Asia Pacific Inflation Device Market

Market Size in USD Million

USD

197.19 Million

USD

316.68 Million

2025

2033

USD

197.19 Million

USD

316.68 Million

2025

2033

| 2026 - 2033 | |

| USD 197.19 Million | |

| USD 316.68 Million | |

| % | |

|

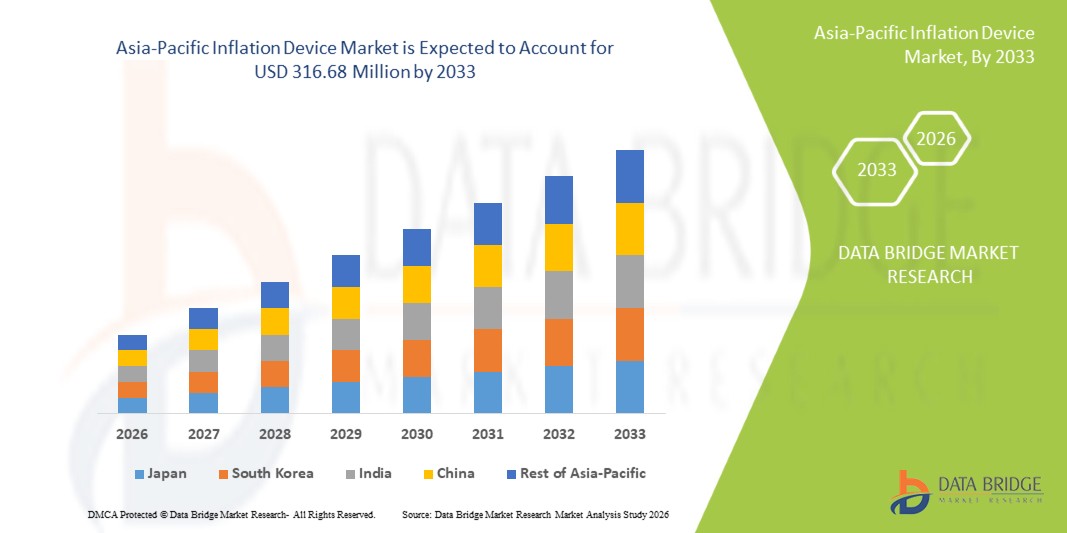

Asia-Pacific Inflation Device Market Size

- The Asia-Pacific inflation device market size was valued at USD 197.19 million in 2025 and is expected to reach USD 316.68 million by 2033, at a CAGR of 6.10% during the forecast period

- The market expansion is primarily driven by the growing number of cardiovascular, gastrointestinal, and vascular interventional procedures across major countries such as China, India, Japan, and South Korea, resulting in rising demand for precise and reliable inflation systems

- In addition, rapid improvements in healthcare infrastructure, increasing adoption of minimally invasive surgeries, and higher investments in advanced interventional cardiology tools are accelerating market penetration

Asia-Pacific Inflation Device Market Analysis

- Inflation devices critical for controlled balloon inflation during interventional cardiology, radiology, vascular, and gastrointestinal procedures are increasingly integral to the region’s rapidly expanding minimally invasive treatment landscape due to their precision, safety features, and compatibility with various catheters and stent systems

- The growing demand in Asia-Pacific is primarily driven by the rising burden of cardiovascular and vascular diseases, rapid adoption of minimally invasive surgeries, and continuous improvements in healthcare infrastructure across major markets such as China, India, Japan, and South Korea

- China dominated the Asia-Pacific inflation device market with a revenue share of 38.5% in 2025, supported by high procedure volumes, strong investment in advanced cath labs, and wider availability of inflation systems through both domestic and global manufacturers, while Japan maintains significant demand due to its mature interventional healthcare ecosystem

- India is expected to be the fastest-growing region during the forecast period, driven by increasing angioplasty procedures, expanding tertiary care networks, and the rising penetration of digital surgical tools within cardiology and radiology domains

- The analog inflation devices segment dominated the Asia-Pacific market with a market share of 52.9% in 2025, driven by their cost-effectiveness, reliability, and widespread adoption across hospitals and interventional laboratories, making them the preferred choice for high-volume cardiovascular and radiology procedures

Report Scope and Asia-Pacific Inflation Device Market Segmentation

|

Attributes |

Asia-Pacific Inflation Device Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Inflation Device Market Trends

“Enhanced Precision Through Digital Integration and Smart Monitoring”

- A significant and accelerating trend in the Asia-Pacific inflation device market is the deepening integration of digital pressure gauges and intelligent monitoring systems that enhance procedural accuracy and clinician control during interventional applications

- For instance, advanced digital inflation devices launched by companies such as Medtronic and Boston Scientific feature high-resolution displays, accurate real-time pressure feedback, and improved ergonomics, allowing clinicians to perform balloon inflation with greater consistency and confidence

- Digital integration in inflation devices enables capabilities such as automated pressure stabilization, optimized deflation cycles, and intelligent alerts for abnormal resistance. For instance, several new systems utilize smart sensors to refine pressure detection accuracy and support clinicians by identifying irregularities during stent deployment or angioplasty

- The seamless integration of inflation devices with cath lab imaging systems and broader interventional platforms facilitates centralized management of procedure data. Through a unified interface, clinicians can monitor inflation metrics alongside imaging and patient vitals, enabling a more synchronized procedural environment

- This trend toward more advanced, intuitive, and interconnected inflation systems is reshaping expectations for procedural precision across hospitals and cath labs. Consequently, companies such as Terumo are developing digital inflation solutions with automated pressure controls, enhanced visibility, and improved workflow compatibility

- The demand for inflation devices that offer seamless digital integration and enhanced precision is growing rapidly across both high-volume hospitals and interventional laboratories, as healthcare providers prioritize efficiency, safety, and improved patient outcomes

Asia-Pacific Inflation Device Market Dynamics

Driver

“Growing Need Due to Rising Interventional Procedure Volumes and Minimally Invasive Adoption”

- The increasing prevalence of cardiovascular, peripheral vascular, and gastrointestinal conditions across Asia-Pacific nations, combined with the accelerating adoption of minimally invasive procedures, is a significant driver fueling the demand for inflation devices

- For instance, in March 2025, several major tertiary hospitals in China and India expanded their interventional cardiology and radiology units, adopting new-generation inflation devices to support the rising volume of angioplasty and stent deployment procedures, thus driving market growth during the forecast period

- As clinicians seek greater precision and enhanced procedural safety, inflation devices provide controlled pressure delivery, accurate monitoring, and improved reliability compared to conventional tools, making them an essential component of modern interventional workflows

- Furthermore, the growing use of balloon catheters, stent systems, and minimally invasive therapeutic tools is strengthening the need for reliable inflation devices that ensure optimal balloon expansion and reduced procedural complications

- The convenience of digital pressure visibility, improved ergonomics for clinicians, and compatibility with a wide range of interventional catheters are key factors propelling the adoption of inflation devices across hospitals and interventional laboratories in the region

- The trend toward upgrading cath lab infrastructure, increasing availability of advanced equipment, and the rising focus on precision-based interventions further contribute to the sustained growth of the Asia-Pacific inflation device market

Restraint/Challenge

“Device Reliability Concerns and Regulatory Compliance Hurdle”

- Concerns surrounding device reliability, pressure accuracy limitations in low-cost models, and potential risks associated with equipment malfunction pose a significant challenge to broader market penetration of inflation devices in the Asia-Pacific region

- For instance, reports of inconsistent pressure readings or leakage in outdated or low-quality inflation devices have made some healthcare institutions hesitant to adopt advanced systems, particularly in resource-limited settings

- Addressing these concerns through stringent manufacturing quality standards, improved pressure calibration technologies, and continuous product upgrades is crucial for building trust among clinicians. Companies such as Terumo and Cook Medical emphasize enhanced durability and pressure accuracy in their device portfolios to strengthen adoption

- In addition, the higher cost of advanced digital inflation devices compared to basic analog models can be a barrier for budget-sensitive hospitals and clinics across emerging Asia-Pacific markets

- While prices are gradually becoming more competitive, the perceived cost burden for technologically advanced inflation systems may continue to hinder adoption, especially for facilities that prioritize basic functionality over digital capabilities

- The availability of refurbished and reusable inflation devices also contributes to reduced reliance on premium, single-use options. The growing preference for these affordable alternatives directly impacts the demand for conventional inflation devices, creating pricing pressures and limiting growth opportunities for established market players

- Overcoming these challenges through improved device reliability, comprehensive clinician training, and broader availability of cost-effective digital models will be essential for ensuring sustained market expansion in the Asia-Pacific region

Asia-Pacific Inflation Device Market Scope

The market is segmented on the basis of type, capacity, application, pressure, function, end user, and distribution channel.

- By Type

On the basis of type, the Asia-Pacific inflation device market is segmented into analog inflation devices and digital inflation devices. The analog inflation device segment dominated the market with the largest market revenue share of 52.9% in 2025, driven by its affordability, simplicity, and widespread adoption in hospitals and interventional laboratories. Analog devices are preferred for standard balloon inflation procedures due to their reliable performance without electronic components. Clinicians favor analog devices in high-volume cardiac and peripheral vascular interventions, especially in cost-sensitive regions. Their mechanical design ensures dependable operation, minimal maintenance, and rapid readiness for repeated procedures. Compatibility with various catheters and balloons supports their dominance. Long-standing familiarity among clinicians further reinforces this segment’s market leadership.

The digital inflation device segment is anticipated to witness the fastest growth rate of 19.8% from 2026 to 2033, fueled by rising demand for precise pressure control, real-time monitoring, and integration with advanced interventional workflows. Digital systems provide automated pressure stabilization, intelligent alerts, and high-resolution displays that improve procedural safety and efficiency. For instance, devices with integrated sensors optimize balloon inflation and identify abnormal resistance during stent deployment. Adoption is accelerating in digitally modernizing cath labs across China, India, and Southeast Asia. Advanced digital devices reduce manual error and enhance confidence during minimally invasive procedures. Integration with imaging platforms supports workflow efficiency and rapid expansion.

- By Capacity

On the basis of capacity, the market is segmented into 20 ml, 25 ml, 30 ml, and 60 ml inflation devices. The 20 ml inflation device segment dominated the market with the largest share in 2025, driven by its suitability for coronary angioplasty and routine stent deployment. These devices are compact, easy to handle, and allow rapid inflation and deflation in high-volume procedures. Their affordability makes them widely accessible across hospitals in emerging Asia-Pacific countries. Clinicians favor 20 ml devices due to reliability, minimal training requirements, and broad compatibility with standard catheters. Multiple manufacturers produce 20 ml inflators, ensuring consistent supply. Their widespread clinical adoption reinforces dominance in this segment.

The 60 ml inflation device segment is expected to witness the fastest growth rate of 18.7% from 2026 to 2033, supported by rising demand in peripheral vascular and gastroenterological interventions that require higher inflation volumes. These devices enable high-pressure, high-volume balloon inflations for complex procedures. Hospitals and specialized centers increasingly prefer 60 ml devices for their versatility. Technological advancements in catheters and balloons are boosting adoption. Expansion of interventional facilities in India, China, and Japan further drives segment growth. Clinician preference for large-capacity systems ensures rapid uptake.

- By Application

On the basis of application, the market is segmented into interventional cardiology, peripheral vascular procedures, interventional radiology, urological procedures, gastroenterological procedures, and others. The interventional cardiology segment dominated the market in 2025, driven by the high volume of angioplasty, stent placement, and balloon dilation procedures. Rising prevalence of coronary artery disease in China and India significantly increases demand. Inflation devices are essential for accurate balloon inflation during stent deployment, ensuring procedural success. Government programs to improve cardiac care infrastructure have expanded access to interventional services. Technological improvements in stents and catheters further drive consumption. Strong presence of cardiology-focused hospitals reinforces dominance. Clinicians’ preference for proven, reliable devices contributes to stable market share.

The interventional radiology segment is expected to witness the fastest CAGR of 20.2% from 2026 to 2033, supported by rising adoption of image-guided minimally invasive procedures. Balloon catheters are increasingly used for vessel dilation, fluid delivery, and therapeutic interventions requiring precise pressure. Inflation devices provide accuracy essential for radiology procedures. Expansion of radiology infrastructure across Asia-Pacific supports adoption. Clinicians’ preference for minimally invasive techniques drives growth. Investment in specialized interventional radiology units further accelerates demand. The rising awareness of safety and precision benefits contributes to rapid market expansion.

- By Pressure

On the basis of pressure, the market is segmented into 30 atm, 40 atm, 55 atm, and others. The 30 atm segment dominated the market in 2025, driven by widespread use in standard coronary and peripheral procedures. These devices meet most procedural requirements and are cost-effective, ensuring broad adoption across hospitals. Clinicians favor 30 atm devices for reliability and familiarity. Multiple manufacturers provide steady supply, supporting dominance. Compatibility with standard balloon catheters reinforces market leadership. Lower cost relative to high-pressure variants ensures continued preference in emerging markets.

The 55 atm segment is anticipated to witness the fastest growth rate of 21.5% from 2026 to 2033, driven by demand for high-pressure balloons in complex coronary and peripheral interventions. High-pressure devices are critical for calcified lesions, peripheral arterial disease, and resistant stenosis. Hospitals performing specialized interventions invest in these systems for safety and accuracy. Technological advances in high-pressure catheters boost adoption. Expansion of specialty vascular centers supports rapid segment growth. Clinicians’ preference for precision tools reinforces rising market share.

- By Function

On the basis of function, the market is segmented into stent deployment and fluid delivery. The stent deployment segment dominated the market in 2025 due to the high volume of coronary and peripheral stent procedures. Inflation devices are essential for controlled balloon expansion and accurate stent placement. Rising cardiovascular disease incidence drives demand. Technological improvements in stents increase procedural volumes. Clinicians rely on inflation devices for procedural success. Broad applicability in interventional procedures reinforces dominance. Hospitals and labs continue to prefer stent deployment devices for routine interventions.

The fluid delivery segment is expected to witness the fastest CAGR of 19.9% from 2026 to 2033, supported by increasing use in image-guided interventions requiring precise contrast or therapeutic fluid administration. Inflation devices with accurate measurement improve procedural safety. Adoption is rising in minimally invasive radiology, gastroenterology, and urology procedures. Multifunctional devices supporting both pressure inflation and fluid management accelerate growth. Expansion of interventional procedures drives market demand. Clinician preference for precise, versatile devices further contributes to rapid adoption.

- By End User

On the basis of end user, the market is segmented into hospitals, interventional laboratories, and clinics. The hospitals segment dominated the market in 2025, driven by high volumes of cardiac, vascular, and radiology interventions. Hospitals have advanced cath labs and trained staff, increasing reliance on inflation devices. Rising hospitalizations for cardiovascular diseases fuel demand. Large-scale procurement ensures steady supply. Government investments in tertiary care facilities reinforce dominance. Skilled cardiologists and interventional radiologists strengthen the segment’s leadership. Hospitals remain the primary buyer for both analog and digital devices.

The interventional laboratories segment is anticipated to witness the fastest growth rate of 20.5% from 2026 to 2033, due to rising establishment of specialized cath labs and minimally invasive centers. These labs focus on precision interventions requiring reliable inflation devices. Growth in ambulatory interventional procedures drives adoption. Advanced equipment in new labs supports rapid market penetration. Private hospital partnerships with device manufacturers accelerate expansion. Rising awareness of procedural safety benefits fuels adoption in interventional laboratories.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, retail sales, and third-party distributors. The direct tender segment dominated the market in 2025, due to high-volume procurement by hospitals and public healthcare institutions across Asia-Pacific. Tender-based purchases ensure cost-effectiveness, consistent supply, and bulk procurement advantages. Government and large private hospitals prefer tenders to reduce procurement costs. Multiple domestic manufacturers support tender sales. The reliability and scalability of this channel reinforce dominance. Tender procurement is widely used for analog and standard digital devices.

The third-party distributors segment is expected to witness the fastest CAGR of 21.0% from 2026 to 2033, driven by growing penetration of international brands and flexible distribution across diverse markets. Distributors enable access to smaller hospitals, clinics, and specialized interventional centers. Rising adoption of digital inflation devices increases reliance on distributor support. Expansion of private clinics and interventional labs fuels demand. Manufacturers are strengthening regional partnerships to enhance market reach. Rapid healthcare infrastructure growth further accelerates segment adoption.

Asia-Pacific Inflation Device Market Regional Analysis

- China dominated the Asia-Pacific inflation device market with a revenue share of 38.5% in 2025, supported by high procedure volumes, strong investment in advanced cath labs, and wider availability of inflation systems through both domestic and global manufacturers, while Japan maintains significant demand due to its mature interventional healthcare ecosystem

- Healthcare providers in China highly value the precision, reliability, and versatility of inflation devices, which are critical for interventional cardiology, peripheral vascular procedures, and image-guided radiology interventions across hospitals and specialized labs

- This widespread adoption is further supported by increasing healthcare expenditure, modernization of hospitals and interventional laboratories, and growing preference for advanced devices that improve procedural safety and efficiency, establishing inflation devices as essential tools in both routine and complex interventions throughout the country

The China Inflation Device Market Insight

The China inflation device market captured the largest revenue share of 38.5% in 2025 within Asia-Pacific, fueled by the rapid expansion of interventional cardiology and peripheral vascular procedures. Hospitals and specialized interventional laboratories are increasingly prioritizing advanced inflation devices for precise stent deployment and fluid delivery. The growing adoption of minimally invasive treatments, alongside government initiatives to modernize healthcare infrastructure, is further driving market growth. Moreover, rising awareness of procedural safety, integration with imaging systems, and the availability of both analog and digital devices are significantly contributing to market expansion.

Japan Inflation Device Market Insight

The Japan inflation device market is gaining momentum due to the country’s high-tech healthcare ecosystem, emphasis on procedural safety, and demand for precision in interventional procedures. Advanced hospitals and cardiac centers are increasingly adopting digital inflation devices to improve workflow efficiency and accuracy. Integration with imaging and diagnostic systems, along with the aging population requiring minimally invasive treatments, is fueling market growth. Moreover, Japan’s well-developed healthcare infrastructure and strong focus on innovation are enabling the adoption of sophisticated inflation systems in both public and private hospitals.

India Inflation Device Market Insight

The India inflation device market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by the country’s rapidly growing middle class, urbanization, and increasing prevalence of cardiovascular and peripheral vascular diseases. Hospitals and interventional labs are rapidly adopting both analog and digital inflation devices for coronary, peripheral, and radiology procedures. Government initiatives promoting smart hospitals and investment in healthcare infrastructure, along with the availability of cost-effective devices, are key factors propelling market growth. Expansion of specialized interventional centers further enhances device adoption across the country.

South Korea Inflation Device Market Insight

The South Korea inflation device market is witnessing steady growth due to the country’s advanced healthcare infrastructure, high adoption of minimally invasive procedures, and emphasis on precision in interventional treatments. Hospitals and specialized cardiac centers are increasingly integrating digital inflation devices to ensure accurate stent deployment and fluid management. Government support for advanced medical technologies, combined with rising healthcare expenditure and modernization of interventional laboratories, is driving market expansion. In addition, collaboration with international manufacturers and a growing preference for devices with real-time monitoring capabilities are contributing to increased adoption in both public and private hospitals.

Asia-Pacific Inflation Device Market Share

The Asia-Pacific Inflation Device industry is primarily led by well-established companies, including:

- Boston Scientific Corporation (U.S.)

- Merit Medical Systems, Inc. (U.S.)

- Teleflex Incorporated (U.S.)

- CONMED Corporation (U.S.)

- Olympus Corporation (Japan)

- B. Braun SE (U.S.)

- Medtronic (Ireland)

- BD (U.S.)

- Johnson and Johnson Services, Inc. (U.S.)

- Cook (U.S.)

- Vygon SAS (France)

- Atrion Medical (U.S.)

- Spectrum Medtech Pvt. Ltd (India)

- Medorah Meditek Pvt. Ltd. (India)

- SMT (India)

- SURETECH MEDICAL INC. (India)

- Elite Medtek (Jiangsu) Co., Ltd (China)

- Advin Health Care (India)

- US Endovascular, LLC (U.S.)

- Terumo Corporation (Japan)

What are the Recent Developments in Asia-Pacific Inflation Device Market?

- In January 2025, Olympus Latin America acquired Sur Medical SpA’s distribution business in Chile, establishing Olympus Corporation Chile. This acquisition enables direct access to Chile’s growing healthcare market, streamlining the distribution of Olympus products and enhancing customer service and support in the region

- In November 2024, Merit Medical Systems has completed the acquisition of Cook Medical’s lead management portfolio for approximately USD 210 million. This acquisition enhances Merit’s electrophysiology and cardiac rhythm management business by adding a comprehensive range of devices used in lead removal and replacement procedures for pacemakers and implantable cardioverter-defibrillators. The integration of these products strengthens Merit’s position in the inflation device market

- In April 2024, Integra LifeSciences Corporation has completed the acquisition of Acclarent, Inc., a company specializing in ENT (ear, nose, and throat) solutions. This acquisition enhances Integra's portfolio in the ENT market, expanding its capabilities in innovative medical technologies for sinus, ear, and nasal treatments, driving further growth in the healthcare sector

- In May 2024, Merit Medical Systems announced the U.S. commercial release of the basixSKY Inflation Device. This analog device is designed for endovascular interventions such as balloon angioplasty and stent placement. It features a comfort-grip handle for one-handed preparation and minimizes rotational torque and handle revolutions to reach pressure. The device is available as a standalone solution and in kits with Merit Angioplasty Packs, configured to offer complementing AccessPLUS, Honor, and PhD hemostasis valves

- In January 2022, Medtronic has acquired Affera, a cardiac technology company specializing in mapping, navigation, and ablation systems for treating arrhythmias such as atrial fibrillation. The acquisition marks Medtronic's entry into the cardiac mapping segment, expanding its cardiac ablation portfolio

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.