Asia Pacific Surgical Robots Market

Market Size in USD Billion

USD

2.25 Billion

USD

5.00 Billion

2024

2032

USD

2.25 Billion

USD

5.00 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.25 Billion | |

| USD 5.00 Billion | |

| % | |

|

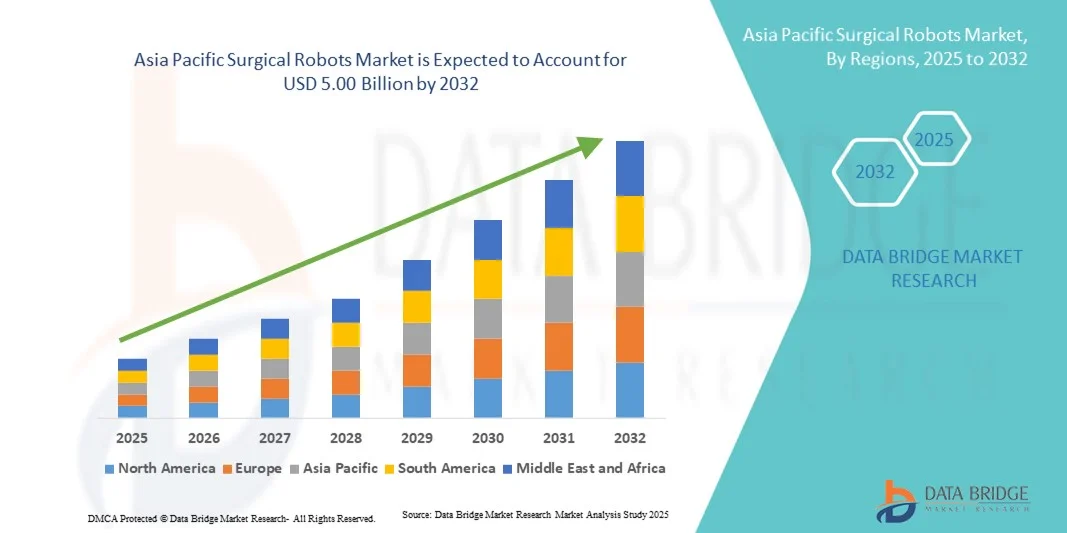

Asia Pacific Surgical Robots Market Size

- The Asia Pacific surgical robots market size was valued at USD 2.25 billion in 2024 and is expected to reach USD 5.00 billion by 2032, at a CAGR of 11.00% during the forecast period

- The market growth is largely fueled by the growing adoption of minimally invasive procedures and continuous technological advancements in robotic-assisted surgery, leading to enhanced precision, reduced recovery times, and improved patient outcomes across various specialties

- Furthermore, rising demand for efficient, user-friendly, and integrated surgical systems in hospitals and surgical centers is establishing surgical robots as a preferred solution for complex procedures. These converging factors are accelerating the uptake of Surgical Robots solutions, thereby significantly boosting the industry’s growth

Asia Pacific Surgical Robots Market Analysis

- Surgical robots, which facilitate minimally invasive and precision-assisted surgical procedures, are becoming core tools in modern healthcare by improving outcomes, reducing patient trauma, and shortening recovery periods

- The growing demand for robotic-assisted surgeries is primarily driven by rising surgical volumes, greater patient preference for minimally invasive procedures, and rapid technological advances such as AI-guided instrumentation and improved haptic feedback

- China dominated the Asia-Pacific surgical robots market with the largest revenue share of 29.7% in 2024, characterized by a mature healthcare infrastructure, strong adoption of advanced surgical technologies, and high investments in robotic-assisted procedures, with leading hospitals and specialty centers driving substantial growth across multiple surgical specialties

- India is expected to be the fastest-growing region in the Asia-Pacific surgical robots market during the forecast period, driven by rising healthcare spending, expanding hospital networks, increasing demand for minimally invasive surgeries, and growing investment in advanced medical infrastructure and training programs for robotic-assisted procedures

- The Robotic Systems segment dominated the market with the largest revenue share of 45.6% in 2024. Hospitals and high-volume surgical centers are increasingly adopting multi-arm and modular robotic platforms for enhanced precision, reduced operation time, and minimally invasive procedures

Report Scope and Surgical Robots Market Segmentation

|

Attributes |

Surgical Robots Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia Pacific Surgical Robots Market Trends

Enhanced Convenience Through AI and Advanced Automation

- A significant and accelerating trend in the Asia Pacific surgical robots market is the deepening integration with artificial intelligence (AI) and advanced automation systems. These technologies are enhancing precision, workflow efficiency, and decision-making during complex surgical procedures

- For instance, Intuitive Surgical introduced an updated version of the da Vinci Xi Surgical System in 2023, incorporating AI-driven motion scaling and enhanced 3D visualization, allowing surgeons to perform minimally invasive procedures with higher accuracy and reduced operative time

- AI integration in surgical robots enables predictive analytics, procedural guidance, and real-time error detection, improving patient outcomes and supporting surgical teams with intelligent decision-making. Furthermore, machine learning algorithms help optimize instrument usage, suggest surgical paths, and reduce intraoperative risks

- The seamless integration of surgical robots with hospital information systems (HIS) and imaging platforms facilitates centralized management of patient data, preoperative planning, and post-operative analysis, creating a unified and efficient surgical workflow

- This trend towards intelligent, precise, and highly automated robotic systems is fundamentally transforming surgical practices, driving demand for more advanced and user-friendly platforms. Companies such as Medtronic and Johnson & Johnson are focusing on AI-enabled robotics with capabilities such as haptic feedback, multi-arm coordination, and real-time data visualization

- The demand for surgical robots that combine automation, AI, and enhanced analytics is growing rapidly across both hospitals and specialty surgical centers, as healthcare providers prioritize patient safety, efficiency, and superior clinical outcomes

Asia Pacific Surgical Robots Market Dynamics

Driver

Rising Demand for Minimally Invasive and Precision Surgeries

- The growing prevalence of chronic illnesses, complex surgical cases, and an aging population is significantly driving the adoption of surgical robots across healthcare facilities. These robotic systems provide highly precise, minimally invasive procedures that reduce patient recovery times, lower complication rates, and shorten hospital stays

- For instance, in March 2022, Medtronic introduced its Hugo™ robotic-assisted surgery system in Asia Pacific, featuring AI-powered motion guidance and advanced 3D visualization. This system allows surgeons to perform intricate procedures with enhanced accuracy and efficiency, which has led to increased hospital interest and installations

- Surgical robots also support standardized procedures and data-driven insights, allowing surgical teams to optimize outcomes, reduce intraoperative errors, and streamline workflow. Hospitals are increasingly investing in these platforms not only to enhance clinical outcomes but also to attract highly skilled surgeons and improve their institutional reputation

- Furthermore, patient awareness of the benefits of robotic-assisted surgery—such as minimal scarring, faster rehabilitation, and lower risk of infection—is contributing to the surge in adoption across multiple specialties, including urology, gynecology, orthopedics, and general surgery

- The combination of advanced technology, clinical efficacy, and rising demand for efficient surgical procedures is positioning surgical robots as a core investment for modern healthcare providers, driving continuous market growth globally

Restraint/Challenge

High Initial Costs and Stringent Regulatory Compliance

- The adoption of surgical robots faces significant hurdles due to their substantial capital investment requirements

- The upfront cost for a multi-arm robotic system often exceeds USD 2 million, which includes not only the hardware but also maintenance, software updates, and specialized staff training. Smaller hospitals or clinics with limited budgets may find these costs prohibitive

- In addition, stringent regulatory standards, including approvals from the U.S. FDA, European CE marking, and country-specific healthcare certifications, can delay market entry for new products and increase compliance-related expenses for manufacturers

- The complexity of training surgical teams to effectively operate robotic systems is another challenge. Hospitals must invest in extensive education programs to ensure safety, efficiency, and optimal use of robotic platforms, which may slow adoption rates

- While technological advancements and competitive pricing are gradually reducing overall costs, the perceived financial risk of adopting advanced surgical robotics continues to pose a restraint, particularly in emerging economies

- Addressing these challenges through leasing models, government subsidies, training initiatives, and scalable robotic solutions will be crucial to enhance accessibility and support the sustainable expansion of the surgical robotics market worldwide

Asia Pacific Surgical Robots Market Scope

The market is segmented on the basis of product type, brands, application, and end-users.

- By Product Type

On the basis of product type, the Asia Pacific surgical robots market is segmented into Instruments, Robotic Systems, and Accessories and Services. The Robotic Systems segment dominated the market with the largest revenue share of 45.6% in 2024. Hospitals and high-volume surgical centers are increasingly adopting multi-arm and modular robotic platforms for enhanced precision, reduced operation time, and minimally invasive procedures. These systems integrate seamlessly with imaging solutions, hospital information systems, and AI-guided analytics, providing superior surgical outcomes and improved workflow efficiency. Leading companies like Intuitive Surgical and Medtronic continuously innovate, offering upgraded systems with new clinical capabilities and enhanced safety features. The robust clinical validation, extensive training programs, and proven patient outcomes reinforce their preference over other products. Demand is also driven by the growing number of specialty surgical centers, expansion of robotic-assisted surgeries in urology and gynecology, and rising awareness of improved recovery times. The adaptability of robotic systems across multiple surgical applications further strengthens their market leadership. Integration with digital platforms for real-time monitoring, predictive maintenance, and remote support adds additional value, making robotic systems indispensable in modern surgical care.

The Accessories and Services segment is expected to witness the fastest CAGR of 10.2% from 2025 to 2032. Growth is driven by increasing consumption of disposable instruments, specialized training programs, and maintenance packages that ensure optimal performance. Hospitals and outpatient centers are investing in bundled service offerings to reduce downtime and maximize system efficiency. Rising adoption of subscription-based service models, online technical support, and AI-powered predictive maintenance is boosting market traction. Accessories such as forceps, scalpels, and instrumentation kits are essential for robotic surgeries, creating recurring revenue opportunities. Training services for surgeons and technical staff improve the safe and effective use of surgical robots. The demand for remote software updates, integrated analytics, and compliance with hospital safety standards further propels this segment. Expanding adoption in both new and retrofit surgical units ensures continuous growth.

- By Brands

On the basis of brands, the Asia Pacific surgical robots market is segmented into DA Vinci Surgical System, CyberKnife, Renaissance, Artas, ROSA, and Others. The DA Vinci Surgical System dominated with a revenue share of 38.5% in 2024, owing to its established clinical presence, high adoption in minimally invasive procedures, and comprehensive ecosystem of instruments and software. Its precision, reproducibility, and ability to reduce complications have made it the benchmark robotic platform. Continuous AI-based upgrades, expanded surgical indications, and training programs for surgeons reinforce leadership. Strong collaborations with hospitals and research institutions enhance credibility and adoption. Its long-standing clinical success and extensive case studies support superior patient outcomes. The global reputation, robust service network, and continual software and hardware innovation further solidify market dominance.

The ROSA brand segment is projected to witness the fastest CAGR of 11.5% from 2025 to 2032, driven by neurosurgery and orthopedic robotic solutions. AI-guided planning, multi-application adaptability, and intuitive interfaces encourage adoption in hospitals and specialty centers. Clinical collaborations, evidence-based studies, and customized training programs are boosting adoption rates. The ability to integrate with hospital information systems and imaging platforms enhances precision and efficiency. Hospitals seeking specialized robotic solutions are increasingly choosing ROSA for spine, brain, and joint surgeries. Strategic partnerships with medical device distributors expand market reach. Rising awareness among surgeons about minimally invasive options is driving interest. ROSA’s modular design allows easy scaling of operations across surgical departments. Cost-effective implementation and consistent postoperative outcomes attract smaller hospitals.

- By Application

On the basis of application, the Asia Pacific surgical robots market is segmented into General Surgery, Urological, Gynaecological, Gastrointestinal, Radical Prostatectomy, Cardiothoracic Surgery, Colorectal Surgery, Radiotherapy, and Others. The Urological Surgery segment dominated with a market share of 27.4% in 2024, owing to high prevalence of prostate and kidney disorders. Robotic-assisted procedures improve precision, reduce complications, and shorten hospital stays. Widespread clinical training, availability of advanced robotic instruments, and evidence-based studies contribute to its market leadership. Hospitals prioritize adoption to attract patients and surgeons while achieving better outcomes. Integration with imaging and diagnostic tools enhances procedural accuracy. Rising geriatric population and incidence of urological conditions amplify demand. Cost savings from reduced hospital stays, fewer complications, and enhanced surgical efficiency support adoption. Availability of specialized urology-focused robotic instruments increases utilization. Institutional preference for proven robotic platforms reinforces growth. Multi-procedure compatibility ensures versatility across hospital departments. The segment benefits from continuous innovation and clinical research investments.

The Gynaecological Surgery segment is expected to witness the fastest CAGR of 9.8% from 2025 to 2032, fueled by rising demand for minimally invasive hysterectomies, myomectomies, and oncology procedures. Patient preference for faster recovery, lower complications, and minimally invasive options drives adoption. Hospitals are expanding robotic-assisted gynecological services to enhance efficiency. Advanced training programs and specialized instruments encourage adoption. Integration with imaging platforms for enhanced precision further supports growth. Expansion in outpatient surgical centers boosts accessibility. Increasing awareness among surgeons about procedural benefits accelerates uptake. Robotic systems for gynecology improve surgeon ergonomics and procedural accuracy. Rising investment in women’s health and adoption in private hospitals further propel the segment. Government initiatives promoting advanced surgical technologies add support. Growing patient awareness of robotic surgical advantages strengthens the market.

- By End-Users

On the basis of end-users, the Asia Pacific surgical robots market is segmented into Clinics, Hospitals, Ambulatory Care Centers, and Others.The Hospitals segment dominated with a revenue share of 50.2% in 2024, driven by large-scale investments in robotic platforms, high surgical volumes, and utilization across multiple specialties. Hospitals leverage robotics to improve precision, attract top surgeons, and enhance operational efficiency. Multi-disciplinary adoption across urology, gynecology, and general surgery contributes to leadership. Integration with hospital IT and analytics platforms improves surgical workflow. Continuous upgrades, staff training, and support services encourage adoption. Leading hospitals prioritize advanced surgical outcomes and reduced complications. Availability of capital investment and government incentives further support expansion. Hospitals’ preference for proven robotic systems ensures steady market share. Long-term partnerships with robotic system providers reinforce dominance. Clinical research and outcome-driven adoption validate investment.

The Ambulatory Care Centers segment is expected to witness the fastest CAGR of 12.3% from 2025 to 2032, fueled by outpatient adoption of robotic-assisted procedures. Increasing preference for same-day surgeries, minimally invasive procedures, and compact robotic platforms drives growth. Cost efficiency and patient convenience promote adoption. Integration with remote monitoring and data management tools supports scalability. Rising investments in outpatient infrastructure and surgical center expansion amplify growth. Surgeons’ preference for accessible, user-friendly robotic systems encourages uptake. Expansion of multi-specialty outpatient centers provides additional opportunities. Awareness of robotic advantages among patients and providers accelerates acceptance. Collaboration with manufacturers for specialized instruments supports adoption. Outpatient-focused robotic solutions increase flexibility and operational efficiency.

Asia Pacific Surgical Robots Market Regional Analysis

- China dominated the Asia-Pacific surgical robots market with the largest revenue share of 29.7% in 2024, characterized by a mature healthcare infrastructure, strong adoption of advanced surgical technologies, and high investments in robotic-assisted procedures, with leading hospitals and specialty centers driving substantial growth across multiple surgical specialties

- India is expected to be the fastest-growing region in the Asia-Pacific surgical robots market during the forecast period, driven by rising healthcare spending, expanding hospital networks, increasing demand for minimally invasive surgeries, and growing investment in advanced medical infrastructure and training programs for robotic-assisted procedures

- Furthermore, as APAC emerges as a hub for surgical technology development and manufacturing, the affordability and accessibility of robotic surgical systems are expanding to a wider healthcare network

China Surgical Robots Market Insight

The China surgical robots market dominated the Surgical Robots market in the Asia-Pacific region with the largest revenue share of 29.7% in 2024, characterized by a mature healthcare infrastructure, strong adoption of advanced surgical technologies, and high investments in robotic-assisted procedures. Leading hospitals and specialty centers across major cities are driving substantial growth in multiple surgical specialties, supported by government initiatives promoting high-tech healthcare solutions and domestic manufacturers producing affordable surgical robotics systems.

India Surgical Robots Market Insigh

The India surgical robots market is expected to be the fastest-growing region in the Asia-Pacific Surgical Robots market during the forecast period, driven by rising healthcare spending, expanding hospital networks, increasing demand for minimally invasive surgeries, and growing investment in advanced medical infrastructure and training programs for robotic-assisted procedures. The rapid modernization of tertiary care hospitals and increasing awareness among surgeons about robotic-assisted surgery benefits are further propelling market growth across the country.

Asia Pacific Surgical Robots Market Share

The Surgical Robots industry is primarily led by well-established companies, including:

- Intuitive Surgical Operations, Inc. (U.S.)

- Medtronic (Ireland)

- Stryker (U.S.)

- Johnson & Johnson and its affiliates (U.S.)

- Zimmer Biomet (U.S.)

- CMR Surgical Ltd. (U.K.)

- Accuray Incorporated. (U.S.)

- THINK Surgical, Inc. (U.S.)

- Renishaw (U.K.)

- Asensus Surgical US, Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Smith + Nephew (U.K.)

Latest Developments in Asia Pacific Surgical Robots Market

- In October 2024, CMR Surgical received U.S. FDA marketing authorization for its Versius Surgical System, granting initial indication for adults undergoing cholecystectomy. This modular, cart-based laparoscopic robot is now cleared for use in the U.S. healthcare market

- In January 2025, Intuitive Surgical reported fourth-quarter earnings surpassing analysts' estimates, driven by increased sales of its surgical robots. The company achieved a revenue of USD2.41 billion, marking a 25% year-over-year increase, and earnings of USD686 million. The rise in earnings was supported by an 18% increase in procedures performed with its da Vinci surgical devices and the installation of 493 da Vinci systems compared to 415 the previous year

- In July 2025, Zimmer Biomet announced a definitive agreement to acquire Monogram Technologies for approximately USD177 million. Monogram specializes in semi- and fully autonomous surgical technologies, including a semi-autonomous knee replacement system approved by the FDA in March 2025. This acquisition is part of Zimmer's strategy to enhance its robotics portfolio and broaden its presence in the growing global robotic surgery market, expected to reach USD16 billion by 2030

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.