Asia Pacific Hemodialysis Peritoneal Dialysis Market

Market Size in USD Billion

USD

29.40 Billion

USD

54.94 Billion

2025

2033

USD

29.40 Billion

USD

54.94 Billion

2025

2033

| 2026 - 2033 | |

| USD 29.40 Billion | |

| USD 54.94 Billion | |

| % | |

|

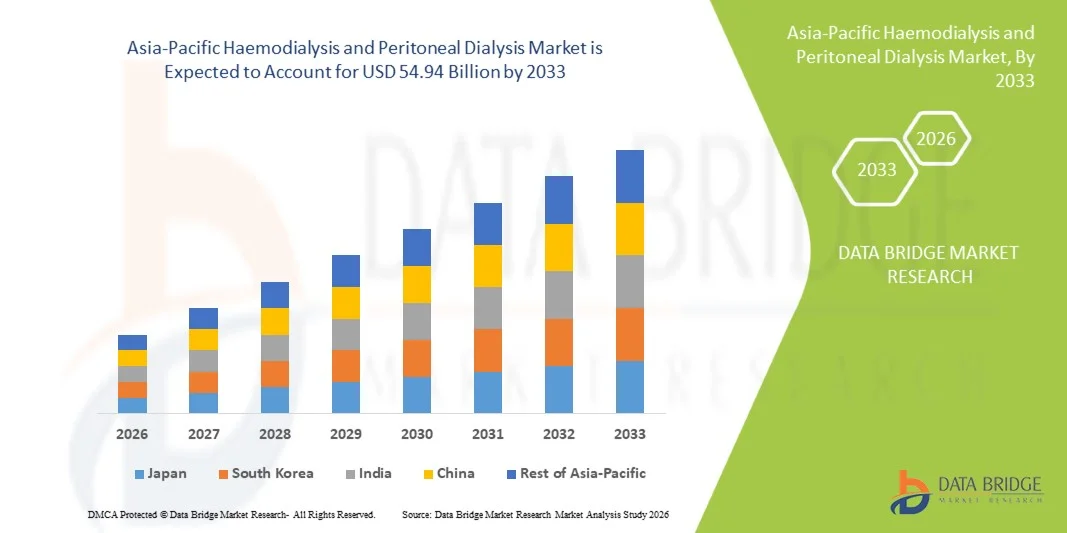

Asia-Pacific Haemodialysis and Peritoneal Dialysis Market Size

- The Asia-Pacific Haemodialysis and Peritoneal Dialysis Market size was valued at USD 29.40 billion in 2025 and is expected to reach USD 54.94 billion by 2033, at a CAGR of 8.13% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic kidney diseases, rising geriatric population, and growing demand for renal replacement therapies, leading to higher adoption of haemodialysis and peritoneal dialysis solutions across healthcare settings

- Furthermore, increasing awareness regarding early diagnosis, advancements in dialysis technologies, and a growing preference for home-based dialysis treatments are establishing haemodialysis and peritoneal dialysis as essential components of modern renal care. These converging factors are accelerating the uptake of these solutions, thereby significantly boosting the industry's growth

Asia-Pacific Haemodialysis and Peritoneal Dialysis Market Analysis

- Haemodialysis and peritoneal dialysis solutions, offering life-sustaining renal replacement therapies, are increasingly vital components of modern healthcare systems across hospitals and home care settings due to their critical role in managing end-stage renal disease and improving patient survival and quality of life

- The escalating demand for dialysis solutions is primarily fueled by the rising prevalence of chronic kidney diseases, increasing geriatric population, growing awareness about treatment options, and a rising preference for home-based and cost-effective dialysis therapies

- China dominated the Asia-Pacific Haemodialysis and Peritoneal Dialysis Market with the largest revenue share of approximately 39.6% in 2025, supported by a large patient pool, expanding healthcare infrastructure, and increasing government initiatives to improve access to dialysis treatment

- India is expected to be the fastest growing region in the Asia-Pacific Haemodialysis and Peritoneal Dialysis Market during the forecast period, with a projected CAGR of 9.2%, driven by rising prevalence of chronic kidney diseases, improving healthcare access, and growing awareness about dialysis treatment options

- The hemodialysis segment dominated the largest market revenue share of 64.5% in 2025, driven by its widespread adoption in hospitals and dialysis centers for treating end-stage renal disease

Report Scope and Asia-Pacific Haemodialysis and Peritoneal Dialysis Market Segmentation

|

Attributes |

Haemodialysis and Peritoneal Dialysis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

• Fresenius Medical Care (Germany) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Asia-Pacific Haemodialysis and Peritoneal Dialysis Market Trends

“Rising Adoption of Home-Based Dialysis and Technological Advancements”

- A significant and accelerating trend in the Asia-Pacific Haemodialysis and Peritoneal Dialysis Market is the increasing adoption of home-based dialysis therapies, supported by advancements in portable and user-friendly dialysis technologies. This trend is enhancing patient convenience, reducing hospital dependency, and improving overall quality of life for individuals with chronic kidney disease

- For instance, in 2024, Fresenius Medical Care expanded its home dialysis solutions portfolio across Asia-Pacific, promoting peritoneal dialysis systems that enable patients to perform treatment safely at home with minimal clinical supervision

- The growing burden of end-stage renal disease (ESRD) across countries such as China, India, and Japan is further accelerating the demand for efficient and accessible dialysis solutions

- Technological advancements in dialysis machines, including compact designs, automated fluid management systems, and improved safety features, are supporting the shift toward home-based care

- In addition, healthcare systems in the region are increasingly promoting peritoneal dialysis as a cost-effective alternative to in-center haemodialysis, especially in resource-constrained settings

- The integration of remote monitoring tools is also enabling healthcare professionals to track patient progress and treatment adherence in real time

- Rising awareness regarding early diagnosis and treatment of kidney disorders is further contributing to the increased adoption of dialysis therapies

- Government initiatives aimed at improving access to renal care services are supporting the expansion of dialysis infrastructure across rural and urban areas

- The growing geriatric population, which is more susceptible to kidney-related disorders, is also driving demand for long-term dialysis solutions

- This trend toward decentralized and patient-centric dialysis care is significantly transforming the treatment landscape in the Asia-Pacific region

Asia-Pacific Haemodialysis and Peritoneal Dialysis Market Dynamics

Driver

“Increasing Prevalence of Chronic Kidney Disease and Expanding Healthcare Access”

- The rising prevalence of chronic kidney disease (CKD) and end-stage renal disease (ESRD) across the Asia-Pacific region is a major driver for the growth of the Asia-Pacific Haemodialysis and Peritoneal Dialysis Market

- For instance, in 2025, World Health Organization reported a significant increase in kidney-related disorders in developing Asian countries, largely attributed to the growing incidence of diabetes and hypertension, thereby increasing the demand for dialysis treatments

- The increasing number of patients requiring long-term renal replacement therapy is placing significant demand on healthcare systems and dialysis service providers

- Expanding healthcare infrastructure and improved access to treatment facilities in emerging economies are further supporting market growth

- Governments and healthcare organizations are investing in dialysis centers and subsidizing treatment costs to improve patient access

- The growing awareness regarding early diagnosis and management of kidney diseases is also contributing to increased treatment adoption

- In addition, the rise in lifestyle-related diseases is further fueling the demand for dialysis therapies across the region

- The availability of reimbursement policies in certain countries is encouraging patients to opt for regular dialysis treatment

- Increasing partnerships between public and private healthcare providers are also expanding the reach of dialysis services

- Overall, the growing patient pool and improving healthcare accessibility are significantly driving market expansion

Restraint/Challenge

“High Treatment Costs and Limited Access in Rural Areas”

- The high cost associated with dialysis treatment and limited access to advanced healthcare facilities in rural regions pose significant challenges to market growth

- For instance, according to International Society of Nephrology, a large proportion of patients in low- and middle-income countries in Asia-Pacific face financial constraints, limiting their ability to access regular dialysis treatment

- Haemodialysis requires substantial infrastructure, including specialized equipment and trained healthcare professionals, which may not be readily available in remote areas

- The recurring cost of dialysis sessions, medications, and hospital visits can place a significant financial burden on patients and their families

- Limited awareness and late diagnosis of kidney diseases in certain regions further restrict timely treatment initiation

- In addition, shortages of skilled nephrologists and technicians can impact the quality and availability of dialysis services

- Inadequate reimbursement policies in some countries also hinder patient access to advanced treatment options

- Transportation challenges and long travel distances to dialysis centers can reduce treatment adherence among rural populations

- The risk of complications and infections associated with dialysis procedures also raises concerns among patients

- Addressing these challenges through cost-effective solutions, infrastructure development, and improved healthcare policies will be essential for sustained market growth

Asia-Pacific Haemodialysis and Peritoneal Dialysis Market Scope

The market is segmented on the basis of type, products, modality, haemodialysis water treatment systems, and end user.

• By Type

On the basis of type, the Asia-Pacific Haemodialysis and Peritoneal Dialysis Market is segmented into Hemodialysis and Peritoneal Dialysis. The hemodialysis segment dominated the largest market revenue share of 64.5% in 2025, driven by its widespread adoption in hospitals and dialysis centers for treating end-stage renal disease. Hemodialysis remains the most commonly used dialysis modality due to its clinical effectiveness, structured treatment protocols, and availability of advanced dialysis machines. The segment benefits from strong healthcare infrastructure, especially in developed regions, where in-center dialysis services are highly accessible. Increasing prevalence of chronic kidney disease (CKD), diabetes, and hypertension is significantly boosting demand. In addition, favorable reimbursement policies and government support programs are encouraging patients to opt for hemodialysis. Technological advancements such as high-flux dialyzers and improved filtration systems are enhancing treatment outcomes. The presence of skilled healthcare professionals and established dialysis networks further strengthens segment growth. Hospitals continue to prefer hemodialysis due to better monitoring and reduced risk in critical cases. Moreover, growing investments in dialysis centers and expansion of healthcare facilities globally are supporting dominance. Rising geriatric population and increasing awareness about renal care are further contributing to market expansion.

The peritoneal dialysis segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, driven by increasing preference for home-based treatment and improved patient convenience. Peritoneal dialysis offers flexibility, allowing patients to perform dialysis at home without frequent hospital visits, which is particularly beneficial for elderly and working populations. The growing shift toward home healthcare and cost-effective treatment options is accelerating adoption. Advancements in automated peritoneal dialysis (APD) systems are making the process more efficient and user-friendly. Rising awareness about infection control and reduced dependency on hospital infrastructure is further supporting demand. Governments and healthcare organizations are promoting peritoneal dialysis to reduce burden on dialysis centers. Emerging markets are witnessing increased uptake due to lower infrastructure requirements compared to hemodialysis. Improved training programs and patient education initiatives are also enhancing acceptance. The segment is further supported by innovations in dialysis solutions and catheter designs. Increasing healthcare expenditure and expansion of home care services are key growth drivers.

• By Products

On the basis of products, the market is segmented into Machine, Consumables, and Services. The consumables segment dominated the market with a revenue share of 58.2% in 2025, owing to the recurring need for dialyzers, tubing, and dialysis fluids in both hemodialysis and peritoneal dialysis procedures. Consumables are essential for every dialysis session, leading to consistent and high-volume demand across healthcare settings. The segment benefits from the increasing number of dialysis patients globally, which directly drives repeat purchases. Hospitals and dialysis centers rely heavily on high-quality consumables to ensure patient safety and treatment efficiency. Continuous innovation in biocompatible materials and improved filtration efficiency is enhancing product adoption. In addition, stringent regulatory standards are encouraging the use of certified and high-performance consumables. The rising incidence of kidney disorders and growing treatment frequency further support segment dominance. Expansion of dialysis centers in emerging economies is boosting demand. Strong distribution networks and partnerships with healthcare providers also contribute to growth. Moreover, increasing awareness regarding infection prevention and hygiene is driving demand for disposable consumables.

The services segment is expected to grow at the fastest CAGR of 9.6% from 2026 to 2033, driven by the increasing outsourcing of dialysis services and maintenance activities by healthcare providers. Service offerings include equipment maintenance, training, and dialysis center management, which are gaining traction due to cost efficiency and operational convenience. Hospitals are increasingly partnering with third-party service providers to improve patient care and reduce administrative burden. The rise of specialized dialysis service providers is supporting market expansion. Growing demand for home dialysis services is also contributing to segment growth. Technological advancements and digital monitoring systems are enhancing service quality and efficiency. Emerging markets are witnessing rapid growth due to increasing healthcare investments. Government initiatives to improve dialysis accessibility are further boosting service adoption. The segment is also benefiting from the expansion of telehealth and remote monitoring solutions. Increasing patient load and need for continuous care are key drivers.

• By Modality

On the basis of modality, the market is segmented into Conventional Long-Term, Short Daily, and Nocturnal. The conventional long-term segment dominated with a revenue share of 61.7% in 2025, as it remains the standard and most widely practiced dialysis regimen globally. This modality is commonly used in clinical settings due to its established protocols and ease of implementation. Healthcare providers prefer conventional dialysis due to its predictability and compatibility with existing infrastructure. The segment benefits from widespread availability in hospitals and dialysis centers. Increasing patient population and growing incidence of kidney failure are major contributors. Moreover, reimbursement support for conventional dialysis sessions encourages adoption. The segment is also supported by trained medical staff and standardized procedures. Technological advancements in dialysis machines are further improving efficiency. High patient trust and familiarity with the procedure also play a key role. Expansion of dialysis facilities in developing regions is boosting growth.

The nocturnal dialysis segment is projected to witness the fastest CAGR of 10.4% from 2026 to 2033, driven by its clinical benefits and improved patient outcomes. Nocturnal dialysis allows longer treatment duration during sleep, leading to better toxin removal and enhanced patient well-being. Increasing awareness about the benefits of extended dialysis sessions is supporting adoption. The modality is gaining popularity among patients seeking better quality of life and flexibility. Home-based nocturnal dialysis is further driving demand. Technological advancements enabling safe overnight dialysis are key growth factors. Healthcare providers are increasingly recommending this approach for suitable patients. Rising focus on personalized treatment is also contributing to growth. The segment is supported by improved monitoring systems and reduced complications. Growing healthcare expenditure and patient-centric care models are accelerating adoption.

• By Haemodialysis Water Treatment Systems

On the basis of haemodialysis water treatment systems, the market is segmented into Central Water Disinfection Systems and Portable Water Disinfection Systems. The central water disinfection systems segment dominated the market with a revenue share of 62.4% in 2025, driven by its widespread adoption in large hospitals and dialysis centers requiring continuous and high-volume water purification. These systems ensure consistent water quality, which is critical for safe and effective haemodialysis procedures. The segment benefits from strong demand in established healthcare facilities where centralized infrastructure is already in place. Central systems are preferred due to their efficiency in handling multiple dialysis units simultaneously. Increasing investments in hospital infrastructure and expansion of dialysis centers are further supporting growth. Strict regulatory standards regarding water purity in dialysis procedures are also driving adoption. In additions, these systems offer long-term cost advantages for high-capacity facilities. The presence of advanced monitoring and automated disinfection features enhances operational reliability. Growing prevalence of chronic kidney diseases is increasing the demand for large-scale dialysis setups. Moreover, developed regions continue to rely heavily on centralized systems due to their scalability and performance.

The portable water disinfection systems segment is expected to witness the fastest CAGR of 10.7% from 2026 to 2033, driven by the rising demand for flexible and decentralized dialysis solutions. Portable systems are gaining popularity in home care settings and smaller clinics due to their compact size and ease of installation. The increasing shift toward home-based dialysis is a major factor fueling segment growth. These systems enable patients to receive treatment outside traditional healthcare facilities, improving convenience and accessibility. Technological advancements have significantly improved the efficiency and safety of portable systems. Growing healthcare infrastructure in emerging markets is also supporting adoption. Portable systems require lower initial investment, making them attractive for smaller providers. The segment is further driven by increasing awareness about home dialysis options. Government initiatives promoting home healthcare and cost-effective treatment are contributing to growth. In additions, the rising geriatric population and need for patient-centric care models are accelerating demand.

• By End User

On the basis of end user, the market is segmented into Hospitals, Dialysis Centers, and Home Care Settings. The dialysis centers segment dominated the market with a revenue share of 49.8% in 2025, driven by the increasing number of specialized centers offering dedicated renal care services. Dialysis centers provide cost-effective and efficient treatment compared to hospitals, making them a preferred choice for patients. The segment benefits from high patient inflow and structured treatment environments. Expansion of private dialysis chains and partnerships with healthcare providers are supporting growth. Increasing prevalence of CKD and ESRD is driving patient volume. Dialysis centers offer advanced equipment and trained staff, ensuring high-quality care. Government initiatives to establish dialysis units in underserved areas are also contributing. The segment is further supported by flexible treatment schedules and accessibility. Growing urbanization and healthcare infrastructure development are boosting demand.

The home care settings segment is expected to witness the fastest CAGR of 11.2% from 2026 to 2033, driven by the rising trend of home-based healthcare and patient preference for convenience. Home dialysis reduces hospital visits and associated costs, making it an attractive option for long-term treatment. Increasing adoption of peritoneal dialysis and portable hemodialysis systems is supporting growth. Technological advancements are enabling safe and efficient home treatment. The segment is gaining traction among elderly patients and those with mobility challenges. Government support and reimbursement policies for home care are encouraging adoption. Rising awareness and patient education programs are also contributing. The COVID-19 pandemic has further accelerated demand for home-based treatments. Improved monitoring systems and telehealth integration are enhancing patient outcomes. Growing focus on personalized care is driving segment expansion.

Asia-Pacific Haemodialysis and Peritoneal Dialysis Market Regional Analysis

- The Asia-Pacific Haemodialysis and Peritoneal Dialysis Market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by the rising prevalence of chronic kidney diseases, increasing healthcare expenditure, and expanding access to dialysis services across countries such as China, Japan, and India

- The region is witnessing strong growth due to improving healthcare infrastructure, growing awareness regarding renal care, and supportive government initiatives aimed at enhancing access to dialysis treatment

- Furthermore, the increasing adoption of advanced dialysis technologies and the expansion of dialysis centers are improving treatment accessibility and outcomes, thereby contributing to market growth across the region

China Asia-Pacific Haemodialysis and Peritoneal Dialysis Market Insight

The China Asia-Pacific Haemodialysis and Peritoneal Dialysis Market accounted for the largest market revenue share of approximately 39.6% in Asia-Pacific in 2025, attributed to the country’s large patient pool, increasing prevalence of chronic kidney diseases, and rapid expansion of healthcare infrastructure. Government initiatives aimed at improving access to dialysis treatment, particularly in rural and underserved areas, are significantly supporting market growth. In additions, the increasing number of dialysis centers and rising adoption of advanced dialysis technologies are further propelling the market in China.

India Asia-Pacific Haemodialysis and Peritoneal Dialysis Market Insight

The India Asia-Pacific Haemodialysis and Peritoneal Dialysis Market is expected to grow at the fastest CAGR of 9.2% during the forecast period, driven by the rising incidence of chronic kidney diseases, increasing awareness regarding early diagnosis and treatment, and improving access to healthcare services. Government programs promoting affordable dialysis treatment, along with the expansion of dialysis centers across urban and rural areas, are contributing to market growth. Furthermore, the growing adoption of cost-effective peritoneal dialysis and increasing investments in healthcare infrastructure are supporting the expansion of the market in India.

Asia-Pacific Haemodialysis and Peritoneal Dialysis Market Share

The Haemodialysis and Peritoneal Dialysis industry is primarily led by well-established companies, including:

• Fresenius Medical Care (Germany)

• Baxter International Inc. (U.S.)

• DaVita Inc. (U.S.)

• B. Braun SE (Germany)

• Nipro Corporation (Japan)

• Asahi Kasei Medical Co., Ltd. (Japan)

• Medtronic (Ireland)

• Cantel Medical (U.S.)

• Toray Medical Co., Ltd. (Japan)

• NxStage Medical, Inc. (U.S.)

• JMS Co., Ltd. (Japan)

• Rockwell Medical, Inc. (U.S.)

• Dialife SA (Switzerland)

• Outset Medical, Inc. (U.S.)

• Kawasumi Laboratories, Inc. (Japan)

• SWS Hemodialysis Care Co., Ltd. (China)

• Nikkiso Co., Ltd. (Japan)

• WEGO Group (China)

• Shenzhen Landwind Industry Co., Ltd. (China)

• Medica S.p.A. (Italy)

Latest Developments in Asia-Pacific Haemodialysis and Peritoneal Dialysis Market

- In March 2021, Baxter International Inc. announced that it received U.S. FDA 510(k) clearance for its AK 98 hemodialysis machine, designed for intermittent hemodialysis and ultrafiltration treatments in patients with acute or chronic renal failure. The approval strengthened Baxter’s hemodialysis portfolio and expanded treatment options for healthcare providers, reinforcing its position in the global dialysis market

- In August 2024, Baxter International Inc. announced a definitive agreement to divest its Kidney Care segment to Carlyle for approximately USD 3.8 billion, with plans to establish it as a new independent company named Vantive. This strategic move aimed to enhance focus on innovation and expand access to dialysis therapies, including both hemodialysis and peritoneal dialysis solutions globally

- In October 2024, Baxter International Inc. reported supply disruptions of peritoneal dialysis solutions in the U.S. after hurricane-related flooding impacted its North Carolina manufacturing facility. The company initiated imports from international sites and ramped up production to address shortages, highlighting the critical importance of supply chain resilience in dialysis care

- In October 2024, Baxter International Inc. announced efforts to restore patient access to peritoneal dialysis therapies to pre-disruption levels following supply shortages caused by manufacturing interruptions. The company increased allocations to hospitals and prioritized vulnerable patient groups, emphasizing the growing demand and dependence on dialysis solutions

- In October 2025, Vantive, formerly part of Baxter’s Kidney Care segment, officially launched operations in Vietnam to expand access to advanced kidney care solutions, including dialysis therapies. The initiative focused on improving treatment accessibility and strengthening healthcare infrastructure in emerging markets

- In January 2025, Baxter International Inc. announced increased allocations and expanded new patient starts for peritoneal dialysis solutions as part of efforts to stabilize supply and meet rising global demand. This development reflects the growing adoption of home-based dialysis therapies and the need for consistent supply of critical consumables

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.