Asia Pacific Hepato Pancreatico Biliary Hpb Surgeries Surgical Devices Market

Market Size in USD Billion

USD

1.29 Billion

USD

2.70 Billion

2024

2032

USD

1.29 Billion

USD

2.70 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.29 Billion | |

| USD 2.70 Billion | |

| % | |

|

Asia-Pacific Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices Market Size

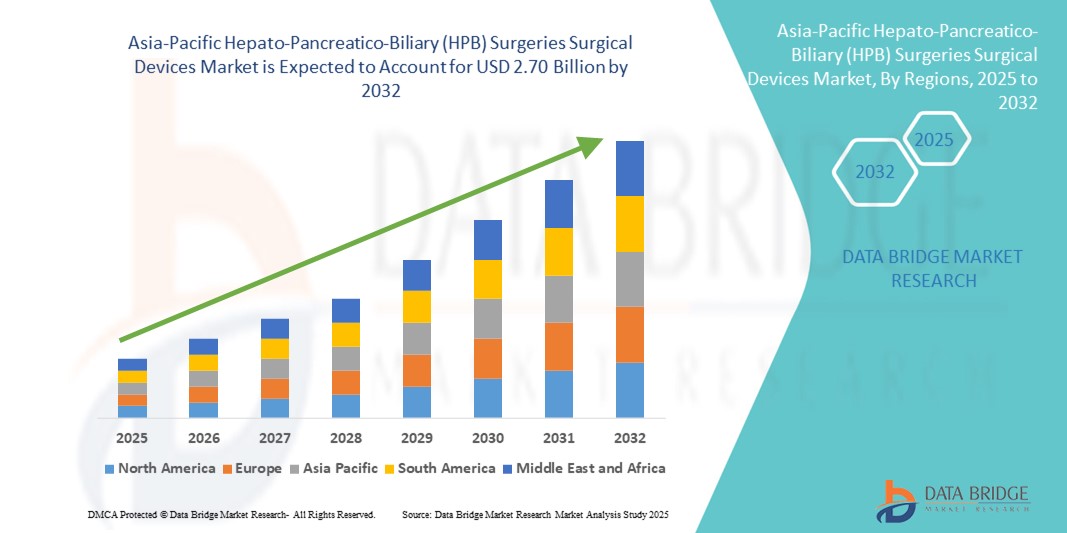

- The Asia-Pacific hepato-pancreatico-biliary (HPB) surgeries surgical devices market size was valued at USD 1.29 billion in 2024 and is expected to reach USD 2.70 billion by 2032, at a CAGR of 9.60% during the forecast period

- The market growth is largely fueled by increasing awareness, rising healthcare access, and advancements in surgical technologies across Asia-Pacific, enabling timely diagnosis and effective treatment of hepato-pancreatico-biliary disorders. The region is witnessing a surge in the number of complex HPB surgeries, particularly in rapidly urbanizing countries such as India, China, and Indonesia, which is contributing to the growing adoption of advanced surgical devices for HPB procedures

- Furthermore, escalating investments in healthcare infrastructure, expansion of specialized surgical centers in both urban and rural areas, and increasing public-private partnerships are driving innovation and availability of premium HPB surgical devices. Government initiatives aimed at improving healthcare outcomes, coupled with the growing presence of international medical device companies and strengthening local manufacturing capabilities, are significantly boosting the growth of the Asia-Pacific Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices market

Asia-Pacific Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices Market Analysis

- The Asia-Pacific Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices Market is witnessing significant growth, propelled by increasing demand for advanced surgical tools and devices used in complex liver, pancreas, and biliary tract surgeries across countries such as China, India, Japan, South Korea, Australia, Thailand, Indonesia, and Vietnam

- Rising incidence of hepatobiliary cancers, growing geriatric populations, and expanding healthcare infrastructure are key factors fueling this market expansion

- China dominated the Asia-Pacific hepato-pancreatico-biliary (HPB) surgeries surgical devices market with the largest revenue share of 42.5% in 2024. This dominance is supported by China’s well-established healthcare infrastructure, increasing number of specialized surgical centers, and robust government initiatives aimed at improving cancer care and surgical outcomes

- India is expected to be the fastest growing country in the Asia-Pacific hepato-pancreatico-biliary (HPB) surgeries surgical devices market with a CAGR of around 14.2% during the forecast period, driven by growing awareness about HPB diseases, rapid advancements in minimally invasive surgical technologies, and the expansion of healthcare services into semi-urban and rural regions. Rising healthcare expenditure and improving access to modern surgical devices further boost market growth in India

- The Adult age group dominated the Asia-Pacific hepato-pancreatico-biliary (HPB) surgeries surgical devices market in 2024 with an estimated share of 70.8%, owing to the higher prevalence of HPB diseases such as liver cancer, pancreatitis, and gallstones in this demographic

Report Scope and Asia-Pacific Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices Market Segmentation

|

Attributes |

Asia-Pacific Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia-Pacific Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices Market Trends

Growing Comfort-Oriented Innovation and Surgical Precision Enhancements

- A significant and accelerating trend in the Asia-Pacific hepato-pancreatico-biliary (HPB) surgeries surgical devices market is the increasing focus on developing comfort-driven surgical devices and precision-enhancing technologies tailored to complex hepatobiliary procedures. Manufacturers are investing in ergonomic instrument designs that reduce surgeon fatigue and improve procedural accuracy

- Major device developers across the region are collaborating with healthcare professionals and biomedical engineers to create next-generation HPB surgical tools featuring improved maneuverability, minimally invasive capabilities, and enhanced tissue compatibility. These innovations address rising demand for safer, more efficient surgeries with quicker patient recovery times

- Increasing adoption of robotic-assisted and laparoscopic HPB surgery systems in hospitals and specialty clinics across countries such as Japan, South Korea, China, and Australia is driving market growth. These systems offer enhanced visualization, precision, and reduced complication rates during hepato-pancreato-biliary surgeries

- Academic medical centers and research institutions in the Asia-Pacific region are actively conducting clinical trials and outcome studies on advanced HPB surgical devices, focusing on safety profiles, operative efficiency, and long-term patient benefits. This evidence-based approach supports product development and clinician adoption

- As healthcare infrastructure expands and emphasis on minimally invasive surgical techniques grows across Asia-Pacific, the Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices market is poised for sustained growth—fueled by technological innovation, clinical validation, and increasing procedural volumes in hepatobiliary care

Asia-Pacific Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices Market Dynamics

Driver

Growing Demand Driven by Rising Health Awareness and Advancements in Surgical Care

- The Asia-Pacific hepato-pancreatico-biliary (HPB) surgeries surgical devices market is experiencing significant growth due to increasing awareness about liver, pancreatic, and biliary health, as well as the rising prevalence of HPB diseases in the region. Countries such as China, India, Japan, and Australia are witnessing a surge in demand for advanced surgical devices as patients and healthcare providers prioritize timely, effective surgical interventions

- For instance, in early 2024, leading medical device manufacturers expanded their product portfolios to include state-of-the-art electrosurgery instruments and robotic-assisted surgical systems designed to improve precision and outcomes in complex HPB surgeries, catering especially to tertiary care hospitals and specialty clinics

- The growing incidence of liver cancer, pancreatic cancer, and gall bladder diseases, combined with enhanced diagnostic capabilities, is driving an increased number of surgeries, thereby propelling demand for innovative and minimally invasive surgical devices across the region

- Government initiatives focused on improving healthcare infrastructure and increasing access to specialized surgical care in rural and urban areas are further supporting market expansion. Public-private partnerships and investments in advanced surgical centers contribute to the growing adoption of HPB surgical devices

- The rapid digitization of healthcare and the integration of robotic and imaging technologies into HPB surgeries are enhancing surgical precision, reducing patient recovery times, and increasing procedural safety, making these technologies more attractive to providers and patients alike

Restraint/Challenge

Limited Penetration in Price-Sensitive and Rural Markets

- Despite significant technological advancements in Hepato-Pancreatico-Biliary (HPB) surgical devices, the high costs associated with these sophisticated technologies remain a substantial barrier to widespread adoption, especially within price-sensitive segments and rural markets. This challenge is particularly pronounced in countries across Southeast Asia and South Asia, where healthcare budgets are limited and infrastructure development is still progressing. Many healthcare facilities in these regions face financial constraints that restrict their ability to procure and maintain advanced surgical equipment

- Furthermore, limited awareness among healthcare providers in rural and less-developed areas about the clinical benefits and improved patient outcomes offered by cutting-edge HPB surgical devices contributes to their underutilization. In addition to this, a lack of specialized training and expertise among medical professionals in these locations further hinders the effective deployment of such technologies outside major urban centers and metropolitan hospitals

- Distribution and logistics also pose critical challenges for market penetration. The supply chains for HPB surgical devices are often fragmented, and the delicate nature of the equipment requires careful handling and reliable transportation. Delivering these sophisticated devices to remote and underserved locations can be difficult, resulting in delays and increased costs, which further limit accessibility

- Moreover, many countries in the Asia-Pacific region depend heavily on imports for high-tech HPB surgical devices. This reliance on imported equipment raises the overall cost due to import duties, taxes, and shipping expenses, making these solutions less affordable and accessible for healthcare providers in lower-income settings where cost sensitivity is paramount

- To address these barriers, market players are increasingly focusing on strategies that strengthen local manufacturing capabilities, reducing dependence on imports and enabling more competitive pricing. In addition, targeted education and training programs for healthcare professionals are being implemented to improve awareness and expertise regarding advanced HPB surgical technologies. Companies are also developing more cost-effective and tailored solutions that meet the unique needs and economic realities of emerging markets in the Asia-Pacific region, aiming to expand access and improve surgical outcomes across a broader patient population

Asia-Pacific Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices Market Scope

The market is segmented on the basis of product, indication, type of surgery, age group, end user, and distribution channel.

- By Product

On the basis of product, the Asia-Pacific hepato-pancreatico-biliary (HPB) surgeries surgical devices market is segmented into electrosurgery instruments, endoscope, visualization and robotic surgical system, hand instruments, access instruments, surgical suture and stapler devices, energy/vessel sealing devices, fluid management system, stents, and others. Among these, the Visualization and Robotic Surgical System segment held a commanding lead with an revenue share of 28.5% in 2024. This dominance is attributable to the increasing integration of advanced imaging and robotic technologies in complex HPB procedures, which enhances surgical precision and patient outcomes.

On the other hand, the surgical suture and stapler devices segment is anticipated to experience the fastest growth, registering a CAGR of 11.2% from 2025 to 2032. This surge is driven by rising demand for minimally invasive surgical solutions and innovations in suturing technologies that offer improved efficiency and reduced operative times.

- By Indication

On the basis of indication, the market is segmented into liver cancer, pancreatic cancer, gall stones, bile duct cancer, cirrhosis, pancreatitis, cholecystitis, and others. The liver cancer segment emerged as the clear market leader in 2024, with 32.1% of total revenue. This dominance is largely attributed to the high incidence of liver malignancies across the Asia-Pacific region, coupled with advancements in specialized surgical devices designed specifically for oncological procedures. These devices enhance precision in tumor resection and improve patient survival rates, making them indispensable in liver cancer management.

In contrast, the Pancreatitis segment is expected to register the fastest growth, with a CAGR of 12.5% during the forecast period. This rapid expansion is driven by growing awareness about the disease, improvements in early diagnostic techniques, and an increased adoption of surgical interventions to manage both acute and chronic pancreatitis cases, which are becoming more prevalent due to lifestyle changes and rising healthcare access.

- By Type of Surgery

On the basis of type of surgery, the market is divided into open surgery and minimally invasive surgery. Minimally invasive surgery commanded a significant share of 61.7% in 2024, reflecting a strong regional shift toward less invasive procedures. These surgical approaches are favored due to their numerous patient benefits, including shorter hospital stays, reduced post-operative pain, quicker recovery times, and lower complication rates. The rising availability of laparoscopic and robotic-assisted surgical devices tailored for HPB procedures further supports this preference. Moreover, this segment is forecasted to experience the highest growth rate with a CAGR of 13.8% from 2025 to 2032, driven by continuous technological innovations and the growing confidence of surgeons and patients in minimally invasive techniques.

- By Age Group

On the basis of age group, the market is segmented into pediatric, adult, and geriatric. The adult age group dominated the market in 2024 with a share of 70.8%, owing to the higher prevalence of HPB diseases such as liver cancer, pancreatitis, and gallstones in this demographic. The adult population’s increasing healthcare access and rising incidence of lifestyle-related conditions further reinforce this segment’s leadership.

Meanwhile, the Geriatric segment is poised for the fastest growth during the forecast period, with a CAGR of 10.9% through 2032. This growth is largely fueled by the aging population across Asia-Pacific countries and the corresponding rise in age-associated HPB disorders, which necessitate specialized surgical management. The increasing focus on geriatric care and advancements in surgical techniques adapted for older patients are also contributing to this upward trend.

- By End User

On the basis of end user, the market includes hospitals, specialty clinics, ambulatory surgical centers, trauma centers, and others. Hospitals dominated as the largest end-user segment, commanding an revenue share of 74.2% in 2024. This dominance is primarily due to hospitals’ well-established infrastructure, advanced surgical facilities, and ability to manage complex Hepato-Pancreatico-Biliary (HPB) surgeries that require multidisciplinary teams and specialized equipment. Large hospital networks also benefit from higher patient volumes and stronger purchasing power, further solidifying their leadership in this segment.

On the other hand, ambulatory surgical centers are projected to register the fastest growth, with a CAGR of 12.3% from 2025 to 2032. This surge is driven by the increasing preference for outpatient surgical procedures that offer reduced hospital stays, lower costs, and faster patient turnover. ASCs are becoming attractive alternatives for less complex HPB surgeries, supported by advancements in minimally invasive techniques that enable safe and efficient treatment outside traditional hospital settings.

- By Distribution Channel

On the basis of distribution channel, the market is divided into direct tender, retail sales, and others. The direct tender segment held the dominant position with a substantial market share of 65.3% in 2024. This leadership is attributed to procurement strategies adopted by governments and large healthcare institutions that favor bulk purchasing agreements and long-term supply contracts to ensure consistent availability and cost-effectiveness of surgical devices. Direct tenders also facilitate streamlined logistics and regulatory compliance, making them a preferred choice in public healthcare sectors across the Asia-Pacific region.

Meanwhile, the Retail Sales is anticipated to experience the fastest growth, registering a robust CAGR of 14.1% during the forecast period. This rapid expansion is fueled by the rising penetration of e-commerce platforms, improved internet accessibility, and changing consumer preferences that favor the convenience of online purchasing. In addition, online channels enable manufacturers and distributors to reach a broader customer base, offer detailed product information, and provide flexible delivery and return policies, all of which contribute to accelerating market growth in this segment.

Asia-Pacific Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices Market Regional Analysis

- Asia-Pacific dominated the global hepato-pancreatico-biliary (HPB) surgeries surgical devices market, accounting for the largest revenue share of 30.3% in 2024. This leadership is driven by the region’s vast population base, increasing healthcare infrastructure investments, and rising demand for advanced surgical technologies to treat HPB diseases. Rapid urbanization, growing health awareness, and the expansion of specialized surgical centers are key factors supporting the region’s dominance

- Increasing demand from hospitals, specialty clinics, and ambulatory surgical centers, coupled with expanding government healthcare initiatives and rising healthcare expenditure, has further contributed to the robust growth of the market in Asia-Pacific

- The market is strengthened by strong domestic manufacturing capabilities in countries such as China, India, and Vietnam, alongside the expansion of distribution networks across Southeast Asia. Moreover, government policies and incentives aimed at improving healthcare access and cancer care management are accelerating adoption of advanced HPB surgical devices throughout the region

China Asia-Pacific Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices Market Insight

The China hepato-pancreatico-biliary (HPB) surgeries surgical devices market led the Asia-Pacific Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices market with the largest revenue share of 42.5% in 2024. This dominance is supported by China’s well-established healthcare infrastructure, increasing number of specialized surgical centers, and robust government initiatives focused on improving cancer care and surgical outcomes. The country’s rapid urbanization and growing health consciousness have also driven higher utilization of advanced HPB surgical technologies. Established local manufacturers and a strong export market further bolster China’s position as the regional leader.

India Asia-Pacific Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices Market Insight

The India hepato-pancreatico-biliary (HPB) surgeries surgical devices market is projected to register the fastest CAGR of around 14.2% during the forecast period, fueled by rising public awareness about HPB diseases, rapid advancements in minimally invasive surgical technologies, and expanding healthcare services into semi-urban and rural regions. Increasing healthcare expenditure and improving access to modern surgical devices are key growth drivers. In addition, government initiatives promoting healthcare infrastructure development and accessibility are expected to support the rising adoption of HPB surgical devices across India.

Asia-Pacific Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices Market Share

The Asia-Pacific Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Cook (U.S.)

- Olympus Corporation (Japan)

- B. Braun SE (Germany)

- TeleMed Systems, Inc. (U.S.)

- Boston Scientific Corporation (U.S.)

- CONMED Corporation (U.S.)

- BD (U.S.)

- CooperSurgical Inc. (U.S.)

- KARL STORZ (Germany)

- Medorah Meditek Pvt. Ltd (India)

- STERIS plc (U.S.)

- FUJIFILM Corporation (Japan)

- Johnson & Johnson and its affiliates (U.S.)

Latest Developments in Asia-Pacific Hepato-Pancreatico-Biliary (HPB) Surgeries Surgical Devices market

- In May 2021, Pentax Medical (Japan) formed a joint venture with China-based Vedkang to co-develop and manufacture therapeutic endoscopy devices in China, strengthening Pentax’s interventional GI (including biliary) portfolio for APAC

- In November 2021, Asensus Surgical reported further adoption of its Senhance robotic system in Japan (Shinmatsudo Central General Hospital), expanding APAC access to a platform used for laparoscopic procedures often performed in HPB surgery (e.g., cholecystectomy)

- In September 2022, Olympus launched the VISERA ELITE III surgical imaging platform, a 4K/IR/UV-compatible system rolled out globally including parts of Asia, to streamline minimally invasive surgery workflows relevant to HPB procedures

- In October 2022, Olympus introduced the EU-ME3 endoscopic ultrasound processor in EMEA and parts of Asia/Oceania, enhancing EUS image quality and workflow for pancreaticobiliary diagnostics and interventions

- In February 2023, Olympus agreed to acquire Korea’s Taewoong Medical, a leading maker of GI metal stents (including biliary stents widely used in HPB care), to bolster its GI EndoTherapy business

- In January 2024, Olympus announced it had closed the Taewoong Medical acquisition—expanding its GI stent offering for biliary indications—before later rescinding the deal in March 2024 citing data-integrity concerns (both milestones materially affected APAC biliary stent supply dynamics)

- In 2024, Boston Scientific reported regulatory approvals for its SpyGlass DS II direct-visualization cholangioscopy system in both China (NMPA) and Japan (PMDA), broadening APAC availability of a key HPB device for ductal stone management and strictures

- In April 2024, Asensus Surgical announced Sendai Tokushukai Hospital (Japan) would initiate a Senhance program, reflecting continued APAC expansion of digital/robotic laparoscopy used across general surgery, including hepatobiliary cases

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.