Asia Pacific Plastic Optical Fiber Market

Market Size in USD Billion

USD

1.17 Billion

USD

2.09 Billion

2025

2033

USD

1.17 Billion

USD

2.09 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.17 Billion | |

| USD 2.09 Billion | |

| % | |

|

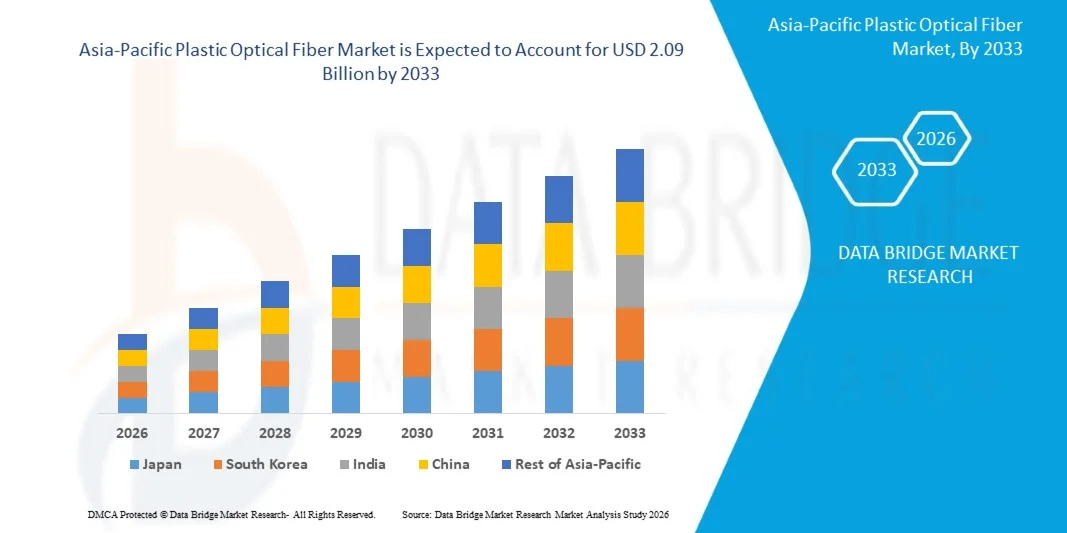

Asia-Pacific Plastic Optical Fiber Market Size

- The Asia-Pacific Plastic Optical Fiber Market size was valued at USD 1.17 Billion in 2025 and is expected to reach USD 2.09 Billion by 2033, at a CAGR of 8.2% during the forecast period

- The APAC Plastic Optical Fiber (POF) Market is witnessing steady growth, driven by rising demand for high-speed data transmission in automotive networks, industrial automation, consumer electronics, and home networking applications. The market is estimated due to increasing adoption of cost-effective and flexible optical communication solutions across developing economies such as China, Japan, South Korea, and India

- Market expansion is supported by growing investments in smart manufacturing, vehicle connectivity systems, and digital infrastructure upgrades across the region. Advancements in lightweight, easy-to-install fiber solutions and increasing preference for short-distance, energy-efficient communication technologies are expected to drive the market.

Asia-Pacific Plastic Optical Fiber Market Analysis

- The APAC Plastic Optical Fiber (POF) market is experiencing steady expansion driven by increasing adoption of high-speed and cost-effective communication solutions across automotive electronics, industrial automation, consumer devices, and home networking systems. Rising digitalization and demand for reliable short-distance data transmission infrastructure are supporting market growth across key economies such as China, Japan, South Korea, and India.

- Market growth is fueled by rising adoption of advanced driver-assistance systems (ADAS), in-vehicle networking, Industry 4.0 initiatives, and increasing automation across manufacturing sectors, where POF offers advantages including electromagnetic interference resistance, lightweight structure, and simplified maintenance.

- The China accounts for 36.70% market share in the Asia Pacific Plastic Optical Fiber market in 2026 and is projected to register a CAGR of 8.2%, supported by expanding smart manufacturing ecosystems, growing vehicle connectivity applications, and increasing deployment of fiber-based communication in industrial and commercial environments.

- India is expected to be the fastest-growing country in the Asia Pacific Plastic Optical Fiber market during the forecast period, driven by rapid expansion in telecommunications infrastructure and increasing adoption in data transmission applications.

- The Step-Index POF segment dominates the market, holding 63.06% share in 2026 and expected to grow at a CAGR of 8.0%, owing to its cost efficiency, ease of installation, flexibility, and suitability for short-range data transmission applications such as automotive infotainment systems, LED lighting networks, and home entertainment connectivity.

Report Scope and Asia-Pacific Plastic Optical Fiber Market Segmentation

|

Attributes |

Plastic Optical Fiber Market Insights |

|

Segments Covered |

|

|

Countries Covered |

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Asia-Pacific Plastic Optical Fiber Market Trends

“Rising adoption in automotive electronics and electric vehicles”

- The rapid electrification of vehicles across APAC is significantly increasing the need for reliable in-vehicle data communication systems. Modern electric vehicles (EVs) integrate advanced infotainment, battery management systems, digital dashboards, and sensor networks, all of which require stable, high-speed data transmission. Plastic Optical Fiber (POF) enables lightweight, flexible, and electromagnetic interference-resistant connectivity, making it suitable for complex automotive electronic architectures.

- Automotive manufacturers across Japan, China, and South Korea are increasingly adopting POF for in-vehicle networking applications such as infotainment systems, ambient lighting, and Advanced Driver-Assistance Systems (ADAS). Compared to traditional copper wiring, POF reduces vehicle weight and simplifies installation, supporting improved energy efficiency and vehicle performance.

- The expansion of electric and connected vehicle production is driving demand for cost-effective short-distance communication technologies. POF supports high data rates over short ranges while maintaining durability under vibration, heat, and harsh automotive environments, making it ideal for internal vehicle communication networks and smart mobility platforms.

- Overall, the shift toward connected, autonomous, and software-defined vehicles is transforming automotive electronic design in APAC. Increasing data exchange within vehicles is accelerating adoption of POF solutions, encouraging automakers to transition toward lightweight, scalable, and future-ready optical communication infrastructure to support next-generation mobility ecosystems.

Asia-Pacific Plastic Optical Fiber Market Dynamics

Driver

“Rising demand for short‑range, high‑speed connectivity”

- The rapid expansion of cloud computing and hyperscale data centers is a key driver of the U.S. data center structured cabling market. As businesses increasingly rely on cloud services for storage, computing power, and application delivery, the demand for large-scale data centers capable of handling massive volumes of data has surged.

- The global plastic optical fiber (POF) market is increasingly driven by the rising demand for short‑range, high‑speed connectivity across several sectors. Plastic optical fiber stands out from traditional glass fiber and copper solutions due to attributes like flexibility, robust performance in confined spaces, immunity to electromagnetic interference, and easier, lower‑cost installation; making it attractive for localized, high‑bandwidth communication needs. Fundamentally designed for distances typically under nearly100 m, POF provides sufficient bandwidth for real‑time data exchange in automotive, residential, industrial, and enterprise networks, where short‑distance performance is critical.

- POF’s short‑range capability helps enable a range of modern high‑speed systems, from in‑vehicle infotainment to localized area networks, by offering a balance of speed, cost, and installation simplicity compared with more complex glass fiber or copper alternatives.

- For instance, In September 2025, FibreTX published an industry news report highlighting that POF adoption is expanding in automotive infotainment and in‑vehicle short‑distance networks, driven by advantages such as EMI immunity, ease of installation, and gigabit‑class links needed for modern vehicle subsystems, demonstrating real-world applications where localized high‑speed connectivity is critical and reinforcing demand driven by short‑range connectivity requirements.

- The demand for short‑range, high‑speed connectivity is a core driver shaping the growth of the Asia Pacific Plastic Optical Fiber market. As industries and consumers alike seek reliable, cost‑effective solutions for localized data transmission, POF has emerged as a compelling alternative to traditional cabling technologies in specific applications where ease of installation, mechanical flexibility, and EMI resistance are paramount. With continued advancements in polymer materials and integration technologies, POF is well‑positioned to support the next wave of connected vehicles, smart infrastructure, and consumer network solutions, even as longer‑haul glass fiber systems continue to dominate backbone communications

Restraint/Challenge

“Vulnerabilities in supply chain and raw material availability”

- The Global Plastic Optical Fiber (POF) Market faces notable challenges related to supply chain vulnerabilities and raw material availability. POF production relies heavily on specialized polymers (e.g., polymethyl methacrylate (PMMA), perfluorinated polymers) and engineered additives that are not as widely produced as the basic plastics used in other industries. Many of these raw materials are sourced from a limited number of suppliers concentrated in specific regions, which increases susceptibility to disruptions from geopolitical tensions, trade restrictions, logistical bottlenecks, and fluctuations in petrochemical feedstock prices.

- Additionally, global events such as natural disasters, factory shutdowns, and tight capacity in polymer extrusion facilities can delay supply; driving up input costs and extending lead times for manufacturers of POF cables and components. These supply risks are further amplified by increasing demand for polymers across electronics, automotive, and consumer goods sectors, intensifying competition for raw materials and pressuring the POF industry’s ability to maintain cost‑competitive, timely delivery of products.

- For instance, In 2025, Patsnap’s PMMA supply chain study identified continued volatility in MMA (methyl methacrylate); the core monomer used to produce PMMA for POF; noting that fluctuating raw material prices and occasional shortages create unpredictability in pricing and supply, making it difficult for POF manufacturers to maintain stable production costs and reliable deliveries. This imbalance between demand and supply highlights that raw material availability remains a structural challenge that can slow market growth for plastic optical fiber products.

- Vulnerabilities in supply chain and raw material availability remain a significant challenge for the Asia Pacific Plastic Optical Fiber market. Dependence on PMMA and other petroleum-based polymers, coupled with geopolitical tensions, transportation bottlenecks, and market price fluctuations, creates uncertainty in production, delivery schedules, and cost management. These constraints limit manufacturers’ ability to scale production efficiently, affect lead times for end users across telecom, automotive, healthcare, and industrial sectors, and pose a barrier to meeting the growing global demand for POF solutions. Addressing these supply chain and material challenges is critical for sustaining long-term growth and adoption of plastic optical fiber technologies worldwide.

Asia-Pacific Plastic Optical Fiber Market Scope

The Asia-Pacific Plastic Optical Fiber Market is segmented into eight notable segments based on type, offering, data transmission speed, network architecture, light source, communication protocol, application, and end-user.

- By Type

On the basis of type, the Asia Pacific Plastic Optical Fiber market is segmented into Step-Index POF and Gradient Index POF. In 2026, the Step-Index POF segment is expected to dominate the Asia Pacific Plastic Optical Fiber market with share of 63.06% due to its widespread adoption in automotive networking, industrial automation, and short-distance communication applications. Step-index POF offers cost-effectiveness, mechanical flexibility, ease of termination, and strong resistance to vibration, making it highly suitable for in-vehicle infotainment systems, factory automation, and home networking. Among subtypes, PMMA-based cables hold significant commercial relevance due to their established manufacturing ecosystem and broad application base.

The Gradient-Index POF segment is anticipated to witness the fastest CAGR of 8.6% from 2026 to 2033, fueled by its cost-effectiveness, simple manufacturing process, and strong suitability for short-distance data transmission applications. Step-index POF offers easy installation, high flexibility, and resistance to electromagnetic interference, making it highly preferred in automotive electronics, industrial automation, consumer electronics, and home networking systems. Increasing adoption of in-vehicle infotainment and lighting networks, along with the expansion of smart factories and Industry 4.0 infrastructure across the APAC region, is further accelerating demand. Additionally, growing preference for lightweight and energy-efficient communication solutions, combined with continuous improvements in polymer materials and transmission performance, is supporting wider deployment of step-index POF across commercial and industrial connectivity applications.

- By Offerings

On the basis of offering, the Asia Pacific Plastic Optical Fiber market is segmented into Components and Services. In 2026, the Components segment is expected to dominate the market with share of 83.41% due to strong demand for transmitters, receivers, connectors, couplers, splitters, and switching units required for POF deployment. LED-based transmitters and photodiode-based receivers remain widely used in automotive and industrial systems owing to their cost efficiency and reliability. Continuous integration of optoelectronic components into vehicles, automation systems, and consumer electronics significantly drives revenue concentration within the components segment compared to service-based offerings.

The Components segment is anticipated to witness the fastest CAGR of 8.3% from 2026 to 2033, fueled by increasing demand for essential Plastic Optical Fiber (POF) hardware such as connectors, transmitters, receivers, cables, and coupling devices required for reliable optical communication systems. Growing deployment of POF across automotive electronics, industrial automation, consumer devices, and smart building infrastructure is driving the need for high-performance and easily integrable components. Additionally, advancements in compact optical modules, improved signal transmission efficiency, and rising adoption of plug-and-play connectivity solutions are supporting segment growth. The expansion of connected devices, Industry 4.0 adoption, and increasing investments in cost-effective short-range communication networks across the APAC region are further accelerating demand for POF components.

- By Data Transmission Speed

On the basis of data transmission speed, the Asia Pacific Plastic Optical Fiber market is segmented into Low-Speed POF (<100 Mbps), Medium-Speed POF (100 Mbps–1 Gbps), and High-Speed POF (>1 Gbps). In 2026, the LowSpeed POF (<100 Mbps) segment is anticipated to dominate the market with share of 45.57% due to its extensive use in automotive infotainment systems, industrial sensor networks, lighting control systems, and short-range communication links. Most current automotive and industrial POF deployments operate within bandwidth ranges that do not require gigabit-level speeds, thereby maintaining strong commercial demand for low-speed solutions.

The High-Speed POF (>1 Gbps) segment is anticipated to witness the fastest CAGR of 8.6% from 2026 to 2033, fueled by increasing demand for cost-effective and reliable short-distance communication solutions in automotive electronics, home networking, industrial control systems, and consumer devices. Low-speed POF is widely adopted for applications such as infotainment connectivity, LED lighting systems, sensors, and automation networks where moderate data transmission speeds are sufficient but durability and ease of installation are critical. Its immunity to electromagnetic interference, lightweight structure, and simplified maintenance make it an attractive alternative to copper cabling in electrically noisy environments. Additionally, growing adoption of smart home devices, factory automation, and connected infrastructure across the APAC region is accelerating deployment of low-speed POF solutions for stable and energy-efficient data communication.

- By Network Architecture

On the basis of network architecture, the Asia Pacific Plastic Optical Fiber market is segmented into Point-to-Point POF Systems, Star Network POF Systems, and Ring Network POF Systems. In 2026, the Star Network POF Systems segment is expected to dominate with the market share 42.10% due to its centralized architecture, scalability, simplified troubleshooting, and compatibility with automotive infotainment and industrial control systems. Star topologies enable efficient signal management and are widely implemented in vehicle communication systems and structured industrial layout.

The Star Network POF Systems segment is anticipated to witness the fastest CAGR of 8.5% from 2026 to 2033, fueled by increasing demand for centralized and reliable communication architectures across automotive, industrial automation, and smart building applications. Star network topology enables efficient data transmission by connecting multiple devices to a single central hub, improving network reliability, fault isolation, and ease of maintenance compared to traditional network structures. The growing adoption of connected devices, smart lighting systems, and in-vehicle infotainment networks is accelerating the use of POF-based star configurations due to their flexibility and simplified installation. Additionally, rising deployment of home automation systems and industrial IoT networks across the APAC region is supporting demand for scalable, cost-effective, and interference-resistant star network POF solutions.

- By Light source

On the basis of light source, the Asia Pacific Plastic Optical Fiber market is segmented into LED-Based POF Systems and Laser-Based POF Systems. In 2026, the LED-Based POF Systems segment is anticipated to dominate with market share 64.97% due to lower cost, longer operational life, simpler thermal management, and adequate performance for short-distance communication. LEDs are extensively used in automotive MOST networks, home entertainment systems, and industrial automation where ultra-high bandwidth is not required.

The Laser-Based POF Systems segment is anticipated to witness the fastest CAGR of 8.6% from 2026 to 2033, fueled by increasing adoption of cost-efficient optical communication solutions across automotive lighting, home networking, and industrial control applications. LED-based transmitters offer advantages such as lower power consumption, longer operational life, and reduced system costs compared to laser-based alternatives, making them highly suitable for short-distance data transmission using plastic optical fibers. Growing deployment of ambient vehicle lighting, infotainment connectivity, and smart building illumination systems is further supporting demand for LED-driven POF systems. Additionally, advancements in high-brightness LEDs and improved signal stability are enhancing transmission performance, encouraging wider adoption in consumer electronics and automation networks across the APAC region.

- By Communication Protocol

On the basis of communication protocol, the Asia Pacific Plastic Optical Fiber market is segmented into MOST (Media Oriented Systems Transport), Ethernet over POF, FlexRay, and CAN over POF. In 2026, the MOST (Media Oriented Systems Transport) segment is expected to dominate the market with share 44.41% due to its strong integration in automotive infotainment and multimedia networking systems. MOST technology has been widely adopted by automotive OEMs for reliable, high-quality audio and video data transmission within vehicles, supporting infotainment, navigation, and entertainment subsystems.

The Ethernet over POF segment is anticipated to witness the fastest CAGR of 8.7% from 2026 to 2033, fueled by increasing integration of advanced infotainment and multimedia networking systems in modern vehicles. MOST technology enables high-speed, synchronized data transmission for audio, video, navigation, and communication applications through Plastic Optical Fiber (POF), ensuring reliable and interference-free connectivity within automotive environments. Growing production of connected and electric vehicles across the APAC region is driving demand for robust in-vehicle networking protocols capable of handling rising data loads from digital dashboards, entertainment systems, and driver-assistance features. Additionally, automakers’ focus on lightweight wiring architectures, improved passenger experience, and seamless multimedia communication is accelerating adoption of MOST-based POF systems in next-generation automotive platforms.

- By Application

On the basis of application, the Asia Pacific Plastic Optical Fiber market is segmented into Industrial Automation & Control, Automotive, Consumer Electronics, Medical Applications, Data Centers & Server Rooms, Smart Infrastructure, and Others. In 2026, the Automotive segment is anticipated to dominate the market with share 28.18% due to extensive deployment of POF in in-vehicle networking, infotainment systems, sensor connectivity, interior lighting systems, and advanced driver-assistance systems (ADAS). The increasing shift toward connected and software-defined vehicles significantly strengthens POF adoption across passenger and commercial vehicle platforms.

The Automotive segment is anticipated to witness the fastest CAGR of 9.0% from 2026 to 2033, fueled by the rapid expansion of connected, electric, and software-defined vehicles across the APAC region. Increasing integration of advanced infotainment systems, digital instrument clusters, Advanced Driver-Assistance Systems (ADAS), and in-vehicle communication networks is driving demand for reliable and high-speed data transmission solutions. Plastic Optical Fiber (POF) is gaining strong adoption in automotive applications due to its lightweight structure, flexibility, immunity to electromagnetic interference, and ease of installation compared to traditional copper wiring. Additionally, growing vehicle electrification, rising consumer demand for enhanced in-car connectivity and entertainment, and automakers’ focus on improving energy efficiency and reducing vehicle weight are accelerating the deployment of POF-based communication systems in next-generation automotive platforms.

- By End User

On the basis of end user, the Asia Pacific Plastic Optical Fiber market is segmented into Industrial, Automotive OEMs, Telecommunication Providers, Consumer Electronics Companies, Healthcare Organizations, Defense, Energy & Aerospace, and Others. In 2026, the Automotive OEMs segment is expected to dominate the market with share 27.28% due to largescale integration of step-index POF systems in passenger vehicles and commercial vehicles. Automotive manufacturers increasingly prefer POF for lightweight cabling, EMI immunity, vibration resistance, and cost-efficient short-distance optical communication, reinforcing strong revenue concentration within this end-user category.

The Automotive OEMs segment is anticipated to witness the fastest CAGR of 8.5% from 2026 to 2033, fueled by increasing integration of advanced electronic architectures and high-speed in-vehicle communication systems in next-generation vehicles. Automotive OEMs are increasingly adopting Plastic Optical Fiber (POF) solutions to support infotainment systems, digital cockpits, ADAS connectivity, and vehicle networking due to their lightweight design, flexibility, and resistance to electromagnetic interference. The growing production of electric and connected vehicles across the APAC region is encouraging OEMs to implement efficient and scalable data transmission technologies that reduce wiring complexity and improve overall vehicle performance. Additionally, rising focus on enhancing passenger experience, improving energy efficiency, and enabling future-ready vehicle platforms is accelerating OEM-level adoption of POF-based communication infrastructure.

Asia-Pacific Plastic Optical Fiber Market Regional Analysis

- The Asia-Pacific region holds a strong dominant position in the Asia Pacific Plastic Optical Fiber market, accounting for 36.71% market share and projected to grow at a CAGR of 8.2% during the forecast period. This leadership is supported by strong automotive manufacturing hubs in China, Japan, and South Korea, rapid industrial automation adoption, and expanding consumer electronics production. Increasing deployment of Plastic Optical Fiber in vehicle infotainment systems, industrial communication networks, and smart infrastructure projects, along with favorable manufacturing ecosystems and cost-efficient production capabilities, strengthens regional market growth. Continuous investments in smart factories, electric vehicles, and digital connectivity infrastructure further enhance adoption across APAC economies.

- Other emerging economies such as India, Southeast Asia, and Australia are contributing steadily to market expansion through rising industrial digitalization, smart city initiatives, and growing demand for affordable short-distance optical communication solutions. Market growth in these regions is supported by increasing adoption of home networking systems, automation technologies, and connected devices, alongside expanding electronics manufacturing activities. Collectively, these countries benefit from growing demand for lightweight, energy-efficient, and interference-resistant communication infrastructure, accelerating Plastic Optical Fiber deployment across automotive, industrial, and commercial applications throughout the region.

China Plastic Optical Fiber Market Insight

The China plastic optical fiber market is witnessing robust growth, fueled by the country’s rapid expansion in telecommunications, data centers, and broadband infrastructure. Increasing adoption of fiber-to-the-home (FTTH) networks and smart city initiatives is driving demand for high-performance, flexible optical fibers. Additionally, rising investments in industrial automation, automotive connectivity, and IoT applications are further supporting market growth. The market is also benefiting from government policies promoting advanced communication technologies and local manufacturing capabilities.

India Plastic Optical Fiber Market Insight

The India Plastic Optical Fiber (POF) market is witnessing steady growth, fueled by rising demand for high-speed data transmission, expanding fiber-to-the-home (FTTH) networks, and increased adoption across automotive, industrial, and consumer electronics sectors. Technological advancements in polymer-based fibers, coupled with government initiatives to enhance digital infrastructure, are further supporting market expansion. The market is characterized by the presence of key domestic manufacturers and increasing investments from global players seeking to capitalize on India’s growing connectivity need.

Japan Medical Device and Accessories Market Insight

The Japan Plastic Optical Fiber (POF) market is witnessing steady growth, fueled by rising demand for high-speed data transmission, expanding fiber-to-the-home (FTTH) networks, and increased adoption across automotive, industrial, and consumer electronics sectors. Technological advancements in polymer-based fibers, coupled with government initiatives to enhance digital infrastructure, are further supporting market expansion. The market is characterized by the presence of key domestic manufacturers and increasing investments from global players seeking to capitalize on India’s growing connectivity need.

Asia-Pacific Plastic Optical Fiber Market Share

The Asia-Pacific Plastic Optical Fiber Market is primarily led by well-established companies, including:

- Mitsubishi Chemical Group Corporation (Japan)

- Toray Industries, Inc. (Japan)

- Asahi Kasei Corporation (Japan)

- AGC Inc. (Japan)

- Firecomms Ltd. (Ireland)

- COMOSS (Germany)

- Fiberoptics Technology Incorporated (U.S.)

- Industrial Fiber Optics, Inc. (U.S.)

- Zdea Group Co., Ltd. (China)

- Nanoptics, Inc. (U.S.)

- FiberFin (U.S.)

- XiOptics LLC (U.S.)

- Jiangsu TX Plastic Optic Fibers Co., Ltd. (China)

- Sichuan Huiyuan Plastic Optical Fiber Co. Ltd (China)

- Daishing POF Co., Ltd. (Japan)

Latest Developments in Asia-Pacific Plastic Optical Fiber Market

- In October 2025, Asahi Kasei has received official approval to establish new facilities at its Kawasaki Works for the production of electrolysis system components, covering both alkaline water electrolysis and chlor-alkali electrolysis. The company anticipates strong demand for alkaline water electrolysis systems as clean hydrogen production expands globally. This signals potential indirect benefits, as the company’s strengthened material expertise and production capabilities may facilitate innovations in polymer-based optical fibers, support advanced manufacturing processes, and enable the development of high-performance POF products for industrial, sensor, and data communication applications.

- In march, OFC 2025 (Optical Fiber Communication Conference) in San Francisco, AGC Inc. showcased its latest optical communications technologies, including polymer optical waveguides, glass optical waveguides, micro lens arrays, and other advanced optical materials. The demonstration highlighted AGC’s focus on high-performance optical components for data transmission, imaging, and sensing applications, reflecting its commitment to innovation in the optical communications industry. This news is directly related to plastic optical fiber, as polymer optical waveguides are a type of plastic optical fiber used for short-distance data transmission, industrial sensors, automotive networks, and consumer electronics.

- In June 2025, Firecomms Ltd. announced a strategic regional distribution partnership with Tecnomic Components to expand demand creation and strengthen customer support for its optical transceivers and fiber optic solutions across South East Asia and India, enhancing its regional market presence and service capabilities.

- In 2025, COMOSS expanding its representation of Firecomms POF products directly impacts the market by increasing the availability and reach of POF solutions in key Asian markets—Japan and South Korea. This expansion helps accelerate adoption of plastic optical fiber technology in industrial, automotive, and communication applications. By distributing Firecomms’ POF transceivers, connectors, and networking solutions, COMOSS strengthens supply chains, supports market growth, and enhances competition, which can drive innovation, price competitiveness, and broader deployment of POF systems in the region.

- In March, Jiangxi Daishing POF Co., Ltd. announced that its Innovative Plastic Optical Fiber 3.0 technology will be globally introduced, achieving dual breakthroughs in high-speed transmission and intelligent packaging, marking a new era in the field of optical fiber communication technology.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Asia Pacific Plastic Optical Fiber Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Asia Pacific Plastic Optical Fiber Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Asia Pacific Plastic Optical Fiber Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.