Asia Pacific Laryngoscopes Market

Market Size in USD Million

USD

242.10 Million

USD

578.35 Million

2024

2032

USD

242.10 Million

USD

578.35 Million

2024

2032

| 2025 - 2032 | |

| USD 242.10 Million | |

| USD 578.35 Million | |

| % | |

|

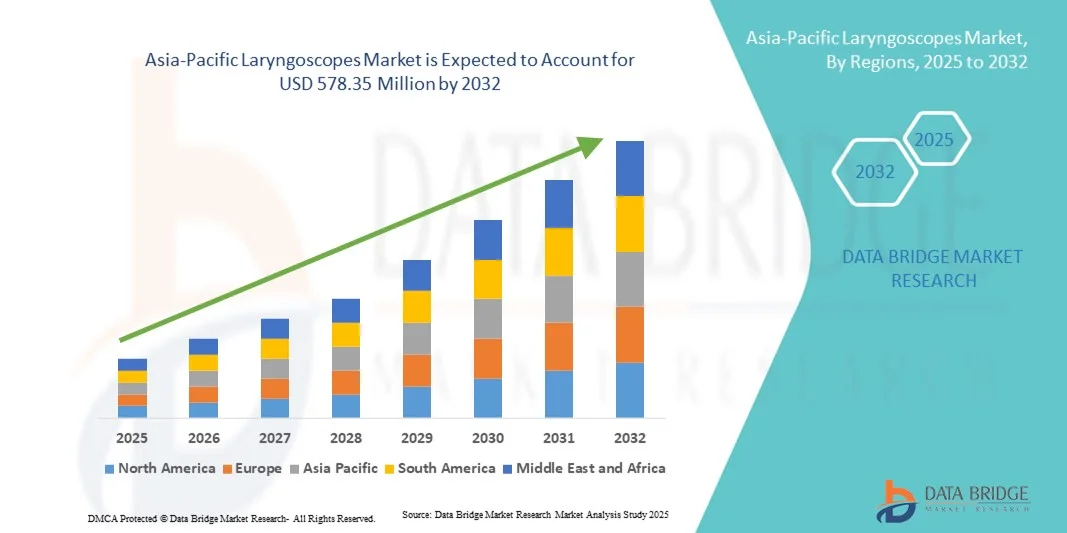

Asia-Pacific Laryngoscopes Market Size

- The Asia-Pacific laryngoscopes market size was valued at USD 242.10 million in 2024 and is expected to reach USD 578.35 million by 2032, at a CAGR of 11.5% during the forecast period

- The market growth is largely fueled by the increasing prevalence of respiratory diseases, advancements in medical technologies, and rising demand for emergency medical services, leading to greater adoption of both rigid and video laryngoscopes in hospitals and clinics

- Furthermore, growing awareness among healthcare professionals about the advantages of video laryngoscopes, along with expanding healthcare infrastructure in countries such as Australia, is establishing laryngoscopes as essential devices in modern airway management. These converging factors are accelerating market adoption, thereby significantly boosting the industry's growth

Asia-Pacific Laryngoscopes Market Analysis

- Laryngoscopes, including rigid, flexible, and video-assisted devices, are increasingly vital components of modern airway management and surgical procedures in both hospitals and ambulatory surgical centers due to their enhanced visibility, precision, and ease of intubation

- The escalating demand for laryngoscopes is primarily fueled by the rising prevalence of respiratory diseases, growing number of surgical procedures, and increasing awareness among healthcare professionals about the advantages of video laryngoscopes

- China dominated the Asia-Pacific laryngoscopes market with the largest revenue share of 38.4% in 2024, characterized by expanding healthcare infrastructure, high patient volumes, and a strong presence of key medical device manufacturers, with hospitals and surgical centers experiencing substantial growth in laryngoscope usage driven by innovations from both established and emerging regional players

- India is expected to be the fastest-growing country in the Asia-Pacific laryngoscopes market during the forecast period due to increasing healthcare investments, rising awareness of advanced airway management techniques, and expanding surgical facilities

- Rigid laryngoscopes segment dominated the Asia-Pacific market with a market share of 55.9% in 2024, driven by their established reputation, wide clinical adoption, and ease of integration into existing surgical protocols

Report Scope and Asia-Pacific Laryngoscopes Market Segmentation

|

Attributes |

Asia-Pacific Laryngoscopes Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Laryngoscopes Market Trends

Growing Adoption of Video and Flexible Laryngoscopes

- A significant and accelerating trend in the Asia-Pacific laryngoscopes market is the increasing adoption of video and flexible laryngoscopes, which provide enhanced visibility and precision during intubation and surgical procedures

- For instance, the McGRATH MAC video laryngoscope is widely used in hospitals across China and India, allowing clinicians to achieve safer and faster intubation compared with traditional rigid devices

- Integration of advanced imaging technologies and ergonomic designs in laryngoscopes enables features such as improved airway visualization, reduced procedural errors, and ease of training for medical staff. For instance, some King Vision devices utilize digital displays and detachable blades to improve patient safety and procedural efficiency

- The seamless integration of video laryngoscopes with surgical workflows and emergency response protocols facilitates better outcomes in critical care and operation theaters. Through a single device, clinicians can manage intubation, airway monitoring, and documentation simultaneously

- This trend towards technologically advanced, intuitive, and safer airway management systems is fundamentally reshaping clinical expectations. Consequently, companies such as Teleflex and Ambu are developing video laryngoscopes with portable displays, detachable blades, and advanced lighting for improved clinical performance

- The demand for laryngoscopes with enhanced visualization and ergonomic designs is growing rapidly across hospitals and ambulatory surgical centers, as clinicians increasingly prioritize patient safety and procedural efficiency

Asia-Pacific Laryngoscopes Market Dynamics

Driver

Increasing Demand Due to Rising Surgical Procedures and Respiratory Diseases

- The rising prevalence of respiratory diseases, growing number of surgical procedures, and expanding emergency care facilities are significant drivers for the heightened demand for laryngoscopes

- For instance, in 2024, AIIMS India reported increased usage of video laryngoscopes in critical care units to manage difficult airways, driving market adoption across the country

- As clinicians become more aware of the advantages of video and flexible laryngoscopes, hospitals are upgrading from traditional rigid devices to advanced systems offering better visualization and safety features

- Furthermore, the growing focus on minimally invasive procedures and outpatient surgeries is making laryngoscopes an essential component in surgical and emergency care settings, offering precise and reliable performance

- Rising investments in healthcare infrastructure, training of medical professionals, and government initiatives to improve patient safety are key factors propelling the adoption of laryngoscopes in both developed and emerging Asia-Pacific countries

Restraint/Challenge

High Device Costs and Training Requirements

- The relatively high cost of advanced video and flexible laryngoscopes, compared with traditional rigid devices, poses a challenge to broader market adoption in price-sensitive regions

- For instance, smaller clinics in Southeast Asia may hesitate to purchase high-end video laryngoscopes despite their advantages due to budget constraints

- Adequate training and skilled personnel are required to operate advanced laryngoscopes effectively, creating an additional barrier for adoption in hospitals with limited resources

- Furthermore, maintenance, sterilization, and replacement of disposable blades add to the operational costs, which can deter adoption among smaller healthcare facilities

- Overcoming these challenges through cost-effective device options, regional training programs, and clinician education on procedural efficiency and safety will be vital for sustained market growth across Asia-Pacific

- Limited awareness of advanced laryngoscope benefits among rural healthcare providers may slow adoption in less urbanized regions

- Regulatory hurdles and the need for device approvals across multiple Asia-Pacific countries can delay market entry for new laryngoscope models

Asia-Pacific Laryngoscopes Market Scope

The market is segmented on the basis of type, category, visualization system, accessories, application, and end user.

- By Type

On the basis of type, the Asia-Pacific laryngoscopes market is segmented into rigid and flexible laryngoscopes. The rigid laryngoscope segment dominated the market with the largest revenue share of 55.9% in 2024, driven by its widespread clinical adoption, reliability in standard surgical procedures, and cost-effectiveness for hospitals. Rigid laryngoscopes are preferred for routine intubation, emergency airway management, and training purposes due to their durability and ease of use. Hospitals and surgical centers in China, Japan, and Australia largely rely on rigid systems, benefiting from their compatibility with multiple blade types. The segment also sees recurring demand for replacement blades and handles, supporting sustained revenue. Furthermore, rigid laryngoscopes require minimal maintenance and sterilization, making them practical for high-volume medical facilities.

The flexible laryngoscope segment is anticipated to witness the fastest growth during the forecast period, driven by its ability to navigate difficult or complex airways, and rising adoption in ICU, emergency, and minimally invasive surgical procedures. Flexible devices reduce patient discomfort and procedural risk, making them increasingly preferred by anesthesiologists and ENT specialists. Rising awareness of fiber-optic and video-assisted techniques, coupled with hospital modernization programs in India, Southeast Asia, and China, supports rapid growth. Manufacturers are introducing portable, reusable, and disposable flexible laryngoscopes to cater to diverse clinical needs. Technological enhancements such as high-definition imaging and ergonomic design further contribute to adoption.

- By Category

On the basis of category, the market is segmented into direct and indirect laryngoscopes. The direct laryngoscope segment dominated the market in 2024 due to its simplicity, cost-effectiveness, and minimal training requirements for clinicians. Hospitals and surgical centers widely prefer direct devices for routine intubation, emergency procedures, and surgical applications. Direct laryngoscopes are compatible with both rigid and flexible blade types, increasing versatility. They are also easy to maintain and sterilize, reducing operational burdens for high-volume hospitals. China, Japan, and Australia account for the largest procurement volumes of direct laryngoscopes due to mature healthcare infrastructure. The segment also benefits from recurring sales of blades and handles.

Indirect laryngoscopes are expected to register the fastest growth during the forecast period, driven by the increasing adoption of video-assisted and fiber-optic systems for complex airway management. Indirect devices allow visualization without aligning the oral, pharyngeal, and tracheal axes, reducing procedural difficulty and patient risk. Expanding ICU and emergency care facilities in India and Southeast Asia are boosting adoption. Technological innovations such as portable displays, high-definition imaging, and detachable blades further enhance the clinical appeal. Awareness campaigns and training programs are also contributing to faster adoption.

- By Visualization System

On the basis of visualization system, the market is segmented into standard, video, and fiber-optic laryngoscopes. Standard laryngoscopes dominated the market with the largest revenue share in 2024 due to wide clinical adoption, ease of use, and affordability. They are widely used in routine surgical, diagnostic, and emergency procedures. Hospitals and specialty clinics in China, Japan, and Australia maintain large inventories of standard laryngoscopes for varied clinical requirements. Standard devices also support multiple blade types and handle designs, enhancing versatility. Recurring demand for replacement blades supports continuous revenue growth. Minimal maintenance and easy sterilization requirements make them ideal for high-volume healthcare facilities.

Video laryngoscopes are expected to witness the fastest growth during the forecast period, fueled by increasing adoption in ICUs, emergency care, and complex surgeries. Video devices improve visualization, reduce intubation failure rates, and support clinician training with real-time displays. India, Southeast Asia, and Australia are emerging as high-growth markets due to hospital modernization initiatives. Technological innovations, including wireless displays and ergonomic designs, further boost adoption. Video laryngoscopes are increasingly used in teaching hospitals to train junior clinicians efficiently. Growing awareness of difficult airway protocols supports accelerated market uptake.

- By Accessories

On the basis of accessories, the market is segmented into handles, blades, fiber bundles, shell and caps, sets and kits, cytology brushes, bulbs, battery holders, bags, and others. Blades dominated the market in 2024 with the largest share due to their essential role in both rigid and flexible laryngoscopes and frequent replacement cycles. Hospitals and surgical centers purchase multiple blade sizes for different patient groups, generating recurring revenue. Blades are widely used in China, Japan, and Australia, where rigid laryngoscopes remain dominant. The segment benefits from disposable and reusable blade options to reduce cross-contamination risk. Standardization of blade sizes and handle compatibility further supports broad adoption. Recurring replacement cycles ensure steady revenue streams for manufacturers.

Handles are expected to witness the fastest growth during the forecast period, due to increasing adoption of portable, ergonomic, and battery-powered laryngoscopes. Modern handles with integrated power sources, detachable blade compatibility, and improved ergonomics are gaining traction in hospitals and surgical centers. India and Southeast Asia show high growth potential as facilities upgrade to advanced devices. Handles also support flexible and video-assisted laryngoscopes, enhancing adoption. Innovations such as lightweight materials and better grip designs contribute to faster uptake. Hospitals value ergonomic handles for reducing clinician fatigue during prolonged procedures.

- By Application

On the basis of application, the market is segmented into surgical and diagnostic. Surgical applications dominated the market in 2024, as laryngoscopes are essential for endotracheal intubation, airway management, ENT surgeries, and minimally invasive procedures. High surgical volumes in hospitals across China, India, and Australia drive strong demand. Surgical usage involves recurring procurement of blades, handles, and maintenance services, boosting revenue. Hospitals also prefer both rigid and video-assisted devices for surgical applications. Increasing awareness of patient safety protocols supports sustained adoption. Well-equipped hospitals and surgical centers continue to invest in advanced laryngoscopes.

Diagnostic applications are expected to witness the fastest growth during the forecast period, driven by adoption of flexible and video laryngoscopes for airway assessments, bronchoscopy guidance, and minimally invasive procedures. Increasing ICU and emergency care facilities in India and Southeast Asia are fueling adoption. Diagnostic use requires precise imaging, which promotes video and fiber-optic devices. Growing awareness of early airway disorder detection supports the segment’s growth. Portable and disposable devices are increasingly preferred for outpatient and ambulatory diagnostic use. Technological improvements such as high-definition imaging accelerate market uptake.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, ambulatory centers, surgical centers, and others. Hospitals dominated the market in 2024 with the largest revenue share due to high procedural volumes, substantial budgets for advanced medical devices, and extensive surgical and emergency infrastructure. Leading countries such as China, Japan, and Australia account for a major portion of hospital procurement. Hospitals prefer rigid and standard laryngoscopes for cost-effective bulk purchases. Recurring purchases of blades and handles further reinforce revenue dominance. Large hospitals also invest in video and flexible laryngoscopes for complex procedures.

Specialty clinics are expected to witness the fastest growth during the forecast period, driven by the increasing number of ENT, anesthesiology, and respiratory care centers in India, Southeast Asia, and Australia. These clinics prioritize flexible and video laryngoscopes for advanced procedures with high precision. Growth is further supported by modernization of outpatient surgical facilities. Rising awareness of difficult airway management among specialists fuels adoption. Specialty clinics often adopt portable, ergonomic devices suitable for smaller setups. Government initiatives to improve clinical standards also contribute to segment growth.

Asia-Pacific Laryngoscopes Market Regional Analysis

- China dominated the Asia-Pacific laryngoscopes market with the largest revenue share of 38.4% in 2024, characterized by expanding healthcare infrastructure, high patient volumes, and a strong presence of key medical device manufacturers, with hospitals and surgical centers experiencing substantial growth in laryngoscope usage driven by innovations from both established and emerging regional players

- Hospitals and surgical centers in the region prioritize advanced laryngoscopes to improve procedural efficiency, patient safety, and outcomes, leading to strong adoption of both rigid and video-assisted devices

- This widespread adoption is further supported by rising investments in healthcare, growing awareness among clinicians about advanced airway management techniques, and increasing numbers of surgical and emergency procedures, establishing laryngoscopes as essential equipment across hospitals, specialty clinics, and ambulatory centers

Japan Laryngoscopes Market Insight

The Japan laryngoscopes market is gaining momentum due to rapid urbanization, a technologically advanced healthcare system, and increasing surgical volumes. Japanese hospitals emphasize precision, safety, and innovation, driving demand for video and fiber-optic laryngoscopes. Integration of advanced airway management devices with ICU and surgical workflows is promoting growth. Moreover, the country’s aging population and increasing prevalence of respiratory conditions are creating higher demand for flexible and minimally invasive laryngoscope systems. Hospitals and specialty clinics in Japan continue to upgrade from standard rigid devices to advanced visualization systems.

India Laryngoscopes Market Insight

The India laryngoscopes market accounted for the fastest growth in the Asia-Pacific region in 2024, attributed to expanding healthcare infrastructure, rapid urbanization, and rising awareness of advanced airway management techniques. India is witnessing a surge in surgical procedures, ICU facilities, and emergency care units, increasing demand for video and flexible laryngoscopes. Government initiatives supporting modern hospitals and medical training programs are enhancing adoption. Affordable device options and rising private hospital networks further contribute to rapid market growth. The growing number of ENT and specialty clinics is also driving adoption of advanced laryngoscope systems.

South Korea Laryngoscopes Market Insight

The South Korea laryngoscopes market is expected to grow steadily, driven by advanced healthcare infrastructure, increasing surgical and ICU procedures, and rising adoption of video and flexible laryngoscopes. Hospitals and specialty clinics prioritize advanced airway management technologies to improve procedural safety and efficiency. Government initiatives to modernize medical facilities and support clinician training programs are further encouraging adoption. The presence of domestic medical device manufacturers and import of international products ensures the availability of high-quality laryngoscopes. Growing awareness about patient safety and airway management protocols is boosting demand for technologically advanced devices.

Asia-Pacific Laryngoscopes Market Share

The Asia-Pacific Laryngoscopes industry is primarily led by well-established companies, including:

- Ambu A/S (Denmark)

- Medtronic (Ireland)

- Olympus Corporation (Japan)

- Teleflex Incorporated (U.S.)

- KARL STORZ SE & Co. KG (Germany)

- Welch Allyn, Inc. (U.S.)

- Richard Wolf GmbH (Germany)

- Schoelly Fiberoptic GmbH (Germany)

- HEINE Optotechnik GmbH & Co. KG (Germany)

- Zhejiang Tiansong Medical Instrument Co., Ltd. (China)

- Shenda Endoscope Co., Ltd. (China)

- China Hawk (China)

- Kangji Medical (China)

- Zhejiang Sujia Medical Technology Co., Ltd. (China)

- Truphatek International Ltd. (Israel)

- Gimmi GmbH (Germany)

- XION (Germany)

- Timesco Healthcare Ltd (U.K.)

- Prodol Meditec, S.A. (Spain)

What are the Recent Developments in Asia-Pacific Laryngoscopes Market?

- In July 2025, Verathon® introduced the GlideScope® ClearFit™, a cover-based video laryngoscope designed to offer cost-effective airway management solutions. This device combines a reusable video baton with a selection of single-use covers, including Mac, Miller, and Hyperangle styles, to address a wide range of patient types and clinical settings

- In September 2023, Olympus announced the launch of its E-SteriScope™ single-use flexible video rhinolaryngoscope. This device is designed for enhanced visualization during nasal and sinus procedures, offering a single-use option to reduce the risk of cross-contamination

- In September 2023, Medtronic launched the latest version of its disposable laryngoscope system, incorporating advanced imaging technology. This development enhances visualization during intubation procedures, marking a significant shift towards integrating digital imaging to reduce complications related to airway management

- In June 2023, Teleflex announced a strategic partnership with Insighters Medical for the exclusive distribution of the Insighters® Video Laryngoscope System. This collaboration aims to expand the availability of advanced airway management solutions in various markets

- In January 2023, Timesco Healthcare Ltd unveiled a groundbreaking video laryngoscope at Arab Health 2023, designed to enhance intubation performance in patients with difficult airways. This device aims to improve visualization and ease of use in challenging clinical scenarios

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.