Asia Pacific Ultrasound Probe Disinfection Market

Market Size in USD Million

USD

117.55 Million

USD

485.57 Million

2025

2033

USD

117.55 Million

USD

485.57 Million

2025

2033

| 2026 - 2033 | |

| USD 117.55 Million | |

| USD 485.57 Million | |

| % | |

|

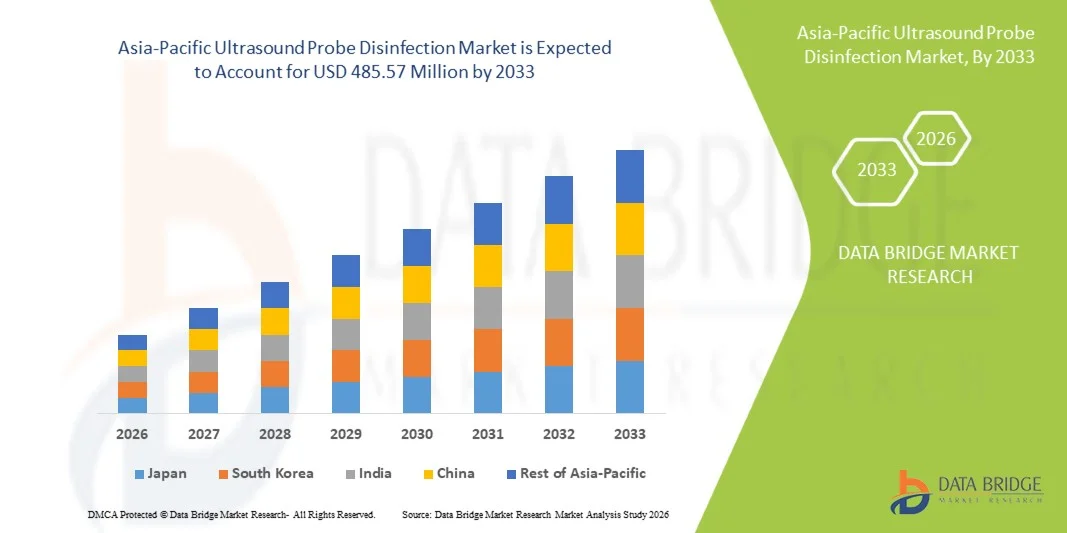

Asia-Pacific Ultrasound Probe Disinfection Market Size

- The Asia-Pacific ultrasound probe disinfection market size was valued at USD 117.55 million in 2025 and is expected to reach USD 485.57 million by 2033, at a CAGR of 19.4% during the forecast period

- The market growth is primarily driven by the increasing awareness of hospital-acquired infections (HAIs) and the rising emphasis on stringent infection control protocols across healthcare facilities in the region, leading to greater adoption of advanced probe disinfection solutions

- Furthermore, rapid expansion of diagnostic imaging services, growing patient volumes, and the modernization of healthcare infrastructure in emerging economies are strengthening demand for high-level disinfection systems, thereby significantly accelerating market growth across Asia-Pacific healthcare settings

Asia-Pacific Ultrasound Probe Disinfection Market Analysis

- Ultrasound probe disinfection solutions, ensuring high-level decontamination of diagnostic ultrasound transducers, are becoming critical components of infection prevention workflows in hospitals, diagnostic imaging centers, and ambulatory care facilities due to increasing focus on patient safety and prevention of cross-contamination in clinical diagnostics

- The escalating demand for ultrasound probe disinfection systems is primarily fueled by the rising number of ultrasound diagnostic procedures, stricter hospital infection control guidelines, and growing awareness of healthcare-associated infections (HAIs), leading to higher adoption of standardized disinfection protocols across healthcare institutions

- China dominated the ultrasound probe disinfection market with the largest revenue share of 38.6% in 2025, supported by rapid expansion of hospital infrastructure, large patient population base, increasing diagnostic imaging volumes, and strong adoption of advanced infection control technologies across healthcare facilities

- India is expected to be the fastest growing country in the ultrasound probe disinfection market during the forecast period due to expanding healthcare infrastructure, rising healthcare expenditure, increasing awareness of infection prevention standards, and growing deployment of ultrasound-based diagnostic services in both urban and semi-urban regions

- High Level Disinfection segment dominated the ultrasound probe disinfection market with a market share of 61.8% in 2025, driven by its proven efficacy in eliminating a wide range of pathogens, regulatory preference for validated sterilization methods, and its critical role in ensuring safe reuse of ultrasound probes in high-volume clinical settings

Report Scope and Asia-Pacific Ultrasound Probe Disinfection Market Segmentation

|

Attributes |

Asia-Pacific Ultrasound Probe Disinfection Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Ultrasound Probe Disinfection Market Trends

“Rising Adoption of Automated High-Level Disinfection Systems”

- A significant and accelerating trend in the Asia-Pacific ultrasound probe disinfection market is the increasing adoption of automated high-level disinfection systems integrated with infection control workflows in hospitals and diagnostic imaging centers, improving consistency, safety, and compliance with clinical hygiene standards

- For instance, advanced systems such as automated endoscope and probe reprocessors are being deployed in hospitals across China, enabling standardized disinfection cycles with minimal manual intervention and reducing the risk of human error in infection control processes

- Automation in probe disinfection enables features such as real-time cycle monitoring, digital traceability logs, and automated chemical dosing, improving compliance with hospital infection prevention protocols and enhancing patient safety in high-volume ultrasound departments

- The integration of digital tracking systems with hospital information systems facilitates centralized monitoring of disinfection records, allowing healthcare providers to maintain audit-ready documentation and ensure adherence to regulatory guidelines across diagnostic imaging units

- Growing integration of portable and compact disinfection units in outpatient clinics is further improving accessibility, enabling smaller healthcare facilities to adopt standardized infection control practices without large infrastructure requirements

- This trend towards automated, standardized, and digitally traceable disinfection processes is fundamentally reshaping clinical expectations for ultrasound hygiene management, with companies developing compact, efficient, and user-friendly disinfection units for hospital deployment

- The demand for automated high-level disinfection systems is growing rapidly across both public and private healthcare facilities, as hospitals increasingly prioritize infection control efficiency, workflow optimization, and patient safety compliance

Asia-Pacific Ultrasound Probe Disinfection Market Dynamics

Driver

“Growing Need Due to Rising Infection Control Awareness and Diagnostic Imaging Expansion”

- The increasing prevalence of hospital-acquired infections (HAIs) and the rapid expansion of diagnostic ultrasound procedures across Asia-Pacific healthcare systems is a significant driver for heightened demand for ultrasound probe disinfection solutions

- For instance, in April 2025, hospitals in India expanded infection prevention programs by upgrading ultrasound departments with dedicated high-level disinfection systems to meet stricter clinical hygiene requirements and improve patient safety outcomes

- As healthcare providers become more aware of cross-contamination risks associated with reusable ultrasound probes, disinfection systems offer advanced benefits such as validated pathogen elimination, automated cycle control, and compliance with infection prevention protocols

- Furthermore, the growing penetration of ultrasound-based diagnostics in cardiology, gynecology, and emergency care is making probe disinfection systems an essential component of routine clinical workflows across hospitals and imaging centers

- The increasing investments by governments and private healthcare providers in upgrading diagnostic imaging infrastructure are further accelerating procurement of advanced disinfection equipment across hospitals

- Rising training initiatives for healthcare staff on infection prevention practices are also improving proper usage and adherence to ultrasound probe disinfection protocols, supporting market expansion

- The rising adoption of standardized infection control protocols, along with government initiatives promoting healthcare quality improvements, is further accelerating the deployment of advanced ultrasound probe disinfection technologies in both urban and semi-urban healthcare facilities

Restraint/Challenge

“High Equipment Costs and Operational Compliance Complexity”

- Concerns surrounding the high cost of advanced ultrasound probe disinfection systems, along with operational complexity in maintaining strict disinfection protocols, pose a significant challenge to broader market penetration across cost-sensitive healthcare facilities

- For instance, smaller diagnostic clinics in Southeast Asia often delay adoption of automated disinfection systems due to budget constraints and reliance on manual disinfection methods despite increasing awareness of infection risks

- Addressing these cost-related barriers through affordable system designs, scalable disinfection solutions, and simplified operational workflows is crucial for improving adoption in emerging healthcare market

- In addition, variability in regulatory enforcement across different Asia-Pacific countries creates challenges in maintaining uniform compliance standards, requiring continuous staff training and system validation in clinical environments

- Limited availability of skilled technicians for operating advanced disinfection systems in rural and semi-urban healthcare facilities further restricts smooth implementation and consistent usage

- Frequent maintenance requirements and dependency on consumables such as disinfectant solutions also add to recurring operational costs, affecting long-term affordability for smaller healthcare providers

- While awareness of infection control is increasing, the perceived high investment requirement and operational maintenance complexity can still hinder widespread adoption, particularly in smaller healthcare facilities and rural diagnostic centers

Asia-Pacific Ultrasound Probe Disinfection Market Scope

The market is segmented on the basis of products & services, level of disinfection, type of probe, end user, and distribution channel.

- By Products & Services

On the basis of products & services, the Asia-Pacific ultrasound probe disinfection market is segmented into instruments, consumables, and services. The instruments segment dominated the market with the largest revenue share of 46.3% in 2025, driven by the high adoption of automated high-level disinfection units in hospitals and diagnostic imaging centers. Healthcare facilities increasingly prefer standalone and integrated disinfection devices to ensure standardized cleaning of ultrasound probes and reduce infection risks. The growing investment in hospital infrastructure across China and India further strengthens demand for advanced disinfection instruments. In addition, long equipment lifecycle and recurring upgrades of installed systems contribute to sustained dominance of this segment. Integration of digital monitoring and automation features also enhances adoption in large healthcare networks.

The consumables segment is expected to witness the fastest growth rate of 13.8% from 2026 to 2033, fueled by continuous usage requirements of disinfectant wipes, chemical solutions, and single-use protective covers. Rising procedural volumes in ultrasound diagnostics significantly increase recurring demand for consumables in hospitals and imaging centers. Increasing awareness regarding cross-contamination risks is driving routine replacement of disinfectant materials after every diagnostic procedure. Furthermore, expanding outpatient diagnostic services in India and Southeast Asia is accelerating consumables consumption. Hospitals are also shifting toward standardized infection control protocols, further boosting repeat purchase cycles.

- By Level of Disinfection

On the basis of level of disinfection, the market is segmented into low level disinfection, intermediate level disinfection, and high level disinfection. The high level disinfection segment dominated the market with the largest revenue share of 61.8% in 2025, driven by its critical role in eliminating a broad range of pathogens from semicritical ultrasound probes. Hospitals and diagnostic centers strongly prefer high-level disinfection to comply with strict infection prevention regulations and reduce hospital-acquired infection risks. Increasing usage of invasive and semi-invasive ultrasound procedures is further strengthening adoption. Automated HLD systems ensure standardized cleaning cycles and reduce manual errors, improving clinical safety. Growing regulatory emphasis across China, Japan, and India is reinforcing its dominance. High procedural volumes in tertiary hospitals also contribute to sustained demand.

The intermediate level disinfection segment is expected to witness the fastest growth rate of 12.9% from 2026 to 2033, driven by its cost-effectiveness and suitability for non-critical ultrasound applications. Smaller diagnostic centers and outpatient facilities are increasingly adopting intermediate-level solutions due to lower operational costs compared to HLD systems. Rising penetration of ultrasound diagnostics in semi-urban regions is further supporting demand. Hospitals are also using intermediate disinfection for lower-risk procedures to optimize workflow efficiency. Growing awareness of infection prevention in budget-constrained healthcare facilities is accelerating adoption.

- By Type of Probe

On the basis of type of probe, the market is segmented into critical devices, noncritical devices, and semicritical devices. The semicritical devices segment dominated the market with the largest revenue share of 54.7% in 2025, driven by widespread use of internal ultrasound probes in gynecology, cardiology, and urology applications. These probes require high-level disinfection due to direct or indirect contact with mucous membranes. Increasing diagnostic volumes in women’s health and cardiac imaging is significantly boosting demand. Hospitals prioritize strict disinfection protocols for semicritical devices to minimize infection risks. Expansion of advanced diagnostic centers in China and India further supports dominance. Regulatory guidelines mandating HLD for semicritical probes reinforce strong adoption across healthcare facilities.

The critical devices segment is expected to witness the fastest growth rate of 13.5% from 2026 to 2033, driven by increasing adoption in minimally invasive and interventional ultrasound-guided procedures. Rising use of ultrasound in surgical environments is increasing demand for sterilization-grade disinfection solutions. Hospitals are investing in advanced reprocessing systems to handle higher-risk devices safely. Growing focus on infection-free surgical environments is accelerating adoption. Technological advancements enabling improved sterilization efficiency are also supporting growth in this segment.

- By End User

On the basis of end user, the market is segmented into hospitals & diagnostic imaging centers, ambulatory care centers, maternity centers, academic & research institutes, and others. The hospitals & diagnostic imaging centers segment dominated the market with the largest revenue share of 58.9% in 2025, driven by high patient inflow and extensive use of ultrasound imaging across multiple departments. These facilities require large-scale disinfection systems to manage high probe usage efficiently. Increasing prevalence of HAIs has led hospitals to adopt automated high-level disinfection solutions. Strong investments in healthcare infrastructure across China and India further strengthen demand. Integration of infection control protocols into hospital workflows ensures consistent usage. Large diagnostic imaging centers also contribute significantly due to high procedural throughput.

The ambulatory care centers segment is expected to witness the fastest growth rate of 14.2% from 2026 to 2033, driven by rising shift toward outpatient diagnostic services. Increasing demand for cost-effective and quick diagnostic procedures is boosting ultrasound usage in ambulatory settings. These centers are increasingly adopting compact and automated disinfection systems. Growing healthcare decentralization across Asia-Pacific is further supporting segment expansion. Rising awareness of infection prevention in outpatient care is also accelerating adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, third party distributors, and others. The direct tender segment dominated the market with the largest revenue share of 49.6% in 2025, driven by large-scale procurement of disinfection systems by public hospitals and government healthcare institutions. Centralized purchasing policies in countries such as China and India favor direct procurement from manufacturers. This ensures cost efficiency and standardized equipment deployment across hospital networks. Increasing government investments in healthcare infrastructure further strengthen this channel. Direct relationships between manufacturers and large hospital chains also support dominance. High-value equipment purchases are typically executed through tender-based systems.

The third party distributors segment is expected to witness the fastest growth rate of 13.3% from 2026 to 2033, driven by expanding reach into smaller hospitals and diagnostic clinics. Distributors play a key role in supplying equipment to semi-urban and rural healthcare facilities. Growing penetration of ultrasound services in emerging regions is increasing reliance on distributor networks. They also provide installation, training, and maintenance support, enhancing adoption. Increasing demand for localized service support is further accelerating growth of this channel.

Asia-Pacific Ultrasound Probe Disinfection Market Regional Analysis

- China dominated the ultrasound probe disinfection market with the largest revenue share of 38.6% in 2025, supported by rapid expansion of hospital infrastructure, large patient population base, increasing diagnostic imaging volumes, and strong adoption of advanced infection control technologies across healthcare facilities

- Healthcare providers in the country are increasingly prioritizing infection control measures, with strong adoption of high-level disinfection systems to reduce hospital-acquired infections and ensure compliance with stringent clinical hygiene standards

- This widespread adoption is further supported by a large patient population base, rising ultrasound diagnostic volumes, and continuous modernization of hospital facilities, establishing China as the leading market for ultrasound probe disinfection solutions in the region

The China Ultrasound Probe Disinfection Market Insight

The China ultrasound probe disinfection market captured the largest revenue share of 38.6% in 2025 within Asia-Pacific, fueled by rapid expansion of hospital infrastructure and increasing adoption of advanced diagnostic imaging systems. Healthcare providers are increasingly prioritizing infection prevention through high-level disinfection of ultrasound probes to reduce hospital-acquired infections and ensure patient safety compliance. The growing preference for automated disinfection systems, combined with rising ultrasound diagnostic volumes and modernization of public hospitals, further propels the market. Moreover, the increasing integration of digital monitoring and standardized infection control protocols across healthcare facilities is significantly contributing to market expansion.

Japan Ultrasound Probe Disinfection Market Insight

The Japan ultrasound probe disinfection market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strict infection control standards and high awareness of healthcare-associated infections in medical facilities. The country’s advanced healthcare infrastructure and aging population are fostering higher utilization of ultrasound diagnostics, increasing the need for reliable probe disinfection systems. Japan’s strong focus on precision healthcare and patient safety is encouraging adoption of automated high-level disinfection solutions. In addition, integration of disinfection systems with hospital workflow automation is supporting consistent growth across hospitals and diagnostic imaging centers.

South Korea Ultrasound Probe Disinfection Market Insight

The South Korea ultrasound probe disinfection market is anticipated to grow at a strong CAGR during the forecast period, driven by advanced digital healthcare infrastructure and increasing emphasis on hospital infection control standards. The country’s highly developed diagnostic imaging ecosystem is supporting widespread use of ultrasound procedures, thereby increasing demand for efficient probe disinfection solutions. Hospitals in South Korea are rapidly adopting automated high-level disinfection systems to enhance workflow efficiency and ensure compliance with strict hygiene regulations. Furthermore, integration of smart hospital systems and growing investments in medical technology innovation are further accelerating market growth.

India Ultrasound Probe Disinfection Market Insight

The India ultrasound probe disinfection market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rapid expansion of diagnostic imaging services and increasing awareness of infection prevention in healthcare settings. Rising healthcare investments, expansion of private diagnostic chains, and growing patient inflow are strengthening demand for ultrasound procedures and associated disinfection systems. Concerns regarding hospital-acquired infections are encouraging hospitals to adopt standardized high-level disinfection practices. Furthermore, government initiatives supporting healthcare infrastructure development and the growth of tier-2 and tier-3 city hospitals are expected to continue stimulating market growth.

Asia-Pacific Ultrasound Probe Disinfection Market Share

The Asia-Pacific Ultrasound Probe Disinfection industry is primarily led by well-established companies, including:

- Nanosonics Limited (Australia)

- STERIS plc (Ireland)

- Ecolab Inc. (U.S.)

- Tristel plc (U.K.)

- Germitec S.A. (France)

- CIVCO Medical Solutions (U.S.)

- CS Medical LLC (U.S.)

- Advanced Sterilization Products (U.S.)

- Schülke & Mayr GmbH (Germany)

- Parker Laboratories, Inc. (U.S.)

- Metrex Research, LLC (U.S.)

- Virox Technologies Inc. (Canada)

- Soluscope SAS (France)

- Borer Chemie AG (Switzerland)

- LANXESS AG (Germany)

- Drägerwerk AG & Co. KGaA (Germany)

- Olympus Corporation (Japan)

- Siemens Healthineers AG (Germany)

- GE HealthCare (U.S.)

- Philips Healthcare (Netherlands)

What are the Recent Developments in Asia-Pacific Ultrasound Probe Disinfection Market?

- In June 2025, Germitec introduced Chronos Max, a next-generation UV-C high-level disinfection (HLD) system designed for ultrasound and TEE probes, with growing adoption across Asia-Pacific healthcare facilities. The system enables rapid, chemical-free disinfection cycles, significantly improving turnaround time in high-volume imaging departments

- In May 2025, Nanosonics continued expansion of its Trophon2 high-level disinfection system, widely used for ultrasound probe reprocessing in hospitals across Asia-Pacific. The system is increasingly adopted in Japan and Australia for automated probe disinfection workflows

- In November 2024, Nanosonics announced the expansion of its trophon ultrasound probe disinfection ecosystem, introducing enhanced compatibility for wireless ultrasound probes across hospital settings. The solution is designed to integrate directly into existing high-level disinfection (HLD) workflows, improving efficiency in busy diagnostic imaging departments

- In February 2024, GE HealthCare introduced workflow improvements across its ultrasound ecosystem, integrating infection-control compatible probe handling practices in hospital systems across Asia-Pacific. The development supports safer reuse of ultrasound probes by aligning imaging systems with standardized disinfection protocols

- In October 2023, Germitec expanded deployment of its UV-C based ultrasound probe disinfection systems across Asia-Pacific hospitals. The solution provides chemical-free high-level disinfection using ultraviolet technology, reducing reliance on liquid disinfectants

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.