Asia Pacific Medical Robots Market

Market Size in USD Billion

USD

3.21 Billion

USD

11.27 Billion

2025

2033

USD

3.21 Billion

USD

11.27 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.21 Billion | |

| USD 11.27 Billion | |

| % | |

|

Asia-Pacific Medical Robots Market Overview

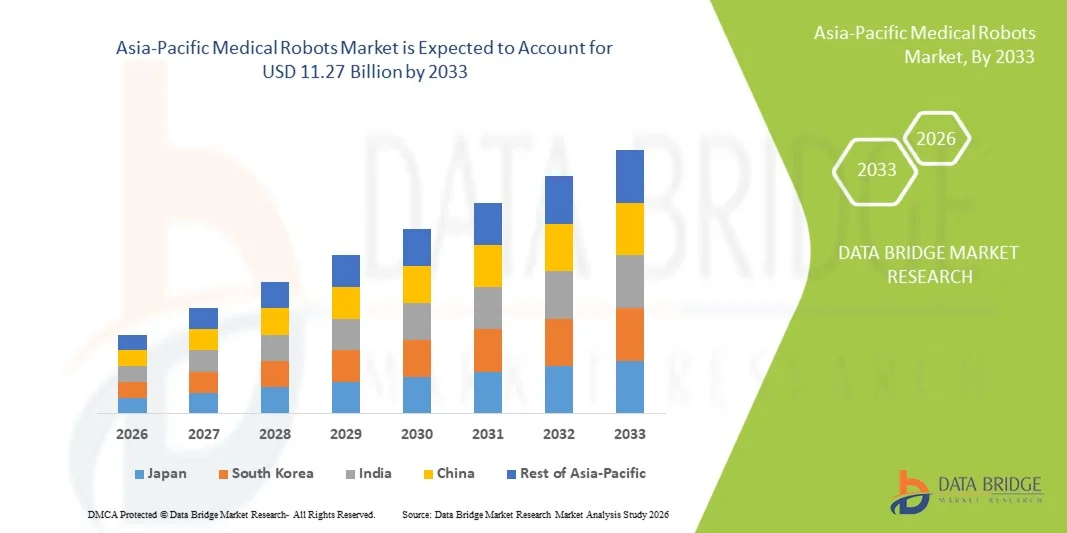

The Asia-Pacific medical robots market was valued at USD 3.21 billion in 2025 and is projected to reach USD 11.27 billion by 2033, growing at a CAGR of 17.0% from 2026 to 2033. The market is witnessing robust growth driven by rising demand for minimally invasive surgical procedures, rapidly aging populations across key economies, and continuous advancements in robotic-assisted medical technologies. The growing prevalence of chronic diseases, increasing healthcare expenditure, and expanding hospital infrastructure are further accelerating market expansion across the region.

The high burden of acute and chronic conditions, along with government initiatives supporting healthcare modernization and medical device innovation, is encouraging hospitals and surgical centers to adopt advanced robotic systems. In addition, innovations in AI-enhanced surgical platforms, micro-robotic devices, and rehabilitation robotics are improving treatment outcomes and patient recovery times, supporting widespread adoption across hospitals, rehabilitation centers, and specialty clinics throughout Asia-Pacific.

Key Market Trends & Insights

- Asia-Pacific held a significant revenue share of 24.8% in the global medical robots market in 2025, supported by rapidly expanding healthcare infrastructure, strong government investment in medical technology, and the presence of leading robotics manufacturers in Japan, China, and South Korea.

- The Surgical Robots segment led the market with a 64.2% share in 2025, driven by increasing demand for precision-based minimally invasive procedures, continuous technological advancements in robotic-assisted surgery platforms, and growing adoption across urology, orthopedics, and general surgery applications.

- Rehabilitation Robots are the fastest-growing product segment, projected to register a CAGR of 19.8%, supported by aging demographics, rising incidence of stroke and musculoskeletal disorders, and increasing investment in post-operative and chronic care rehabilitation infrastructure.

- The Hospitals segment dominated the end-user category with a revenue share of 58.6% in 2025, driven by high procedural volumes, availability of specialized surgical teams, and increasing capital investment in robotic surgical systems across tertiary care facilities.

- Clinic applications dominated the application segment with the highest revenue share in 2025, as outpatient surgical centers and specialty clinics increasingly adopt compact robotic systems for minimally invasive interventions.

- Direct Tender dominated the distribution channel segment in 2025, as government healthcare procurement programs and large hospital networks leverage centralized purchasing to acquire high-value medical robotic systems.

- The Compact modality segment held a dominant market share of 71.4% in 2025, driven by space constraints in clinical settings and growing preference for versatile, footprint-efficient robotic platforms suitable for multi-specialty deployment.

Market Size & Forecast

- Asia-Pacific Market Value (2025): USD 3.21 Billion

- Expected Market Value (2033): USD 11.27 Billion

- Forecast CAGR (2026–2033): 17.0%

Report Scope and Asia-Pacific Medical Robots Market Segmentation

|

Attributes |

Driving Simulators Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific |

|

Key Market Players |

· Intuitive Surgical, Inc. (U.S.) · Medtronic plc (Ireland) · Stryker Corporation (U.S.) · Smith + Nephew (U.K.) · Zimmer Biomet Holdings, Inc. (U.S.) · Johnson & Johnson and its affiliates (U.S.) · Siemens Healthineers AG (Germany) · TINAVI Medical Technologies Co., Ltd. (China) · Meere Company Inc. (South Korea) · Medicaroid Corporation (Japan) · CMR Surgical Ltd. (U.K.) · Renishaw plc (U.K.) · Accuray Incorporated (U.S.) · Hocoma AG (Switzerland) · ReWalk Robotics Ltd. (Israel) · Ekso Bionics Holdings, Inc. (U.S.) |

|

Market Opportunities |

· Expansion of domestically manufactured low-cost surgical robotic platforms for emerging healthcare markets · Increasing adoption of AI-powered autonomous surgical systems and micro-robotic diagnostic devices |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Asia-Pacific Medical Robots Market Trends

Trend: Rising Adoption of AI-Enhanced Surgical Robotic Systems in Asia-Pacific

The growing integration of artificial intelligence and machine learning technologies into surgical robotic platforms is emerging as a major trend in the Asia-Pacific medical robots market. Healthcare providers and device manufacturers are increasingly leveraging AI-powered systems to enhance surgical precision, improve decision-making during complex procedures, and reduce operative complications — all without relying on traditional, manual surgical techniques. The deployment of AI-driven surgical robots is helping hospitals and surgical centers expand access to advanced interventions, reduce procedure times, and deliver more consistent patient outcomes across both urban and underserved healthcare settings.

For instance, in February 2026, Medicaroid Corporation announced the deployment of its hinotori Surgical Robot System integrated with AI-assisted motion guidance in over 50 hospitals across Japan, enabling surgeons to perform complex laparoscopic procedures with enhanced precision and reduced learning curves.

In addition, according to research published by Johns Hopkins Engineering for Professionals, AI-driven autonomous surgical systems are being developed to enable robots to "think and act autonomously," significantly improving safety, precision, and recovery times for patients undergoing robotic-assisted surgery. Furthermore, the rising incidence of chronic diseases and the growing demand for minimally invasive surgical interventions are collectively accelerating the adoption of AI-enhanced medical robots across hospitals, ambulatory surgical centers, and specialty clinics throughout Asia-Pacific.

Asia-Pacific Medical Robots Market Dynamics

Key Market Driver: Rapidly Aging Population and Rising Prevalence of Chronic Diseases

The rapidly aging population and rising prevalence of chronic diseases are significantly driving demand for medical robotic solutions across Asia-Pacific. Hospitals, rehabilitation centers, and specialty clinics are investing heavily in next-generation surgical robots, rehabilitation robotics, and assistive devices to support precision-based interventions and post-operative recovery for elderly and chronically ill patients. Increasing adoption of minimally invasive robotic surgery, AI-driven diagnostic platforms, and soft robotic exosuits is further accelerating demand for advanced medical robotic systems capable of addressing complex clinical needs.

For instance,

According to BIS Research, the Asia-Pacific surgical robots market was valued at USD 4.6 billion in 2018 and is forecast to exceed USD 8.49 billion by 2025, driven by the rising aging population, increasing cases of acute and chronic diseases, and better benefits to patients and surgeons from robotic-assisted procedures.

Key Restraint/Challenge: High Capital Investment and Limited Reimbursement Coverage

A major challenge in the Asia-Pacific medical robots market is the high capital investment associated with acquiring and maintaining advanced robotic surgical systems. Premium medical robotic platforms involving AI-enhanced surgical consoles, patient carts, and proprietary software entail substantial upfront expenditure. In addition, inconsistent reimbursement policies, limited insurance coverage for robotic-assisted procedures, and high operational costs create barriers to widespread adoption across cost-sensitive healthcare systems.

For instance,

The average cost of a da Vinci Surgical System ranges between USD 1.5 million and USD 2 million per unit, with additional annual service and maintenance expenses, restricting access for many hospitals and surgical centers in emerging Asia-Pacific markets.

Key Market Opportunity: Expansion of Domestically Manufactured Low-Cost Surgical Robots

The increasing investment in domestically manufactured low-cost surgical robotic platforms presents significant opportunities for the Asia-Pacific medical robots market. Growing efforts by manufacturers in China, South Korea, and Japan to develop affordable robotic systems are enabling wider distribution of access to surgical interventions for populations with the greatest need. Democratization of operating rooms through localized production is improving treatment accessibility, reducing procurement costs, and reaching previously underserved patient populations across the region.

For instance,

In March 2026, Meere Company Inc. announced the commercial launch of its Revo-i robotic surgical system in Southeast Asian markets, offering a cost-effective alternative to Western surgical robots and expanding access to robotic-assisted surgery across hospitals in Thailand, Indonesia, and Vietnam.

Asia-Pacific Medical Robots Market Scope

The Asia-Pacific medical robots market is segmented on the basis of type, product, modality, components, application, end user, and distribution channel.

- By Type

On the basis of type, the Asia-Pacific medical robots market is segmented into external large robots, geriatric robots, assistive robots, and miniature in vivo robots. The external large robots segment held the largest market share of 52.3% in 2025, owing to their widespread deployment in surgical suites for complex orthopedic, neurological, and cardiovascular procedures. Increasing adoption of multi-arm robotic platforms and AI-enhanced navigation systems by tertiary care hospitals has further strengthened segment dominance across Asia-Pacific.

The miniature in vivo robots segment is expected to witness the fastest CAGR of 21.4% over the forecast period, driven by their ability to navigate internal body cavities for targeted drug delivery, minimally invasive diagnostics, and precision microsurgery. Growing investment in micro-robotic research and commercialization by leading academic institutions and medical device companies is further accelerating adoption of miniature robotic systems in clinical applications.

- By Product

On the basis of product, the Asia-Pacific medical robots market is segmented into surgical robots, rehabilitation robots, hospital and pharmacy robots, bio robotics, non-invasive radio surgery robots, telepresence robots, medical transportation robots, and sanitation and disinfectant robots. The surgical robots segment accounted for the highest market share of 64.2% in 2025, driven by growing demand for minimally invasive surgical procedures, enhanced precision, and improved patient outcomes across urology, orthopedics, and general surgery applications.

The rehabilitation robots segment is anticipated to show the fastest growth at a CAGR of 19.8% over the forecast period, fueled by rapidly aging demographics, rising incidence of stroke and neurodegenerative disorders, and increasing investment in post-operative and chronic care rehabilitation infrastructure across hospitals and rehabilitation centers in Asia-Pacific.

- By Modality

On the basis of modality, the Asia-Pacific medical robots market is segmented into compact and portable. The compact modality segment accounts for 71.4% of the total market share, as hospitals and surgical centers increasingly prioritize space-efficient robotic platforms suitable for multi-specialty deployment across operating rooms and outpatient settings.

The portable segment is expected to witness the fastest CAGR of 22.6% over the forecast period, driven by growing demand for mobile robotic systems in rural healthcare settings, home-based rehabilitation applications, and telepresence-enabled remote consultations across underserved regions in Asia-Pacific.

- By Components

On the basis of components, the Asia-Pacific medical robots market is segmented into actuators, sensors, robot controller, patient cart, surgeon console, vision cart, dispensing system, and additional products. The surgeon console segment held the largest market share of 28.7% in 2025, as it serves as the primary interface for robotic-assisted surgical procedures, integrating advanced visualization, haptic feedback, and AI-enhanced guidance systems.

The sensors segment is expected to witness the fastest CAGR of 20.2% over the forecast period, driven by increasing integration of force-sensing, motion-tracking, and real-time imaging technologies into next-generation medical robotic platforms to enhance surgical precision and patient safety. These advanced sensors enable accurate instrument positioning, improved navigation, and real-time feedback during procedures, reducing the risk of errors and complications. Growing demand for intelligent robotic systems, coupled with continuous technological advancements in sensor technologies and image-guided surgery, is further accelerating segment growth across healthcare facilities.

- By Application

On the basis of application, the Asia-Pacific medical robots market is segmented into research, clinic, pharmacy, and others. The clinic segment accounts for the majority of the total market share at 48.6%, as outpatient surgical centers and specialty clinics increasingly adopt compact robotic systems for minimally invasive interventions, diagnostic procedures, and rehabilitation therapies.

The pharmacy segment is expected to witness the fastest CAGR of 23.1% over the forecast period, driven by growing adoption of automated dispensing systems, inventory management robots, and AI-powered medication verification platforms across hospital pharmacies and retail pharmacy chains in Asia-Pacific. These technologies help reduce medication errors, improve dispensing accuracy, optimize inventory control, and enhance operational efficiency. Rising prescription volumes, increasing healthcare digitalization, and growing investments in pharmacy automation solutions are further accelerating segment growth across the region.

- By End User

On the basis of end user, the Asia-Pacific medical robots market is segmented into hospitals, specialty clinics, research institutes, ambulatory surgical centers, laboratories, rehabilitation centers, and others. Hospitals held a 58.6% share in 2025, leveraging clinical expertise, advanced surgical suites, and integrated robotic platforms to deliver comprehensive patient care across multiple medical specialties.

The ambulatory surgical centers segment is expected to grow at a CAGR of 19.4%, driven by increasing patient preference for outpatient procedures, lower procedural costs, and growing adoption of compact robotic surgical systems designed for high-volume, same-day surgical interventions. These facilities offer shorter hospital stays, faster recovery times, and improved operational efficiency compared to traditional inpatient settings. Technological advancements in minimally invasive robotic surgery, coupled with increasing healthcare cost-containment efforts and expanding availability of specialized outpatient surgical services, are further supporting robust segment growth.

- By Distribution Channel

On the basis of distribution channel, the Asia-Pacific medical robots market is segmented into direct tender, retail sales, third party distributors, and others. The direct tender channel dominated the market with a 54.8% revenue share in 2025, driven by government healthcare procurement programs, centralized hospital purchasing networks, and manufacturer partnerships with large tertiary care facilities across Asia-Pacific.

The third party distributors segment is anticipated to witness the fastest CAGR of 18.7% during the forecast period, driven by expanding regional distribution networks, growing demand from mid-sized hospitals and specialty clinics, and increasing penetration of medical robotic systems into emerging healthcare markets across Southeast Asia and South Asia.

Asia-Pacific Medical Robots Market Regional Analysis

Asia-Pacific is expected to grow at the fastest CAGR of 17.0% in the global medical robots market during the forecast period 2026–2033, supported by rapidly expanding healthcare infrastructure, rising demand for minimally invasive surgical procedures, and the growing presence of domestic medical robotics manufacturers in China, Japan, and South Korea. The region also benefits from strong government initiatives supporting healthcare modernization, increasing healthcare expenditure, and rising adoption of AI-enhanced surgical platforms and rehabilitation robotics across hospitals, specialty clinics, and rehabilitation centers.

China Medical Robots Market Insight

The China medical robots market is anticipated to grow at a CAGR of 18.4% between 2026 and 2033. The country's rapidly expanding healthcare infrastructure, along with increasing government investment in medical device innovation and AI-driven surgical technologies, is driving demand across surgical, rehabilitation, and pharmacy automation applications. In addition, growing awareness of the clinical benefits of robotic-assisted surgery — including enhanced precision, reduced recovery times, and improved patient outcomes — is accelerating medical robot adoption among hospitals and surgical centers nationwide.

Japan Medical Robots Market Insight

The Japan medical robots market, growing at a CAGR of 15.6% from 2026 to 2033, remains a major contributor to regional revenue, driven by advanced healthcare technology adoption, strong government support for medical robotics research, and the presence of leading domestic manufacturers. Japan is one of the most advanced countries in terms of surgical robotics deployment and rehabilitation robotics innovation, with high awareness regarding the effectiveness and success of robotic-assisted medical interventions among the Japanese population, further supporting steady market expansion.

South Korea Medical Robots Market Insight

The South Korea medical robots market is expected to grow at a CAGR of 16.2% from 2026 to 2033, driven by strong domestic robotics manufacturing capabilities, increasing adoption of minimally invasive surgical procedures, and government initiatives supporting medical device exports. The country's focus on developing cost-effective surgical robotic platforms for global markets is further strengthening its position as a key player in the Asia-Pacific medical robots ecosystem.

Asia-Pacific Medical Robots Market Share

The Asia-Pacific Medical Robots industry is primarily led by well-established companies, including:

- Intuitive Surgical, Inc. (U.S.)

- Medtronic plc (Ireland)

- Stryker Corporation (U.S.)

- Smith + Nephew plc (U.K.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Johnson & Johnson and its affiliates (U.S.)

- Siemens Healthineers AG (Germany)

- TINAVI Medical Technologies Co., Ltd. (China)

- Meere Company Inc. (South Korea)

- Medicaroid Corporation (Japan)

- CMR Surgical Ltd. (U.K.)

- Renishaw plc (U.K.)

- Accuray Incorporated (U.S.)

- Hocoma AG (Switzerland)

- ReWalk Robotics Ltd. (Israel)

- Ekso Bionics Holdings, Inc. (U.S.)

Latest Developments in Asia-Pacific Medical Robots Market

- In April 2026, Meere Company Inc. announced the successful deployment of its Revo-i robotic surgical system in over 30 hospitals across Southeast Asia, marking a significant expansion milestone in the company's strategy to challenge global surgical robotics leaders with cost-effective, locally manufactured robotic platforms.

- In March 2026, TINAVI Medical Technologies Co., Ltd. received regulatory approval from China's National Medical Products Administration (NMPA) for its next-generation orthopedic surgical robot featuring AI-enhanced navigation and real-time imaging integration, expanding the company's product portfolio for minimally invasive spine and joint replacement procedures.

- In February 2026, Medicaroid Corporation announced a strategic partnership with major Japanese hospital networks to deploy hinotori Surgical Robot Systems integrated with AI-assisted motion guidance across 50 additional facilities, accelerating adoption of robotic-assisted laparoscopic surgery throughout Japan.

- In January 2026, CMR Surgical Ltd. announced the installation of its Versius Surgical Robotic System in leading hospitals across India and Australia, expanding access to minimal access surgery in underserved Asia-Pacific markets and reinforcing the company's commitment to democratizing robotic surgery globally.

- In November 2025, Johnson & Johnson MedTech announced the expansion of its MONARCH platform for robotic-assisted bronchoscopy across select hospitals in China and South Korea, advancing minimally invasive lung cancer diagnosis capabilities in the Asia-Pacific region.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.