Asia Pacific Rett Syndrome Market

Market Size in USD Billion

USD

5.54 Billion

USD

163.76 Billion

2024

2032

USD

5.54 Billion

USD

163.76 Billion

2024

2032

| 2025 - 2032 | |

| USD 5.54 Billion | |

| USD 163.76 Billion | |

| % | |

|

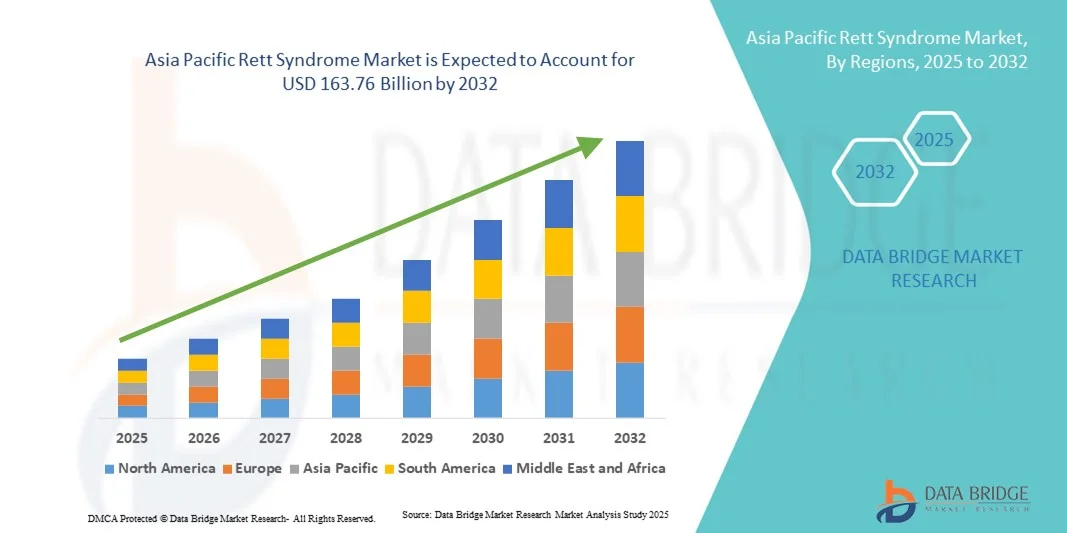

Asia Pacific Rett Syndrome Market Size

- The Asia Pacific Rett Syndrome market size was valued at USD 5.54 billion in 2024 and is expected to reach USD 163.76 billion by 2032, at a CAGR of 52.70% during the forecast period

- The Rett Syndrome market growth is largely fueled by increasing research and development activities aimed at understanding the genetic mechanisms behind the disorder, particularly MECP2 gene mutations, and the development of innovative therapeutic approaches such as gene therapy and neuro-restorative treatments

- Furthermore, the growing prevalence of Rett Syndrome among female populations, coupled with rising awareness initiatives and improved diagnostic capabilities, is driving greater demand for advanced treatment options and supportive care solutions. These converging factors are accelerating the uptake of Rett Syndrome therapies, thereby significantly boosting the industry's growth

Asia Pacific Rett Syndrome Market Analysis

- Rett Syndrome, a rare neurodevelopmental disorder primarily affecting females, has witnessed growing medical attention due to advancements in genetic research, particularly surrounding the MECP2 gene mutation, which has led to the exploration of targeted therapies and gene-editing technologies

- The increasing demand for effective rett syndrome treatments is driven by rising awareness among healthcare professionals and families, expanded diagnostic programs, and ongoing clinical trials focusing on symptomatic management and potential disease-modifying drugs

- China dominated the rett syndrome market with the largest revenue share of 38.9% in 2024, driven by increased investments in rare disease research, government initiatives supporting genetic and neurological disorder awareness, and the presence of advanced biotechnology and pharmaceutical companies

- India is expected to be the fastest-growing country in the rett syndrome market during the forecast period, with a projected CAGR of 9.7% from 2025 to 2032. Growth is primarily fueled by rising awareness of neurological and genetic disorders, expanding pediatric healthcare networks, and increasing government support for rare disease management

- The Branded segment dominated the largest market revenue share of 72.0% in 2024, reflecting the premium pricing and high development costs associated with orphan-designation therapeutics, investigator drugs, and specialized formulations often used in Rett care

Report Scope and Rett Syndrome Market Segmentation

|

Attributes |

Rett Syndrome Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Asia Pacific Rett Syndrome Market Trends

Enhanced Convenience Through AI and Digital Health Integration

- A significant and accelerating trend in the rett syndrome market is the deepening integration of artificial intelligence (AI) and digital health technologies for early diagnosis, patient monitoring, and personalized therapy. This convergence is revolutionizing Rett Syndrome care by enabling more accurate assessments, continuous monitoring, and optimized treatment outcomes

- For instance, AI-powered diagnostic systems are being developed to analyze patient movement patterns, eye-tracking data, and brain activity, which helps in early identification of Rett Syndrome and tracking disease progression. Similarly, AI-integrated wearable devices can assist clinicians in remotely monitoring vital signs and behavioral changes, providing real-time alerts to caregivers and healthcare providers

- The incorporation of AI in digital health platforms allows for predictive analytics to anticipate symptom flare-ups, improve therapy planning, and adjust treatment protocols. Moreover, voice-assisted technologies are being adapted to help non-verbal Rett patients communicate, improving their quality of life and social interaction

- The seamless integration of digital tools with healthcare systems facilitates centralized data management and coordinated care. Through a single digital platform, clinicians can access patient histories, monitor treatment responses, and collaborate with multidisciplinary teams, ensuring efficient and data-driven care delivery

- This trend toward intelligent, adaptive, and patient-centered healthcare is fundamentally transforming the management of Rett Syndrome across the region. Consequently, biotech companies and digital health startups are investing in AI-driven platforms that enhance patient engagement, therapy adherence, and long-term outcomes

- The growing demand for AI-supported Rett Syndrome management solutions is being driven by rising healthcare digitization, increasing focus on rare disease care, and the need for remote patient monitoring, particularly in underserved regions

Asia Pacific Rett syndrome Market Dynamics

Driver

Growing Research Initiatives and Technological Advancements in Rare Disease Management

- The expanding focus on rare neurological disorders, supported by government initiatives, research collaborations, and growing awareness, is a major driver of the Rett Syndrome market growth

- For instance, in May 2024, Neurogene Inc. and University College London expanded their partnership for clinical trials on gene therapy targeting MECP2 mutations, a key cause of Rett Syndrome. Such collaborations are accelerating the development of advanced therapeutic options and driving innovation in the region

- Advances in gene therapy, RNA modulation, and AI-assisted drug discovery are opening new possibilities for personalized Rett Syndrome treatments. Furthermore, telemedicine and remote healthcare platforms are enabling continuous patient support, particularly in areas with limited access to specialized care

- The increasing prevalence of rare disease registries and the integration of digital tools for early diagnosis are expected to further enhance patient identification, contributing to market expansion

Restraint/Challenge

Limited Access to Specialized Care and High Treatment Costs

- Despite growing technological advancements, limited access to specialized healthcare facilities remains a major challenge. Many regions face shortages of trained neurologists and rehabilitation experts, delaying accurate diagnosis and treatment

- High treatment costs, including those for gene therapy, physiotherapy, and advanced rehabilitation devices, pose financial challenges for families, particularly in low- and middle-income countries

- For instance, in October 2024, reports from the International Rett Syndrome Foundation (IRSF) highlighted that the average annual treatment expense for advanced Rett care exceeded USD 60,000 in some parts of the Middle East, making therapies unaffordable for a large portion of patients

- In addition, the lack of healthcare infrastructure, low reimbursement coverage for rare diseases, and insufficient awareness among general practitioners further restrain market growth

- Addressing these barriers requires increased government investment, cross-border research funding, and public-private partnerships aimed at improving rare disease care accessibility. Moreover, expanding affordable AI-driven and telehealth solutions could bridge the gap between patients and specialized Rett Syndrome centers, ensuring sustainable growth of the market across the region

Asia Pacific Rett Syndrome Market Scope

The market is segmented on the basis of type, stages, treatment type, drug type, route of administration, end user, and distribution channel.

- By Types

On the basis of types, the Rett syndrome market is segmented into Classic Rett Syndrome and Atypical Rett Syndrome. The Classic Rett Syndrome segment dominated the largest market revenue share of 64.2% in 2024, reflecting its higher diagnostic recognition and more consistent clinical profile versus atypical variants. Classic Rett typically follows a well-characterized course with regression of acquired skills after a period of normal development, which concentrates clinical attention, referral patterns, and therapeutic interventions in this group. Because classic Rett presents with hallmark phenotypes and is associated with pathogenic MECP2 mutations in the majority of cases, it attracts proportionally greater diagnostic testing, specialist referrals, and enrollment in observational cohorts. The result is a concentration of healthcare spending — genetic testing, multidisciplinary care, seizure management, and supportive therapies — in classic cases. Payers and hospitals more commonly code and reimburse classic Rett encounters, making it the primary revenue contributor in registries and specialty clinics. Clinical trial programs historically recruit predominantly classic Rett patients for endpoint consistency, further reinforcing market focus. Advocacy groups and foundations direct much of their diagnostic and caregiver support toward classic Rett, increasing uptake of services. In many high-income markets, newborn screening discussions and earlier genetic testing pipelines favor canonical MECP2 presentations, perpetuating the segment’s lead. Continuing research into genotype–phenotype correlations in classic Rett sustains investment into diagnostics and supportive care pathways. Overall, classic Rett’s clearer clinical and genetic definition drives its dominant market share across diagnostics, therapeutics, and care services.

The Atypical Rett Syndrome segment is expected to record the fastest CAGR of 11.4% from 2025 to 2032, reflecting expanded molecular diagnosis and broader case ascertainment. Increased access to next-generation sequencing and improved clinician awareness are uncovering atypical and variant presentations that were previously misdiagnosed or undetected, expanding the patient pool. As laboratories lower testing costs and as newborn/pediatric genetic panels widen, more atypical cases are being identified, which increases demand for specialist clinics and tailored supportive therapies. Growth is also supported by research interest in non-MECP2 genetic contributors and epigenetic modulators that may explain atypical phenotypes, stimulating targeted clinical programs. Pharmaceutical and biotech exploratory programs are beginning to include atypical cohorts in early-phase trials, increasing therapeutic demand. Patient advocacy and registry expansion efforts are specifically seeking atypical patients to improve natural history data, which drives diagnostic service uptake. In addition, telemedicine and decentralized care models improve access for patients with less classical phenotypes who live far from centers of excellence, accelerating service penetration. Health systems updating coding and reimbursement for rare neurological disorders also enhance coverage for atypical presentations. The combination of better detection, research inclusion, and service access underpins rapid growth for this segment.

- By Stages

On the basis of stages, the Rett syndrome market is segmented into Stage I Early Onset, Stage II Rapid Destruction, Stage III Plateau, and Stage IV Late Motor Deterioration. The Stage III Plateau segment dominated the largest market revenue share of 43.7% in 2024, because many patients spend extended periods in the plateau phase where chronic management, rehabilitation, seizure control, and supportive therapies are most intensive and recurring. During Stage III, families and clinicians focus on long-term care plans — physiotherapy, occupational therapy, feeding support, and anticonvulsant management — which generate steady recurring revenues for clinics and service providers. Specialized outpatient programs, home-care packages, adaptive equipment procurement, and ongoing monitoring increase resource utilization in this phase. Insurance authorizations and established care pathways are often optimized around plateau-phase needs, making reimbursement more predictable for providers. Clinical trials targeting symptomatic management (e.g., seizure reduction, motor function support) frequently enroll plateau-phase patients, concentrating research resources and funding in this stage. Registries and natural history studies often have their largest datasets for plateau-stage participants, which attracts clinician expertise and service development. The plateau stage’s extended duration and multifaceted care needs — respiratory, nutritional, orthopedic — translate into sustained market value across multiple product and service categories. Hospitals and specialty centers therefore report the greatest volume of billed services and device utilization for Stage III cohorts. Educational and respite care services for plateau patients also contribute to the segment’s market share.

The Stage I Early Onset segment is projected to exhibit the fastest CAGR of 12.0% from 2025 to 2032, because improved early detection and expanding newborn/pediatric genetic panels are enabling diagnosis at younger ages. Early-stage identification opens windows for early intervention programs, enrollment in early-phase therapeutic trials, and initiation of supportive therapies that were previously delayed, driving demand for pediatric specialty services. Screening initiatives, clinician education, and more routine use of exome sequencing in infants with developmental delay are increasing case ascertainment in Stage I. Early intervention models include feeding support, developmental therapy, and early seizure surveillance, all of which generate new recurring revenues and create pathways for disease-modifying trials. Payers are increasingly receptive to funding early intervention given evidence for improved long-term outcomes, which supports service expansion. Biotech programs focusing on gene-targeting therapies also prioritize early-diagnosed infants for potential maximal benefit, concentrating trial activity and associated healthcare utilization in Stage I. The net effect is a rapid expansion of diagnostic, therapeutic, and support services targeted at early-stage cohorts.

- By Treatment Type

On the basis of treatment category, the Rett syndrome market is segmented into Drug Class, Therapy Type, and Others. The Therapy Type segment dominated the largest market revenue share of 51.9% in 2024, because multidisciplinary supportive therapies — physiotherapy, occupational therapy, speech and feeding therapy, behavioral interventions — represent the backbone of current Rett care and account for sustained clinic visits and reimbursed services. Therapy-based care is highly utilized across all stages, is typically long-term, and involves a broad set of providers (therapists, nutritionists, neurologists), creating multiple revenue streams for clinical practices and rehabilitation centers. Many healthcare systems and insurers recognize the functional benefits of therapy, which leads to recurring authorizations and bundled payments for chronic neurodevelopmental care. Therapy demand also fuels allied product markets, such as adaptive feeding devices, orthoses, positioning aids, and communication supports. Professional training programs and certification pathways for Rett-specific therapy approaches further expand the provider base. Furthermore, schools and community programs increasingly integrate therapy services, broadening the payer mix and increasing covered sessions. All these factors combine to make therapy the leading treatment category in market value.

The Drug Class segment is expected to record the fastest CAGR of 13.1% from 2025 to 2032, driven by accelerating clinical development of targeted pharmacologic approaches including small molecules, antisense oligonucleotides, gene therapy platforms, and neuroactive agents aimed at core symptoms. The pipeline acceleration is attracting venture and pharma investment into MECP2-targeted strategies and symptomatic pharmacotherapies for seizures, breathing irregularities, and motor dysfunction, increasing demand for drug manufacturing, distribution, and specialist prescribing. Early regulatory approvals or accelerated pathways for orphan indications can rapidly scale market uptake for novel drug classes. Increasing numbers of investigator-initiated and industry trials expand clinical service needs and drug utilization in specialty centers. The maturation of manufacturing capacity for oligonucleotide and gene-modifying products also supports commercial readiness. Patient advocacy groups facilitating trial recruitment and early access programs drive adoption once therapies are approved. As disease-modifying candidates progress toward late-stage trials, market value tied to drug classes will expand faster than legacy supportive services.

- By Drug Type

On the basis of drug type, the Rett syndrome market is segmented into Branded and Generics. The Branded segment dominated the largest market revenue share of 72.0% in 2024, reflecting the premium pricing and high development costs associated with orphan-designation therapeutics, investigator drugs, and specialized formulations often used in Rett care. Branded products — whether anticonvulsants repurposed for Rett, novel neuroactive small molecules, or proprietary supportive formulations — command higher margins and are typically procured through specialty pharmacies and hospital formularies, concentrating revenue in branded channels. Intellectual property protection, limited manufacturer competition, and the need for specialist dispensing arrangements sustain branded product pricing. For rare disorders, branded drugs often include risk-sharing or access programs that centralize distribution through specialty networks, increasing visible market share. In addition, newly approved orphan drugs are commonly branded and marketed through partnership programs with patient groups, which amplifies commercial uptake. The combined effects of concentrated prescribing in specialty centers and brand premiuming explain branded dominance in the current market landscape.

The Generics segment is expected to achieve the fastest CAGR of 14.5% from 2025 to 2032, as patent expirations of older anticonvulsants and symptomatic agents, plus manufacturing scale-up of repurposed small molecules, create opportunities for lower-cost generic offerings and broadened access. As generics enter formularies and retail/online pharmacy channels, per-patient drug costs decline and treatment volumes increase, expanding market penetration. Growing demand in emerging markets and public health procurement programs drives rapid uptake of affordable generics. Generic competition also pressures prices, which increases utilization and total volume, particularly for widely used symptomatic medications. Regulatory pathways that streamline generic approval for narrow-indication drugs further accelerate entry. The increased availability of generics spurs inclusion in government treatment programs and insurance formularies, expanding patient access and driving the segment’s accelerated growth.

- By Route Of Administration

On the basis of route of administration, the Rett syndrome market is segmented into Oral, Parenteral, and Others. The Oral route dominated the largest market revenue share of 68.4% in 2024, because most symptomatic medications (antiepileptics, muscle relaxants, supportive neuroactive agents) and many adjunctive therapies are delivered orally with convenient dosing that supports home administration and outpatient management. Oral formulations reduce the need for clinic-based administration, improve adherence in children and adolescents, and are readily dispensed via retail and hospital pharmacies. The convenience and lower administration cost of oral drugs favor their inclusion in chronic care plans and reimbursement policies. Caregiver familiarity and well-established pediatric dosing protocols for oral medications underpin broad use. Supply chains for oral medications are mature and widely distributed, which sustains market volume. Patient preference for non-invasive routes and clinician willingness to manage regimens at home further entrench oral delivery as the primary route.

The Parenteral route is expected to show the fastest CAGR of 15.8% from 2025 to 2032, driven by the commercial maturation of advanced therapeutics (gene therapies, enzyme replacement concepts, and ASOs) that require intravenous or intrathecal delivery. Such disease-modifying approaches necessitate clinic or hospital administration, specialized cold-chain logistics, and infusion services, all of which generate rapid growth in parenteral product demand and service provision. Investments in infusion centers, hospital pharmacy capacity, and trained clinical teams expand parenteral delivery readiness. As late-stage trial results for parenteral biologics or gene therapies emerge, regulatory approvals would create immediate market uptake via hospital channels. The higher unit prices of parenteral biologics also amplify revenue growth relative to volume, accelerating overall segment CAGR. Expanded reimbursement frameworks for complex biologic administration further support rapid adoption of parenteral routes.

- By End User

On the basis of end user, the Rett syndrome market is segmented into Hospitals, Specialty Clinics, Research Organisations, and Others. The Hospitals segment dominated the largest market revenue share of 56.5% in 2024, as hospitals provide comprehensive multidisciplinary care, inpatient management for severe complications, access to diagnostic labs, and authorized administration sites for advanced therapies. Hospital systems host neurology, pediatric, respiratory, and nutrition services required by Rett patients, concentrating clinical encounters and revenue there. Complex interventions — parenteral drug administration, surgical procedures for scoliosis, and inpatient seizure monitoring — are predominantly hospital-based, increasing billable services. Hospitals also participate in clinical trials and registries, which further concentrates research-related spending and infrastructure costs within these institutions. Public and private hospital networks’ procurement frameworks and purchasing power also direct device and drug channel flows, adding to revenue concentration. Training programs and center-of-excellence designations are often hospital-linked, improving referral capture. All these functions combine to make hospitals the principal end-user market for Rett services and products.

The Research Organisations segment is expected to grow the fastest at a CAGR of 16.2% from 2025 to 2032, driven by expanding basic and translational research into MECP2 biology, gene-editing technologies, and biomarker development. Increased grant funding, public–private partnerships, and industry-sponsored trials boost demand for specialized services, reagents, and contract research capacity. As gene-targeting approaches advance, research organisations play a critical role in preclinical development and early human trials, attracting investment and service contracts. The proliferation of patient registries and natural history studies also requires research infrastructure and data management services, which escalates spending in this segment. Collaborations between academia and biotech accelerate translational pipelines, further amplifying research organisation market share. Growth in CRO capabilities for rare disease programs and regulatory incentives for orphan drug development sustain high CAGR for this end-user group.

- By Distribution Channel

On the basis of distribution channel, the Rett syndrome market is segmented into Hospital Pharmacy, Online Pharmacy, Retail Pharmacy, and Others. The Hospital Pharmacy segment dominated the largest market revenue share of 49.7% in 2024, reflecting the concentration of specialty product dispensing (parenteral biologics, gene therapy administration kits, hospital-only formulations) and in-house pharmacy services required for complex Rett care. Hospital pharmacies manage authorized distribution for high-cost orphan drugs, coordinate infusion and cold-chain logistics, and support clinical trial drug supply, making them central to the Rett therapeutic supply chain. Their integration with inpatient and outpatient services facilitates bundled care delivery and simplifies reimbursement. Hospital pharmacies also provide medication counseling, adherence monitoring, and clinical pharmacists’ oversight, which are particularly important for multi-drug regimens and high-risk pediatric populations. Specialty procurement contracts and tendering for orphan products further concentrate distribution value in hospital pharmacy channels.

The Online Pharmacy channel is projected to expand the fastest with a CAGR of 17.0% from 2025 to 2032, fueled by telemedicine adoption, caregiver preference for home delivery of chronic oral medications and supportive consumables, and improved regulatory frameworks enabling remote dispensing for rare disease patients. Online pharmacies reduce access barriers for families living far from centers of excellence by delivering routine medications, nutritional supplements, and device consumables directly to homes. Integration with electronic prescriptions, patient portals, and specialty pharmacy programs allows continuity of care and simplifies refill logistics for lifelong therapies. The increasing comfort with e-commerce for health products, plus logistics improvements for temperature-sensitive shipments, underpins rapid online channel growth. As more supportive and symptomatic medications for Rett become available through licensed e-pharmacies, caregivers will increasingly rely on online distribution, amplifying this channel’s fast expansion.

Asia Pacific Rett Syndrome Market Regional Analysis

- The Asia-Pacific rett syndrome market is poised to grow at the fastest CAGR of 10.3% during the forecast period of 2025 to 2032, driven by increasing government focus on rare disease management, advancements in genomic research, and growing awareness among healthcare professionals and parents

- Countries such as China, Japan, and India are at the forefront of regional progress, supported by expanding healthcare infrastructure, rising healthcare expenditure, and the growing presence of pharmaceutical and biotechnology companies focusing on neurological and genetic disorders

- Furthermore, the region’s emphasis on early diagnosis, coupled with collaborations between global and local research organizations, is enhancing treatment access and accelerating clinical developments for Rett Syndrome across Asia-Pacific

China Rett Syndrome Market Insight

China rett syndrome market dominated the Rett Syndrome market with the largest revenue share of 38.9% in 2024, driven by increased investments in rare disease research, government initiatives supporting genetic and neurological disorder awareness, and the presence of advanced biotechnology and pharmaceutical companies. The country's continued expansion of pediatric neurology centers and the inclusion of Rett Syndrome in various rare disease registries have enhanced early diagnosis and patient management. Furthermore, collaborations between Chinese research institutes and global biotech firms are leading to innovative therapeutic developments and expanded clinical trials, reinforcing China’s leadership position in the Asia-Pacific Rett Syndrome market.

India Rett Syndrome Market Insight

India rett syndrome market is expected to be the fastest-growing country in the Rett Syndrome market during the forecast period, with a projected CAGR of 9.7% from 2025 to 2032. Growth is primarily fueled by rising awareness of neurological and genetic disorders, expanding pediatric healthcare networks, and increasing government support for rare disease management. The Indian government’s initiatives to include rare diseases in public health programs, alongside improved access to diagnostic services and genetic testing, are significantly improving early identification of Rett Syndrome cases. In addition, collaborations between research organizations, hospitals, and global pharmaceutical companies are promoting the development of novel therapies and clinical studies, positioning India as a rapidly emerging hub for Rett Syndrome research and treatment innovation

Asia Pacific Rett Syndrome Market Share

The Rett Syndrome industry is primarily led by well-established companies, including:

- Anavex Life Sciences (U.S.)

- Neuren Pharmaceuticals (Australia)

- Acadia Pharmaceuticals Inc. (U.S.)

- Taysha Gene Therapies (U.S.)

- Novartis AG (Switzerland)

- Biogen Inc. (U.S.)

- AveXis (U.S.)

- Anavex Corp (U.S.)

- Neurogene Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Roche Holding AG (Switzerland)

- Marinus Pharmaceuticals (U.S.)

- GW Pharmaceuticals (U.K.)

- Johnson & Johnson (U.S.)

- Pfizer Inc. (U.S.)

- Ultragenyx Pharmaceutical Inc. (U.S.)

- Astellas Pharma Inc. (Japan)

- Ovid Therapeutics (U.S.)

- Novaremed AG (Switzerland)

Latest Developments in Asia Pacific Rett Syndrome Market

- In March 2023, the U.S. Food and Drug Administration (FDA) approved Trofinetide (brand name DAYBUE) for the treatment of Rett syndrome in patients aged 2 years and older, marking the first ever therapy approved for this rare neurodevelopmental disorder

- In April 2024, Acadia Pharmaceuticals Inc. announced that Health Canada accepted for filing its new drug submission for Trofinetide (DAYBUE) and granted Priority Review, moving the therapy closer to approval in the Canadian market

- In May 2025, Taysha Gene Therapies announced positive clinical data from Part A of its REVEAL Phase 1/2 trial of investigational gene therapy TSHA‑102 in Rett syndrome, with 100 % of treated patients (in the small cohort) gaining or regaining at least one developmental milestone, and the U.S. FDA agreed to the design for the next pivotal Part B study

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.