electrosurgical innovations among smaller healthcare facilities further fuels adoption, making retail a key growth channel.

Asia-Pacific Electrosurgery Equipment Market Regional Analysis

- The Asia-Pacific electrosurgery equipment market is projected to witness significant growth during the forecast period of 2026 to 2033

- Driven by the region's expanding healthcare infrastructure, increasing surgical procedure volumes, and rapid adoption of advanced surgical technologies

- The rising prevalence of chronic diseases and demand for minimally invasive surgeries are creating strong demand for electrosurgery devices across hospitals, specialty clinics, and ambulatory surgical centers

China Electrosurgery Equipment Market Insight

China electrosurgery equipment market dominated the electrosurgery equipment market with the largest revenue share of 42.5% in 2025, characterized by rapid healthcare infrastructure expansion, strong government investments, and increasing adoption of advanced surgical technologies in both public and private hospitals. The country continues to experience substantial growth in surgical device installations, fueled by rising procedural volumes and innovations from leading domestic and international manufacturers.

India Electrosurgery Equipment Market Insight

India electrosurgery equipment market is expected to be the fastest-growing region in the electrosurgery equipment market during the forecast period, projected to record a robust CAGR of 12.8% from 2026 to 2033, fueled by rising healthcare expenditure, expanding hospital networks, increasing awareness about minimally invasive surgeries, and government initiatives promoting advanced surgical care.

Asia-Pacific Electrosurgery Equipment Market Share

The Electrosurgery Equipment industry is primarily led by well-established companies, including:

• Medtronic (Ireland)

• Johnson & Johnson (U.S.)

• ConMed Corporation (U.S.)

• Olympus Corporation (Japan)

• ERBE Elektromedizin (Germany)

• Aesculap AG (Germany)

• Smith & Nephew (U.K.)

• Richard Wolf GmbH (Germany)

• Stryker Corporation (U.S.)

• Arthrex, Inc. (U.S.)

• B. Braun Melsungen AG (Germany)

• Medline Industries, Inc. (U.S.)

• Storz Medical AG (Switzerland)

Latest Developments in Asia-Pacific Electrosurgery Equipment Market

- In June 2023, Olympus Corporation (Japan) introduced the ESG‑410 Electrosurgical Generator, a next‑generation generator designed for urology and related procedures. The device reportedly features enhanced ignition capacitors for more stable plasma generation during resection loops, an upgraded touchscreen interface for improved user control, and optional wireless foot-pedal operation — representing a notable product launch during this period

- In March 2024, Medtronic launched its new Valleylab FT10 energy platform, an advanced electrosurgical generator with so-called “smart tissue‑sensing” capability — which adjusts energy delivery in real time based on tissue response, aiming to optimize cutting/coagulation balance and reduce thermal damage. This was widely reported as a key device upgrade in the global electrosurgical equipment market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.