Asia Pacific Food Container And Kitchen Appliances Market

Market Size in USD Billion

USD

21.57 Billion

USD

35.96 Billion

2025

2033

USD

21.57 Billion

USD

35.96 Billion

2025

2033

| 2026 - 2033 | |

| USD 21.57 Billion | |

| USD 35.96 Billion | |

| % | |

|

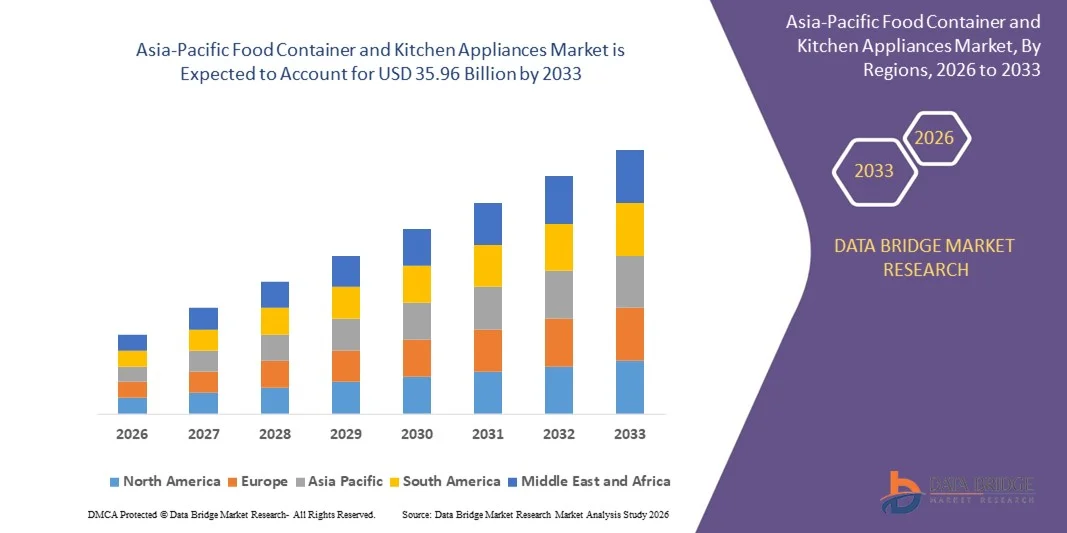

Asia-Pacific Food Container and Kitchen Appliances Market Size

- The Asia-Pacific food container and kitchen appliances market size was valued at USD 21.57 billion in 2025 and is expected to reach USD 35.96 billion by 2033, at a CAGR of 6.60% during the forecast period

- The market growth is largely fuelled by the increasing consumer demand for convenient, sustainable, and innovative kitchen solutions

- The growing preference for eco-friendly and durable food storage solutions, coupled with the rising popularity of smart kitchen appliances, is positioning this market as a key segment in the FMCG industry, significantly boosting its growth

Asia-Pacific Food Container and Kitchen Appliances Market Analysis

- Food containers and kitchen appliances, encompassing cookware, storage solutions, and smart appliances, are critical components of modern households and commercial kitchens, offering enhanced convenience, sustainability, and integration with smart home ecosystems

- The escalating demand is primarily driven by increasing consumer focus on food safety, sustainability, and time-saving kitchen solutions, alongside the growing adoption of smart appliances with IoT and AI capabilities

- China food container and kitchen appliances market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, a growing middle-class population, and high levels of consumer spending on household products

- Japan is expected to witness the highest compound annual growth rate (CAGR) in the Asia-Pacific food container and kitchen appliances market due to increasing adoption of smart and energy-efficient appliances, strong emphasis on product quality and convenience, and growing demand for compact and technologically advanced kitchen solutions driven by changing lifestyles and an aging population

- The Food Containers segment dominated the largest market revenue share of 34.8% in 2025, driven by the critical need for packaging in the growing processed and convenience food industries, alongside rising consumer awareness for food safety and hygiene

Report Scope and Asia-Pacific Food Container and Kitchen Appliances Market Segmentation

|

Attributes |

Asia-Pacific Food Container and Kitchen Appliances Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

• Panasonic Corporation (Japan) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia-Pacific Food Container and Kitchen Appliances Market Trends

Rising Demand For Convenience, Hygiene, And Smart Kitchen Solutions

- The increasing focus on convenient food storage, meal preparation, and hygienic kitchen practices is significantly shaping the Asia-Pacific food container and kitchen appliances market. Consumers are increasingly opting for durable, BPA-free, and easy-to-use containers along with efficient kitchen appliances that simplify daily cooking and storage. This trend is strengthening adoption across urban households, encouraging manufacturers to introduce innovative, space-saving, and multifunctional products tailored to modern lifestyles

- Rapid urbanization, rising disposable incomes, and changing dietary habits are accelerating demand for food containers and kitchen appliances across countries such as China, India, Japan, and South Korea. Busy work schedules and the growth of nuclear families are driving preference for appliances that save time and enhance convenience, while reusable and airtight food containers are gaining popularity for preserving freshness and reducing food waste

- Technological advancements and smart home integration are influencing purchasing decisions, with manufacturers emphasizing energy efficiency, smart features, and modern designs. These factors help brands differentiate products in a competitive market and appeal to tech-savvy consumers, while also supporting sustainability goals through reduced energy consumption and eco-friendly materials

- For instance, in 2024, leading appliance manufacturers in Japan and South Korea expanded their portfolios with smart kitchen appliances and modular food storage solutions designed for compact urban homes. These launches targeted consumers seeking efficiency, hygiene, and modern aesthetics, with strong distribution across online platforms, specialty stores, and large retail chains

- While demand for food containers and kitchen appliances is growing, sustained market expansion depends on continuous product innovation, competitive pricing, and efficient supply chains. Manufacturers are focusing on local manufacturing, improved distribution networks, and product customization to meet diverse consumer preferences across the Asia-Pacific region

Asia-Pacific Food Container and Kitchen Appliances Market Dynamics

Driver

Growing Urbanization And Demand For Convenient Kitchen Solutions

- Rapid urbanization and lifestyle changes are major drivers for the Asia-Pacific food container and kitchen appliances market. Consumers are increasingly investing in modern kitchen products that offer convenience, efficiency, and improved food safety. This shift is encouraging manufacturers to develop compact, multifunctional appliances and advanced storage solutions suitable for smaller living spaces

- Expanding applications across residential households, foodservice outlets, and small commercial kitchens are influencing market growth. Kitchen appliances such as mixers, microwaves, air fryers, and rice cookers, along with airtight food containers, help streamline cooking and storage, meeting the needs of fast-paced urban lifestyles

- Manufacturers are actively promoting new product launches through digital marketing, e-commerce platforms, and retail partnerships. These efforts are supported by rising consumer awareness of hygiene, food preservation, and energy efficiency, encouraging collaboration between appliance brands, material suppliers, and technology providers

- For instance, in 2023, appliance brands in China and India reported increased sales of compact kitchen appliances and reusable food containers, driven by higher adoption among urban households. Companies highlighted energy efficiency, durability, and affordability in marketing campaigns to strengthen brand positioning and customer loyalty

- Although urbanization and convenience trends support growth, wider adoption depends on affordability, product durability, and after-sales service. Investments in localized production, supply chain efficiency, and technology integration will be critical for maintaining competitive advantage in the Asia-Pacific market

Restraint/Challenge

Price Sensitivity And Intense Market Competition

- High price sensitivity among consumers in several Asia-Pacific countries remains a key challenge, particularly in emerging economies. Premium kitchen appliances and high-quality food containers often face resistance due to budget constraints, limiting penetration beyond urban and high-income segments

- Market competition is intense, with the presence of numerous local and international players offering similar products at varying price points. This makes brand differentiation challenging and puts pressure on profit margins, especially for manufacturers investing in advanced features and sustainable materials

- Supply chain disruptions, fluctuating raw material prices, and logistics challenges also impact market growth. Dependence on plastics, metals, and electronic components exposes manufacturers to cost volatility, which can affect pricing strategies and product availability

- For instance, in 2024, manufacturers in Southeast Asia reported challenges related to rising raw material costs and competitive pricing pressures from unorganized local players. These factors limited the adoption of premium kitchen appliances and branded food containers in price-sensitive markets

- Addressing these challenges will require cost optimization, product innovation, and strategic pricing. Strengthening distribution networks, expanding e-commerce presence, and educating consumers on long-term value, durability, and energy savings will be essential to unlock the long-term growth potential of the Asia-Pacific food container and kitchen appliances market

Asia-Pacific Food Container and Kitchen Appliances Market Scope

The market is segmented on the basis of product type, material, and distribution channel.

- By Product Type

On the basis of product type, the Global Food Container and Kitchen Appliances Market is segmented into cookware, kitchen appliances, food containers, serveware, and baby/kids. The Food Containers segment dominated the largest market revenue share of 34.8% in 2025, driven by the critical need for packaging in the growing processed and convenience food industries, alongside rising consumer awareness for food safety and hygiene.

The Kitchen Appliances segment is expected to witness robust growth from 2026 to 2033. This growth is driven by increasing disposable incomes, urbanization, and the rising adoption of smart and energy-efficient kitchen appliances. The demand for modern and multi-functional appliances that offer convenience and enhanced cooking experiences is a key driver.

- By Material

On the basis of material, the Global Food Container and Kitchen Appliances Market is segmented into rigid packaging, flexible packaging, paperboard, metal, glass, and others. The Rigid Packaging segment hold the largest market revenue share in 2025, primarily due to its widespread use for durability, protection, and preservation of food products across various applications, including dairy, beverages, and ready-to-eat meals.

The Rigid Packaging segment is also anticipated to witness the fastest growth rate from 2026 to 2033, driven by continuous innovations in material science offering enhanced barrier properties and sustainability features, alongside increasing demand for longer shelf life and improved product safety.

- By Distribution Channel

On the basis of distribution channel, the Global Food Container and Kitchen Appliances Market is segmented into store-based retailers and e-commerce. The Store-Based Retailers segment hold the largest market revenue share in 2025, attributed to consumers' preference for physical inspection of products, immediate purchase, and personalized assistance, especially for larger kitchen appliances.

The E-commerce segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rising trend of online shopping, increased internet penetration, convenient home delivery options, and the wide array of products available on digital platforms, making it easier for consumers to compare and purchase.

Asia-Pacific Food Container and Kitchen Appliances Market Regional Analysis

- China food container and kitchen appliances market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, a growing middle-class population, and high levels of consumer spending on household products

- China represents one of the largest markets for kitchen appliances and food storage solutions, with strong demand across residential, commercial, and foodservice applications.

- The expansion of smart cities, rising adoption of modern kitchens, and availability of affordable products from strong domestic manufacturers are key factors driving market growth

Japan Food Container And Kitchen Appliances Market Insight

The Japan food container and kitchen appliances market is expected to witness strong growth from 2026 to 2033, driven by the country’s advanced technological landscape, high urban density, and strong demand for convenience-oriented household products. Japanese consumers place significant emphasis on hygiene, precision, and space efficiency, which is accelerating the adoption of high-quality food containers and compact, multifunctional kitchen appliances. The integration of smart features, energy-efficient technologies, and minimalist designs is further supporting market growth. Moreover, Japan’s aging population is likely to increase demand for easy-to-use, ergonomic, and safe kitchen appliances that simplify daily cooking and food storage in both residential and small commercial settings

Asia-Pacific Food Container and Kitchen Appliances Market Share

The Asia-Pacific food container and kitchen appliances industry is primarily led by well-established companies, including:

• Panasonic Corporation (Japan)

• LG Electronics Inc. (South Korea)

• Samsung Electronics Co., Ltd. (South Korea)

• Haier Group Corporation (China)

• Midea Group Co., Ltd. (China)

• Whirlpool of India Ltd. (India)

• Godrej Appliances (India)

• Bajaj Electricals Ltd. (India)

• Sharp Corporation (Japan)

• Toshiba Lifestyle Products & Services Corporation (Japan)

• Hitachi, Ltd. (Japan)

• TTK Prestige Ltd. (India)

• Joyoung Co., Ltd. (China)

• SUPOR (China)

• Electrolux Appliances Asia Pacific (Australia)

Latest Developments in Asia-Pacific Food Container and Kitchen Appliances Market

- In March 2025, Samsung Electronics Co., Ltd., Product Launch, announced the introduction of its first Air to Water Heat Pump lineup, showcasing advanced heating solutions developed by an Asia-Pacific–origin company. The system is designed to deliver high energy efficiency, ultra-low noise performance, and smart home integration through AI Home and SmartThings connectivity. This development strengthens Samsung’s global appliance portfolio while highlighting APAC-led innovation in sustainable home technologies. The launch supports the growing demand for energy-efficient climate solutions and enhances Samsung’s competitive positioning in the global heating and kitchen appliance ecosystem

- In May 2024, Thermomix, Product Innovation, launched the Thermomix Sensor, a smart cooking thermometer aimed at improving precision and consistency in home cooking. The device enables real-time temperature monitoring through mobile connectivity, supporting baking, grilling, and roasting applications. This innovation benefits consumers by reducing cooking errors and enhancing convenience, particularly in premium kitchen segments. The launch reinforces Thermomix’s strong presence in Asia-Pacific markets and drives increased adoption of smart kitchen appliances across the region.

- In February 2023, Electrolux, Market Expansion and Product Launch, introduced a premium range of built-in kitchen appliances in India, including ovens, hobs, dishwashers, and coffee machines. The new lineup focuses on energy efficiency, smart features, and sustainable cooking solutions tailored to modern Indian households. This expansion enhances Electrolux’s footprint in the Asia-Pacific region and supports rising demand for premium kitchen infrastructure. The development positively impacts the market by accelerating innovation, sustainability adoption, and consumer interest in advanced kitchen appliances

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.