Asia Pacific Skin Graft Market

Market Size in USD Million

USD

281.40 Million

USD

549.28 Million

2025

2033

USD

281.40 Million

USD

549.28 Million

2025

2033

| 2026 - 2033 | |

| USD 281.40 Million | |

| USD 549.28 Million | |

| % | |

|

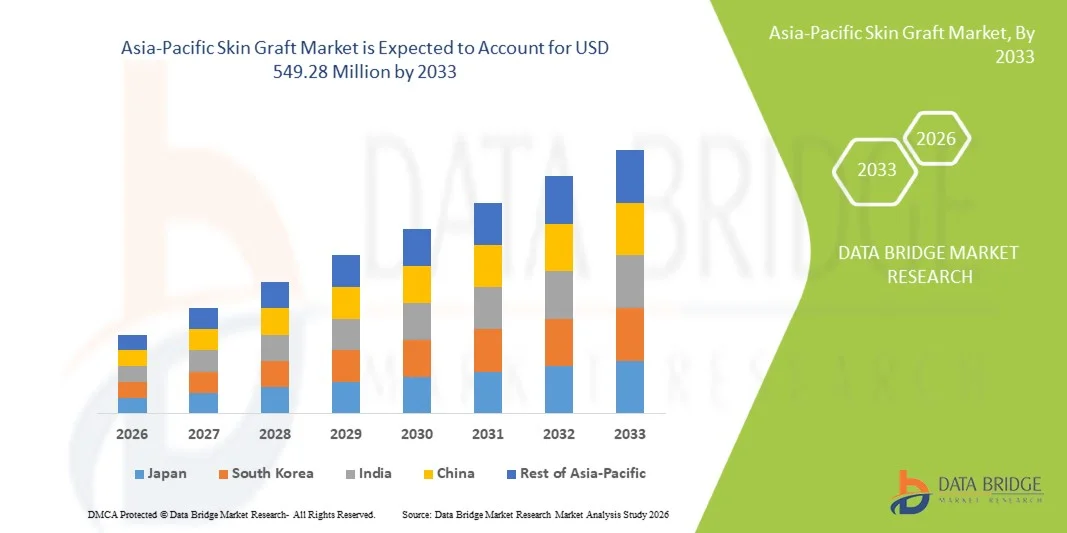

Asia-Pacific Skin Graft Market Size

- The Asia-Pacific Skin Graft Market size was valued at USD 281.4 Million in 2025 and is expected to reach USD 549.28 Million by 2033, at a CAGR of 8.72% during the forecast period

- The market growth is largely fueled by the increasing incidence of burn injuries, chronic wounds, and skin-related disorders, along with advancements in surgical techniques and wound care management, leading to improved treatment outcomes in both hospital and clinical settings

- Furthermore, rising demand for effective wound healing solutions, growing awareness about reconstructive and cosmetic procedures, and advancements in bioengineered and synthetic graft technologies are establishing skin grafts as essential treatment options. These converging factors are accelerating the uptake of Skin Graft solutions, thereby significantly boosting the industry's growth

Asia-Pacific Skin Graft Market Analysis

- Skin grafts, used for the treatment of burn injuries, chronic wounds, and reconstructive surgeries, are increasingly vital in modern healthcare settings due to their effectiveness in promoting wound healing, reducing infection risks, and improving patient recovery outcomes

- The escalating demand for skin graft solutions is primarily fueled by the rising incidence of burn cases, increasing prevalence of chronic wounds such as diabetic ulcers, and growing adoption of advanced wound care and reconstructive procedures

- China dominated the Asia-Pacific Skin Graft Market with the largest revenue share of approximately 35.9% in 2025, supported by rapidly expanding healthcare infrastructure, increasing incidence of burn injuries and chronic wounds, and growing adoption of advanced wound care technologies. The country is witnessing substantial growth in skin graft procedures across hospitals, burn centers, and specialty clinics due to rising awareness and demand for effective and faster healing solutions

- India is expected to be the fastest-growing region in the Asia-Pacific Skin Graft Market during the forecast period, registering a CAGR of approximately 9.1%, driven by increasing healthcare investments, growing awareness of advanced wound care treatments, expanding hospital networks, and rising adoption of bioengineered and synthetic skin graft solutions

- The split-thickness segment dominated the largest market revenue share of 45.3% in 2025, driven by its widespread use in treating burns and large surface wounds

Report Scope and Asia-Pacific Skin Graft Market Segmentation

|

Attributes |

Skin Graft Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

• Integra LifeSciences Corporation (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Asia-Pacific Skin Graft Market Trends

“Increasing Adoption of Advanced Wound Care and Regenerative Solutions”

- A significant and accelerating trend in the Asia-Pacific Skin Graft Market is the growing adoption of advanced wound care solutions and regenerative treatment approaches aimed at improving healing outcomes and reducing recovery time. This trend is largely driven by the rising prevalence of chronic wounds, burns, and surgical procedures requiring effective skin repair

- For instance, biologically derived grafts such as allografts and xenografts are increasingly being utilized in hospitals and burn care centers due to their ability to promote faster tissue regeneration and reduce the risk of infection. Similarly, the use of bioengineered skin substitutes is gaining traction as a reliable alternative to traditional grafting techniques

- Advancements in skin graft technologies, including improved preservation techniques, enhanced biocompatibility, and better integration with host tissues, are significantly improving clinical outcomes. These innovations enable more efficient wound closure and minimize complications such as graft rejection or scarring

- The increasing integration of skin graft procedures into standard wound management protocols is further supporting market growth. Healthcare providers are adopting comprehensive treatment approaches that combine grafting with advanced dressings and supportive therapies to enhance patient recovery

- This trend toward more effective, reliable, and patient-centric treatment solutions is reshaping clinical practices in wound care and reconstructive surgery. Consequently, leading companies are focusing on developing next-generation graft materials with improved healing properties and ease of application

- The demand for advanced skin graft solutions is growing rapidly across hospitals, specialty clinics, and ambulatory surgical centers, as healthcare providers increasingly prioritize faster healing, reduced hospital stays, and improved patient outcomes

Asia-Pacific Skin Graft Market Dynamics

Driver

“Rising Incidence of Chronic Wounds and Burn Injuries”

- The increasing prevalence of chronic wounds, including diabetic foot ulcers, pressure ulcers, and venous leg ulcers, is a major driver for the Asia-Pacific Skin Graft Market. In addition, the rising number of burn injuries and trauma cases is significantly contributing to the demand for effective skin repair solutions

- For instance, the growing global burden of diabetes has led to a higher incidence of non-healing wounds, prompting healthcare providers to adopt advanced skin grafting techniques to accelerate healing and prevent complications such as infections or amputations

- Healthcare professionals are increasingly recognizing the clinical benefits of skin grafts in promoting faster wound closure, reducing pain, and improving overall treatment outcomes, which is further supporting market growth

- Moreover, the rising number of reconstructive and cosmetic surgeries is driving the adoption of skin graft procedures, particularly in cases requiring tissue regeneration and aesthetic restoration

- The growing emphasis on improving patient outcomes, reducing hospital stays, and minimizing long-term complications is encouraging the widespread use of skin grafts across hospitals and specialized wound care centers

Restraint/Challenge

“High Treatment Costs and Limited Accessibility in Developing Regions”

- The high cost associated with advanced skin graft procedures and bioengineered skin substitutes remains a significant challenge for market growth, particularly in developing regions with limited healthcare budgets. Treatment costs often include surgical procedures, hospitalization, and post-operative care, making it less accessible to a broader patient population

- For instance, healthcare facilities in low- and middle-income countries may face difficulties in adopting advanced grafting technologies due to financial constraints and lack of reimbursement support. This limits the availability of effective treatment options for patients suffering from severe wounds and burns

- In addition, limited awareness regarding advanced wound care solutions and lack of trained healthcare professionals can hinder the effective use of skin graft technologies in certain regions. Inadequate training and infrastructure may lead to suboptimal treatment outcomes

- Challenges related to graft rejection, risk of infection, and complications associated with certain graft types can also create hesitation among patients and healthcare providers, particularly when alternative treatments are available

- Overcoming these challenges will require the development of cost-effective grafting solutions, improved healthcare infrastructure, enhanced training programs for medical professionals, and increased awareness regarding the benefits of advanced skin graft treatments in improving patient recovery and quality of life

Asia-Pacific Skin Graft Market Scope

The market is segmented on the basis of graft type, graft thickness, application, equipment, and end users.

• By Graft Type

On the basis of graft type, the Asia-Pacific Skin Graft Market is segmented into autologous, isogeneic, allogeneic, xenogeneic, and prosthetic. The autologous segment dominated the largest market revenue share of 42.6% in 2025, driven by its high success rate and minimal risk of immune rejection since the graft is harvested from the patient’s own body. This type is widely preferred in burn treatment and reconstructive surgeries due to its superior compatibility and faster healing outcomes. Hospitals and surgeons prioritize autografts for critical wound management procedures. The increasing number of burn injuries and trauma cases globally is further supporting demand. Technological advancements in graft harvesting and transplantation techniques are improving procedural outcomes. Favorable clinical guidelines and higher patient acceptance are also contributing to its dominance. The reduced risk of disease transmission enhances reliability. Growing healthcare infrastructure in emerging economies supports wider adoption.

The allogeneic segment is expected to witness the fastest CAGR of 10.9% from 2026 to 2033, fueled by the increasing availability of donor skin through skin banks and rising demand for temporary wound coverage. Allografts are extensively used in severe burns and large wound cases where autografts are not immediately feasible. Advancements in preservation and storage technologies are improving graft viability and usability. Increasing awareness about organ and tissue donation is also supporting segment growth. Hospitals are increasingly adopting allografts for emergency care and staged surgical procedures. The expansion of tissue banking facilities globally is accelerating availability. Reduced procedure time compared to autografts enhances clinical efficiency. Growing R&D in bioengineered skin substitutes is further boosting adoption.

• By Graft Thickness

On the basis of graft thickness, the Asia-Pacific Skin Graft Market is segmented into split-thickness, full-thickness, and composite graft. The split-thickness segment dominated the largest market revenue share of 45.3% in 2025, driven by its widespread use in treating burns and large surface wounds. These grafts are easier to harvest and have a higher success rate due to better revascularization. Surgeons prefer split-thickness grafts for their flexibility and ability to cover extensive wound areas. Faster healing at the donor site also contributes to their popularity. Increasing incidence of burn injuries and chronic wounds globally supports demand. Technological advancements in dermatome devices are enhancing graft precision. Hospitals favor this approach for cost-effectiveness and efficiency. High clinical success rates further reinforce dominance.

The full-thickness segment is expected to witness the fastest CAGR of 10.5% from 2026 to 2033, driven by increasing demand for aesthetically superior outcomes in reconstructive and cosmetic surgeries. Full-thickness grafts provide better color match and texture, making them ideal for visible body areas such as the face. Rising awareness regarding cosmetic procedures is fueling adoption. Surgeons are increasingly opting for full-thickness grafts in specialized procedures. Growth in plastic and reconstructive surgeries globally supports expansion. Improved surgical techniques are enhancing graft survival rates. Higher patient satisfaction is contributing to demand. Advancements in wound care management are further boosting segment growth.

• By Application

On the basis of application, the Asia-Pacific Skin Graft Market is segmented into extensive wound, burns, extensive skin loss due to infection, skin cancers, and others. The burns segment accounted for the largest market revenue share of 40.8% in 2025, driven by the high global incidence of burn injuries requiring immediate and effective wound coverage. Skin grafting is a critical component in burn treatment to prevent infection and fluid loss. Hospitals extensively utilize grafting procedures for severe burn cases. Increasing industrial accidents and domestic burn cases are contributing to demand. Government initiatives for burn care management are supporting adoption. Technological advancements in grafting techniques improve survival outcomes. Availability of specialized burn care centers enhances treatment access. Rising awareness regarding early treatment further boosts segment growth.

The skin cancers segment is expected to witness the fastest CAGR of 11.3% from 2026 to 2033, driven by the rising global prevalence of skin cancer and increasing surgical excision procedures. Skin grafting is widely used post-tumor removal for reconstruction. Growing awareness about early diagnosis and treatment is supporting demand. Advancements in oncological surgeries are improving outcomes. Increasing geriatric population contributes to higher incidence rates. Demand for aesthetic reconstruction post-surgery is also rising. Hospitals and specialty clinics are key adopters. Improved healthcare access in emerging markets accelerates growth.

• By Equipment

On the basis of equipment, the Asia-Pacific Skin Graft Market is segmented into dermatome, general surgical instruments, consumables, and others. The dermatome segment dominated the largest market revenue share of 38.7% in 2025, driven by its essential role in harvesting skin grafts with precision and uniform thickness. Advanced dermatomes improve surgical efficiency and reduce procedural complications. Hospitals and surgical centers rely heavily on these devices for consistent outcomes. Technological innovations such as powered and electric dermatomes enhance usability. Increasing number of grafting procedures globally supports demand. Surgeons prefer dermatomes for accuracy and reduced tissue damage. Rising healthcare investments further boost adoption. Continuous product upgrades strengthen market presence.

The consumables segment is expected to witness the fastest CAGR of 11.7% from 2026 to 2033, fueled by the recurring need for surgical supplies such as blades, dressings, and fixation materials. Increasing volume of grafting procedures directly drives consumable demand. Hospitals and clinics require continuous replenishment, ensuring steady growth. Advancements in wound care products improve healing outcomes. Growing focus on infection control boosts adoption of high-quality consumables. Emerging markets contribute significantly due to expanding healthcare access. Cost-effectiveness and high turnover rate support rapid growth.

• By End Users

On the basis of end users, the Asia-Pacific Skin Graft Market is segmented into hospitals and clinics, academic and research, and others. The hospitals and clinics segment dominated the largest market revenue share of 48.9% in 2025, driven by the high volume of surgical procedures and availability of advanced healthcare infrastructure. Hospitals are primary centers for burn treatment and reconstructive surgeries. Presence of skilled professionals and specialized equipment supports adoption. Increasing patient admissions for trauma and chronic wounds drive demand. Government funding and insurance coverage enhance accessibility. Continuous advancements in surgical techniques improve outcomes. Hospitals remain the preferred choice for complex procedures.

The academic and research segment is expected to witness the fastest CAGR of 10.8% from 2026 to 2033, driven by increasing research activities in regenerative medicine and bioengineered skin substitutes. Universities and research institutions are focusing on innovative grafting technologies. Rising funding for tissue engineering supports growth. Collaborations between academia and industry accelerate innovation. Development of artificial skin and advanced graft materials enhances future prospects. Growing interest in clinical trials contributes to expansion. Improved research infrastructure in emerging economies further boosts segment growth.

Asia-Pacific Skin Graft Market Regional Analysis

- Asia-Pacific dominated the Asia-Pacific Skin Graft Market with a significant revenue share in 2025, supported by rapidly expanding healthcare infrastructure, increasing prevalence of burn injuries and chronic wounds, and rising adoption of advanced wound care technologies across the region. The market is witnessing growing utilization of skin graft procedures across hospitals, burn centers, and specialty clinics, driven by increasing demand for effective tissue repair and faster healing outcomes

- Healthcare providers in the region are increasingly focusing on improving patient outcomes, reducing recovery time, and enhancing wound management practices, leading to widespread adoption of advanced skin graft solutions, including bioengineered skin substitutes and allografts

- This growth is further supported by rising healthcare expenditure, improving access to medical facilities, and ongoing advancements in regenerative medicine, establishing skin grafting as a critical component in modern wound care and reconstructive procedures

China Asia-Pacific Skin Graft Market Insight

The China Asia-Pacific Skin Graft Market dominated the Asia-Pacific region with the largest revenue share of approximately 35.9% in 2025, driven by rapidly expanding healthcare infrastructure, increasing incidence of burn injuries and chronic wounds, and growing adoption of advanced wound care technologies. The country is experiencing substantial growth in skin graft procedures across hospitals, burn centers, and specialty clinics due to rising awareness and demand for effective and faster healing solutions. Additionally, increasing investments in healthcare and the presence of both domestic and international market players are further supporting market expansion.

India Asia-Pacific Skin Graft Market Insight

The India Asia-Pacific Skin Graft Market is expected to be the fastest-growing region in Asia-Pacific during the forecast period, registering a CAGR of approximately 9.1%. This growth is driven by increasing healthcare investments, growing awareness of advanced wound care treatments, and the expanding network of hospitals and specialty clinics across the country. Rising incidences of chronic wounds, burn injuries, and surgical procedures, along with increasing adoption of bioengineered and synthetic skin graft solutions, are further contributing to the rapid growth of the market in India.

Asia-Pacific Skin Graft Market Share

The Skin Graft industry is primarily led by well-established companies, including:

• Integra LifeSciences Corporation (U.S.)

• Zimmer Biomet Holdings, Inc. (U.S.)

• Smith & Nephew plc (U.K.)

• MiMedx Group, Inc. (U.S.)

• Organogenesis Holdings Inc. (U.S.)

• Avita Medical, Inc. (U.S.)

• Mölnlycke Health Care AB (Sweden)

• Coloplast A/S (Denmark)

• 3M Health Care (U.S.)

• B. Braun S.E. (Germany)

• Convatec Group plc (U.K.)

• Integra LifeSciences (U.S.)

• Kerecis (Iceland)

• AlloSource (U.S.)

• LifeNet Health (U.S.)

• Medtronic plc (Ireland)

• Cook Biotech Incorporated (U.S.)

• Acelity L.P. Inc. (U.S.)

• Derma Sciences (U.S.)

• Wright Medical Group N.V. (Netherlands)

Latest Developments in Asia-Pacific Skin Graft Market

- In December 2021, key industry players such as AVITA Medical, Organogenesis Inc., and MiMedx Group were featured in a global industry outlook highlighting their expansion in advanced skin graft substitutes and bioengineered tissue solutions. These developments emphasized growing investment in regenerative medicine and innovative grafting approaches to address chronic wounds and burn injuries worldwide

- In June 2023, AVITA Medical received U.S. FDA approval for the RECELL® Autologous Cell Harvesting Device for the treatment of full-thickness skin defects, expanding its clinical use beyond burn care. The system allows clinicians to create spray-on skin cells from a patient’s own tissue, reducing the need for traditional grafting and improving healing outcomes, thereby strengthening the adoption of regenerative skin graft technologies globally

- In July 2022, manufacturers across the global market introduced next-generation dermatomes and skin grafting instruments, improving surgical precision, minimizing tissue damage, and enhancing graft survival rates. These technological advancements supported wider clinical adoption of skin grafting procedures in hospitals and specialized wound care centers

- In March 2024, Medline Industries received U.S. FDA authorization for its Autologous Regeneration of Tissue (ART) Skin Harvesting System, a minimally invasive device that uses fine needles to harvest skin grafts. This innovation marked a shift toward less invasive graft collection techniques and improved patient recovery outcomes in global surgical practices

- In September 2024, global market participants accelerated research and development in bioengineered skin substitutes and artificial skin technologies, focusing on improving graft integration, reducing scarring, and enhancing long-term healing outcomes. This trend reflected the growing importance of regenerative medicine in the evolution of skin graft procedures

- In May 2025, the global Asia-Pacific Skin Graft Market witnessed continued commercialization of advanced grafting systems and regenerative solutions, driven by increasing demand for burn care, chronic wound management, and reconstructive surgeries. Companies expanded their product portfolios and geographic presence to strengthen market penetration and improve patient outcomes worldwide

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.