Asia Pacific Lung Cancer Therapeutics Market

Market Size in USD Billion

USD

1.47 Billion

USD

2.75 Billion

2024

2032

USD

1.47 Billion

USD

2.75 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.47 Billion | |

| USD 2.75 Billion | |

| % | |

|

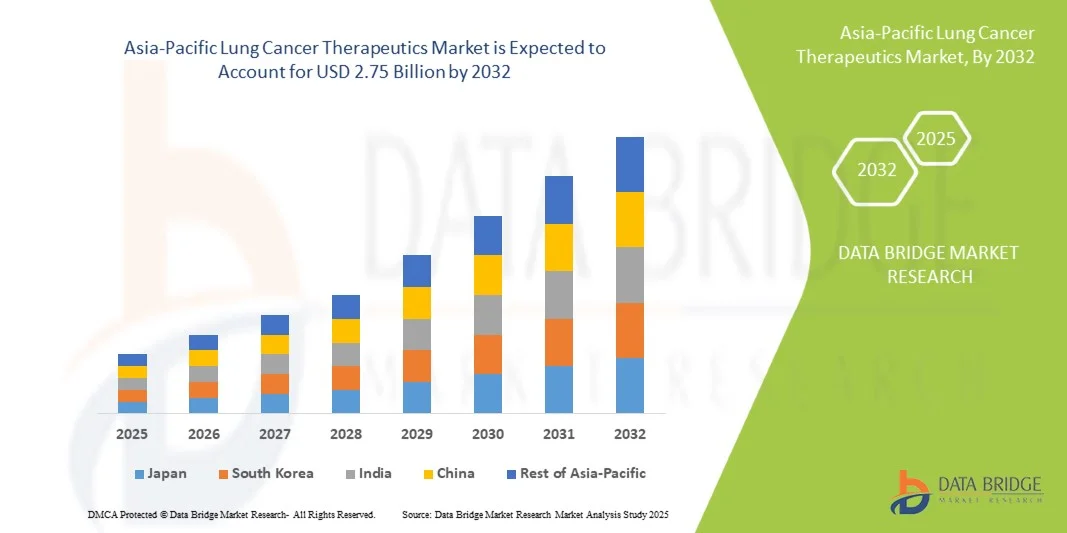

Asia-Pacific Lung Cancer Therapeutics Market Size

- The Asia-Pacific Lung Cancer Therapeutics Market size was valued at USD 1.47 billion in 2024 and is expected to reach USD 2.75 billion by 2032, at a CAGR of 8.1% during the forecast period

- The market growth is largely fuelled by increasing incidence of lung cancer in the region, expansion of advanced therapies, improving healthcare infrastructure, and greater accessibility in emerging Asia‑Pacific markets

- Furthermore, stronger demand for personalized lung‑cancer treatment, rising screening and early‑detection initiatives, and increasing adoption of integrated care pathways are establishing lung‑cancer therapeutics as a key oncology segment. These converging factors are accelerating uptake of newer therapeutics, thereby significantly boosting the industry’s growth

Asia-Pacific Lung Cancer Therapeutics Market Analysis

- Lung cancer therapeutics, encompassing targeted therapies, immunotherapies, and chemotherapy for lung cancer treatment, are increasingly vital components of modern oncology care in both hospital and outpatient settings due to their enhanced efficacy, personalized treatment approaches, and integration with precision medicine initiatives

- The escalating demand for lung cancer therapeutics is primarily fueled by rising incidence of lung cancer in Asia-Pacific countries, growing awareness and early screening programs, and increasing adoption of advanced therapies such as targeted and immuno-oncology drugs

- China dominated the Asia-Pacific Lung Cancer Therapeutics Market with the largest revenue share of 48.1% in 2024, characterized by high prevalence of lung cancer, strong government support for cancer care infrastructure, and a robust pipeline of novel drugs

- India is expected to be the fastest growing country in the Asia-Pacific Lung Cancer Therapeutics Market during the forecast period due to increasing healthcare expenditure, growing availability of advanced therapies, and rising patient awareness

- Targeted therapy segment dominated the Asia-Pacific Lung Cancer Therapeutics Market with a market share of 45.9% in 2024, driven by its proven efficacy in non-small cell lung cancer (NSCLC), personalized treatment options based on genetic biomarkers, and rapid adoption in hospitals and specialty oncology centers

Report Scope and Asia-Pacific Lung Cancer Therapeutics Market Segmentation

|

Attributes |

Asia-Pacific Lung Cancer Therapeutics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Lung Cancer Therapeutics Market Trends

“Precision Medicine and Biomarker-Driven Therapies”

- A significant and accelerating trend in the Asia-Pacific Lung Cancer Therapeutics Market is the increasing adoption of precision medicine, where treatments are tailored based on genetic biomarkers, enhancing efficacy and minimizing adverse effects

- For instance, targeted therapies such as EGFR and ALK inhibitors in China allow clinicians to select drugs specifically suited to the patient’s tumor mutation profile, improving survival rates and reducing trial-and-error prescribing

- Precision medicine integration enables continuous monitoring of patient response and adaptive treatment adjustments, while emerging diagnostic tools such as liquid biopsies provide real-time insights into tumor evolution

- The seamless incorporation of biomarker-driven therapies with hospital oncology systems and digital health platforms allows clinicians to optimize treatment plans and coordinate care more effectively

- This trend towards more personalized, data-driven, and adaptive treatment strategies is fundamentally reshaping patient expectations in lung cancer care, prompting pharmaceutical companies such as AstraZeneca and Boehringer Ingelheim to focus on biomarker-guided therapeutics

- The demand for precision and biomarker-integrated lung cancer therapeutics is growing rapidly across both hospital and outpatient settings, as healthcare providers increasingly prioritize personalized outcomes and treatment efficiency

Asia-Pacific Lung Cancer Therapeutics Market Dynamics

Driver

“Rising Lung Cancer Incidence and Expanding Healthcare Infrastructure”

- The increasing prevalence of lung cancer across Asia-Pacific countries, coupled with expanding healthcare infrastructure and access to advanced therapies, is a major driver of market growth

- For instance, in 2024, China launched multiple government-supported lung cancer screening initiatives to increase early diagnosis, enabling timely treatment with targeted and immuno-oncology therapies

- As awareness of lung cancer risk factors grows and screening programs expand, more patients are being diagnosed at treatable stages, boosting demand for therapeutics

- Furthermore, investments in oncology hospitals, diagnostic facilities, and reimbursement schemes are enabling wider access to advanced lung cancer treatments across emerging countries such as India and Vietnam

- The growing integration of novel therapies with existing treatment protocols, combined with increased patient access to advanced diagnostics and care pathways, is accelerating adoption in both urban and semi-urban healthcare centers

- Rising collaborations between pharmaceutical companies and research institutions are accelerating the development and clinical adoption of next-generation lung cancer therapeutics across the region

- Increasing government and private funding for oncology research and clinical trials in countries such as Japan and South Korea is fostering innovation and supporting the introduction of new lung cancer treatment options

Restraint/Challenge

“High Treatment Costs and Regulatory Barriers”

- The high cost of advanced lung cancer therapeutics, including targeted therapies and immunotherapies, poses a significant challenge to broader market penetration in the Asia-Pacific region

- For instance, the price of EGFR inhibitors or checkpoint inhibitors can limit accessibility for patients in low- and middle-income countries, affecting overall adoption rates

- Strict regulatory approval processes and varying country-specific drug reimbursement policies further delay market entry for novel therapies, creating hurdles for pharmaceutical companies

- While government initiatives and patient assistance programs are gradually improving accessibility, perceived high treatment costs continue to hinder adoption, particularly in rural and underinsured populations

- Addressing these challenges through pricing strategies, expanded insurance coverage, faster regulatory approvals, and patient support programs will be vital for sustained market growth in the Asia-Pacific lung cancer therapeutics sector

- Limited healthcare workforce and inadequate oncology specialists in certain countries restrict the administration and monitoring of advanced lung cancer therapies, slowing market expansion

- Variability in diagnostic infrastructure and access to biomarker testing across Asia-Pacific countries poses challenges for implementing personalized treatment regimens, impacting overall adoption of precision therapeutics

Asia-Pacific Lung Cancer Therapeutics Market Scope

The market is segmented on the basis of cancer type, molecule type, drug class, treatment type, therapy type, end user, and distribution channel.

- By Cancer Type

On the basis of cancer type, the market is segmented into Non-Small Cell Lung Cancer (NSCLC), Metastatic Lung Cancer, Pulmonary Neuroendocrine Tumors, Mediastinal Tumors, Mesothelioma, and Chest Wall Tumors. The NSCLC segment dominated the market with the largest revenue share in 2024, driven by its high prevalence in Asia-Pacific countries such as China, Japan, and India. NSCLC accounts for approximately 85% of lung cancer cases, creating substantial demand for targeted therapies and immunotherapies. Hospitals and specialty clinics are increasingly adopting advanced treatment regimens for NSCLC, including EGFR inhibitors and combination therapies, boosting overall market revenue. The segment benefits from strong ongoing clinical research, approval of new targeted drugs, and increasing awareness of early diagnosis programs. NSCLC-focused therapies also enjoy robust reimbursement coverage in key countries, further reinforcing market dominance.

The Metastatic Lung Cancer segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by the rising incidence of late-stage diagnoses and the growing availability of advanced therapeutics. Targeted therapies, immunotherapy, and combination treatments are increasingly used to manage metastatic cases, improving patient survival and quality of life. Expansion of oncology centers in emerging countries and government screening initiatives support the adoption of advanced therapies for metastatic patients. Growing physician awareness and patient preference for advanced treatment options further contribute to rapid adoption. Increasing clinical trial activity and availability of novel agents for metastatic lung cancer are expected to sustain this growth trend.

- By Molecule Type

On the basis of molecule type, the market is segmented into small molecules and biologics. The Small Molecules segment dominated the market in 2024 due to the extensive use of tyrosine kinase inhibitors (TKIs) such as EGFR inhibitors, which are orally administered and widely accessible. Small molecules provide effective targeted therapy for specific genetic mutations and are commonly prescribed across NSCLC and metastatic cases. These drugs benefit from established manufacturing processes, extensive clinical validation, and relatively lower costs compared to biologics, encouraging adoption across hospitals and specialty clinics. Strong pipeline activity for new small molecule drugs further sustains market dominance. Patients and clinicians often prefer small molecules for their ease of administration and predictable pharmacokinetics. In addition, government and insurance reimbursement schemes support wider access, reinforcing this segment’s leading position.

The Biologics segment is anticipated to witness the fastest growth from 2025 to 2032, driven by increasing use of monoclonal antibodies and immuno-oncology agents. Biologics such as PD-1/PD-L1 inhibitors are increasingly integrated into combination therapies to improve efficacy in NSCLC and metastatic lung cancer patients. Growing availability in China, Japan, and South Korea, coupled with rising patient awareness of immunotherapy, is propelling adoption. Ongoing research and new approvals for biologics expand treatment options, attracting more hospitals and clinics to adopt these therapies. The segment also benefits from strategic partnerships between pharmaceutical companies and healthcare providers to increase accessibility.

- By Drug Class

On the basis of drug class, the market is segmented into alkylating agents, antimetabolites, EGFR inhibitors, mitotic inhibitors, multikinase inhibitors, and others. The EGFR Inhibitors segment dominated in 2024 due to high prevalence of EGFR mutations in Asian populations, particularly in China and Japan. EGFR inhibitors such as gefitinib, erlotinib, and osimertinib are widely prescribed for NSCLC patients, offering targeted action with improved survival rates. Market dominance is reinforced by ongoing clinical trials, increasing physician adoption, and reimbursement support. EGFR inhibitors are also often combined with other therapies to enhance patient outcomes, further boosting market share. The availability of oral EGFR inhibitors adds convenience for patients and encourages adherence to therapy. Rapid advancements in next-generation EGFR inhibitors further support market growth.

The Multikinase Inhibitors segment is expected to witness the fastest CAGR from 2025 to 2032, driven by their multi-targeted action against several oncogenic pathways. These drugs are increasingly used in combination regimens to treat advanced or refractory lung cancers. Clinical research, growing regulatory approvals, and rising adoption in tertiary hospitals and specialty clinics are key growth enablers. The segment benefits from increasing awareness among oncologists regarding the advantages of multitargeted therapy. Enhanced efficacy and reduced resistance in combination regimens further encourage adoption. Emerging markets in India and Southeast Asia present new opportunities for this segment.

- By Treatment Type

On the basis of treatment type, the market is segmented into chemotherapy, radiation therapy, targeted therapy, immunotherapy, and others. The Targeted Therapy segment dominated the market in 2024 with a market share of 45.9% due to its personalized approach and high efficacy in NSCLC. Targeted therapies are increasingly preferred over traditional chemotherapy for specific patient populations with genetic mutations. Strong clinical data, growing physician awareness, and rising patient preference for less toxic treatments support dominance. Early adoption in hospitals and specialty clinics in China, Japan, and India contributes significantly to revenue. Targeted therapy also allows combination with immunotherapies to improve survival rates in advanced lung cancer. The segment is supported by reimbursement policies in key markets, enhancing accessibility and adoption.

The Immunotherapy segment is expected to witness the fastest growth from 2025 to 2032, driven by the increasing integration of checkpoint inhibitors into treatment protocols. Expanding approvals of PD-1/PD-L1 inhibitors and combination therapies are improving outcomes for advanced-stage lung cancer patients. Awareness campaigns, improved access to biologics, and increasing adoption in top hospitals across Asia-Pacific are fueling growth. Rapid technological advancements in immuno-oncology are enhancing patient outcomes and expanding applicability. Strong pipeline activity and collaborations between pharma companies and hospitals support adoption. Rising patient preference for less invasive therapies further accelerates market growth.

- By Therapy Type

On the basis of therapy type, the market is segmented into single drug therapy and combination therapy. The Single Drug Therapy segment dominated in 2024 due to widespread adoption of monotherapies such as EGFR inhibitors and standard chemotherapy. Single drug regimens are simpler to administer, have established dosing guidelines, and are cost-effective for hospital and outpatient use. Clinical familiarity and strong reimbursement frameworks in China, Japan, and India further strengthen market share. Hospitals often prioritize single drug therapy for early-stage patients. Monotherapy adoption remains strong due to ease of monitoring adverse events. Well-established treatment guidelines further support continued dominance.

The Combination Therapy segment is expected to witness the fastest CAGR from 2025 to 2032, driven by enhanced efficacy from combining targeted therapies with immunotherapy or chemotherapy. Combination therapy adoption is rising in tertiary hospitals and oncology centers to manage advanced-stage and refractory lung cancers. Growing clinical evidence supporting synergistic effects and patient outcomes accelerates adoption. The segment benefits from increasing approvals of combination regimens. Rising awareness among oncologists about multi-drug benefits further fuels growth. Integration with precision medicine approaches enhances personalized treatment efficacy.

- By End User

On the basis of end user, the market is segmented into hospitals, homecare, specialty clinics, and others. The Hospitals segment dominated in 2024 due to the high concentration of oncology specialists, availability of advanced diagnostics, and infrastructure for complex therapies. Hospitals remain the preferred point of care for advanced lung cancer treatment, offering chemotherapy, targeted therapy, and immunotherapy under expert supervision. Adoption is also driven by government reimbursement schemes and hospital procurement programs in major Asia-Pacific countries. Hospitals provide integrated patient care and monitoring for complex regimens. Their capability to conduct clinical trials further enhances market dominance. Established hospital networks facilitate adoption of advanced therapeutics efficiently.

The Specialty Clinics segment is expected to witness the fastest growth from 2025 to 2032, fueled by increasing outpatient oncology services and the rise of specialized cancer centers in urban areas. These clinics provide convenient access to targeted and combination therapies for patients seeking personalized care outside large hospital settings. Growing adoption of telemedicine platforms supports treatment monitoring. Specialty clinics also focus on patient-centric care, enhancing adherence. Rising investments in oncology infrastructure contribute to growth. The segment is increasingly preferred by younger, urban patients for its convenience and accessibility.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, online, and others. The Hospital Pharmacy segment dominated in 2024 due to direct supply of therapeutics for inpatient and outpatient treatments. Hospitals ensure proper handling, dosing, and monitoring of advanced therapies, making this channel preferred for high-cost drugs such as biologics and immunotherapies. Close coordination with physicians and hospital supply chains reinforces dominance. Hospital pharmacies also offer patient education on therapy administration. Integrated supply chains ensure timely drug availability and reduce wastage. Hospital pharmacies remain the primary choice for high-risk or advanced-stage patients.

The Online segment is expected to witness the fastest CAGR from 2025 to 2032, driven by digital health platforms, e-pharmacies, and telemedicine services that facilitate home delivery of oral targeted therapies. Growth is supported by patient preference for convenience, increasing smartphone penetration, and regulatory approvals for online drug dispensing in select Asia-Pacific countries. Online channels improve accessibility in remote regions. They also allow patients to maintain adherence to therapy schedules. Telehealth integration provides real-time guidance on drug administration. Rising trust in e-commerce platforms and improved logistics infrastructure further accelerate growth.

Asia-Pacific Lung Cancer Therapeutics Market Regional Analysis

- China dominated the Asia-Pacific Lung Cancer Therapeutics Market with the largest revenue share of 48.1% in 2024, characterized by high prevalence of lung cancer, strong government support for cancer care infrastructure, and a robust pipeline of novel drugs

- Patients and healthcare providers in the region increasingly prioritize personalized treatment approaches, including EGFR inhibitors, ALK inhibitors, and combination therapies, which are widely used in major hospitals and specialty oncology centers

- This widespread adoption is further supported by advanced healthcare infrastructure, increasing clinical research initiatives, and high patient awareness of early detection and precision medicine, establishing lung cancer therapeutics as a key oncology segment in China

The China Asia-Pacific Lung Cancer Therapeutics Market Insight

The China Asia-Pacific Lung Cancer Therapeutics Market captured the largest revenue share of 48.1% in 2024 within Asia-Pacific, fueled by the high prevalence of lung cancer and robust adoption of targeted therapies and immuno-oncology treatments. Patients and healthcare providers are increasingly prioritizing precision medicine, including EGFR and ALK inhibitors, for effective management of NSCLC and metastatic lung cancer. Government-supported screening programs, increasing awareness of early diagnosis, and strong healthcare infrastructure are driving widespread adoption across hospitals and specialty oncology centers. Moreover, ongoing clinical trials, drug approvals, and rising patient demand for personalized therapy are significantly contributing to market expansion. The integration of advanced diagnostics and treatment regimens in major hospitals further strengthens China’s dominance in the regional market.

Japan Asia-Pacific Lung Cancer Therapeutics Market Insight

The Japan Asia-Pacific Lung Cancer Therapeutics Market is experiencing steady growth due to rapid urbanization, a high incidence of lung cancer, and increasing awareness of precision medicine. Japanese healthcare providers are adopting advanced therapeutics, including targeted therapies and immunotherapies, integrated with molecular diagnostics for personalized treatment plans. The country’s technologically advanced healthcare infrastructure supports the implementation of novel drug regimens in both hospital and outpatient settings. In addition, the aging population is driving demand for safer, effective, and easier-to-administer lung cancer treatments. Ongoing R&D collaborations between pharmaceutical companies and hospitals further promote adoption. Government initiatives promoting early cancer detection and insurance coverage for advanced therapies also contribute to market growth.

India Asia-Pacific Lung Cancer Therapeutics Market Insight

The India Asia-Pacific Lung Cancer Therapeutics Market accounted for a significant revenue share in Asia-Pacific in 2024, driven by rising lung cancer incidence, rapid urbanization, and expanding healthcare access. Hospitals and specialty oncology clinics are increasingly adopting targeted and combination therapies to manage NSCLC and metastatic lung cancers. The government’s push towards early cancer screening programs and digital healthcare initiatives supports widespread adoption. Moreover, growing awareness among patients and caregivers about precision medicine and immunotherapy is boosting demand. Availability of affordable generic drugs and rising domestic pharmaceutical manufacturing capacity further enhance accessibility. Expansion of oncology centers in urban and semi-urban regions strengthens India’s market position in the Asia-Pacific region.

South Korea Asia-Pacific Lung Cancer Therapeutics Market Insight

The South Korea Asia-Pacific Lung Cancer Therapeutics Market is witnessing strong growth due to high lung cancer incidence and advanced healthcare infrastructure. Hospitals and specialty clinics are rapidly adopting targeted therapies, immunotherapies, and combination regimens for NSCLC and metastatic lung cancers. The country’s focus on precision medicine and biomarker-driven treatment strategies enables highly personalized care. Strong government support for oncology research, early screening programs, and insurance coverage for advanced drugs is further driving adoption. South Korea also benefits from active pharmaceutical R&D collaborations and the availability of innovative therapies. The rising patient awareness of treatment options and preference for advanced therapeutics are contributing to sustained market expansion.

Asia-Pacific Lung Cancer Therapeutics Market Share

The Asia-Pacific Lung Cancer Therapeutics industry is primarily led by well-established companies, including:

- AstraZeneca (U.K.)

- F. Hoffmann La Roche Ltd (Switzerland)

- Merck & Co., Inc. (U.S.)

- Bristol Myers Squibb Company (U.S.)

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Johnson & Johnson (U.S.)

- Boehringer Ingelheim International GmbH (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

- Amgen Inc. (U.S.)

- Sanofi (France)

- Astellas Pharma Inc. (Japan)

- Sun Pharmaceutical Industries Ltd (India)

- GSK plc (U.K.)

- AbbVie Inc. (U.S.)

- Daiichi Sankyo Company, Limited (Japan)

- Eli Lilly and Company (U.S.)

- Bayer AG (Germany)

- Exelixis, Inc. (U.S.)

What are the Recent Developments in Asia-Pacific Lung Cancer Therapeutics Market?

- In May 2024, Zai Lab announced approval of the New Drug Application (NDA) by China’s NMPA for Repotrectinib (Augtyro) for adult patients with locally advanced or metastatic NSCLC underscoring the expansion of ROS1/ALK targeting agents in China

- In March 2024, China’s NMPA accepted a supplemental New Drug Application (sNDA) for Savolitinib (Orpathys) to extend indication to treatment‑naïve or previously treated locally advanced/metastatic NSCLC patients with MET exon 14 skipping alterations signalling pipeline growth in Asia‑Pacific region for MET‑driven therapies

- In November 2023, the NMPA granted conditional marketing approval in China to Vebreltinib (APL‑101; PBL‑1001) for NSCLC patients harboring MET exon 14 skipping mutations marking another MET‑targeted therapy entry into China’s lung cancer therapeutics ecosystem

- In March 2023, the Gumarontinib (SCC244) received conditional approval from China’s National Medical Products Administration (NMPA) for the treatment of adult patients with locally advanced or metastatic Non‑Small Cell Lung Cancer (NSCLC) harboring MET exon 14 skipping mutations

- In December 2022, Durvalumab (Imfinzi) in combination with Tremelimumab (Imjudo) plus chemotherapy was approved in Japan by the Ministry of Health, Labour and Welfare (MHLW) for unresectable, advanced or recurrent NSCLC, expanding immunotherapy combinations in the Japanese lung cancer market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.