Asia Pacific Hydroxyl Terminated Polybutadiene Htpb Market

Market Size in USD Million

USD

80.57 Million

USD

140.51 Million

2025

2033

USD

80.57 Million

USD

140.51 Million

2025

2033

| 2026 - 2033 | |

| USD 80.57 Million | |

| USD 140.51 Million | |

| % | |

|

Asia-Pacific Hydroxyl-Terminated Polybutadiene (HTPB) Market Size

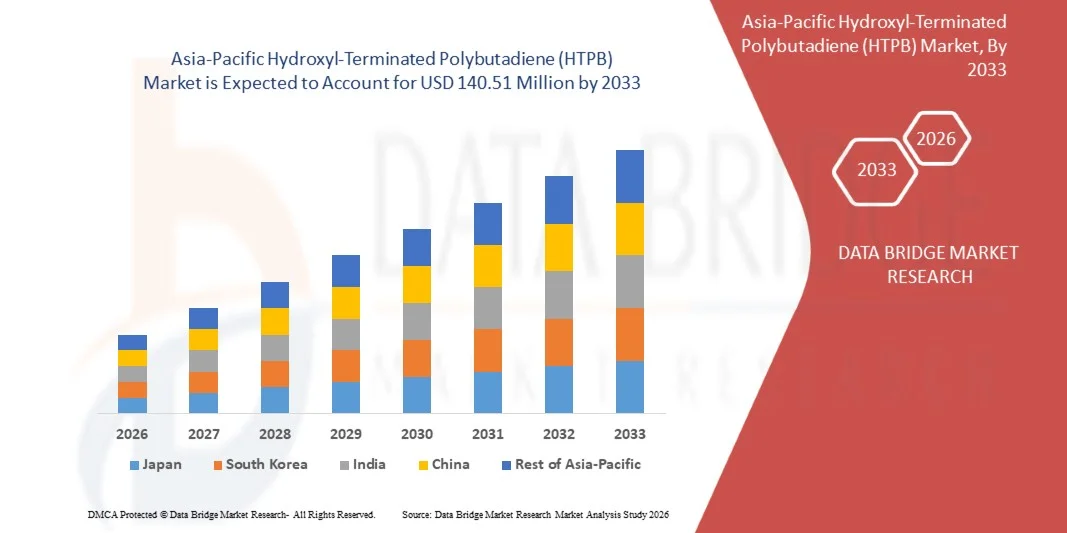

- The Asia-Pacific hydroxyl-terminated polybutadiene (HTPB) market size was valued at USD 80.57 million in 2025 and is expected to reach USD 140.51 million by 2033, at a CAGR of 7.20% during the forecast period

- The market growth is largely fuelled by the rising demand for solid rocket propellants and advanced defense systems across major economies such as China and India

- Increasing utilization of HTPB in adhesives, sealants, coatings, and elastomers for industrial and aerospace applications is further supporting market expansion

Asia-Pacific Hydroxyl-Terminated Polybutadiene (HTPB) Market Analysis

- The Asia-Pacific HTPB market is witnessing strong expansion due to rising defense budgets and increasing focus on indigenous missile and space technology development programs

- Rapid industrialization and expanding applications in automotive, construction, and chemical industries are further strengthening regional demand for high-performance polymer materials

- China dominated the Asia-Pacific hydroxyl-terminated polybutadiene (HTPB) market in 2025, driven by its strong aerospace and defense manufacturing base, expanding space exploration programs, and large-scale missile development initiatives. The country’s significant investments in indigenous propulsion technologies are increasing demand for HTPB as a key binder in solid rocket propellants

- Japan is expected to witness the highest compound annual growth rate (CAGR) in the Asia-Pacific hydroxyl-terminated polybutadiene (HTPB) market due to increasing investments in aerospace innovation, satellite development, and advanced polymer technologies. The country’s strong focus on high-performance materials and precision engineering is driving adoption of HTPB in specialized applications such as rocket propulsion and industrial formulations

- The conventional hydroxyl terminated polybutadienes segment held the largest market revenue share in 2025 driven by its widespread use in solid propellant formulations and established performance reliability in aerospace and defense applications. These materials offer strong mechanical stability, chemical resistance, and compatibility with various curing agents, making them highly preferred in high-energy propulsion systems. Growing demand from missile and space launch programs is further supporting segment dominance. In addition, continuous production advancements are improving formulation efficiency and scalability

Report Scope and Asia-Pacific Hydroxyl-Terminated Polybutadiene (HTPB) Market Segmentation

|

Attributes |

Asia-Pacific Hydroxyl-Terminated Polybutadiene (HTPB) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

• Idemitsu Kosan Co., Ltd. (Japan) |

|

Market Opportunities |

• Expansion In Aerospace And Defense Applications |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia-Pacific Hydroxyl-Terminated Polybutadiene (HTPB) Market Trends

“Rising Demand for Defense-Grade Propellant Materials”

• The increasing focus on strengthening defense capabilities across Asia-Pacific countries is significantly shaping the HTPB market, as it is widely used as a binder in solid rocket propellants. Rising geopolitical tensions and modernization of missile systems are driving demand for high-performance polymer materials. HTPB is gaining traction due to its superior elasticity, chemical resistance, and mechanical stability in extreme conditions. This trend is supporting its widespread adoption in aerospace and defense manufacturing. Governments are also increasing investments in indigenous propulsion technologies

• Expanding space exploration programs and satellite launch initiatives in countries such as China, India, and Japan are further accelerating demand for HTPB-based formulations. The material plays a critical role in enhancing the efficiency and reliability of rocket motors used in space missions. Increasing collaboration between defense organizations and aerospace agencies is strengthening innovation in propulsion systems. Growing private sector participation in space technologies is also boosting consumption. This is creating a strong ecosystem for advanced polymer materials

• Rising industrial applications of HTPB in adhesives, sealants, coatings, and elastomers is further supporting market expansion. Manufacturers are increasingly adopting HTPB due to its flexibility, durability, and resistance to environmental degradation. Growth in automotive and construction industries is further contributing to demand. The shift toward high-performance specialty chemicals is strengthening market penetration across non-defense sectors. Companies are also focusing on improving formulation efficiency and material performance

• For instance, in 2024, leading defense and aerospace organizations in China and India expanded their solid rocket motor production programs by increasing the use of HTPB-based binders in propulsion systems. These developments were aimed at enhancing missile range, stability, and performance reliability. The initiatives also supported domestic manufacturing capabilities and reduced dependency on imported materials. This expansion strengthened regional supply chains for advanced polymer systems. It also reinforced Asia-Pacific’s position in global aerospace material production

• While demand is increasing, sustained market growth depends on raw material availability, cost optimization, and advancements in polymer processing technologies. Manufacturers are focusing on improving production scalability and enhancing performance consistency for aerospace-grade applications. Regulatory compliance and quality certification requirements also influence adoption. Continuous research in high-energy propulsion systems is expected to support long-term market stability

Asia-Pacific Hydroxyl-Terminated Polybutadiene (HTPB) Market Dynamics

Driver

“Growing Demand From Aerospace And Defense Propulsion Systems”

• Rising investments in missile systems, rockets, and space launch vehicles are a major driver for the Asia-Pacific HTPB market. The material is widely used as a binder in solid propellants due to its high energy efficiency and mechanical strength. Governments are prioritizing defense modernization programs to enhance strategic capabilities. Increasing focus on indigenous technology development is further strengthening domestic production of HTPB-based systems. This is significantly supporting long-term market expansion

• Expanding space programs and satellite deployment activities are influencing market growth across the region. HTPB is essential for ensuring stable combustion and structural integrity in propulsion systems. Growing collaboration between aerospace agencies and private space companies is further increasing material demand. Rising frequency of satellite launches for communication, navigation, and defense applications is also contributing to consumption. This trend is strengthening the aerospace material supply chain

• Increasing use of HTPB in industrial applications such as adhesives, sealants, and elastomeric coatings is further driving demand. The material’s flexibility, durability, and resistance to harsh environments make it suitable for high-performance applications. Growth in automotive manufacturing and construction activities is expanding its usage scope. Manufacturers are focusing on improving product formulations to enhance performance efficiency. This diversification is strengthening overall market growth

• For instance, in 2023, major aerospace and defense organizations in India and Japan increased procurement of HTPB-based formulations for use in advanced rocket propulsion systems. These developments were driven by rising demand for improved missile accuracy and enhanced payload capabilities. The initiatives also supported domestic production of strategic defense materials. This contributed to strengthening regional supply chain resilience. It also encouraged further investment in advanced polymer research

• Although growth prospects are strong, wider adoption depends on cost efficiency, raw material availability, and technological advancements in polymer processing. Companies are investing in R&D to improve performance characteristics and reduce production costs. Supply chain stability and regulatory compliance remain key factors influencing market expansion. Continuous innovation in propulsion technology will be critical for sustaining long-term demand

Restraint/Challenge

“High Production Complexity And Raw Material Price Volatility”

• The complex manufacturing process of HTPB and dependence on petrochemical feedstocks remain key challenges for market growth. Fluctuations in raw material prices can significantly impact production costs and profit margins. Limited availability of high-quality input materials also affects supply consistency. This increases operational uncertainty for manufacturers. As a result, pricing stability remains a major concern in the market

• Strict quality and safety standards in aerospace and defense applications further add to production challenges. HTPB used in propulsion systems must meet stringent performance and reliability requirements. Compliance with regulatory frameworks increases development time and cost. Manufacturers must invest heavily in testing and certification processes. This limits entry for smaller players in the market

• Supply chain disruptions and logistical challenges also impact market expansion, particularly for specialized chemical materials. Transportation and storage requirements for HTPB-based compounds add to operational complexity. Dependency on limited suppliers increases vulnerability to shortages. Companies must maintain strong inventory management systems to ensure uninterrupted supply. This adds to overall production costs

• For instance, in 2024, several aerospace material suppliers in South Korea and Malaysia reported increased production costs due to volatility in butadiene feedstock prices, affecting HTPB manufacturing output for defense applications. These challenges also delayed procurement cycles for propulsion system manufacturers. Supply constraints impacted timely delivery of critical aerospace components. This highlighted vulnerabilities in raw material sourcing networks. It also emphasized the need for localized supply chain development

• Overcoming these challenges will require diversification of raw material sources, investment in cost-efficient production technologies, and improved supply chain resilience. Strengthening domestic chemical manufacturing capabilities can reduce dependency on imports. Advanced process optimization and recycling technologies may help stabilize production costs. Collaboration between defense agencies and chemical manufacturers will be essential for long-term market sustainability.

Asia-Pacific Hydroxyl-Terminated Polybutadiene (HTPB) Market Scope

The Asia-Pacific hydroxyl-terminated polybutadiene (HTPB) market is segmented into three notable segments based on product, application, and end use.

• By Product

On the basis of product, the market is segmented into conventional hydroxyl terminated polybutadienes and low molecular weight hydroxyl terminated polybutadienes. The conventional hydroxyl terminated polybutadienes segment held the largest market revenue share in 2025 driven by its widespread use in solid propellant formulations and established performance reliability in aerospace and defense applications. These materials offer strong mechanical stability, chemical resistance, and compatibility with various curing agents, making them highly preferred in high-energy propulsion systems. Growing demand from missile and space launch programs is further supporting segment dominance. In addition, continuous production advancements are improving formulation efficiency and scalability.

The low molecular weight hydroxyl terminated polybutadienes segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for advanced polymer applications requiring improved flexibility and processability. These variants are gaining traction in adhesives, sealants, and coatings due to their enhanced reactivity and performance characteristics. Rising adoption in specialty chemical applications and industrial formulations is further accelerating growth. Manufacturers are focusing on developing customized molecular structures to improve end-use efficiency. This segment is benefiting from expanding industrial diversification of HTPB applications.

• By Application

On the basis of application, the market is segmented into rocket fuel, rubber material, paint, polyurethane, and others. The rocket fuel segment held the largest market revenue share in 2025 driven by strong demand for HTPB as a binder in solid propellant systems used in missiles and space launch vehicles. Its excellent energy efficiency, mechanical strength, and combustion stability make it highly suitable for aerospace propulsion applications. Increasing investments in defense modernization programs and space exploration missions are further strengthening demand. Government-backed aerospace initiatives are also contributing to segment growth. This application remains the core driver of HTPB consumption in the region.

The polyurethane segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising use of HTPB in flexible foams, elastomers, and coatings. Its ability to enhance durability, elasticity, and chemical resistance is supporting increased adoption across industrial applications. Growing demand from automotive, construction, and packaging industries is further fueling expansion. Manufacturers are focusing on improving material performance for high-end polyurethane formulations. Expanding industrial applications beyond defense are significantly broadening market scope.

• By End Use

On the basis of end use, the market is segmented into building & construction, aerospace & defense, automotive, electrical & electronics, construction, packaging, and others. The aerospace & defense segment held the largest market revenue share in 2025 driven by extensive use of HTPB in rocket propellants and missile systems across Asia-Pacific countries. Rising defense budgets and increasing focus on indigenous space programs are significantly boosting demand. The material’s high performance under extreme conditions makes it indispensable for propulsion applications. Strong government support for defense manufacturing is further reinforcing segment dominance. Continuous innovation in missile and satellite technologies is also driving long-term consumption.

The automotive segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing use of HTPB in adhesives, sealants, and elastomeric components. The material’s flexibility, durability, and resistance to environmental stress are supporting its adoption in vehicle manufacturing. Growing demand for lightweight and high-performance materials in electric and conventional vehicles is further accelerating growth. Expanding automotive production across Asia-Pacific economies is strengthening market penetration. Manufacturers are increasingly integrating HTPB-based formulations to enhance vehicle performance and efficiency.

Asia-Pacific Hydroxyl-Terminated Polybutadiene (HTPB) Market Regional Analysis

- China dominated the Asia-Pacific hydroxyl-terminated polybutadiene (HTPB) market in 2025, driven by its strong aerospace and defense manufacturing base, expanding space exploration programs, and large-scale missile development initiatives. The country’s significant investments in indigenous propulsion technologies are increasing demand for HTPB as a key binder in solid rocket propellants

- Rapid industrialization and growth in specialty chemical production are further supporting market expansion

- In addition, China’s well-established chemical manufacturing infrastructure and strong government backing for defense modernization are enhancing production capabilities and supply chain efficiency

- The increasing focus on self-reliance in advanced materials is further strengthening China’s dominant position in the regional market

Japan Hydroxyl-Terminated Polybutadiene (HTPB) Market Insight

The Japan hydroxyl-terminated polybutadiene (HTPB) market is expected to witness steady growth from 2026 to 2033, driven by increasing investments in aerospace research, satellite development programs, and advanced material technologies. Japan’s strong emphasis on precision engineering and high-performance chemical materials is supporting adoption of HTPB in specialized applications such as rocket propulsion systems and industrial polymers. Growing collaboration between government space agencies and private aerospace companies is further accelerating demand. In addition, rising use of HTPB in automotive, electronics, and adhesive applications is broadening its industrial scope. The country’s focus on innovation, sustainability, and advanced manufacturing is expected to continue supporting market development over the forecast period.

Asia-Pacific Hydroxyl-Terminated Polybutadiene (HTPB) Market Share

The Asia-Pacific hydroxyl-terminated polybutadiene (HTPB) industry is primarily led by well-established companies, including:

• Idemitsu Kosan Co., Ltd. (Japan)

• Nippon Soda Co., Ltd. (Japan)

• Mitsubishi Chemical Corporation (Japan)

• Asahi Kasei Corporation (Japan)

• Showa Denko K.K. (Japan)

• JXTG Nippon Oil & Energy Corporation (Japan)

• Sumitomo Chemical Co., Ltd. (Japan)

• Toray Industries, Inc. (Japan)

• LG Chem Ltd. (South Korea)

• Hanwha Solutions Corporation (South Korea)

• Lotte Chemical Corporation (South Korea)

• Reliance Industries Limited (India)

• Bharat Petroleum Corporation Limited (India)

• Hindustan Petroleum Corporation Limited (India)

• China National Petroleum Corporation (CNPC) (China)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Asia Pacific Hydroxyl Terminated Polybutadiene Htpb Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Asia Pacific Hydroxyl Terminated Polybutadiene Htpb Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Asia Pacific Hydroxyl Terminated Polybutadiene Htpb Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.