Asia Pacific Medical Equipment Maintenance Market

Market Size in USD Billion

USD

11.60 Billion

USD

24.24 Billion

2025

2033

USD

11.60 Billion

USD

24.24 Billion

2025

2033

| 2026 - 2033 | |

| USD 11.60 Billion | |

| USD 24.24 Billion | |

| % | |

|

Asia-Pacific Medical Equipment Maintenance Market Size

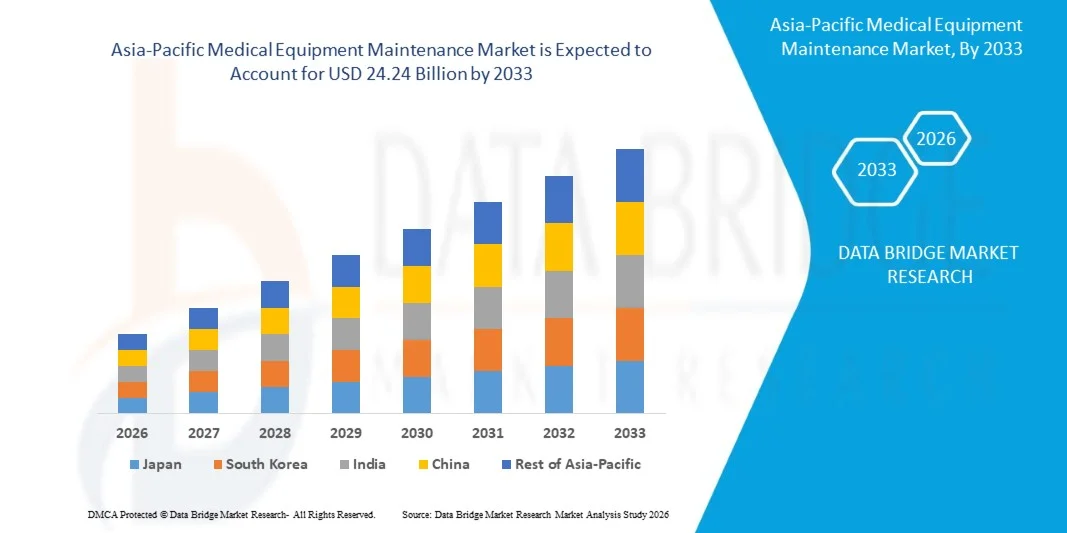

- The Asia-Pacific Medical Equipment Maintenance Market size was valued at USD 11.60 billion in 2025 and is expected to reach USD 24.24 billion by 2033, at a CAGR of 9.65% during the forecast period

- The market growth is largely fueled by the increasing demand for efficient maintenance and servicing of advanced medical equipment, driven by the rising adoption of technologically sophisticated devices across hospitals and diagnostic centers, which is leading to greater emphasis on equipment uptime and operational efficiency

- Furthermore, growing healthcare expenditure and the need to ensure patient safety and regulatory compliance are encouraging healthcare providers to adopt regular maintenance services, thereby strengthening the demand for reliable and cost-effective equipment maintenance solutions and supporting overall market expansion

Asia-Pacific Medical Equipment Maintenance Market Analysis

- Medical equipment maintenance, encompassing preventive, corrective, and operational services for a wide range of healthcare devices, is becoming a critical function within healthcare facilities to ensure accuracy, reliability, and continuous performance of diagnostic and therapeutic systems across clinical environments

- The increasing reliance on complex medical technologies, coupled with the rising burden of chronic diseases and expanding healthcare infrastructure, is significantly driving the demand for maintenance services as healthcare providers focus on minimizing downtime and extending the lifecycle of high-value medical equipment

- South Korea dominated the Asia-Pacific Medical Equipment Maintenance Market in 2025, due to its advanced healthcare infrastructure, high adoption of technologically sophisticated medical devices, and strong presence of leading medical equipment manufacturers

- Japan is expected to be the fastest growing country in the Asia-Pacific Medical Equipment Maintenance Market during the forecast period due to its aging population and increasing demand for advanced medical technologies across healthcare facilities

- Imaging equipment segment dominated the market with a market share of 39% in 2025, due to the high cost, complexity, and criticality of systems such as MRI, CT, and X-ray machines that require regular calibration and servicing to ensure accuracy and compliance. Healthcare facilities prioritize maintenance of imaging systems due to their continuous utilization in diagnostics and the need to avoid costly downtime

Report Scope and Asia-Pacific Medical Equipment Maintenance Market Segmentation

|

Attributes |

Medical Equipment Maintenance Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Asia-Pacific Medical Equipment Maintenance Market Trends

“Increasing Integration of Remote Monitoring and Connected Maintenance Solutions”

- A significant trend in the Asia-Pacific Medical Equipment Maintenance Market is the increasing integration of remote monitoring and connected maintenance solutions, driven by the growing need for real-time equipment performance tracking and proactive servicing across healthcare facilities. This integration is enhancing the efficiency of maintenance operations and reducing unexpected equipment failures in critical care environments

- For instance, GE HealthCare provides remote equipment monitoring and predictive maintenance solutions through its digital platforms, enabling hospitals to track device performance and schedule timely servicing. These capabilities improve equipment uptime and support continuous clinical operations without disruptions

- The adoption of connected maintenance technologies is expanding as healthcare providers seek to minimize downtime of high-value equipment such as imaging systems and life-support devices. This is strengthening the role of digital service platforms in ensuring uninterrupted healthcare delivery

- Hospitals are increasingly utilizing data-driven maintenance systems that leverage real-time analytics to detect performance issues before failure occurs. This shift is improving maintenance planning and reducing the risk of costly emergency repairs

- The growing reliance on integrated healthcare IT ecosystems is encouraging seamless connectivity between medical devices and maintenance systems. This is supporting centralized monitoring and efficient asset management across multiple facilities

- The market is witnessing strong momentum toward predictive and remote servicing models that enhance operational efficiency, reduce maintenance costs, and ensure compliance with healthcare quality standards, reinforcing the importance of connected maintenance solutions in modern healthcare infrastructure

Asia-Pacific Medical Equipment Maintenance Market Dynamics

Driver

“Growing Installed Base of Complex and High-Value Medical Equipment”

- The increasing installation of complex and high-value medical equipment across hospitals and diagnostic centers is driving the demand for specialized maintenance services to ensure optimal performance and longevity of these assets. Advanced systems require regular servicing to maintain accuracy and support critical healthcare procedures

- For instance, Siemens Healthineers AG offers comprehensive maintenance services for imaging systems such as MRI and CT scanners, ensuring consistent performance and compliance with clinical standards. These services help healthcare providers maintain diagnostic precision and reduce operational risks

- The rapid expansion of healthcare infrastructure is contributing to a larger installed base of sophisticated devices that require continuous monitoring and maintenance. This is increasing reliance on professional service providers for equipment upkeep

- The growing use of technologically advanced diagnostic and therapeutic equipment is elevating the need for preventive and corrective maintenance solutions. This is ensuring reliability and minimizing disruptions in patient care delivery

- The sustained increase in demand for advanced medical technologies and the need to ensure their efficient functioning are collectively driving the growth of maintenance services, positioning them as essential components of healthcare operations

Restraint/Challenge

“Stringent Regulatory Compliance and Quality Standards”

- The Asia-Pacific Medical Equipment Maintenance Market faces challenges due to stringent regulatory compliance and quality standards that govern the servicing and calibration of healthcare devices. These regulations require adherence to strict protocols, increasing operational complexity for service providers

- For instance, U.S. Food and Drug Administration enforces rigorous guidelines for the maintenance and performance validation of medical devices, requiring service providers to meet detailed compliance requirements. These regulations ensure patient safety but add to the burden of documentation and procedural accuracy

- Maintenance activities must comply with strict certification and quality assurance processes to ensure equipment reliability and clinical safety. This increases the need for skilled personnel and specialized training programs

- The requirement to maintain detailed service records and follow standardized procedures adds administrative complexity and extends service timelines. This can impact operational efficiency and increase overall maintenance costs

- The need to consistently meet evolving regulatory standards while maintaining service efficiency continues to restrain market growth, placing pressure on providers to balance compliance, cost, and operational effectiveness

Asia-Pacific Medical Equipment Maintenance Market Scope

The market is segmented on the basis of device type, service type, service provider, and end user.

• By Device Type

On the basis of device type, the Asia-Pacific Medical Equipment Maintenance Market is segmented into imaging equipment, endoscopic device, surgical instrument, electro-medical equipment, dental equipment, and life support devices. The imaging equipment segment dominated the market with the largest revenue share of 39% in 2025, driven by the high cost, complexity, and criticality of systems such as MRI, CT, and X-ray machines that require regular calibration and servicing to ensure accuracy and compliance. Healthcare facilities prioritize maintenance of imaging systems due to their continuous utilization in diagnostics and the need to avoid costly downtime. The segment benefits from stringent regulatory requirements and the necessity for precision in diagnostic outcomes, further strengthening demand for routine servicing and upgrades.

The life support devices segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the increasing adoption of critical care equipment such as ventilators, infusion pumps, and patient monitoring systems across hospitals and emergency care units. These devices are essential for patient survival, requiring continuous monitoring, preventive maintenance, and rapid servicing to avoid malfunctions. The rising prevalence of chronic diseases and expanding ICU infrastructure are further accelerating demand for maintenance services in this segment, supported by advancements in connected and remote monitoring technologies.

• By Service Type

On the basis of service type, the Asia-Pacific Medical Equipment Maintenance Market is segmented into preventive maintenance, corrective maintenance, and operational maintenance. The preventive maintenance segment held the largest market revenue share in 2025 driven by the growing emphasis on minimizing equipment downtime and ensuring compliance with healthcare safety standards. Healthcare providers increasingly adopt scheduled servicing and inspection programs to extend equipment lifespan and reduce unexpected breakdowns. Preventive maintenance also supports cost optimization by identifying potential failures early, thereby avoiding expensive repairs and operational disruptions in critical care environments.

The corrective maintenance segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising complexity of advanced medical devices and the need for immediate repair services in case of equipment failure. Hospitals and diagnostic centers rely on rapid corrective interventions to maintain continuity in patient care and avoid delays in treatment procedures. Increasing integration of sophisticated electronics and software in medical equipment further drives demand for specialized repair services, ensuring accurate restoration of functionality in critical systems.

• By Service Provider

On the basis of service provider, the Asia-Pacific Medical Equipment Maintenance Market is segmented into original equipment manufacturers, independent service organizations, and in-house maintenance. The original equipment manufacturers segment dominated the market with the largest revenue share in 2025, driven by their expertise, access to proprietary technology, and ability to provide certified and high-quality maintenance services. Healthcare institutions often prefer OEM services to ensure compliance with manufacturer standards and maintain warranty coverage. The availability of advanced diagnostic tools and trained personnel further strengthens the position of OEMs in delivering reliable and efficient maintenance solutions.

The independent service organizations segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by their cost-effective service offerings and flexibility in catering to multi-brand equipment maintenance. ISOs are gaining traction among small and medium healthcare providers seeking affordable alternatives to OEM services without compromising on service quality. The growing demand for customized maintenance contracts and quicker response times further supports the expansion of independent service providers in the market.

• By End User

On the basis of end user, the Asia-Pacific Medical Equipment Maintenance Market is segmented into private-sector organizations and public-sector organizations. The private-sector organizations segment held the largest market revenue share in 2025 driven by higher healthcare spending, advanced infrastructure, and rapid adoption of technologically sophisticated medical equipment. Private hospitals and diagnostic centers prioritize regular maintenance services to ensure operational efficiency, patient safety, and brand reputation. The increasing focus on quality healthcare delivery and accreditation standards further strengthens the demand for comprehensive maintenance solutions in this segment.

The public-sector organizations segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising government investments in healthcare infrastructure and the expansion of public hospitals and medical facilities. Governments are increasingly focusing on improving healthcare accessibility and service quality, leading to higher procurement of medical equipment and associated maintenance services. The implementation of large-scale healthcare programs and modernization initiatives further accelerates the demand for structured maintenance frameworks in public healthcare systems.

Asia-Pacific Medical Equipment Maintenance Market Regional Analysis

- South Korea dominated the Asia-Pacific Medical Equipment Maintenance Market with the largest revenue share in 2025, driven by its advanced healthcare infrastructure, high adoption of technologically sophisticated medical devices, and strong presence of leading medical equipment manufacturers

- The country’s well-established hospital network, supported by significant investments in digital healthcare systems and stringent regulatory standards for equipment performance and safety, reinforces consistent demand for maintenance services across diagnostic and therapeutic applications

- The presence of skilled service providers, increasing integration of smart and connected medical devices, and rising focus on preventive maintenance strategies further strengthen South Korea’s dominant position during the forecast period. Growing demand for high-quality healthcare services and continuous technological upgrades in hospitals support sustained market expansion

Japan Asia-Pacific Medical Equipment Maintenance Market Insight

The Japan market is anticipated to grow at the fastest CAGR from 2026 to 2033, supported by its aging population and increasing demand for advanced medical technologies across healthcare facilities. The country’s strong emphasis on precision, quality standards, and regular equipment servicing drives the adoption of comprehensive maintenance solutions. Rising investments in hospital modernization and the expansion of diagnostic capabilities are further accelerating demand. The adoption of predictive and remote maintenance technologies is gaining traction, improving operational efficiency and reducing equipment downtime. Japan’s focus on innovation and reliability positions it as the fastest-growing market in the region.

India Asia-Pacific Medical Equipment Maintenance Market Insight

India is projected to witness significant growth in the Asia-Pacific Medical Equipment Maintenance Market during 2026–2033, fueled by expanding healthcare infrastructure and increasing investments in both public and private healthcare sectors. The rising adoption of advanced medical devices across hospitals and diagnostic centers is driving demand for reliable maintenance services. Growing awareness regarding equipment efficiency, patient safety, and regulatory compliance is further supporting market expansion. The rapid growth of multi-specialty hospitals and diagnostic chains is enhancing service demand across urban and semi-urban areas. Government initiatives to strengthen healthcare systems and improve accessibility continue to boost market development across the country.

Asia-Pacific Medical Equipment Maintenance Market Share

The medical equipment maintenance industry is primarily led by well-established companies, including:

- Medtronic (U.S.)

- Stryker (U. S.)

- Siemens Healthineers AG (Germany)

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (The Netherlands)

- Canon Medical Systems Corporation (Japan)

- Hitachi High-Tech Corporation (Japan)

- Fujifilm Holdings Corporation (Japan)

- Shimadzu Corporation (Japan)

- Agfa-Gevaert N.V. (Belgium)

- Drägerwerk AG & Co. KGaA (Germany)

- Carestream Health (U.S.)

- Aramark (U.S.)

- Crothall Healthcare (U.S.)

- Alpha Source Group (U.S.)

- Alliance Medical Limited (U.K.)

- Althea Group Holdings Limited (Austraila)

- Pantheon Healthcare (U.K.)

Latest Developments in Asia-Pacific Medical Equipment Maintenance Market

- In November 2024, Medline Industries, a leading medical supply firm, confidentially filed for an initial public offering (IPO) in the U.S., aiming to raise over USD 5 billion. The IPO, expected as early as the second quarter of 2025, could value the company at approximately USD 50 billion, marking a significant move for its private equity owners. This development reflects strong investor confidence in the healthcare supply chain sector and is expected to support Medline’s expansion, including investments in distribution networks and advanced medical equipment service capabilities

- In August 2024, Getinge acquired U.S.-based organ transport company Paragonix Technologies for approximately USD 477 million. This strategic move aims to enhance Getinge's offerings in the organ transplant sector by integrating Paragonix's advanced organ preservation solutions. The acquisition strengthens Getinge’s portfolio in critical care and life sciences, enabling improved efficiency and reliability in organ transportation, which is closely linked to the performance and maintenance of specialized medical equipment

- In July 2024, Owens & Minor, a medical supplies distributor, announced its agreement to acquire Rotech Healthcare for USD 1.36 billion in cash. This strategic move aims to expand Owens & Minor's presence in the home-based care sector, enhancing its portfolio with Rotech's offerings, including devices for sleep apnea and diabetes treatments. The acquisition reflects the growing demand for home healthcare equipment and associated maintenance services, driven by the shift toward decentralized and patient-centric care models

- In April 2024, Ecolab announced the sale of its global surgical solutions business to Medline for USD 950 million in cash. This unit, which generated over USD 400 million in sales the previous year, provides sterile drape solutions for surgical settings. The divestiture is part of Ecolab's strategy to focus on its core healthcare offerings, while enabling Medline to strengthen its surgical product portfolio and expand its integrated service capabilities within hospital environments

- In January 2024, Siemens Healthineers announced the expansion of its digital solutions for medical equipment maintenance. The new service integrates artificial intelligence and predictive analytics to minimize downtime and enhance the operational efficiency of medical equipment in hospitals. This advancement supports proactive maintenance strategies, improves asset utilization, and aligns with the broader industry trend toward smart healthcare infrastructure and data-driven service models

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Asia Pacific Medical Equipment Maintenance Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Asia Pacific Medical Equipment Maintenance Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Asia Pacific Medical Equipment Maintenance Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.