Asia Pacific Pvc Compound Market

Market Size in USD Billion

USD

79.19 Billion

USD

116.11 Billion

2024

2032

USD

79.19 Billion

USD

116.11 Billion

2024

2032

| 2025 - 2032 | |

| USD 79.19 Billion | |

| USD 116.11 Billion | |

| % | |

|

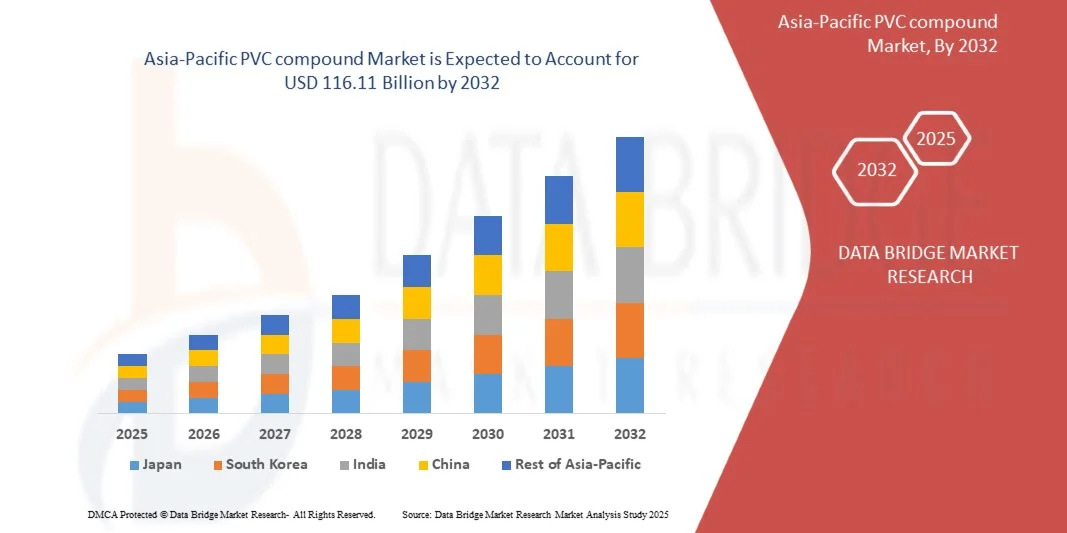

Asia-Pacific PVC compound Market Size

- The Asia-Pacific PVC compound market size was valued at USD 79.19 billion in 2024 and is expected to reach USD 116.11 billion by 2032, at a CAGR of 4.90% during the forecast period.

- The market growth is primarily driven by increasing demand from the construction, automotive, and electrical & electronics sectors, coupled with ongoing urbanization and industrialization across the region.

- Additionally, advancements in PVC compounding technology, such as enhanced durability, flame retardancy, and sustainability, are supporting wider adoption across applications, thereby propelling the market expansion over the coming years.

Asia-Pacific PVC compound Market Analysis

- PVC compounds, used in applications such as construction, automotive, and electrical & electronics, are increasingly critical in the Asia-Pacific region due to their durability, versatility, and cost-effectiveness, supporting the development of infrastructure and industrial products.

- The rising demand for PVC compounds is primarily driven by rapid urbanization, industrial growth, and increasing consumer preference for lightweight, low-maintenance, and sustainable materials.

- China dominated the Asia-Pacific PVC compound market with the largest revenue share of 38.5% in 2024, characterized by massive construction activity, strong automotive production, and the presence of leading chemical manufacturers, with domestic innovations in high-performance and eco-friendly PVC compounds further boosting market adoption.

- India is expected to be the fastest-growing country in the Asia-Pacific PVC compound market during the forecast period due to accelerating infrastructure projects, increasing disposable incomes, and growing demand from the automotive and electrical sectors.

- The rigid product segment dominated the market with the largest revenue share of 55.8% in 2024, driven by its extensive use in construction applications such as pipes, window profiles, and cable insulation, where structural strength and durability are critical

Report Scope and Asia-Pacific PVC compound Market Segmentation

|

Attributes |

Asia-Pacific PVC compound Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia-Pacific PVC compound Market Trends

“Enhanced Performance Through Advanced PVC Compounding Technologies”

- A significant and accelerating trend in the Asia-Pacific PVC compound market is the adoption of advanced compounding technologies that improve material performance, durability, and sustainability. These innovations are enabling broader applications across construction, automotive, electrical & electronics, and packaging sectors.

- For instance, specialty PVC compounds with superior flame retardancy, impact resistance, and chemical stability are increasingly being used in electrical cables, automotive interiors, piping systems, and packaging materials, meeting both regulatory standards and demanding performance requirements. Similarly, bio-based and recycled PVC compounds are gaining traction as manufacturers focus on sustainability and reducing environmental impact.

- Advanced compounding techniques also allow customization for specific application needs, such as enhanced weather resistance, flexibility, UV stability, or thermal endurance. Certain modern PVC formulations are engineered to withstand extreme climates or prolonged sunlight exposure, ensuring longer service life and lower maintenance costs.

- The integration of these high-performance compounds into industrial and construction applications enables manufacturers to achieve higher efficiency, lower lifecycle costs, and compliance with stringent safety regulations. Through tailored solutions, companies can meet diverse industry requirements while supporting sustainability initiatives.

- This trend toward high-performance, customizable, and eco-friendly PVC compounds is reshaping market expectations, encouraging suppliers such as Shin-Etsu and Formosa Plastics to innovate with compounds offering superior durability, flame retardancy, and application-specific properties.

- The demand for advanced PVC compounds is growing rapidly across construction, automotive, electrical, and packaging sectors, as manufacturers increasingly prioritize material performance, safety, and sustainability.

Asia-Pacific PVC compound Market Dynamics

Driver

“Growing Demand Driven by Rapid Urbanization and Industrial Expansion”

- The accelerating pace of urbanization and industrialization across Asia-Pacific, coupled with increasing demand for high-performance construction, automotive, and electrical components, is a major driver for the expanding PVC compound market.

- For instance, in 2024, leading manufacturers such as Shin-Etsu and Formosa Plastics announced expansions in PVC compound production facilities to cater to growing demand from infrastructure projects, real estate development, and automotive component suppliers. These strategic investments are expected to propel market growth over the forecast period.

- Industries increasingly require materials with enhanced durability, flame retardancy, chemical resistance, and thermal stability. PVC compounds provide an effective solution for applications such as pipes, cables, flooring, automotive parts, and electrical housings, offering superior performance compared to conventional materials.

- Additionally, the rising adoption of sustainable building practices and eco-friendly technologies is driving demand for PVC compounds that are recyclable or formulated with reduced environmental impact, in line with regional regulatory standards and consumer preferences.

- The versatility, cost-effectiveness, ease of processing, and ability to meet specific application needs make PVC compounds a preferred choice across construction, automotive, and electrical sectors in both emerging and developed Asia-Pacific markets.

Restraint/Challenge

“Environmental Concerns and Raw Material Price Volatility”

- Environmental concerns associated with the production and disposal of PVC, including the release of harmful additives and plasticizers, pose a significant challenge to the market. Stricter regulations and growing consumer awareness around sustainability can limit the use of conventional PVC compounds in certain applications.

- For Instance, regulatory restrictions in countries such as Japan and Australia on specific PVC additives have encouraged manufacturers to develop sustainable alternatives, which may involve higher costs or reformulated production processes.

- Addressing these environmental concerns through bio-based PVC compounds, phthalate-free formulations, and advanced recycling techniques is critical to sustaining market growth. Companies like Formosa Plastics and LG Chem are actively investing in eco-friendly PVC technologies to comply with regulations and meet evolving consumer expectations.

- Additionally, volatility in raw material prices, particularly chlorine and ethylene, can influence PVC compound production costs, affecting pricing and profitability for manufacturers.

- While technological innovations are gradually mitigating environmental and cost challenges, navigating regulatory compliance, consumer perception, and raw material price fluctuations remains crucial for long-term growth in the Asia-Pacific PVC compound market.

Asia-Pacific PVC compound Market Scope

Asia-Pacific PVC compound market is segmented of the basis product type, type, compound, manufacturing process, raw material and end-user.

• By Product Type

On the basis of product type, the Asia-Pacific PVC compound market is segmented into rigid products and flexible products, while also classified by type into non-plasticized PVC and plasticized PVC. The rigid product segment dominated the market with the largest revenue share of 55.8% in 2024, driven by its extensive use in construction applications such as pipes, window profiles, and cable insulation, where structural strength and durability are critical. Non-plasticized PVC, in particular, is favored for applications requiring high stiffness and long-term stability.

The flexible product segment is expected to witness the fastest growth rate of 22.1% from 2025 to 2032, owing to rising demand in automotive interiors, electrical insulation, and consumer goods that require pliable, lightweight, and cost-effective materials. Plasticized PVC, with its enhanced flexibility

- By Type

On the basis of type, the Asia-Pacific PVC compound market is segmented into non-plasticized PVC and plasticized PVC. The non-plasticized PVC segment dominated the market with the largest revenue share in 2024, driven by its superior rigidity, chemical resistance, and widespread use in construction applications such as pipes, window profiles, and fittings. Manufacturers and end-users often prefer non-plasticized PVC for infrastructure projects due to its long service life, structural strength, and cost-effectiveness.

The plasticized PVC segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by rising demand in flexible applications such as flooring, cable insulation, automotive interiors, and packaging. Plasticized PVC offers enhanced flexibility, durability, and ease of processing, making it ideal for applications requiring pliability without compromising performance. Increasing adoption of customized formulations and eco-friendly plasticizers is also contributing to the rapid growth of this segment across various end-user industries in the region and processability, further supports adoption across emerging industrial and residential applications.

• By Compound

On the basis of compound, the market is segmented into dry PVC compounds and wet PVC compounds. The dry PVC compound segment held the largest market revenue share of 61.5% in 2024, primarily due to its stability, ease of storage, and versatility for various manufacturing processes, including extrusion and injection molding. Dry compounds are widely preferred in high-volume industrial applications such as pipes, flooring, and cables.

The wet PVC compound segment is expected to witness the fastest CAGR of 20.5% from 2025 to 2032, fueled by the growing demand for specialized formulations in coatings, films, and flexible sheets. Wet compounds offer advantages in blending with additives and achieving tailored properties, making them increasingly attractive for automotive, packaging, and medical applications.

• By Manufacturing Process

On the basis of manufacturing process, the market is segmented into injection molding, extrusion, and others. The extrusion segment dominated the market with the largest revenue share of 57.3% in 2024, driven by its suitability for producing pipes, profiles, and sheets with consistent quality and cost efficiency. Extrusion is widely preferred in the construction and electrical sectors for high-volume production.

The injection molding segment is expected to witness the fastest growth rate of 21.8% from 2025 to 2032, supported by increasing demand for complex automotive components, consumer goods, and medical devices that require precise shapes, high dimensional accuracy, and superior surface finish. Advanced injection molding techniques, coupled with performance-enhancing PVC compounds, are further accelerating adoption.

• By Raw Material

On the basis of raw material, the market is segmented into PVC resin, plasticizers, stabilizers, lubricants, fillers, functional additives, and alloying polymers. PVC resin dominated the market with the largest revenue share of 63.7% in 2024, as it forms the core material for almost all PVC compound formulations and is essential for applications in construction, automotive, and electrical industries.

Plasticizers and stabilizers are expected to witness the fastest growth rate of 23.0% from 2025 to 2032, owing to rising demand for flexible PVC products, enhanced durability, and flame retardancy. Functional additives, fillers, and alloying polymers are increasingly used to meet application-specific requirements, including chemical resistance, thermal stability, and sustainability, further driving raw material consumption across sectors.

• By End-User

On the basis of end-user, the Asia-Pacific PVC compound market is segmented into medical, building and construction, packaging, automotive, consumer goods, electrical and electronics, and others. The building and construction segment dominated the market with the largest revenue share of 52.4% in 2024, driven by the extensive use of PVC compounds in pipes, window profiles, flooring, and insulation materials, supported by rapid urbanization and infrastructure development.

The automotive segment is expected to witness the fastest CAGR of 24.2% from 2025 to 2032, as demand for lightweight, flexible, and durable interior and exterior components grows in line with rising vehicle production and stricter fuel efficiency regulations. PVC compounds’ versatility and cost-effectiveness further support their adoption across other sectors such as electrical, packaging, and medical devices.

Asia-Pacific PVC compound Market Regional Analysis

- China dominated the PVC compound market with the largest revenue share of 38.5% in 2024, driven by rapid urbanization, industrialization, and growing demand from construction, automotive, and electrical & electronics sectors.

- Consumers and businesses in the region increasingly prioritize high-performance materials that offer durability, flame retardancy, and cost efficiency, making PVC compounds a preferred choice for pipes, flooring, cables, and automotive components.

- This widespread adoption is further supported by the expansion of manufacturing infrastructure, rising disposable incomes in emerging economies, and favorable government initiatives promoting industrial growth and modern infrastructure development, establishing PVC compounds as a critical material across residential, commercial, and industrial applications.

China PVC Compound Market Insight

The China PVC compound market accounted for the largest revenue share in the Asia-Pacific region in 2024, driven by strong demand from the construction, automotive, and electrical industries. The country’s robust infrastructure development, rapid urbanization, and expanding manufacturing capabilities continue to fuel PVC compound consumption. Growing investments in building and construction activities, especially in residential and industrial projects, are further accelerating market growth. Moreover, China’s leading position as a major exporter of PVC products and the adoption of advanced compounding technologies are enhancing product quality and performance. The increasing focus on sustainability and recyclability is also pushing manufacturers toward eco-friendly PVC formulations to meet domestic and international standards.

Japan PVC Compound Market Insight

The Japan PVC compound market is witnessing steady growth, supported by rising applications in the automotive, electronics, and medical sectors. Japanese manufacturers are emphasizing high-performance, precision-engineered PVC compounds that meet stringent safety and quality regulations. The demand for lightweight, durable, and heat-resistant materials in automotive interiors and wiring harnesses is a major growth driver. Additionally, Japan’s strong focus on environmental sustainability and recycling initiatives encourages the use of non-phthalate and bio-based plasticizers in PVC compounding. The country's well-developed technological infrastructure and innovation-driven chemical industry continue to enhance the production of specialty PVC compounds with superior performance characteristics.

India PVC Compound Market Insight

The India PVC compound market is expected to grow at the fastest CAGR during the forecast period, fueled by rapid industrialization, urban expansion, and the government’s push for affordable housing and infrastructure development. The booming construction and electrical sectors are major consumers of PVC compounds for pipes, cables, and profiles. Additionally, the rising demand for cost-effective and durable materials in the automotive and packaging industries supports market expansion. Increasing foreign investments in polymer production and the establishment of new compounding facilities are enhancing local supply capabilities. The growing emphasis on sustainable materials and the shift toward non-toxic PVC compounds are expected to further stimulate the market in India.

South Korea PVC Compound Market Insight

The South Korea PVC compound market is experiencing consistent growth, driven by increasing demand from the construction, electronics, and consumer goods industries. The country’s technologically advanced polymer manufacturing sector and focus on producing high-quality, performance-driven compounds are strengthening market competitiveness. South Korean companies are investing in the development of specialty PVC formulations, particularly those with improved flexibility, weather resistance, and thermal stability, to cater to high-end industrial applications. Moreover, sustainability initiatives and regulatory standards promoting the use of eco-friendly and recyclable materials are further encouraging innovation within the PVC compounding industry..

Asia-Pacific PVC compound Market Share

The PVC compound industry is primarily led by well-established companies, including:

- Shin-Etsu Chemical Co., Ltd. (Japan)

- LG Chem (South Korea)

- Formosa Plastics Corporation (Taiwan)

- Reliance Industries Limited (India)

- Solvay S.A. (Belgium)

- BASF SE (Germany)

- Occidental Petroleum Corporation – OxyChem (U.S.)

- Kem One (France)

- SABIC (Saudi Arabia)

- Dow Inc. (U.S.)

- INOVYN (UK)

- Vinnolit GmbH & Co. KG (Germany)

- Axiall Corporation (U.S.)

- Thai Plastic and Chemicals PLC (Thailand)

- China National Chemical Corporation – ChemChina (China)

- Tianjin Dagu Chemical Co., Ltd. (China)

- China Petroleum & Chemical Corporation – Sinopec (China)

- Nan Ya Plastics Corporation (Taiwan)

- Mitsui Chemicals, Inc. (Japan)

- LG Polymers India Pvt. Ltd. (India)

What are the Recent Developments in Asia-Pacific PVC compound Market?

- In April 2023, Shin-Etsu Chemical Co., Ltd., a global leader in PVC and specialty chemicals, launched a strategic initiative in India aimed at expanding its high-performance PVC compound portfolio for construction and automotive applications. This initiative highlights the company’s commitment to delivering durable, flame-retardant, and environmentally compliant materials tailored to the growing infrastructure and industrial demands in the region. By leveraging its global expertise and advanced compounding technologies, Shin-Etsu is strengthening its presence in the rapidly expanding Asia-Pacific PVC compound market.

- In March 2023, LG Chem introduced a new line of flexible PVC compounds specifically engineered for automotive interiors and wiring applications in South Korea. The development emphasizes LG Chem’s focus on enhancing material performance, including heat resistance, durability, and sustainability. This innovation underscores the company’s dedication to meeting the evolving needs of the automotive sector and supporting the region’s push toward high-quality, eco-friendly PVC solutions.

- In March 2023, Reliance Industries Limited successfully commissioned an upgraded PVC compounding facility in Gujarat, India, aimed at catering to the booming construction and electrical sectors. The facility leverages advanced extrusion and blending technologies to produce high-quality PVC compounds with improved mechanical properties and environmental compliance. This project highlights Reliance’s role in driving industrial growth and supporting urbanization through reliable, cost-effective PVC materials.

- In February 2023, Formosa Plastics Corporation announced a strategic partnership with leading construction material suppliers across Southeast Asia to expand the adoption of dry and wet PVC compounds for pipes, flooring, and electrical insulation applications. The collaboration is designed to enhance supply chain efficiency and ensure consistent material quality, reinforcing Formosa Plastics’ commitment to supporting regional industrial and infrastructure development.

- In January 2023, Solvay S.A. unveiled its latest range of non-plasticized PVC compounds at the Asia-Pacific Polymer Expo 2023 in Singapore. The compounds feature improved thermal stability, flame retardancy, and recyclability, making them ideal for building and construction, automotive, and electrical applications. This product launch highlights Solvay’s focus on integrating advanced materials technology to meet the region’s increasing demand for high-performance, sustainable PVC solutions.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Asia Pacific Pvc Compound Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Asia Pacific Pvc Compound Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Asia Pacific Pvc Compound Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.