Asia Pacific Snack Food Packaging Market

Market Size in USD Billion

USD

9.30 Billion

USD

15.26 Billion

2025

2033

USD

9.30 Billion

USD

15.26 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.30 Billion | |

| USD 15.26 Billion | |

| % | |

|

Asia-Pacific Snack Food Packaging Market Overview

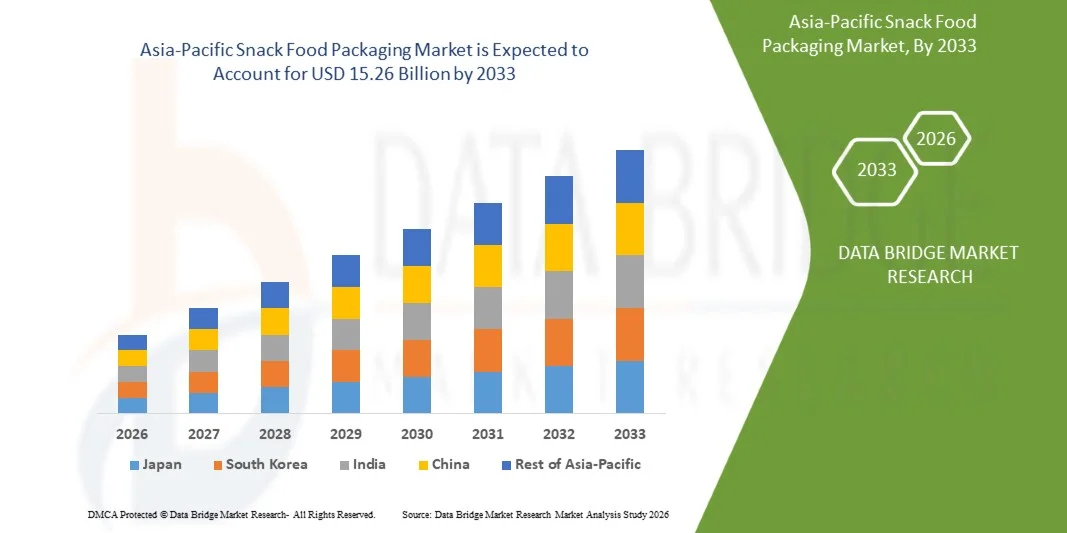

The Asia-Pacific Snack Food Packaging Market was valued at USD 9.30 billion in 2025 and is projected to reach USD 15.26 billion by 2033, growing at a CAGR of 6.5% from 2026 to 2033. Sustainability has emerged as a major transformation driver across the APAC snack food packaging market. Regulatory pressures, corporate sustainability commitments, and growing consumer awareness are accelerating the adoption of recyclable, recycled-content, paper-based, and mono-material packaging solutions.

Packaging companies are increasingly developing designs that reduce material consumption while maintaining functionality and product protection. Investments in recycling infrastructure, circular economy initiatives, and advanced packaging technologies are further reshaping industry dynamics. In addition, digital printing, smart labeling, and automation technologies are creating new opportunities for operational efficiency and brand engagement. As snack consumption expands across both developed and emerging markets, the industry continues to evolve toward packaging solutions that balance performance, sustainability, convenience, and cost effectiveness.

Market Size & Forecast

- Global Market Value (2025): USD 9.30 Billion

- Expected Market Value (2033): USD 15.26 Billion

- Forecast CAGR (2026–2033): 6.5%

- Leading Region in 2025: China

- Fastest Growing Region: India

Key Market Trends & Insights

- China dominated the Asia-Pacific Snack Food Packaging Market with the largest revenue share of 31.32% in 2025, due to its vast snack food manufacturing base, expanding packaged food consumption, rapid urbanization, and strong demand for convenient and on-the-go food products. The country's well-established packaging industry, growing adoption of flexible packaging formats, increasing investments in sustainable packaging solutions, and the continued expansion of e-commerce and modern retail channels further contributed to its market leadership.

- The flexible packaging segment led the market with a 66.49% share in 2025, driven by its cost-effectiveness, lightweight nature, superior barrier properties, and ability to extend product shelf life. Growing demand for convenient, resealable, and portable snack packaging, coupled with increasing adoption of pouches, sachets, and wraps by manufacturers seeking to reduce material usage and transportation costs, further strengthened the segment’s market dominance.

- India is expected to be the fastest-growing region at a CAGR of 7.5% from 2026 to 2033, fueled by rising consumption of packaged snacks, increasing urbanization, growing disposable incomes, and the expansion of organized retail and e-commerce channels. The country's large young population, evolving consumer lifestyles, greater demand for convenience foods, and increasing investments in food processing and sustainable packaging technologies are further accelerating the adoption of advanced snack food packaging solutions.

- Flexible packaging is the fastest-growing packaging type, projected to register a CAGR of 6.7%, reflecting the surge in demand for convenient, resealable, and portable snack packaging, coupled with increasing adoption of pouches, sachets, and wraps by manufacturers seeking to reduce material usage and transportation costs.

- The plastic segment dominates the packaging material category with a 54.16% revenue share in 2025, led by its versatility, durability, lightweight characteristics, and excellent barrier properties that help preserve product freshness and extend shelf life. Widespread use of plastic films, laminates, and pouches in snack food packaging, combined with their cost-effectiveness, design flexibility, and compatibility with high-speed packaging processes, has reinforced the segment’s leading position across the market.

- Heat seal segment accounts for 43.62% of the market, preferred for its strong sealing performance, ability to preserve product freshness, enhanced protection against moisture and contamination, and compatibility with high-speed packaging operations. Its cost-effectiveness, reliability across a wide range of packaging materials, and suitability for both flexible and rigid snack packaging formats have made it a widely adopted sealing solution among snack food manufacturers.

- The paper & paperboard segment is the fastest-growing packaging material category, with a CAGR of 7.3%, driven by increasing consumer preference for environmentally sustainable packaging, growing regulatory pressure to reduce plastic waste, and rising adoption of recyclable and biodegradable materials by snack food manufacturers. Advances in barrier coating technologies, improved printability, and the ability of paper-based packaging to support brand sustainability goals are further accelerating demand across the snack food industry.

Report Scope and Asia-Pacific Snack Food Packaging Market Segmentation

|

Attributes |

Asia Pacific Snack Food Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia-Pacific Snack Food Packaging Market Trends

Trend: Growing Adoption of Sustainable, Recyclable, and Eco-Friendly Packaging Solutions

The increasing adoption of sustainable, recyclable, and eco-friendly packaging solutions is creating a significant growth opportunity for the global snack food packaging market. Consumers, retailers, food manufacturers, and regulatory authorities are placing greater emphasis on reducing packaging waste, lowering carbon footprints, and improving recyclability. Snack food brands are therefore investing in paper-based packaging, mono-material recyclable films, post-consumer recycled (PCR) plastics, compostable materials, and fiber-based alternatives to conventional multi-layer plastics. These innovations are helping manufacturers meet sustainability commitments while enhancing brand value and consumer trust. Furthermore, advancements in barrier technologies are enabling sustainable materials to provide the shelf-life protection required for snacks such as chips, nuts, granola bars, confectionery products, and baked goods. As governments worldwide introduce circular economy initiatives and extended producer responsibility (EPR) regulations, packaging companies that can deliver recyclable and resource-efficient solutions are gaining a competitive advantage. This transition is expected to accelerate demand for innovative snack food packaging formats and materials over the coming years.

For instance,

- In April 2025, Amcor announced a partnership with Riverside Natural Foods to launch MadeGood Trail Mix Bars in AmFiber paper-based packaging. The new packaging solution delivers curbside recyclability in the paper stream while maintaining product protection and performance standards required for snack products. The wrapper uses FSC-certified fiber and represents a category-first recyclable paper-based packaging solution for snack bars. This demonstrates the growing commercialization of recyclable paper packaging for snack foods, creating new opportunities for sustainable packaging suppliers and converters.

- In February 2025, Berry Global and Mars announced the rollout of pantry jars made with 100% recycled plastic for M&M’S, SKITTLES, and STARBURST products. According to the company announcement, the packaging transition is expected to eliminate more than 1,300 metric tons of virgin plastic annually while maintaining recyclability and product functionality. The increasing use of recycled-content packaging by major snack and confectionery brands is driving demand for advanced sustainable packaging materials and recycling infrastructure.

The transition toward sustainable, recyclable, and eco-friendly packaging is emerging as a major growth catalyst for the global snack food packaging market. Investments by leading packaging manufacturers and snack food brands in paper-based materials, recycled-content plastics, fiber-based packaging, and recycle-ready flexible formats are accelerating the commercialization of sustainable solutions. As consumer preferences, corporate sustainability commitments, and regulatory requirements continue to align, demand for innovative, environmentally responsible snack packaging is expected to expand significantly, creating long-term opportunities for packaging material producers, converters, and technology developers.

Asia-Pacific Snack Food Packaging Market Dynamics

Key Market Driver: Increasing Demand for Convenience and Ready-To-Eat Snack Products

The growing consumer preference for convenience foods and ready-to-eat (RTE) snack products is a major factor driving demand in the global snack food packaging market. Rapid urbanization, increasingly busy lifestyles, rising workforce participation, and the expansion of on-the-go consumption habits have led consumers to seek snack products that are portable, easy to store, and ready for immediate consumption. This shift has encouraged food manufacturers to introduce a wider range of packaged snacks, including healthy snacks, protein snacks, chips, nuts, trail mixes, and meal-replacement products. As a result, packaging has become a critical component in ensuring product freshness, shelf-life extension, portability, convenience, and brand differentiation. Demand is increasing for resealable pouches, single-serve packs, lightweight flexible packaging, tamper-evident formats, and sustainable packaging solutions that enhance consumer convenience while maintaining product quality throughout distribution and retail channels.

For instance,

- In April 2026, MarketScreener reported that Duni Group launched its “Sealable Ronda” paper-based bowl for ready-to-eat meals and convenience foods. The packaging features hermetic sealing and modified atmosphere packaging (MAP) technology to extend shelf life and maintain freshness. This development highlights how the growing demand for ready-to-eat and on-the-go food products is driving the need for advanced and convenient packaging solutions.

- In April 2026, Business Standard reported that Good Goodies launched a new healthy snack brand in India featuring a packaging-led transparency strategy, including front-of-pack ingredient visibility. The initiative aims to help consumers quickly evaluate products and make informed purchasing decisions. This development highlights how rising demand for ready-to-eat and healthy snacks is driving packaging innovations that improve convenience, product visibility, and consumer engagement.

The increasing popularity of convenience foods and ready-to-eat snack products is significantly accelerating growth in the global snack food packaging market. As consumers seek portable, shelf-stable, and easy-to-consume food options, manufacturers are investing in packaging solutions that enhance freshness, convenience, safety, and sustainability. Recent product launches, packaging innovations, and expanding snack portfolios across the food industry demonstrate how evolving consumption patterns are creating sustained demand for advanced snack food packaging formats worldwide.

Key Restraint/Challenge: Fluctuations in Raw Material Costs Impacting Production Economics

The snack food packaging market faces a significant restraint from fluctuations in raw material costs, which directly impact packaging production economics and profitability. Snack food packaging relies heavily on materials such as polyethylene (PE), polypropylene (PP), polyethylene terephthalate (PET), aluminum foil, paperboard, and recycled fiber, all of which are subject to volatility driven by crude oil prices, energy costs, geopolitical tensions, supply chain disruptions, trade policies, and changing demand-supply dynamics. Because packaging manufacturers often operate under long-term supply contracts with food companies, sudden increases in raw material prices can compress margins before cost increases can be passed on to customers. In addition, unpredictable material pricing makes procurement planning, inventory management, and investment decisions more challenging for packaging producers. For snack food manufacturers, higher packaging costs can increase overall product costs, reduce profitability, and potentially lead to price increases that affect consumer demand. As a result, ongoing volatility in resin, paper, and metal markets continues to create uncertainty across the snack food packaging value chain and acts as a restraint on market growth.

For instance,

- In June 2024, Sonoco Products Company announced a minimum 6% price increase for all converted paperboard products in the U.S. and Canada. According to the company, the increase was necessary because of continued rises in the cost of uncoated recycled paperboard (URB), its primary raw material, along with broader inflationary pressures affecting production. This demonstrates how rising raw material costs directly increase packaging production expenses, forcing manufacturers to raise prices and affecting the economics of snack food packaging production.

- In April 2025, Flexible Packaging Europe (FPE) reported that polyethylene prices increased significantly during the first quarter of 2025, with HDPE rising by 3% and LDPE by 4% compared with the previous quarter. FPE attributed the increases to raw material cost inflation, supply-chain bottlenecks, and lower import availability. Polyethylene is a key material used in flexible snack packaging. Rising PE prices increase packaging conversion costs and reduce margin stability for packaging manufacturers.

Fluctuating prices of resins, paperboard, aluminum, and other packaging substrates remain a major challenge for the global snack food packaging market. Volatility driven by inflation, energy prices, geopolitical tensions, trade policies, and supply-chain disruptions increases production costs, complicates procurement planning, and creates margin pressure for packaging manufacturers. As raw material uncertainty persists, both packaging suppliers and snack food producers must continuously adjust pricing, sourcing, and inventory strategies, making raw material cost fluctuations a significant restraint on the market’s long-term growth and profitability.

Key Market Opportunity: Advancements in Smart Packaging Technologies for Enhanced Consumer Interaction and Product Traceability

The growing adoption of smart packaging technologies is creating a significant opportunity for the snack food packaging market by transforming packaging from a passive protective medium into an interactive communication and traceability platform. Technologies such as QR codes, NFC (Near Field Communication), RFID tags, GS1 Digital Link-enabled 2D barcodes, augmented reality (AR), and cloud-connected packaging solutions allow snack manufacturers to engage consumers directly through smartphones while simultaneously improving supply chain visibility. Consumers increasingly seek transparency regarding ingredient sourcing, nutritional content, sustainability practices, and product authenticity. Smart packaging enables brands to provide this information instantly through digital interfaces, enhancing trust and brand loyalty. Furthermore, regulators and retailers are placing greater emphasis on product traceability and transparency, encouraging the adoption of connected packaging systems that can track products across the supply chain. For snack food companies, these technologies create opportunities for personalized marketing campaigns, loyalty programs, real-time consumer feedback, anti-counterfeiting measures, recall management, and sustainability communication. As digitalization becomes a core element of food packaging strategies, smart packaging is expected to emerge as a key differentiator that enhances consumer experience while delivering operational efficiencies and traceability benefits.

For instances,

- In April 2025, GS1 (Global Standards Organization) highlighted the advancement of GS1 Digital Link technology as part of the global transition toward next-generation 2D barcodes. The organization stated that a single QR code can connect consumers to product information, certifications, usage instructions, sustainability data, and traceability records while maintaining compatibility with retail scanning systems. GS1 noted that Digital Link-enabled packaging strengthens brand loyalty and improves supply chain traceability by linking physical products to dynamic digital content. This demonstrates how snack food manufacturers can use a single smart code on packaging to enhance consumer interaction and provide end-to-end product traceability, creating new value beyond traditional packaging functions.

- In March 2025, Packaging World reported discussions at the AIPIA & AWA Smart Packaging World Congress regarding GS1 Digital Link and connected packaging solutions. Industry experts emphasized that the technology enables greater transparency, traceability, and consumer engagement by transforming conventional barcodes into digital gateways that connect shoppers with detailed product information and brand experiences. development highlights growing industry investment in connected packaging, opening opportunities for snack brands to strengthen consumer engagement while improving visibility across supply chains.

Advancements in smart packaging technologies are creating a strong growth opportunity for the global snack food packaging market by enabling brands to deliver greater transparency, traceability, and personalized consumer experiences. As QR codes, GS1 Digital Link standards, NFC-enabled solutions, and connected packaging platforms gain wider adoption, snack manufacturers can transform packaging into a powerful digital engagement channel while meeting increasing demands for supply-chain visibility and product authenticity. The convergence of consumer expectations, digital transformation initiatives, and evolving traceability requirements is expected to accelerate the deployment of smart packaging solutions across the snack food industry, supporting both brand value creation and operational efficiency.

Asia-Pacific Snack Food Packaging Market Scope

The Asia-Pacific Snack Food Packaging Market is segmented on the basis of packaging type, packaging material, closure type, barrier property, pack size, label type, packaging technology, application, and distribution channel.

- By Packaging Type

On the basis of packaging type, the global snack food packaging market is segmented into flexible packaging, rigid packaging, secondary & multipack packaging, and semi-rigid packaging. The flexible packaging segment led the market with a 66.49% share in 2025, driven by its cost-effectiveness, lightweight nature, superior barrier properties, and ability to extend product shelf life. Growing demand for convenient, resealable, and portable snack packaging, coupled with increasing adoption of pouches, sachets, and wraps by manufacturers seeking to reduce material usage and transportation costs, further strengthened the segment’s market dominance.

Flexible packaging is the fastest-growing packaging type, projected to register a CAGR of 6.7%, reflecting the surge in demand for convenient, resealable, and portable snack packaging, coupled with increasing adoption of pouches, sachets, and wraps by manufacturers seeking to reduce material usage and transportation costs.

- By Packaging Material

On the basis of packaging material, the global snack food packaging market is segmented into plastic, paper & paperboard, laminates & composites, bio-based/sustainable materials, metal, and glass. The plastic segment dominated the market with a 54.16% share in 2025, owing to its excellent barrier properties, lightweight nature, durability, and cost-effectiveness. Plastic packaging provides effective protection against moisture, oxygen, and contamination, helping extend product shelf life and maintain snack quality. Its versatility in various packaging formats, compatibility with high-speed production processes, and ability to support attractive printing and branding further contribute to its widespread adoption in the snack food packaging industry.

The paper & paperboard segment is the fastest-growing packaging material category, with a CAGR of 7.3%, driven by increasing consumer preference for environmentally sustainable packaging, growing regulatory pressure to reduce plastic waste, and rising adoption of recyclable and biodegradable materials by snack food manufacturers. Advances in barrier coating technologies, improved printability, and the ability of paper-based packaging to support brand sustainability goals are further accelerating demand across the snack food industry.

- By Closure Type

On the basis of closure type, the Asia-Pacific Snack Food Packaging Market is segmented into heat seal, zipper/resealable, tamper-evident seals, pull-tab/tear-off, snap-on lids, and press-fit caps. The heat seal segment led the market with a 43.62% share in 2025, supported by its superior sealing strength, ability to maintain product freshness, and effectiveness in protecting snack products from moisture, oxygen, and contamination. Its compatibility with high-speed packaging lines, cost efficiency, and widespread use across flexible packaging formats such as pouches, bags, and wraps have made heat sealing the preferred closure method for snack food manufacturers throughout the region.

The zipper/resealable segment is expected to experience the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by increasing consumer demand for convenience, product freshness, and portion-controlled consumption. Resealable packaging allows multiple uses while preserving flavor, texture, and shelf life, making it particularly attractive for premium and family-sized snack products. Additionally, changing lifestyles, growing preference for on-the-go snacking, and manufacturers’ focus on enhancing user experience and reducing food waste are accelerating the adoption of zipper and resealable packaging formats across the Asia Pacific region.

- By Barrier Property

On the basis of barrier property, the global snack food packaging market is segmented into high barrier, medium barrier, active & modified atmosphere packaging, and low barrier. The high barrier segment dominated the market with a share of 49.18% in 2025 due to its ability to provide superior protection against moisture, oxygen, light, and other external contaminants that can compromise product quality and shelf life. High-barrier packaging is widely used for snack products requiring extended freshness, flavor retention, and enhanced food safety during storage and transportation. Growing demand for packaged snacks, longer distribution networks, and manufacturers’ focus on reducing product spoilage and food waste have further strengthened the adoption of high-barrier packaging solutions.

The low barrier segment is anticipated to witness the fastest CAGR of 7.2% from 2026 to 2033, driven by increasing demand for cost-effective packaging solutions for short shelf-life snack products, growing adoption of lightweight packaging materials, and rising emphasis on recyclability and sustainability. Manufacturers are increasingly utilizing low-barrier packaging for products that require basic protection while reducing material usage and packaging costs. Additionally, advancements in eco-friendly films and consumer preference for sustainable packaging formats are further supporting segment growth.

- By Pack Size

On the basis of pack size, the global snack food packaging market is segmented into multi-serve packs, single-serve packs, family packs, and bulk/institutional packs. The multi-serve packs segment dominated the market with a share of 38.85% in 2025 due to their strong appeal among households seeking convenience, value, and extended consumption. These packs offer cost advantages compared to smaller formats while allowing consumers to consume snacks over multiple occasions. Growing demand for at-home snacking, increasing purchases through supermarkets and hypermarkets, and the widespread adoption of resealable packaging solutions that help maintain product freshness have further supported the dominance of the multi-serve packs segment.

The single-serve packs segment is expected to witness the fastest CAGR of 7.1% from 2026 to 2033, driven by growing consumer preference for convenience, portability, and portion-controlled snacking. Busy lifestyles, increasing demand for on-the-go food products, and rising health consciousness are encouraging consumers to choose individually packaged snack portions that support controlled consumption and reduce food waste. Additionally, the expansion of modern retail, e-commerce platforms, and impulse purchasing trends is further boosting demand for single-serve snack packaging across the Asia Pacific region.

- By Label Type

On the basis of label type, the global snack food packaging market is segmented into pressure-sensitive labels (PSL), shrink sleeve labels, wrap-around labels, digital printed labels, smart & interactive labels, and in-mold labels (IML). The pressure-sensitive labels (PSL) segment dominated the market with a 41.65% share in 2025 due to its versatility, cost-effectiveness, and compatibility with a wide range of packaging materials and product categories. PSLs offer strong adhesion without requiring heat, water, or solvents for application, making them highly suitable for high-speed production environments across industries such as food & beverages, pharmaceuticals, personal care, household products, and logistics.

The smart & interactive labels segment is expected to witness the fastest CAGR of 7.4% from 2026 to 2033, this growth is driven by increasing demand for enhanced consumer engagement, product traceability, and brand transparency. Technologies such as QR codes, NFC tags, and augmented reality-enabled labels allow consumers to access product information, nutritional details, promotional content, and sustainability credentials through smartphones. Additionally, rising adoption of digital packaging solutions, growing focus on supply chain visibility, and manufacturers’ efforts to improve customer experience and brand differentiation are accelerating the deployment of smart and interactive labels in snack food packaging.

- By Packaging Technology

On the basis of packaging technology, the global snack food packaging market is segmented into thermoforming/form-fill-seal (FFS), modified atmosphere packaging (MAP), blow molding/injection molding, vacuum packaging, and aseptic/retort processing. The modified atmosphere packaging (MAP) segment dominated the market with a share of 42.18% in 2025 due to its ability to significantly extend product shelf life by controlling the composition of gases inside the package and reducing exposure to oxygen and moisture. MAP helps preserve the freshness, flavor, texture, and nutritional quality of snack products while minimizing the need for preservatives. Its effectiveness in reducing product spoilage, supporting longer distribution cycles, and meeting consumer demand for high-quality packaged foods has made it a widely adopted packaging technology among snack food manufacturers globally.

The modified atmosphere packaging (MAP) segment is expected to witness the fastest CAGR of 7.2% from 2026 to 2033, driven by the growing need to extend shelf life, preserve product freshness, and maintain the quality of snack foods without relying heavily on preservatives. MAP technology helps control oxygen and moisture levels within the package, reducing spoilage and improving product stability during storage and transportation. Increasing demand for premium packaged snacks, expansion of modern retail channels, and rising focus on food safety and waste reduction are further accelerating the adoption of MAP solutions across the Asia-Pacific Snack Food Packaging Market.

- By Application

On the basis of application, the global snack food packaging market is segmented into chips & crisps, nuts & seeds, confectionery snack products, extruded snacks, bakery snacks, pretzels & crackers, protein/energy bars, popcorn, functional/specialty snacks, baked snacks, dried fruits, and others. The chips & crisps segment dominated the market with a share of 24.85% in 2025 due to its large consumer base, high consumption frequency, and extensive availability across retail channels worldwide. Chips and crisps require specialized packaging solutions that provide excellent moisture, oxygen, and contamination barriers to maintain freshness, texture, and flavor. The segment's dominance is further supported by continuous product innovations, growing demand for convenient snack options, and increasing adoption of flexible packaging formats that offer portability, product visibility, and extended shelf life.

The popcorn segment is expected to witness the fastest CAGR of 8.3% from 2026 to 2033, driven by increasing consumer preference for healthier and low-calorie snack alternatives. Rising demand for flavored, premium, and ready-to-eat popcorn products is encouraging manufacturers to invest in advanced packaging solutions that enhance product freshness and shelf appeal. Additionally, growing distribution through supermarkets, convenience stores, and e-commerce platforms is further accelerating demand for innovative and sustainable popcorn packaging formats.

- By Distribution Channel

On the basis of distribution channel, the global snack food packaging market is segmented into direct and indirect. The direct segment dominated the market with a share of 56.97% in 2025 due to strong relationships between packaging manufacturers and large food processing companies. Direct sales channels enable customized packaging solutions, bulk procurement, faster communication, and greater control over product specifications and quality requirements. Additionally, long-term supply agreements and increasing demand for tailored packaging formats among major snack brands continue to support the segment's leading position.

The indirect segment is expected to witness the fastest CAGR of 7.0% from 2026 to 2033, driven by the expanding presence of distributors, packaging suppliers, and third-party sales networks that improve market accessibility for small and medium-sized snack manufacturers. Growing demand for flexible purchasing options, wider product availability, and the rapid expansion of regional packaging distribution networks are further supporting the growth of indirect sales channels across emerging and developing markets.

Asia-Pacific Snack Food Packaging Market Regional Analysis

China dominated the Asia-Pacific Snack Food Packaging Market with the largest revenue share of 31.32% in 2025, due to its vast snack food manufacturing base, expanding packaged food consumption, rapid urbanization, and strong demand for convenient and on-the-go food products. The country's well-established packaging industry, growing adoption of flexible packaging formats, increasing investments in sustainable packaging solutions, and the continued expansion of e-commerce and modern retail channels further contributed to its market leadership.

India Snack Food Packaging Market Insight

The India snack food packaging market is experiencing robust growth, driven by rising consumption of packaged snacks, rapid urbanization, and changing consumer lifestyles. Growing demand for convenient, on-the-go food products, coupled with the expansion of modern retail and e-commerce channels, is increasing the need for innovative and cost-effective packaging solutions. Additionally, investments in sustainable packaging materials, flexible packaging formats, and domestic food processing capabilities are supporting market expansion across the country.

Japan Snack Food Packaging Market Insight

The Japan snack food packaging market remains a significant contributor to regional growth, supported by a highly developed food manufacturing sector and strong emphasis on product quality, safety, and convenience. Demand for premium, functional, and environmentally friendly packaging solutions is increasing as manufacturers focus on extending shelf life and enhancing consumer experience. Technological advancements in barrier materials, smart packaging, and recyclable packaging formats continue to drive innovation and adoption across the Japanese market.

Australia Snack Food Packaging Market Insight

The Australia snack food packaging market is witnessing steady growth, supported by increasing demand for packaged and ready-to-eat snack products. Consumers' preference for convenience, portion-controlled packaging, and sustainable materials is encouraging manufacturers to adopt advanced packaging solutions. Furthermore, growing regulatory focus on reducing packaging waste and improving recyclability is accelerating investments in eco-friendly packaging technologies, strengthening market development across the country.

Indonesia Snack Food Packaging Market Insight

The Indonesia snack food packaging market is expanding rapidly due to a growing middle-class population, increasing disposable incomes, and rising consumption of packaged food products. The expansion of supermarkets, convenience stores, and online food retail platforms is boosting demand for attractive, durable, and affordable packaging solutions. In addition, increasing investments in food processing infrastructure and the adoption of flexible packaging formats are supporting long-term growth in the Indonesian snack food packaging industry.

Asia-Pacific Snack Food Packaging Market Share

The Asia Pacific snack food packaging industry is primarily led by well-established companies, including:

- Smurfit Westrock plc (Ireland)

- Amcor plc (Switzerland)

- Mondi (U.K.)

- Graphic Packaging International, LLC (U.S.)

- Sonoco Products Company (U.S.)

- Sealed Air Corporation (U.S.)

- Jinan Huafeng Printing Co., Ltd (China)

- Huhtamäki Oyj (Finland)

- SIG Combibloc Group AG (Switzerland)

- Novolex Holdings, LLC (U.S.)

- Constantia Flexibles (Austria)

- ProAmpac LLC (U.S.)

- UFlex Packaging (India)

- Inteplast Group (U.S.)

- Winpak Ltd. (Canada)

- Printpack (U.S.)

- Coveris (Austria)

- Schur Flexibles Group (Austria)

- Gualapack S.p.A. (Italy)

- Nosco, Inc. (U.S.)

- ePac Holdings, LLC (U.S.)

- Glenroy, Inc. (U.S.)

- Shako Flexipack Private Limited (India)

- Swiss Pac India (India)

- Dot Packtech (India)

- KANHA PRINT N PACK (India)

Latest Developments in Asia-Pacific Snack Food Packaging Market

- In April 2026, Amcor unveiled a new closure targeting applications such as mayonnaise, ketchup, and sweet sauces. The 55 mm Flava Flip Top Closure 38/400 is a lightweight upgrade compared to previous versions. The new generation of the 38/400 neck finish range is designed for circularity to help brand owners meet and exceed their sustainability goals. Amcor has achieved an absolute weight reduction of 1.9 g, bringing the new cap’s weight down to 8.5 g, an 18.7% relative reduction compared to the earlier generation of 55mm Flip Top Closure.

- In March 2026, Amcor offered an in-depth view of its expanded portfolio of rigid and flexible packaging solutions at Natural Products Expo West in Anaheim, California, at the Anaheim Convention Center from March 4-6, 2026.

- In June 2026, Amcor underlined its commitment to the healthcare market with a further multi-million-dollar investment in its state-of-the-art manufacturing facility in Sira, Karnataka, India. With this investment, the company has strengthened its capabilities in the design and development of high-performance healthcare packaging and patient-centric drug-delivery solutions, supporting rapidly growing demand across India and South Asia.

- In April 2025, Amcor plc completed the acquisition (combination) of Berry Global on April 30, 2025. The transaction was structured as an all-stock merger, with Berry shareholders receiving 7.25 Amcor shares for each Berry share. After closing, Berry became a wholly owned subsidiary of Amcor.

- In April 2026, Mondi opened its new packaging production facility in Pittsburgh, Pennsylvania, further expanding its manufacturing capabilities in the United States to better support customers with reliable, high-quality paper-based packaging solutions across key end markets. The new state‑of‑the‑art plant produces a wide range of paper bags for customers in the eCommerce, food, feed, building materials, and chemicals sectors.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Asia Pacific Snack Food Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Asia Pacific Snack Food Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Asia Pacific Snack Food Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.