Asia Pacific Uterine Cancer Diagnostics Market

Market Size in USD Billion

USD

2.63 Billion

USD

5.98 Billion

2024

2032

USD

2.63 Billion

USD

5.98 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.63 Billion | |

| USD 5.98 Billion | |

| % | |

|

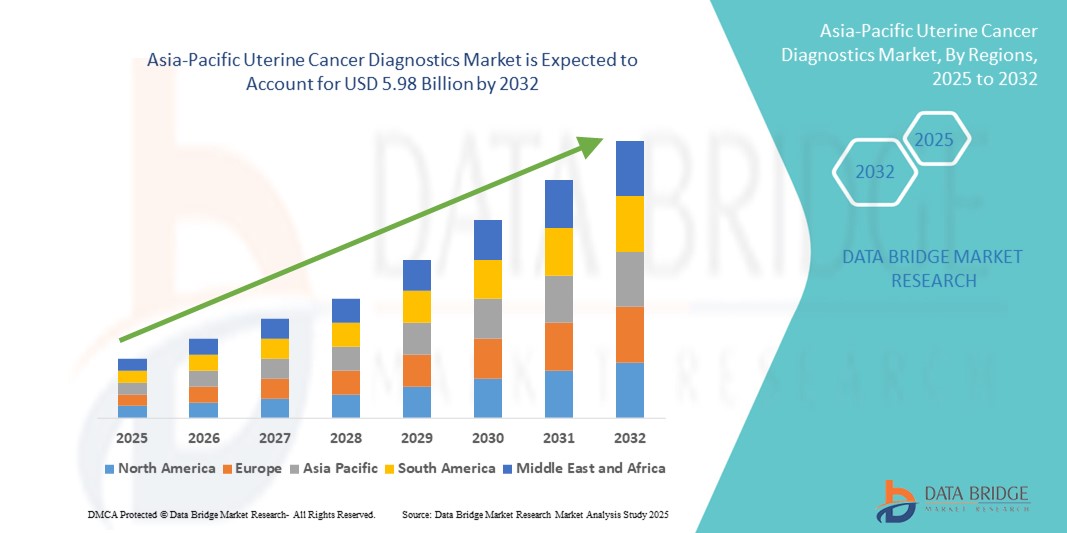

Asia-Pacific Uterine Cancer Diagnostics Market Size

- The Asia-Pacific uterine cancer diagnostics market size was valued at USD 2.63 Billion in 2024 and is expected to reach USD 5.98 Billion by 2032, at a CAGR of 10.8% during the forecast period

- The market growth is largely fueled by the rising prevalence of uterine cancer across Asia-Pacific, increasing awareness regarding early detection, and advancements in diagnostic technologies such as molecular diagnostics, imaging modalities, and biomarker-based testing. Countries like China, India, and Japan are witnessing a surge in demand for uterine cancer diagnostics, driven by growing healthcare expenditure, urbanization, and government-supported cancer screening programs aimed at improving patient outcomes

- Furthermore, escalating investments in cancer care infrastructure, expansion of diagnostic centers in rural and semi-urban areas, and increasing collaborations between global diagnostic companies and local healthcare providers are driving accessibility and innovation. Favorable reimbursement policies, combined with the growing presence of international players and rising adoption of AI-enabled diagnostic platforms, are significantly boosting the growth of the Asia-Pacific uterine cancer diagnostics market

Asia-Pacific Uterine Cancer Diagnostics Market Analysis

- The Asia-Pacific Uterine Cancer Diagnostics market is witnessing significant growth, fueled by the rising incidence of uterine cancer, increasing awareness about women’s health, and the expanding availability of advanced diagnostic technologies across countries such as China, India, Japan, South Korea, Australia, Thailand, Indonesia, and Vietnam. The adoption of early detection methods, molecular diagnostics, and imaging solutions is playing a key role in improving patient outcomes and driving market demand

- Increased investments in research and development, a surge in clinical studies targeting gynecological cancers, stricter regulatory frameworks, and a growing emphasis on precision oncology are further supporting the expansion of uterine cancer diagnostics in the region. Healthcare providers are increasingly integrating advanced diagnostic platforms to ensure timely and accurate disease detection

- China dominated the Asia-Pacific uterine cancer diagnostics market, accounting for the largest revenue share of 42.0% in 2024. This dominance is attributed to the country’s advanced healthcare infrastructure, large patient population, growing adoption of cutting-edge molecular and imaging diagnostics, and supportive government initiatives promoting cancer screening programs and early detection

- India is projected to register the fastest CAGR of 9.2% in the Asia-Pacific uterine cancer diagnostics market during 2025–2032, driven by increasing awareness of uterine cancer, expanding healthcare access in semi-urban and urban areas, rising investments in oncology-focused infrastructure, and the growing adoption of advanced diagnostic tools such as high-resolution imaging and biomarker-based testing in hospitals and diagnostic centers

- Endometrial cancer diagnostics dominated the Asia-Pacific uterine cancer diagnostics market with a revenue share of 71.3% in 2024, owing to its higher prevalence among women in the Asia-Pacific region and the growing demand for early detection and personalized treatment strategies

Report Scope and Asia-Pacific Uterine Cancer Diagnostics Market Segmentation

|

Attributes |

Asia-Pacific Uterine Cancer Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia-Pacific Uterine Cancer Diagnostics Market Trends

Growing Demand for Advanced Diagnostic Solutions and Enhanced Healthcare Outcomes

- A significant and accelerating trend in the Asia-Pacific uterine cancer diagnostics market is the increasing focus on high-precision diagnostic testing, early disease detection, and integration of advanced technologies to improve patient outcomes. This includes efforts to enhance diagnostic accuracy, reduce turnaround times, and adopt innovations aligned with evolving international healthcare standards

- Leading diagnostic service providers and healthcare institutions across the region are collaborating with hospitals, oncology centers, and research organizations to deliver next-generation diagnostic solutions such as molecular testing, high-resolution imaging, biomarker analysis, and minimally invasive screening technologies. These initiatives cater to the growing demand for reliable, early, and actionable diagnostic results

- Rising adoption of advanced uterine cancer diagnostics across hospitals, specialized clinics, and research institutes is further driving market growth. These diagnostic services are increasingly recognized for their ability to ensure early detection, guide personalized treatment plans, and improve overall patient care

- Academic institutions, oncology research centers, and government-led healthcare programs in countries such as China, India, Japan, and Australia are continuously investing in new diagnostic methodologies, validation protocols, and automation technologies—leading to enhanced service quality, faster testing, and scientifically validated results tailored to regional healthcare needs

- As the Asia-Pacific region emphasizes early detection, innovation in diagnostics, and improved healthcare infrastructure, the Uterine Cancer Diagnostics market is poised for sustained growth—driven by rising disease prevalence, government health initiatives, technological advancements, and the increasing integration of clinical research with diagnostic services

Asia-Pacific Uterine Cancer Diagnostics Market Dynamics

Driver

Growing Demand Driven by Advancements in Healthcare and Precision Oncology

- The Asia-Pacific uterine cancer diagnostics market is witnessing accelerated growth, fueled by the expansion of healthcare infrastructure, biotechnology research, and advanced diagnostic capabilities across key countries such as China, India, Japan, South Korea, and Australia. Rising investments in early cancer detection, precision medicine, and personalized treatment approaches are driving the adoption of innovative diagnostic solutions

- For instance, In March 2024, Siemens Healthineers expanded its molecular diagnostic capabilities in the Asia-Pacific region, enhancing services in high-precision biomarker analysis, genetic testing, and histopathology to support healthcare providers in delivering faster and more accurate uterine cancer diagnostics across key markets such as China, India, and Japan

- The increasing prevalence of uterine cancer, coupled with growing awareness of early detection and treatment benefits, is prompting hospitals, clinics, and research centers to adopt advanced diagnostic technologies, such as molecular assays, imaging solutions, and automated sample processing

- Government initiatives promoting oncology research, investment in cancer care infrastructure, and incentives for early disease screening programs are further supporting market growth. Countries such as Singapore and South Korea are establishing themselves as regional hubs for advanced diagnostics, attracting collaborations from global healthcare and biotechnology players

- The integration of digital platforms, laboratory information management systems (LIMS), and automated diagnostic equipment is enabling providers to efficiently process large volumes of patient samples, improve accuracy, reduce turnaround times, and ensure compliance with stringent clinical and regulatory standards

Restraint/Challenge

Limited Access in Semi-Urban and Rural Regions

-

- Despite rapid advancements in urban healthcare infrastructure, the Asia-Pacific uterine cancer diagnostics market faces challenges in reaching smaller hospitals, clinics, and semi-urban or rural regions, particularly in Southeast Asia and parts of South Asia. High costs of advanced diagnostics, limited awareness of early detection benefits, and budget constraints often hinder adoption.

- Infrastructure limitations, including insufficient healthcare networks, lack of specialized laboratories, and underdeveloped sample transport systems, further restrict timely access to advanced diagnostic services.

- Many smaller healthcare facilities still rely on basic cytology or conventional diagnostic methods, which may not meet international standards, creating a gap between patient needs and available diagnostic capabilities.

- Uneven distribution of accredited diagnostic centers across the region forces patients and healthcare providers in remote areas to depend on long-distance sample transport, increasing costs and delaying results.

- To overcome these barriers, leading market players are introducing mobile diagnostic units, decentralized testing models, and strategic collaborations with regional hospitals and clinics to expand accessibility. Cost-effective testing packages and outreach programs are being implemented to improve adoption in price-sensitive and underserved regions while maintaining high standards of accuracy and compliance

Asia-Pacific Uterine Cancer Diagnostics Market Scope

The market is segmented on the basis of diagnostic type, cancer type, age group, end user, and distribution channel.

- By Diagnostic Type

On the basis of diagnostic type, the Asia-Pacific uterine cancer diagnostics market is segmented into instrument-based and procedure-based diagnostics. The instrument-based diagnostics segment dominated the market with a revenue share of 62.4% in 2024, driven by the increasing adoption of high-precision tools such as molecular analyzers, imaging devices, and automated pathology systems that enable accurate and rapid detection of uterine cancers. These instruments are critical for early diagnosis, treatment monitoring, and research applications.

The procedure-based diagnostics segment in the Asia-Pacific market is projected to grow at the fastest CAGR of 9.8% from 2025 to 2032. This growth is largely driven by the rising preference for minimally invasive biopsy techniques, hysteroscopy, and other procedural methods that provide improved patient comfort, reduced recovery time, and more accurate clinical outcomes. Increasing awareness among clinicians and patients regarding the benefits of procedure-based diagnostics, coupled with advancements in imaging technologies and endoscopic tools, is further fueling the adoption of these techniques across hospitals and specialized diagnostic centers in the region

- By Type

On the basis of type, the Asia-Pacific uterine cancer diagnostics market is segmented into endometrial cancer and uterine sarcoma. Endometrial cancer diagnostics led the market with a revenue share of 71.3% in 2024, primarily due to its higher prevalence among women in the region and the increasing focus on early detection and personalized treatment strategies. The dominance of this segment is further supported by rising awareness about risk factors, government-backed screening programs, and the adoption of advanced molecular and genetic testing techniques that enable precise diagnosis and tailored therapeutic interventions.

Uterine sarcoma is anticipated to register the fastest CAGR of 10.2% during the forecast period, driven by rapid advancements in molecular profiling, imaging modalities, and targeted diagnostic tools. The increasing recognition of rare uterine cancer types and the need for highly specialized diagnostic approaches to accurately identify and differentiate sarcomas from other uterine malignancies are key factors contributing to the robust growth of this segment. Enhanced clinical research and the integration of innovative diagnostic technologies are expected to further accelerate market adoption in this category.

- By Age Group

On the basis of age group, the Asia-Pacific uterine cancer diagnostics market is segmented into <30, 31–40, 41–50, 51–60, and >60 years. The 51–60 years segment accounted for the largest share of 33.5% in 2024, reflecting the significantly higher incidence of uterine cancers among middle-aged women. This trend is further reinforced by the growing implementation of age-targeted screening programs, routine gynecological check-ups, and heightened awareness of risk factors specific to this age group, enabling earlier detection and timely intervention.

The 41–50 years segment is projected to grow at the fastest CAGR of 9.5% from 2025 to 2032, supported by increasing awareness among women approaching menopause about the importance of preventive screenings. The adoption of early diagnostic interventions, combined with educational initiatives and accessibility to advanced testing methods, is fueling the growth of this segment, helping clinicians identify potential cases at an earlier stage and improving overall patient outcomes.

- By End User

On the basis of end user, the Asia-Pacific uterine cancer diagnostics market is segmented into hospitals, diagnostic centers, cancer research centers, ambulatory surgical centers, specialized clinics, and others. Hospitals dominated the market with a share of 44.1% in 2024, driven by their comprehensive infrastructure, ability to handle high patient volumes, and integrated care pathways that combine advanced diagnostics, treatment, and follow-up care. The presence of specialized oncology departments and access to state-of-the-art diagnostic equipment further consolidates their leading position.

Diagnostic centers accounted for 26.5% of the market in 2024 and are expected to witness the fastest growth with a CAGR of 9.3%, propelled by the expansion of independent laboratories and increased patient preference for specialized diagnostic services. Additionally, the growing trend of outsourcing complex tests from smaller healthcare facilities to dedicated diagnostic centers is enhancing service accessibility and supporting the rapid adoption of advanced uterine cancer diagnostic solutions across the region.

- By Distribution Channel

On the basis of distribution channel, the Asia-Pacific uterine cancer diagnostics market is segmented into direct tender, third-party distributors, and others. The direct tender segment accounted for the largest revenue share of 55.8% in 2024, driven by large-scale procurement by hospitals, government-led initiatives for national screening programs, and long-term institutional contracts with diagnostic equipment suppliers. This approach ensures a consistent supply of advanced uterine cancer diagnostic tools to key healthcare facilities, facilitating widespread adoption and supporting large patient populations across the region.

The third-party distributors segment is projected to register the fastest CAGR of 8.9%, propelled by growing collaborations between manufacturers and regional distributors. These partnerships are enhancing the reach of diagnostic solutions to semi-urban and rural areas, improving accessibility for smaller clinics and healthcare centers. By bridging the gap between suppliers and remote healthcare facilities, third-party distributors play a crucial role in ensuring timely availability of advanced diagnostic technologies, thereby supporting early detection and improved patient care outcomes.

Asia-Pacific Uterine Cancer Diagnostics Market Regional Analysis

- Asia-Pacific held a revenue share of 23.5% in the global uterine cancer diagnostics market in 2024. This leadership position is driven by the region’s vast population base, rapid expansion of healthcare infrastructure, growing oncology-focused facilities, and increasing adoption of advanced molecular and imaging diagnostics. Government-led cancer screening initiatives and rising awareness of uterine cancer are further supporting market growth

- A rising focus on early detection, personalized diagnostics, and integration of biomarker-based and high-resolution imaging technologies is also contributing to market growth. Expansion of hospitals, specialty clinics, and diagnostic centers, along with public-private collaborations, is enabling the region to cater to both domestic and international patients. Strategic partnerships between regional providers and global technology leaders are accelerating adoption of cutting-edge diagnostics

- The demand for uterine cancer diagnostics is further supported by substantial investments from public and private sectors to enhance healthcare infrastructure, oncology-focused facilities, and advanced diagnostic technologies. Key growth contributors include the increasing prevalence of uterine cancer, adoption of personalized medicine, and rising access to minimally invasive and biomarker-driven testing. In addition, urbanization, rising healthcare expenditure, and government initiatives to promote early detection and screening have collectively fueled market growth across the region

China Asia-Pacific Uterine Cancer Diagnostics Market Insight

The China uterine cancer diagnostics market held the largest market share in the Asia-Pacific region at 42.0% in 2024, solidifying its leadership through advanced healthcare infrastructure, supportive government screening programs, and adoption of molecular and imaging diagnostics. Rapid urbanization, increasing patient awareness, and strong domestic industrial capabilities have driven demand for high-quality diagnostic services. China’s position as a hub for advanced oncology diagnostics is reinforced by well-established local laboratories and foreign-invested diagnostic service providers, creating a competitive and innovation-driven market environment.

India Asia-Pacific Uterine Cancer Diagnostics Market Insight

The India uterine cancer diagnostics market is projected to register the fastest CAGR of 9.2% from 2025 to 2032, driven by rising awareness of uterine cancer, expanding healthcare access in semi-urban and urban areas, and growing adoption of advanced diagnostic tools such as high-resolution imaging and biomarker-based testing. Government initiatives, investments in oncology infrastructure, and collaborations between Indian diagnostic providers and global technology leaders are further accelerating market growth. Expansion of diagnostic centers, hospitals, and specialty clinics across tier 2 and tier 3 cities is supporting increased service demand and improving patient access to timely and accurate diagnostics.

Asia-Pacific Uterine Cancer Diagnostics Market Share

The Asia-Pacific Uterine Cancer Diagnostics industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Siemens Healthineers AG (Germany)

- Narang Medical Limited (India)

- ESAOTE S.p.A. (Italy)

- Olympus Corporation (Japan)

- Integra LifeSciences Corporation (U.S.)

- Canon Medical Systems Corporation (Japan)

- KARL STORZ SE & Co. KG (Germany)

- Stryker (U.S.)

- Guzip Biomarkers Corporation (China)

- General Electric Company (U.S.)

- FUJIFILM Corporation (Japan)

- Koninklijke Philips N.V. (Netherlands)

- B. Braun SE (Germany)

- Jalal Surgical (Pakistan)

Latest Developments in Asia-Pacific Uterine Cancer Diagnostics market

- In March 2024, WuXi AppTec, a leading global provider of comprehensive services that support the pharmaceutical, biotechnology, and medical device industries, announced the expansion of its analytical testing facilities in China. This expansion aims to enhance capabilities in bioanalytical services, stability testing, and microbiological analysis to support both domestic and global clients in achieving faster regulatory approvals

- In 2024, a study conducted in Japan aimed to establish quality indicators (QIs) for endometrial cancer and explore the factors contributing to treatment nonadherence. The study highlighted the increasing incidence and mortality rates of endometrial cancer globally, including in Japan, and emphasized the importance of promoting quality cancer care through guideline adherence

- In 2024, a study assessed the diagnostic role of hysteroscopy in endometrial cancer detection compared to pathology as a gold standard. The study demonstrated that hysteroscopy has a sensitivity of 86.4% and a specificity of 99.2% for the confirmation of endometrial carcinoma, highlighting its effectiveness as a diagnostic tool in detecting uterine cancer

- In November 2022, Koninklijke Philips N.V., announced the Asia-Pacific launch of a next-generation compact portable ultrasound solution at the Radiological Society of North America (RSNA) annual meeting to bring the diagnostic quality associated with premium cart-based ultrasound systems to more patients. it is portable and versatile with good image quality or performance. it is compatible with Philips ultrasound systems Affiniti and EPIQ transducer. This has helped the company to expand its product portfolio

- In April 2022, Medtronic and GE Healthcare announced a collaboration focused on the unique needs and demand for care at Ambulatory Surgery Centers (ASCs) and Office Based Labs (OBLs). Because of this collaboration, customers can access extensive product portfolios, financial solutions and exceptional service. GE Healthcare Interventional Imaging solutions are built to help our customers deliver care at a higher level for patients, which is very useful of cancer patients. This has helped the company to expand its business

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.