Asia Pacific Liquid Roofing Market

Market Size in USD Billion

USD

3.22 Billion

USD

5.87 Billion

2024

2032

USD

3.22 Billion

USD

5.87 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.22 Billion | |

| USD 5.87 Billion | |

| % | |

|

What is the Asia-Pacific Liquid Roofing Market Size and Growth Rate?

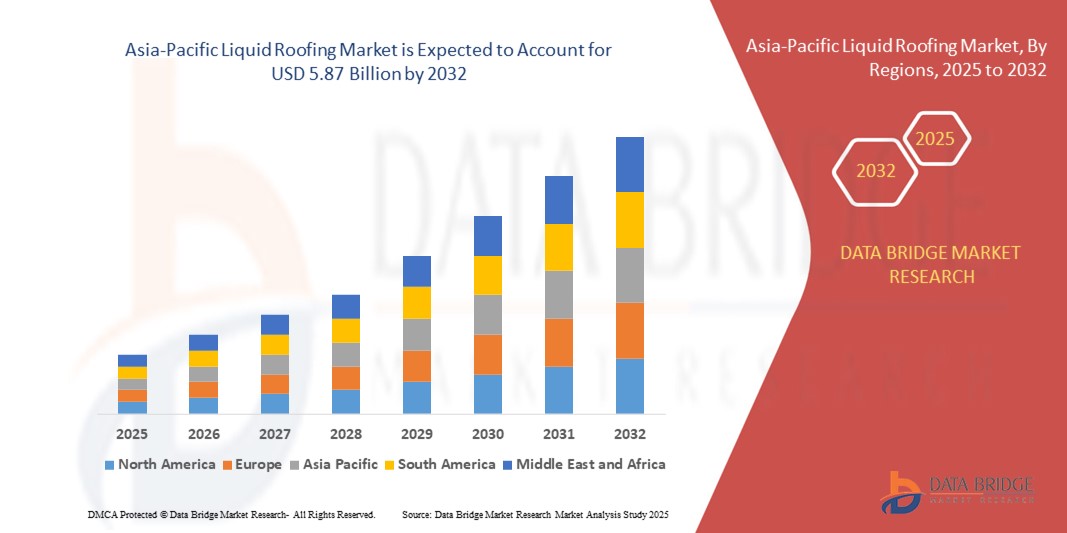

- Asia-Pacific liquid roofing market size was valued at USD 3.22 billion in 2024 and is expected to reach USD 5.87 billion by 2032, at a CAGR of 7.80% during the forecast period

- Factors such as growing demand for water proofing solutions, increased focus on construction and infrastructural growth are expected to drive the market growth rate during the forecast period. The major restraint that fluctuating raw material prices for liquid roofing products. Growing demand for green liquid roofing expected to provide opportunities for market growth. However, installation and weather dependency complexity are projected to challenge the market growth

What are the Major Takeaways of Liquid Roofing Market?

- The climate change brings about more extreme weather events, the need to protect buildings and infrastructure from water damage becomes paramount. Liquid roofing offers a versatile and durable solution for waterproofing flat or low-sloped roofs, making it a popular choice for commercial, residential, and industrial applications

- One of the key drivers behind the growing demand for liquid roofing is its ability to provide seamless protection against water infiltration. Traditional roofing materials such as asphalt or metal may develop seams and joints over time, which can become vulnerable points for water penetration

- Liquid roofing, on the other hand, forms a continuous membrane over the roof surface, effectively sealing off any potential entry points for water. This seamless nature enhances waterproofing performance and reduces the such aslihood of leaks and subsequent damage to the underlying structure

- China is expected to dominate the Asia-Pacific liquid roofing market with the market share of 51.13% in 2024, supported by rapid infrastructure development, urban expansion, and high demand for waterproofing materials

- India Liquid Roofing market is expected to expand at a significant CAGR of 10.87% during the forecast period, driven by accelerated urbanization, government initiatives such as Smart Cities Mission, and increasing residential construction

- The Bituminous Coatings segment dominated the market with a revenue share of 31.5% in 2024, primarily due to its cost-effectiveness, proven waterproofing capabilities, and strong adoption in large-scale residential and industrial applications

Report Scope and Liquid Roofing Market Segmentation

|

Attributes |

Liquid Roofing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Liquid Roofing Market?

Rising Demand for Sustainable and Energy-Efficient Roofing Solutions

- A major and accelerating trend in the global liquid roofing market is the shift toward eco-friendly, energy-efficient, and long-lasting roofing solutions. Liquid-applied systems are being increasingly adopted as they reduce material waste, enhance thermal insulation, and extend building lifespans

- For instance, liquid roofing systems incorporating cool roof coatings can reflect sunlight and reduce indoor cooling requirements, lowering energy consumption and utility costs. Manufacturers are also developing low-VOC, water-based formulations to comply with green building standards

- Advanced coatings such as polyurethane, silicone, and hybrid systems offer durability, resistance to UV radiation, ponding water, and weather extremes, making them suitable for both new constructions and refurbishments

- Furthermore, liquid-applied membranes are compatible with diverse roof types, including flat, pitched, and metal roofs, thereby driving adoption across residential, commercial, and industrial applications

- This rising focus on sustainability and performance is compelling major companies such as Sika AG and BASF SE to invest heavily in R&D for innovative formulations. For instance, BASF offers Elastocoat C, a spray-applied polyurea roof coating designed to provide superior waterproofing and durability

- As a result, the trend toward sustainable liquid roofing solutions is reshaping market dynamics, aligning with global energy-efficiency mandates and green construction practices

What are the Key Drivers of Liquid Roofing Market?

- Growing demand for roof refurbishment and repair in aging infrastructure, particularly in developed economies, is fueling the adoption of liquid roofing due to its cost-effectiveness and ease of application

- For instance, in March 2024, SOPREMA launched a new liquid-applied waterproofing membrane targeted at commercial refurbishment projects, highlighting the segment’s growth potential

- Rising awareness about energy savings and environmental sustainability is also accelerating demand. Liquid roofing systems with reflective coatings are increasingly being used to meet LEED certification and other green building requirements

- Rapid urbanization and construction activity in emerging economies, coupled with stricter building codes, are pushing demand for reliable and eco-friendly roofing solutions

- The convenience of fast application, minimal disruption to building use, and seamless waterproofing further enhances adoption, especially for commercial and industrial buildings

Which Factor is Challenging the Growth of the Liquid Roofing Market?

- High installation and material costs of premium liquid roofing systems remain a barrier, particularly for residential users and price-sensitive markets. While liquid systems offer long-term savings, the upfront cost compared to traditional roofing can deter adoption

- For instance, in 2023, reports indicated that polyurethane and silicone-based coatings cost 15–25% more than conventional bituminous materials, slowing penetration in cost-conscious regions

- Performance limitations under extreme weather conditions also pose a challenge. In very cold climates, some liquid-applied membranes may face issues related to curing and adhesion

- Availability of cheaper substitutes, such as sheet membranes and bituminous systems, creates competitive pressure, especially in markets where sustainability is not yet a priority

- Addressing these challenges requires manufacturers to focus on cost optimization, localized formulations, and consumer education regarding long-term benefits. Companies such as Henkel Corporation and MAPEI S.p.A. are investing in R&D to develop more affordable yet durable alternatives

- Overcoming these hurdles is crucial for ensuring wider adoption and sustained growth in the global Liquid Roofing market

How is the Liquid Roofing Market Segmented?

The market is segmented on the basis of type, communication protocol, unlocking mechanism, and application.

- By Type

On the basis of type, the liquid roofing market is segmented into Bituminous Coatings, Acrylic Coatings, Elastomeric Membranes, Silicone Coatings, PU/Acrylic Hybrids, Polyurethane Coatings, Epoxy Coatings, EPDM Rubbers, and Others. The Bituminous Coatings segment dominated the market with a revenue share of 31.5% in 2024, primarily due to its cost-effectiveness, proven waterproofing capabilities, and strong adoption in large-scale residential and industrial applications. Bituminous systems also benefit from widespread contractor familiarity and ease of application.

The Acrylic Coatings segment is expected to witness the fastest CAGR of 8.9% from 2025 to 2032, driven by its eco-friendly composition, UV resistance, and ability to reflect sunlight, which aligns with the increasing demand for energy-efficient roofing solutions. In addition, silicone and polyurethane coatings are gaining traction in niche applications due to their durability and chemical resistance.

- By Roof Type

On the basis of roof type, the liquid roofing market is segmented into Flat Roof, Pitched Roof, Saw Tooth, and Others. The Flat Roof segment accounted for the largest market share of 46.8% in 2024, as liquid roofing systems are particularly well-suited for seamless application on flat surfaces, where water pooling and leakage risks are higher. Flat roofs are widely used in commercial and industrial buildings, driving demand.

The Pitched Roof segment is expected to record the fastest growth at a CAGR of 9.2% from 2025 to 2032, fueled by rising adoption in residential projects where pitched designs dominate. Growing awareness of aesthetic appeal, coupled with liquid roofing’s flexibility to coat different slopes and surfaces, contributes to its demand. Furthermore, the saw tooth roof category is also gaining momentum, especially in manufacturing plants, where natural lighting integration pairs well with waterproof roofing solutions.

- By Substrate

On the basis of substrate, the liquid roofing market is segmented into Concrete, Composite, Metal, and Others. The Concrete segment dominated the market with a 38.7% revenue share in 2024, supported by the extensive use of concrete in modern infrastructure and the compatibility of liquid coatings with porous concrete surfaces. These coatings enhance durability, provide waterproofing, and extend the lifecycle of concrete roofs, making them a preferred choice in residential and commercial buildings.

The Metal substrate segment is expected to witness the fastest CAGR of 8.7% during 2025–2032, driven by rising demand in industrial and warehouse facilities. Liquid coatings prevent corrosion, resist temperature fluctuations, and improve thermal performance in metal structures. Composite substrates are also gaining relevance, especially in modular construction projects where lightweight materials are being adopted. This diversification in substrate compatibility is strengthening the market reach of liquid roofing systems.

- By Installation

On the basis of installation, the liquid roofing market is segmented into Reroofing and Repairs and New Construction. The Reroofing and Repairs segment dominated the market with 54.1% revenue share in 2024, driven by the rising need to extend the lifespan of aging infrastructure and buildings. Liquid roofing offers cost-effective refurbishment without complete removal of existing roofs, making it attractive for property owners and facility managers. It also minimizes downtime during application, which is vital for commercial and industrial establishments.

The New Construction segment is projected to grow at the fastest CAGR of 9.4% from 2025 to 2032, fueled by rapid urbanization, real estate expansion, and increasing investments in commercial and residential projects worldwide. Governments’ push for sustainable infrastructure and green buildings also supports adoption of advanced liquid roofing systems in new projects, particularly those that demand energy efficiency and durability.

- By End User

On the basis of end user, the liquid roofing market is segmented into Residential Building, Commercial Building, Industrial Building, and Public Infrastructure. The Commercial Building segment held the largest market share of 36.9% in 2024, owing to the widespread use of liquid roofing in office complexes, malls, healthcare centers, and educational institutions. These buildings often feature flat roofs and require high-performance waterproofing solutions, making liquid systems a popular choice.

The Residential Building segment is expected to grow at the fastest CAGR of 9.1% from 2025 to 2032, driven by rising adoption in housing projects, energy-efficient homes, and the demand for affordable yet durable waterproofing systems. Industrial buildings are also a strong segment, as factories and warehouses require chemical-resistant and weatherproof roofing. Meanwhile, public infrastructure projects, such as airports and transit hubs, are increasingly incorporating liquid roofing for long-term reliability and low maintenance.

Which Country Holds the Largest Share of the Asia-Pacific Liquid Roofing Market?

- China is expected to dominate the Asia-Pacific liquid roofing market with the market share of 51.13% in 2024, supported by rapid infrastructure development, urban expansion, and high demand for waterproofing materials

- The country’s strong emphasis on smart cities and sustainable construction is driving adoption of PU, acrylic, and silicone coatings. Furthermore, the expansion of local manufacturing ensures affordable solutions, making China a dominant hub for liquid-applied roofing systems.

India Liquid Roofing Market Insight

India liquid roofing market is expected to expand at a significant CAGR of 10.87% during the forecast period, driven by accelerated urbanization, government initiatives such as Smart Cities Mission, and increasing residential construction. Rising consumer preference for cost-effective and long-lasting waterproofing membranes is fostering demand. Moreover, the hot and humid climate creates a strong need for durable, heat-reflective coatings, boosting growth across residential, commercial, and public infrastructure projects.

Japan Liquid Roofing Market Insight

The Japan liquid roofing market is gaining traction due to the country’s aging infrastructure, high adoption of advanced technologies, and emphasis on disaster-resilient construction. Growing investments in renovation of old buildings and adoption of eco-friendly elastomeric membranes are boosting demand. In addition, the increasing focus on sustainable and energy-efficient roofing systems, supported by Japan’s commitment to carbon reduction, is strengthening market growth.

Australia Liquid Roofing Market Insight

The Australia liquid roofing market is witnessing rapid growth, supported by the thriving construction industry, rising infrastructure investments, and preference for sustainable solutions. The demand for UV-resistant and heat-reflective coatings is high, particularly due to the country’s extreme weather conditions. Renovation activities and government support for green building initiatives are further enhancing the adoption of liquid-applied roofing membranes across commercial and residential sectors.

Which are the Top Companies in Liquid Roofing Market?

The liquid roofing industry is primarily led by well-established companies, including:

- 3M (U.S.)

- BASF SE (Germany)

- Henkel Corporation (Germany)

- Sika AG (Switzerland)

- BMI Group Holdings UK Limited (U.K.)

- SOPREMA (France)

- SAINT-GOBAIN (France)

- Dow (U.S.)

- Johns Manville (U.S.)

- MAPEI S.p.A. (Italy)

- Akzo Nobel N.V. (Netherlands)

- Henry Company (U.S.)

- KRATON CORPORATION (U.S.)

- Pidilite Industries Ltd. (India)

- Garland Industries, Inc. (U.S.)

- GAF, Inc. (U.S.)

- H.B. Fuller Company (U.S.)

- STP Limited (India)

- RPM International Inc. (U.S.)

- KEMPER SYSTEM (Germany)

- ALT Global, LLC (U.S.)

- Widopan Products GmbH (Germany)

What are the Recent Developments in Asia-Pacific Liquid Roofing Market?

- In October 2024, Mapei acquired Wykamol, a local manufacturer, to strengthen its presence in the U.K. market. Through Mapei UK, the company aims to enhance its waterproofing product portfolio and better serve regional demand. This move reflects Mapei’s commitment to expanding its geographical reach and product diversity

- In February 2024, Mapei S.p.A. acquired Bitumat, a waterproofing specialist and producer of liquid-applied membranes in Saudi Arabia, to reinforce its market position in the Middle East. Bitumat’s extensive reach is expected to help Mapei access critical source markets. This acquisition underscores Mapei’s strategic focus on international growth and market penetration

- In January 2023, Sika AG and INEOS Enterprises entered into an agreement for INEOS to purchase MBCC Group’s admixtures business in the U.S., Canada, Europe, and the U.K., along with full operations in Australia and New Zealand. The disposal was required as part of Sika’s compliance measures following the MBCC Group acquisition. This step demonstrates Sika’s proactive approach in maintaining regulatory compliance while optimizing its portfolio

- In December 2022, Sika AG inaugurated a new manufacturing facility in Chongqing, China, dedicated to producing liquid membranes and mortars. The factory is positioned to strengthen Sika’s role in this rapidly growing region, which is evolving into a key commercial hub. This expansion highlights Sika’s long-term vision to capture growth opportunities in urbanizing markets

- In October 2021, STP Limited, India, achieved ISO 9001:2015 certification for its quality management system, affirming its alignment with global standards of excellence. This certification validates the company’s consistent focus on quality and customer satisfaction. This milestone reflects STP’s dedication to maintaining international credibility and operational efficiency

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Asia Pacific Liquid Roofing Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Asia Pacific Liquid Roofing Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Asia Pacific Liquid Roofing Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.