Asia Pacific Lung Cancer Screening Software Market

Market Size in USD Million

USD

450.00 Million

USD

2,040.55 Million

2025

2033

USD

450.00 Million

USD

2,040.55 Million

2025

2033

| 2026 - 2033 | |

| USD 450.00 Million | |

| USD 2,040.55 Million | |

| % | |

|

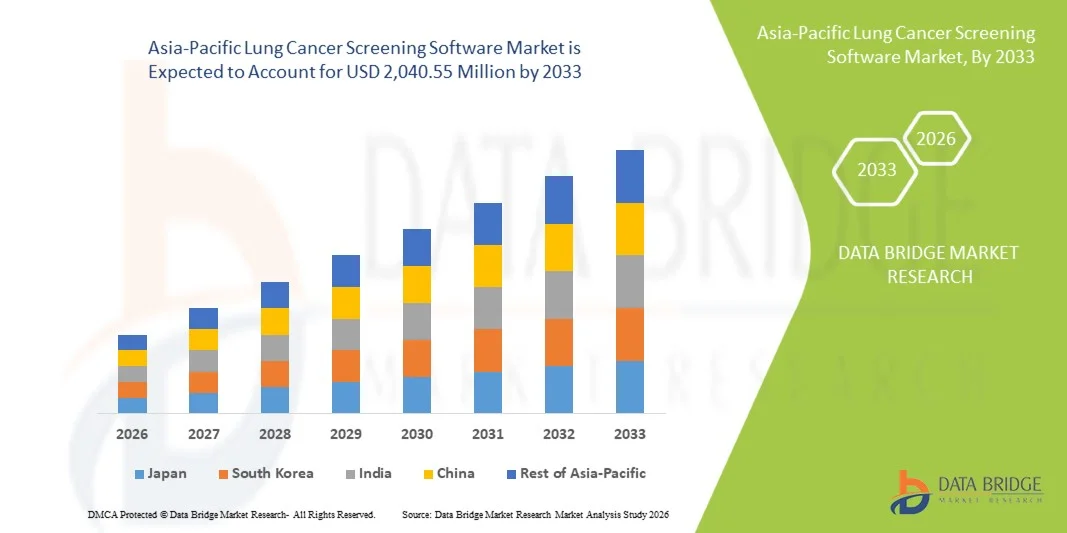

Asia-Pacific Lung Cancer Screening Software Market Size

- The Asia-Pacific lung cancer screening software market size was valued at USD 450.00 million in 2025 and is expected to reach USD 2,040.55 million by 2033, at a CAGR of 20.8% during the forecast period

- The market growth is primarily driven by the rising incidence of lung cancer across Asia-Pacific, increasing adoption of AI-powered imaging and diagnostic software, and growing implementation of national lung cancer screening programs in countries such as China, Japan, and South Korea, which are enhancing early detection capabilities and clinical efficiency

- Furthermore, expanding healthcare digitalization, increasing investments in radiology workflow automation, and growing demand for accurate, non-invasive, and cost-effective screening solutions are accelerating the adoption of lung cancer screening software, thereby significantly boosting the industry’s growth

Asia-Pacific Lung Cancer Screening Software Market Analysis

- Lung cancer screening software, comprising AI-powered imaging analysis, radiology workflow systems, and computer-aided detection tools, is increasingly becoming a critical component of modern oncology diagnostics due to its ability to improve early detection accuracy, streamline radiologist workflows, and enable large-scale CT-based screening programs across hospitals and diagnostic centers

- The escalating demand for these solutions is primarily driven by the rising burden of lung cancer across Asia-Pacific, expanding government-led screening initiatives, and rapid adoption of AI-enabled diagnostic platforms that enhance CT interpretation efficiency, reduce diagnostic delays, and support cost-effective early-stage cancer detection

- China dominated the Asia-Pacific lung cancer screening software market with the largest revenue share of 35.7% in 2025, supported by strong national screening programs, advanced healthcare infrastructure, and rapid deployment of AI-based radiology tools

- India is expected to be the fastest growing country in the lung cancer screening software market during the forecast period due to increasing investments in healthcare digitization, expanding diagnostic networks, and rising awareness of early cancer screening

- The lung cancer screening radiology solution segment dominated the Asia-Pacific market in 2025 with a market share of 41.9%, driven by its central role in CT-based screening programs, strong integration with hospital systems such as PACS/RIS, and high clinical reliance on radiology software for accurate nodule detection and early-stage cancer diagnosis

Report Scope and Asia-Pacific Lung Cancer Screening Software Market Segmentation

|

Attributes |

Asia-Pacific Lung Cancer Screening Software Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Lung Cancer Screening Software Market Trends

“Rising Integration of AI-Driven Imaging and Clinical Decision Support Systems”

- A significant and accelerating trend in the Asia-Pacific lung cancer screening software market is the deepening integration of artificial intelligence (AI) with CT imaging platforms, radiology workflows, and computer-aided detection systems, improving early-stage lung cancer identification accuracy and screening efficiency across healthcare facilities

- For instance, advanced AI-based screening platforms such as those used in major hospital networks in China and Japan are being integrated with PACS and RIS systems, enabling automated nodule detection, risk scoring, and faster radiologist review workflows

- AI integration in lung cancer screening software enables capabilities such as automated lesion segmentation, predictive risk stratification, and intelligent alerts for suspicious pulmonary nodules, improving diagnostic precision and reducing radiologist workload in high-volume screening programs

- The seamless integration of screening software with hospital information systems and cloud-based imaging platforms facilitates centralized data access, enabling clinicians to manage patient scans, historical imaging records, and diagnostic reports within unified digital ecosystems

- This trend toward intelligent, data-driven, and interoperable screening solutions is reshaping clinical expectations, with companies increasingly developing AI-enabled radiology tools that support real-time decision-making and large-scale population screening initiatives

- The demand for advanced lung cancer screening software is growing rapidly across Asia-Pacific as healthcare providers prioritize early detection, operational efficiency, and scalable AI-powered diagnostic infrastructure

- In addition, the rising adoption of cloud-based radiology platforms is enabling cross-border data sharing and multi-center screening programs, improving diagnostic consistency and expanding access to advanced screening tools in emerging Asia-Pacific markets

Asia-Pacific Lung Cancer Screening Software Market Dynamics

Driver

“Rising Burden of Lung Cancer and Expansion of National Screening Programs”

- The increasing prevalence of lung cancer across Asia-Pacific, coupled with expanding government-led screening initiatives and growing adoption of digital diagnostic infrastructure, is a major driver accelerating demand for lung cancer screening software

- For instance, in April 2025, major healthcare authorities in China expanded AI-assisted lung cancer screening programs across multiple provinces, integrating advanced imaging analytics into public hospital screening workflows to improve early detection rates

- As healthcare systems prioritize early diagnosis and improved patient outcomes, lung cancer screening software provides advanced capabilities such as automated CT scan analysis, nodule tracking, and risk-based patient stratification

- Furthermore, increasing investments in healthcare digitization and radiology automation are making AI-enabled screening tools a core component of hospital diagnostic workflows across both public and private sectors

- The growing need for efficient, large-scale screening in high-risk populations, combined with rising awareness of early cancer detection benefits, is strongly driving adoption across the region

- Expanding availability of cloud-based and AI-powered radiology solutions further supports integration into existing healthcare infrastructure, boosting overall market growth

- In addition, supportive government funding initiatives and public-private partnerships in countries such as India and South Korea are strengthening screening program implementation and accelerating software deployment

- Moreover, increasing physician acceptance of AI-assisted diagnostics due to improved accuracy and reduced workload is further boosting adoption across tertiary care hospitals and diagnostic centers

Restraint/Challenge

“Data Privacy Concerns and High Implementation Complexity”

- Concerns surrounding patient data privacy, regulatory compliance, and cybersecurity risks in AI-driven healthcare systems pose a significant challenge to broader adoption of lung cancer screening software across Asia-Pacific

- For instance, increasing scrutiny of cross-border medical data sharing and AI model transparency requirements in countries such as Japan and South Korea has made healthcare providers cautious in deploying cloud-based diagnostic platforms

- Addressing these concerns requires strict compliance with healthcare data protection regulations, secure encryption protocols, and transparent AI validation processes to build trust among healthcare providers and regulators

- In addition, the relatively high cost of implementing advanced AI screening systems, along with the need for specialized IT infrastructure and trained radiology personnel, can limit adoption in smaller hospitals and developing healthcare settings

- While large urban hospitals are rapidly adopting these technologies, rural and resource-constrained regions continue to face barriers in deployment due to infrastructure limitations and budget constraints

- Overcoming these challenges through cost-effective deployment models, improved regulatory harmonization, and enhanced cybersecurity frameworks will be essential for sustained market expansion

- Furthermore, interoperability issues between legacy hospital systems and modern AI platforms often delay implementation timelines and increase integration complexity

- Moreover, shortage of skilled radiologists and AI-trained healthcare professionals in several Asia-Pacific countries further constrains the optimal utilization of advanced screening software solutions

Asia-Pacific Lung Cancer Screening Software Market Scope

The market is segmented on the basis of mode of delivery, product, type, application, platform, purchase mode, end user, and distribution channel.

- By Mode of Delivery

On the basis of mode of delivery, the Asia-Pacific lung cancer screening software market is segmented into cloud-based solutions, on-premise solutions, and web-based solutions. The cloud-based solutions segment dominated the market with the largest revenue share of 52% in 2025, driven by increasing adoption of scalable healthcare IT infrastructure and the need for centralized access to radiology data across multi-location hospital networks. Cloud deployment enables real-time image sharing, AI-based analytics integration, and seamless updates, making it highly suitable for large-scale lung cancer screening programs. It also reduces dependency on heavy on-site IT infrastructure, which is critical for cost-sensitive healthcare systems in emerging Asia-Pacific economies. Growing integration with AI diagnostic engines further strengthens its dominance. In addition, rising government focus on digital health transformation is accelerating cloud adoption across hospitals and diagnostic centers.

The cloud-based solutions segment is also expected to witness the fastest growth rate from 2026 to 2033, fueled by rapid healthcare digitalization, expansion of tele-radiology services, and increasing adoption of AI-powered diagnostic platforms. Hospitals and diagnostic centers are increasingly shifting toward cloud ecosystems to support remote screening, cross-border data collaboration, and centralized patient record management. The flexibility of subscription-based pricing models is further encouraging adoption among mid-sized healthcare providers. Rising investments in healthcare cloud infrastructure across India and Southeast Asia are significantly contributing to growth. Moreover, increasing demand for real-time analytics in cancer screening programs is boosting cloud penetration.

- By Product

On the basis of product, the market is segmented into lung cancer screening radiology solution, patient management software, nodule management software, data collection and reporting, patient coordination and workflow, lung nodule computer-aided detection, pathology and cancer staging, statistical audit reporting, screening PACS, and practice management and audit log tracking. The lung cancer screening radiology solution segment dominated the market with the largest revenue share of 41.9% in 2025, driven by its central role in CT-based screening workflows and early detection of pulmonary nodules. These solutions are widely integrated with PACS and RIS systems, ensuring seamless imaging analysis and reporting for radiologists. High reliance on radiology-centric AI tools in mass screening programs across China, Japan, and South Korea further supports its leadership. It enables faster clinical decision-making in high-volume hospital environments. Increasing burden of lung cancer also reinforces demand for advanced radiology screening tools. In addition, strong government-backed screening initiatives are boosting deployment in public healthcare systems.

The lung nodule computer-aided detection (CAD) segment is also expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of AI-based diagnostic assistance tools that enhance early-stage cancer detection accuracy. CAD systems significantly reduce radiologist workload by automatically identifying suspicious nodules in CT scans. Continuous improvements in deep learning models are increasing detection sensitivity and reliability. Integration with cloud-based imaging platforms is further expanding accessibility across smaller hospitals. Rising shortage of trained radiologists in Asia-Pacific is also accelerating demand for CAD solutions. Moreover, increasing clinical trust in AI-assisted diagnosis is supporting rapid market expansion.

- By Type

On the basis of type, the market is segmented into computer-assisted screening and traditional screening. The computer-assisted screening segment dominated the market with the largest revenue share of 70% in 2025, driven by rapid adoption of AI-enabled diagnostic technologies and increasing demand for accurate and scalable lung cancer detection solutions. These systems enhance early detection by analyzing CT scans with high precision and consistency compared to manual interpretation. They also reduce diagnostic errors and improve workflow efficiency in radiology departments. Government support for AI-based healthcare innovation in China and Japan is further strengthening adoption. Increasing screening programs for high-risk populations is also contributing to dominance. In addition, hospitals are rapidly shifting toward automated workflows to handle rising imaging volumes.

The computer-assisted screening segment is also expected to witness the fastest growth rate from 2026 to 2033, fueled by expansion of national lung cancer screening programs and integration of AI tools into routine clinical workflows. Healthcare providers are adopting automated systems to overcome radiologist shortages and improve diagnostic throughput. Advancements in real-time image processing and AI model accuracy are enhancing clinical acceptance. Cloud-based deployment of screening tools is further accelerating accessibility in developing regions. Increasing investments in digital healthcare infrastructure across India and Southeast Asia are boosting growth. Moreover, growing awareness of early cancer detection is driving widespread adoption.

- By Application

On the basis of application, the market is segmented into non-small cell lung cancer (NSCLC) and small cell lung cancer (SCLC). The non-small cell lung cancer (NSCLC) segment dominated the market with the largest revenue share of 80% in 2025, driven by its high prevalence across Asia-Pacific and its slower progression compared to SCLC, which makes it more suitable for early screening and intervention. Screening software is primarily optimized to detect NSCLC-related nodules in CT imaging. Increasing use of AI-based detection tools is improving early identification rates. Strong focus on population-wide screening programs is further supporting dominance. Hospitals are prioritizing NSCLC detection due to higher treatment success rates when diagnosed early. In addition, rising smoking-related cancer cases are expanding the patient pool.

The NSCLC segment is also expected to witness the fastest growth rate from 2026 to 2033, driven by increasing awareness of early diagnosis and expansion of structured screening programs. AI-enabled imaging tools are improving detection of early-stage NSCLC lesions. Governments in China, India, and Japan are actively promoting lung cancer screening initiatives. Rising healthcare investments are supporting wider deployment of screening technologies. Increasing adoption of precision medicine approaches is also boosting demand. Furthermore, growing hospital infrastructure is enabling large-scale screening expansion.

- By Platform

On the basis of platform, the market is segmented into standalone and integrated solutions. The integrated platform segment dominated the market with the largest revenue share of 75% in 2025, driven by strong demand for interoperable healthcare systems that connect radiology software with PACS, RIS, and EHR platforms. Integrated systems improve workflow efficiency and ensure seamless data exchange across departments. They also enable better coordination between radiologists and oncologists. Large hospitals prefer integrated solutions for centralized patient management. Increasing adoption of AI-enabled enterprise healthcare systems further supports dominance. In addition, government digital health initiatives are promoting interoperability standards.

The integrated platform segment is also expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for unified healthcare ecosystems and smart hospital initiatives. Hospitals are increasingly investing in integrated AI-based diagnostic platforms. These systems reduce duplication of data and improve diagnostic speed. Expansion of multi-specialty hospital networks across Asia-Pacific is further boosting adoption. Growing need for real-time clinical decision support is also contributing to growth. Moreover, increasing investment in healthcare IT modernization is accelerating integration trends.

- By Purchase Mode

On the basis of purchase mode, the market is segmented into institutional and individual. The institutional segment dominated the market with the largest revenue share of 90% in 2025, driven by large-scale procurement by hospitals, government healthcare programs, and diagnostic chains. Institutions prefer bulk licensing models for cost efficiency and scalability. These solutions are integrated into national screening programs and hospital networks. Increasing government funding for cancer screening is also supporting dominance. Institutional buyers require compliance-ready and interoperable systems. In addition, long-term service contracts with vendors strengthen adoption.

The institutional segment is also expected to witness the fastest growth rate from 2026 to 2033, driven by expansion of public healthcare infrastructure and rising investment in AI-based diagnostic programs. Governments across Asia-Pacific are actively funding lung cancer screening initiatives. Large private hospital chains are also expanding procurement of advanced software solutions. Increasing cancer burden is pushing institutions toward early detection tools. Subscription-based enterprise models are becoming more common. Furthermore, digital transformation of healthcare systems is accelerating institutional adoption.

- By End User

On the basis of end user, the market is segmented into oncology centers, hospitals, ambulatory surgical centers, and others. The hospitals segment dominated the market with the largest revenue share of 65% in 2025, driven by high patient volume and advanced imaging infrastructure. Hospitals serve as primary centers for CT-based lung cancer screening programs. They also have better access to AI-enabled diagnostic tools and trained radiology staff. Government screening initiatives are largely implemented through hospitals. Increasing adoption of integrated healthcare IT systems further supports dominance. In addition, hospitals are key hubs for early cancer diagnosis and treatment planning.

The oncology centers segment is also expected to witness the fastest growth rate from 2026 to 2033, driven by increasing specialization in cancer care and rising demand for advanced screening technologies. Oncology centers are rapidly adopting AI-based diagnostic tools for precision screening. Rising cancer incidence is fueling expansion of dedicated oncology infrastructure. These centers focus heavily on early detection and personalized treatment pathways. Increasing investments in specialized cancer hospitals are supporting growth. Moreover, collaboration between oncology centers and AI vendors is accelerating adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and third-party distributors. The direct tender segment dominated the market with the largest revenue share of 80% in 2025, driven by large-scale procurement by government healthcare systems and hospital networks. Direct procurement ensures better pricing, compliance, and customization. It is widely used in national screening programs. Vendors prefer direct engagement for long-term contracts. Increasing public healthcare funding supports dominance. In addition, integration complexity of AI systems favors direct deployment models.

The direct tender segment is also expected to witness the fastest growth rate from 2026 to 2033, driven by rising government-led digital health initiatives and expansion of national cancer screening programs. Public procurement systems are becoming more centralized. Governments are investing heavily in AI-based diagnostic infrastructure. Hospitals are increasingly relying on tender-based purchasing for large deployments. Growing need for standardized screening platforms is also boosting demand. Moreover, expansion of public-private partnerships is strengthening direct distribution channels.

Asia-Pacific Lung Cancer Screening Software Market Regional Analysis

- China dominated the Asia-Pacific lung cancer screening software market with the largest revenue share of 35.7% in 2025, supported by strong national screening programs, advanced healthcare infrastructure, and rapid deployment of AI-based radiology tools

- Healthcare institutions in the country are increasingly deploying advanced CT imaging analytics, computer-aided detection tools, and integrated PACS/RIS systems to improve early-stage lung cancer detection accuracy and support high-volume screening initiatives

- This widespread adoption is further supported by strong government funding for healthcare digitalization, continuous expansion of hospital infrastructure, and growing collaboration between domestic AI companies and medical imaging providers, establishing China as the key growth hub in the Asia-Pacific lung cancer screening software market

The China Lung Cancer Screening Software Market Insight

The China lung cancer screening software market captured the largest revenue share in Asia-Pacific in 2025, driven by large-scale government-led screening programs and high lung cancer prevalence. Hospitals are increasingly adopting AI-powered CT imaging platforms and computer-aided detection tools to improve early diagnosis accuracy. Strong public healthcare investment and rapid digitalization of hospital infrastructure are further accelerating deployment. In addition, collaboration between domestic AI companies and medical imaging providers is enhancing innovation in radiology workflows. China’s extensive hospital network enables large-scale implementation of screening programs. Moreover, integration of AI with PACS systems is significantly improving diagnostic efficiency across urban healthcare facilities.

Japan Lung Cancer Screening Software Market Insight

The Japan lung cancer screening software market is growing steadily due to its advanced healthcare system and strong focus on early cancer detection. Hospitals are increasingly integrating AI-based radiology solutions to enhance precision in CT scan interpretation. The country’s aging population is significantly increasing demand for frequent and preventive screening programs. Strong adoption of digital health technologies and government support for medical innovation are further supporting market growth. Japan also emphasizes high-quality diagnostic accuracy, which drives adoption of advanced screening software. In addition, integration with hospital information systems is improving workflow efficiency across healthcare institutions.

India Lung Cancer Screening Software Market Insight

The India lung cancer screening software market is emerging as one of the fastest-growing in Asia due to rising cancer awareness and expanding healthcare infrastructure. Increasing adoption of AI-based diagnostic tools in private hospitals and diagnostic chains is improving early detection rates. Government initiatives supporting digital health and smart hospital development are further boosting demand. The growing burden of lung cancer, especially in urban populations, is driving need for scalable screening solutions. In addition, increasing investments in radiology infrastructure and cloud-based healthcare platforms are accelerating adoption. Cost-effective AI screening tools are also making advanced diagnostics more accessible across tier-2 and tier-3 cities.

South Korea Lung Cancer Screening Software Market Insight

The South Korea lung cancer screening software market is expanding due to strong digital healthcare infrastructure and high adoption of AI-driven medical imaging technologies. Hospitals are increasingly using advanced screening software integrated with PACS systems to improve diagnostic accuracy. Government-led cancer screening initiatives and strong insurance coverage are supporting widespread adoption. The country’s focus on precision medicine and smart hospital systems is further driving market growth. In addition, collaboration between healthcare institutions and AI technology companies is accelerating innovation. High technological readiness is enabling rapid integration of automated lung cancer detection tools.

Asia-Pacific Lung Cancer Screening Software Market Share

The Asia-Pacific Lung Cancer Screening Software industry is primarily led by well-established companies, including:

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- GE HealthCare (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Fujifilm Holdings Corporation (Japan)

- Agfa-Gevaert N.V. (Belgium)

- Carestream Health, Inc. (U.S.)

- TeraRecon, Inc. (U.S.)

- Riverain Technologies LLC (U.S.)

- Median Technologies (France)

- Esaote S.p.A. (Italy)

- Visage Imaging GmbH (Germany)

- MeVis Medical Solutions AG (Germany)

- Riverain Technologies LLC (U.S.)

- Coreline Soft Co., Ltd. (South Korea)

- Lunit Inc. (South Korea)

- AZmed SAS (France)

- Thirona B.V. (Netherlands)

- Aidoc Medical Ltd. (Israel)

- Zebra Medical Vision Ltd. (Israel)

What are the Recent Developments in Asia-Pacific Lung Cancer Screening Software Market?

- In April 2026, AstraZeneca India partnered with the Telangana government to launch AI-powered lung cancer screening across 20 public hospitals in India. This initiative integrates AI-based chest X-ray and nodule detection software developed by Indian health-tech firms such as Qure.ai to improve early detection rates

- In January 2026, NHS-style AI screening expansion trends influenced Asia-Pacific adoption with new AI lung cancer diagnostic trials and robotic-assisted screening research. While led in the UK, similar AI-based diagnostic approaches are being rapidly adopted across Asia-Pacific hospitals, particularly in Japan and Australia

- In November 2025, India’s Yashoda Hospitals launched an AI-driven lung nodule clinic in partnership with Qure.ai and AstraZeneca to improve early lung cancer detection. The initiative integrates AI-powered chest X-ray screening software into routine hospital workflows to automatically detect and triage suspicious lung nodules

- In June 2025, researchers highlighted rapid advancement of AI-based lung cancer screening models in East Asia through clinical studies and hospital deployments. A Hong Kong–based clinical study evaluated AI-based lung cancer screening systems for high-risk populations, including never-smokers

- In June 2025, advanced transformer-based AI models for lung cancer screening and risk prediction were published for large-scale CT analysis. New deep learning frameworks trained on over 90,000 CT scans were introduced for predicting lung cancer risk up to 6 years in advance

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.