Asia Pacific Negative Pressure Wound Therapy Devices Market

Market Size in USD Million

USD

753.50 Million

USD

1,131.20 Million

2025

2033

USD

753.50 Million

USD

1,131.20 Million

2025

2033

| 2026 - 2033 | |

| USD 753.50 Million | |

| USD 1,131.20 Million | |

| % | |

|

Asia-Pacific Negative Pressure Wound Therapy Devices Market Size

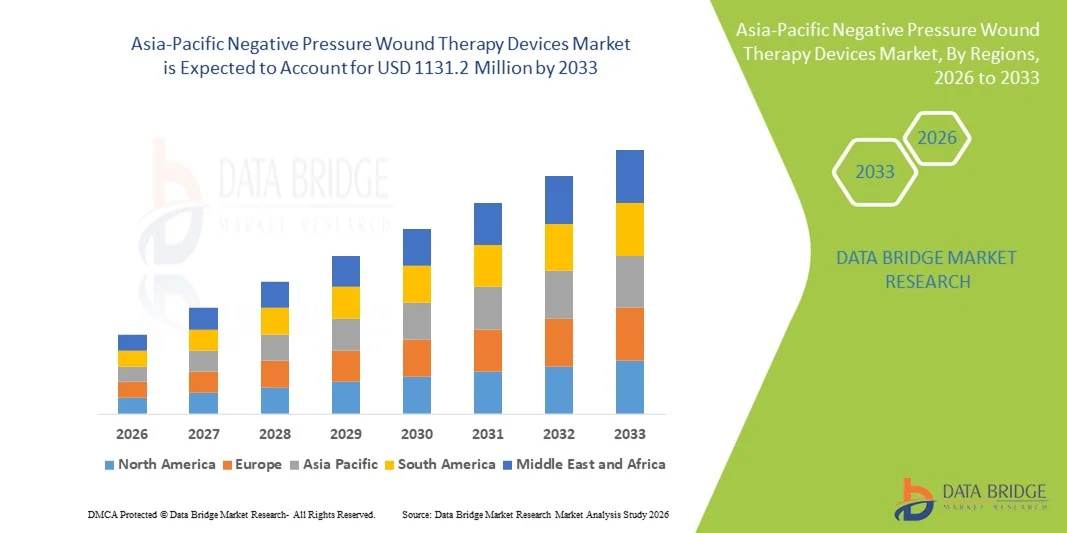

- The Asia-Pacific negative pressure wound therapy devices market size was valued at USD 753.50 Million in 2025 and is expected to reach USD 1131.2 Million by 2033, at a CAGR of 5.21% during the forecast period

- The market growth is largely fueled by the rising prevalence of chronic wounds such as diabetic foot ulcers, pressure ulcers, and venous leg ulcers, along with the increasing number of surgical procedures worldwide. Continuous technological advancements in portable and single-use negative pressure wound therapy (NPWT) systems are further supporting broader adoption across hospitals and homecare settings

- Furthermore, growing awareness about advanced wound care management, increasing geriatric population, and the proven clinical benefits of NPWT devices in accelerating healing, reducing infection risk, and shortening hospital stays are establishing Negative Pressure Wound Therapy devices as a preferred treatment option. These converging factors are accelerating the uptake of Negative Pressure Wound Therapy Devices solutions, thereby significantly boosting the industry’s growth

Asia-Pacific Negative Pressure Wound Therapy Devices Market Analysis

- Negative Pressure Wound Therapy (NPWT) devices, which apply controlled sub-atmospheric pressure to promote wound healing, are increasingly vital in modern wound care management across hospitals, outpatient centers, and homecare settings due to their effectiveness in accelerating tissue granulation, reducing edema, and lowering infection risk

- The escalating demand for NPWT devices is primarily fueled by the rising prevalence of chronic wounds such as diabetic foot ulcers and pressure ulcers, increasing surgical procedures, growing geriatric population, and expanding awareness regarding advanced wound care therapies

- China dominated the Negative Pressure Wound Therapy Devices market with the largest revenue share of 36.9% in 2025, driven by a large patient pool suffering from chronic wounds, expanding hospital infrastructure, increasing healthcare expenditure, and growing adoption of advanced wound care technologies across urban healthcare facilities

- India is expected to be the fastest-growing region in the Negative Pressure Wound Therapy Devices market during the forecast period, expanding at a CAGR of 10.8% from 2026 to 2033, supported by improving access to advanced medical devices, rising incidence of diabetes-related wounds, and increasing government focus on strengthening healthcare infrastructure

- The re-usable device segment held the largest market revenue share of 58.4% in 2025, attributed to its long-term cost efficiency in hospital settings

Report Scope and Negative Pressure Wound Therapy Devices Market Segmentation

|

Attributes |

Negative Pressure Wound Therapy Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Asia-Pacific Negative Pressure Wound Therapy Devices Market Trends

Advancements in Portable and Single-Use NPWT Systems

- A significant and accelerating trend in the global Negative Pressure Wound Therapy Devices market is the increasing shift toward portable, lightweight, and single-use NPWT systems that enable greater patient mobility and home-based care. These innovations are transforming wound management practices by reducing hospital stays and improving patient comfort

- For instance, in 2023, 3M expanded its V.A.C. therapy portfolio with single-use NPWT systems designed for outpatient and homecare settings, enabling effective wound healing while minimizing the need for prolonged hospitalization

- The growing preference for outpatient surgical procedures and home healthcare services is encouraging manufacturers to design compact and user-friendly NPWT devices that are easy to operate for both clinicians and patients

- Technological improvements in canister-free systems, quieter pumps, and extended battery life are enhancing device convenience and compliance, making NPWT more accessible across diverse care environments

- Increasing focus on infection control and faster wound closure rates is further driving the adoption of advanced NPWT systems in both acute and chronic wound management applications

Asia-Pacific Negative Pressure Wound Therapy Devices Market Dynamics

Driver

Rising Prevalence of Chronic Wounds and Surgical Procedures

- The increasing prevalence of chronic wounds such as diabetic foot ulcers, pressure ulcers, and venous leg ulcers is a primary driver of the Negative Pressure Wound Therapy Devices market. Growing cases of diabetes, obesity, and cardiovascular diseases are contributing significantly to wound incidence globally

- For instance, Smith+Nephew’s PICO single-use NPWT system has been widely adopted in post-surgical wound management and diabetic ulcer treatment, demonstrating improved healing outcomes and reduced risk of surgical site infections

- The rising number of surgical procedures worldwide, particularly orthopedic, cardiovascular, and cosmetic surgeries, is increasing demand for NPWT devices to reduce complications and accelerate recovery

- Expanding geriatric populations, who are more prone to slow-healing wounds and chronic conditions, are further contributing to sustained market demand

- Increased awareness among healthcare professionals regarding the clinical benefits of NPWT, including reduced infection rates, faster granulation tissue formation, and shorter hospital stays, is supporting broader adoption

Restraint/Challenge

High Treatment Costs and Limited Accessibility

- The high cost of NPWT devices and associated consumables, including dressings and canisters, remains a significant barrier to widespread adoption, particularly in low- and middle-income countries

- For instance, advanced NPWT systems from leading manufacturers such as 3M and Smith+Nephew can involve substantial upfront device costs along with recurring expenses for specialized dressings, limiting accessibility in budget-constrained healthcare settings

- Limited reimbursement coverage in certain regions further restricts patient access to NPWT therapy, especially for homecare treatment

- The requirement for trained healthcare professionals to properly apply and monitor NPWT systems can pose operational challenges in smaller clinics and rural healthcare facilities

- Overcoming these challenges will require improved reimbursement frameworks, cost-effective device innovations, expanded training programs, and broader awareness initiatives to ensure equitable access to NPWT technologies

Asia-Pacific Negative Pressure Wound Therapy Devices Market Scope

The market is segmented on the basis of product, type, wound, end user, distribution channel, and application.

- By Product

On the basis of product, the Negative Pressure Wound Therapy Devices market is segmented into stand-alone, portable, and disposable devices. The portable segment dominated the largest market revenue share of 46.8% in 2025, driven by the increasing shift toward outpatient care and home-based wound management. Portable systems provide greater mobility and flexibility, allowing patients to continue therapy without prolonged hospital stays. Their compact design, ease of operation, and improved battery performance enhance patient compliance. Growing prevalence of chronic wounds such as diabetic foot ulcers and pressure ulcers significantly contributes to sustained demand. Hospitals increasingly prefer portable systems to reduce inpatient burden and optimize operational efficiency. Technological advancements including digital pressure monitoring and quiet pump mechanisms further strengthen adoption. Rising geriatric population globally also fuels demand for convenient wound care solutions. Favorable reimbursement policies in developed regions support higher penetration. Increased surgical procedures worldwide further expand usage. Strong product availability and clinician familiarity ensure consistent revenue generation. The portable segment is projected to grow at a CAGR of 8.1% from 2026 to 2033.

The disposable segment is expected to witness the fastest CAGR of 10.4% from 2026 to 2033, supported by rising demand for single-patient-use systems that minimize infection risks. Disposable NPWT devices eliminate maintenance requirements and reduce cross-contamination concerns. They are particularly suitable for short-term post-operative wound care and home settings. Lightweight structure and simplified application procedures enhance patient comfort. Growing awareness regarding hospital-acquired infections drives adoption. Increasing demand in emerging markets due to cost-effective models further accelerates growth. Manufacturers are introducing compact and affordable disposable systems to strengthen accessibility. Expanding outpatient treatment models contribute significantly to segment expansion. Favorable clinical outcomes and simplified disposal processes enhance acceptance among providers. Continuous innovation and rising healthcare infrastructure development are expected to maintain rapid growth momentum.

- By Type

On the basis of type, the market is segmented into re-usable device and single-use device. The re-usable device segment held the largest market revenue share of 58.4% in 2025, attributed to its long-term cost efficiency in hospital settings. Large healthcare facilities prefer reusable systems for managing complex and high-exudate wounds. These systems provide adjustable pressure settings and advanced therapy customization options. Increasing number of surgical and trauma cases globally supports strong utilization. Established reimbursement frameworks in developed countries strengthen segment dominance. Reusable systems are widely adopted in tertiary care hospitals due to reliability and durability. Continuous technological upgrades including automated alarms and canister management features improve performance. High patient admission rates further sustain demand. Strong presence of key manufacturers offering advanced reusable platforms boosts market confidence. Clinical effectiveness and extended product lifecycle ensure stable revenue contribution. The segment is projected to expand at a CAGR of 7.6% during the forecast period.

The single-use device segment is anticipated to register the fastest CAGR of 10.7% from 2026 to 2033, driven by growing emphasis on infection control and simplified wound management. Increasing preference for sterile, disposable treatment options supports rapid adoption. These devices are ideal for ambulatory and home healthcare environments. Minimal setup requirements reduce training needs and operational complexity. Rising awareness about patient-centric care models enhances growth prospects. Expanding healthcare access in emerging economies accelerates penetration.

- By Wound

On the basis of wound, the market is segmented into surgical wound, diabetic ulcers, burn, pressure ulcers, venous ulcers, and others. The surgical wound segment dominated the largest market revenue share of 34.6% in 2025, owing to the high global volume of surgical procedures. NPWT devices are widely used to promote faster healing and reduce post-operative complications. Growth in orthopedic, cardiovascular, and reconstructive surgeries significantly contributes to segment expansion. Hospitals increasingly adopt advanced incision management systems to minimize infection risk. Favorable clinical evidence supporting NPWT in surgical recovery enhances utilization. Rising healthcare expenditure globally sustains demand growth. Technological integration enabling improved wound monitoring strengthens segment position. Increasing awareness about advanced wound closure techniques further supports adoption. High patient inflow in hospitals ensures steady revenue generation. The segment is expected to grow at a CAGR of 8.2% over the forecast period.

The diabetic ulcers segment is projected to witness the fastest CAGR of 11.6% from 2026 to 2033, driven by the rapidly rising diabetic population worldwide. Chronic non-healing wounds require prolonged advanced therapy, increasing device demand. Rising awareness regarding limb preservation treatments supports adoption. Expanding screening and early diagnosis programs further accelerate growth. Increasing incidence of obesity and sedentary lifestyles significantly contributes to the growing diabetic patient pool globally. Diabetic foot ulcers often lead to severe complications, including infections and amputations, thereby increasing the need for advanced wound care solutions such as NPWT. Healthcare providers increasingly recommend negative pressure systems to promote faster granulation tissue formation and improved blood circulation. Favorable reimbursement policies in developed countries further strengthen adoption rates. Rising investments in specialized diabetic wound care clinics also support segment expansion. Technological advancements in portable and disposable NPWT systems make treatment more accessible in outpatient and home settings. Growing government initiatives aimed at reducing diabetes-related complications enhance early intervention strategies. In addition, increasing patient awareness regarding effective wound management solutions is expected to sustain strong segment growth throughout the forecast period.

- By End User

On the basis of end user, the market is segmented into hospitals, wound care centers, ambulatory centers, home healthcare, clinics, and community centers. The hospitals segment accounted for the largest revenue share of 49.3% in 2025, supported by advanced infrastructure and high patient admissions. Hospitals manage a significant volume of post-surgical and trauma-related wounds requiring NPWT. Availability of skilled healthcare professionals enhances effective therapy administration. Strong procurement contracts and reimbursement frameworks strengthen dominance. Specialized surgical departments further increase utilization. Technological advancements in hospital-grade systems improve treatment outcomes. Rising complex wound cases globally sustain demand. The segment is projected to grow at a CAGR of 7.8% during the forecast period.

The home healthcare segment is expected to register the fastest CAGR of 11.2% from 2026 to 2033, fueled by increasing preference for convenient and cost-effective care. Aging populations and chronic disease prevalence drive demand for home-based therapy. Portable and disposable NPWT systems significantly support expansion. Growing awareness about at-home advanced wound management accelerates adoption. Rising hospital overcrowding and efforts to reduce inpatient costs further encourage the transition toward home-based treatment models. Patients recovering from surgeries increasingly prefer receiving therapy in familiar home environments, improving comfort and compliance. Technological advancements such as lightweight pumps, longer battery life, and simplified dressing systems enhance usability in non-clinical settings. Expanding telehealth services allow healthcare professionals to remotely monitor wound healing progress, strengthening confidence in home care solutions. Favorable reimbursement coverage for home healthcare services in several developed countries supports higher penetration. Increasing availability of trained home healthcare nurses further improves treatment outcomes. Growing government initiatives promoting decentralized healthcare delivery models also contribute to segment growth. In addition, rising awareness among caregivers regarding effective chronic wound management is expected to sustain strong expansion throughout the forecast period.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tenders and retail. The direct tenders segment dominated with a revenue share of 63.5% in 2025, driven by bulk procurement by hospitals and healthcare institutions. Long-term supply contracts ensure consistent revenue streams for manufacturers. Competitive pricing through institutional tenders supports higher purchase volumes. High patient inflow in large facilities sustains demand. Established supplier relationships enhance market stability. Favorable government procurement policies in several regions further strengthen dominance. The segment is projected to grow at a CAGR of 7.5% during the forecast period.

The retail segment is anticipated to witness the fastest CAGR of 9.8% from 2026 to 2033, supported by increasing demand from home healthcare patients and smaller clinics. Growing availability of NPWT devices in pharmacies and medical stores enhances accessibility. Rising consumer awareness about advanced wound care solutions boosts retail sales. Expansion of organized pharmacy chains and medical supply outlets further strengthens product visibility and availability. Increasing preference for over-the-counter procurement of portable and disposable NPWT systems contributes to higher sales volume. The rise of e-commerce platforms offering medical devices also supports retail channel growth by improving convenience and competitive pricing. Patients discharged early from hospitals often purchase NPWT accessories and consumables directly through retail networks. Improved distribution partnerships between manufacturers and regional suppliers enhance product reach in semi-urban and rural areas. Promotional activities and educational campaigns conducted by pharmacies help increase awareness regarding proper wound management. Simplified product packaging and user-friendly instructions further encourage direct purchase by caregivers and patients. Growing penetration of private healthcare services and outpatient clinics also drives demand through retail outlets. In addition, increasing emphasis on home-based chronic wound care is expected to sustain strong growth momentum in the retail segment throughout the forecast period.

- By Application

On the basis of application, the market is segmented into chronic wounds and acute wounds. The chronic wounds segment held the largest revenue share of 55.7% in 2025, driven by the increasing prevalence of diabetic foot ulcers, venous leg ulcers, and pressure ulcers. Long treatment duration associated with chronic wounds supports sustained device utilization. Growing elderly population significantly contributes to higher incidence rates. Advanced NPWT systems are widely recommended for chronic wound healing acceleration. Rising healthcare costs associated with untreated chronic wounds encourage early adoption. Favorable reimbursement structures strengthen market penetration. Continuous product innovation further enhances therapeutic outcomes. Increasing awareness among healthcare providers sustains demand growth. The segment is projected to grow at a CAGR of 8.4% during the forecast period.

The acute wounds segment is expected to witness the fastest CAGR of 10.1% from 2026 to 2033, supported by rising trauma injuries, burns, and surgical cases worldwide. Increasing emergency care admissions contribute to higher NPWT utilization. Technological advancements enabling faster wound closure further accelerate segment growth. Growing incidence of road accidents and sports-related injuries significantly drives demand for advanced wound management solutions. Acute burn cases require effective exudate management and infection control, where NPWT systems play a critical role. Hospitals increasingly adopt negative pressure therapy to reduce healing time and minimize scar formation. Rising number of cosmetic and reconstructive surgeries further contributes to segment expansion. Improved clinical evidence supporting NPWT in acute wound stabilization enhances physician confidence. Rapid urbanization and industrialization in emerging economies also increase trauma-related injuries. Advancements in portable NPWT systems enable early intervention even in emergency and ambulatory settings. Increasing healthcare expenditure and improved emergency care infrastructure further strengthen market growth. In addition, the need to reduce hospital stay duration and prevent secondary infections is expected to sustain strong demand for NPWT devices in acute wound management throughout the forecast period.

Asia-Pacific Negative Pressure Wound Therapy Devices Market Regional Analysis

- The Asia-Pacific negative pressure wound therapy devices market is projected to grow at the fastest pace during the forecast period of 2026 to 2033, driven by the rising burden of chronic wounds, increasing surgical procedures, and improving healthcare infrastructure across developing economies. Rapid urbanization, growing healthcare expenditure, and expanding hospital networks in countries such as China, Japan, and India are significantly contributing to market expansion

- The region is witnessing a surge in diabetes cases, which is leading to a higher incidence of diabetic foot ulcers and other chronic wounds, thereby increasing demand for advanced wound care solutions including NPWT systems

- In addition, supportive government initiatives aimed at strengthening public healthcare systems and improving access to advanced medical technologies are accelerating adoption across tertiary care hospitals and specialty clinics. The growing presence of global medical device manufacturers and expansion of local production capabilities are further enhancing affordability and availability of NPWT devices across the region

China Negative Pressure Wound Therapy Devices Market Insight

China negative pressure wound therapy devices market dominated the Asia-Pacific Negative Pressure Wound Therapy Devices market with the largest revenue share of 36.9% in 2025, driven by a large patient pool suffering from chronic wounds, expanding hospital infrastructure, increasing healthcare expenditure, and growing adoption of advanced wound care technologies across urban healthcare facilities. The rapid growth of tertiary hospitals and specialized wound care centers has significantly boosted the demand for NPWT systems in both surgical and chronic wound applications. Rising incidence of diabetes and trauma-related injuries further contributes to sustained market demand. Moreover, strong government investments in healthcare modernization and the presence of domestic manufacturers offering cost-competitive solutions are enhancing market penetration across both urban and semi-urban regions.

India Negative Pressure Wound Therapy Devices Market Insight

India negative pressure wound therapy devices market is expected to be the fastest-growing market in the Asia-Pacific Negative Pressure Wound Therapy Devices sector, expanding at a CAGR of 10.8% from 2026 to 2033. Growth is supported by improving access to advanced medical devices, rising incidence of diabetes-related wounds, and increasing government focus on strengthening healthcare infrastructure. The expansion of multi-specialty hospitals, growing awareness regarding advanced wound care therapies, and rising healthcare spending are contributing to increased adoption of NPWT devices. Furthermore, government initiatives aimed at expanding medical device manufacturing and enhancing rural healthcare accessibility are creating new growth opportunities. As India continues to modernize its healthcare ecosystem, demand for cost-effective and portable NPWT solutions is expected to increase significantly during the forecast period.

Asia-Pacific Negative Pressure Wound Therapy Devices Market Share

The Negative Pressure Wound Therapy Devices industry is primarily led by well-established companies, including:

- 3M Company (U.S.)

- Smith & Nephew plc (U.K.)

- Mölnlycke Health Care AB (Sweden)

- ConvaTec Group plc (U.K.)

- Coloplast A/S (Denmark)

- Cardinal Health, Inc. (U.S.)

- Medela AG (Switzerland)

- PAUL HARTMANN AG (Germany)

- Acelity L.P. Inc. (U.S.)

- Talley Group Ltd. (U.K.)

- Devon Medical Products (U.S.)

- ATMOS MedizinTechnik GmbH & Co. KG (Germany)

- Genadyne Biotechnologies, Inc. (U.S.)

- DeRoyal Industries, Inc. (U.S.)

- Medtronic plc (Ireland)

- Integra LifeSciences Holdings Corporation (U.S.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- B. Braun Melsungen AG (Germany)

- Hollister Incorporated (U.S.)

- Lohmann & Rauscher GmbH & Co. KG (Germany)

Latest Developments in Asia-Pacific Negative Pressure Wound Therapy Devices Market

- In April 2023, Convatec Group PLC completed the acquisition of the anti-infective nitric oxide technology platform from 30 Technology Limited, expanding its wound care portfolio and R&D capabilities to enhance negative pressure wound therapy outcomes

- In May 2023, Smith+Nephew was awarded an innovative technology contract from Vizient, Inc. for its PICO single-use NPWT systems, bolstering research and development and facilitating wider adoption of its portable wound therapy products

- In April 2024, Smith & Nephew PLC launched its RENASYS EDGE Negative Pressure Wound Therapy System in the United States — a lightweight, compact NPWT system designed for improved home-based chronic wound management with patient-centred usability

- In May 2025, the U.S. Department of Defense awarded Smith+Nephew a 10-year contract valued up to USD 75 million to supply its RENASYS TOUCH NPWT systems, supporting wound management across military and aeromedical care environments

- In February 2025, 3M Health Care received FDA clearance for its Veraflo Cleanse Choice Complete NPWT system, an advanced wound therapy device incorporating irrigation functionality to manage infected wounds and support comprehensive clinical care

- In August 2024, Guard Medical secured FDA 510(k) approval for expanded sizes (up to 25 cm) of its NPseal surgical NPWT dressing, enhancing surgical wound care effectiveness in larger anatomical areas

- In September 2024, Solventum launched its V.A.C. Peel and Place Dressing, an extended-wear wound dressing for NPWT aimed at reducing dressing change frequency and improving patient compliance — part of broader product innovation to simplify care delivery

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.