Asia Pacific Venous Diseases Treatment Market

Market Size in USD Billion

USD

1.30 Billion

USD

2.49 Billion

2024

2032

USD

1.30 Billion

USD

2.49 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.30 Billion | |

| USD 2.49 Billion | |

| % | |

|

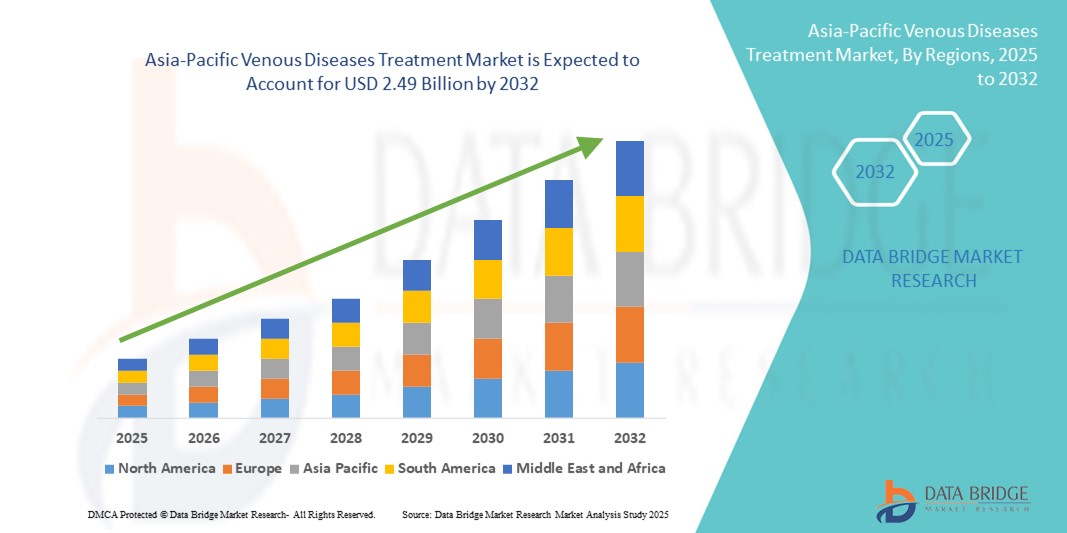

Asia-Pacific Venous Diseases Treatment Market Size

- The Asia-Pacific venous diseases treatment market size was valued at USD 1.30 Billion in 2024 and is expected to reach USD 2.49 Billion by 2032, at a CAGR of 8.40% during the forecast period

- The market growth is primarily driven by the rising prevalence of venous diseases, increasing healthcare access, and advancements in diagnostic and therapeutic technologies across Asia-Pacific, enabling timely and effective treatment for conditions such as varicose veins, chronic venous insufficiency, and deep vein thrombosis. Countries like India, China, and Japan are witnessing a surge in adoption of minimally invasive procedures and endovascular interventions, contributing to the growing demand for advanced venous disease treatments

- In addition, escalating investments in healthcare infrastructure, expansion of specialized vascular centers in semi-urban and rural areas, and increasing public-private partnerships are enhancing treatment availability and patient access. Government-led awareness programs on venous health, along with the growing presence of international medical device providers and local healthcare capabilities, are further accelerating the growth of the Asia-Pacific venous diseases treatment market

Asia-Pacific Venous Diseases Treatment Market Analysis

- The Asia-Pacific venous diseases treatment market is witnessing strong growth, driven by the rapid expansion of healthcare infrastructure, rising prevalence of venous disorders, and increasing adoption of advanced treatment modalities across key countries such as China, India, Japan, South Korea, Australia, Thailand, Indonesia, and Vietnam. The growing awareness about chronic venous insufficiency, varicose veins, deep vein thrombosis (DVT), and related complications is further fueling market demand

- Increasing investments in R&D, a surge in clinical trials for novel therapies, stricter regulatory requirements, and the adoption of minimally invasive procedures such as endovenous laser therapy (EVLT) and radiofrequency ablation (RFA) are supporting market expansion across the region. The trend toward patient-centric care, early diagnosis, and outpatient treatment options is enhancing the overall adoption of venous disease therapies

- China dominated the Asia-Pacific venous diseases treatment market, accounting for the largest revenue share of 30.5% in 2024, driven by its strong healthcare infrastructure, increasing government initiatives to address chronic diseases, high patient volume, and rapid adoption of advanced treatment technologies. The country’s well-established pharmaceutical and medical device manufacturing base also supports the availability of state-of-the-art venous disease therapies

- India is projected to register the fastest CAGR in the Asia-Pacific venous diseases treatment market during the forecast period, fueled by growing healthcare access, increasing adoption of minimally invasive procedures, expansion of specialty vascular centers, and rising awareness of treatment options among patients. The country’s focus on improving rural and semi-urban healthcare facilities and rising investment in advanced medical technologies are further accelerating market growth

- The Deep Vein Thrombosis (DVT) segment dominated the Asia-Pacific venous diseases treatment market with a share of 31.7% in 2024, fueled by its high prevalence, growing awareness of associated complications such as pulmonary embolism, and an increasing focus on early detection, diagnosis, and intervention

Report Scope and Asia-Pacific Venous Diseases Treatment Market Segmentation

|

Attributes |

Asia-Pacific Venous Diseases Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia-Pacific Venous Diseases Treatment Market Trends

Increasing Adoption of Advanced Venous Treatment Solutions and Regulatory Compliance

- A significant and accelerating trend in the Asia-Pacific venous diseases treatment market is the increasing focus on high-precision treatment technologies, evidence-based protocols, and regulatory compliance across healthcare providers. This includes efforts to improve patient outcomes, minimize procedural complications, and align with evolving regional and international healthcare standards

- Leading medical device manufacturers and healthcare providers across the region are investing in next-generation venous treatment solutions such as endovenous laser ablation (EVLA), radiofrequency ablation (RFA), sclerotherapy, and advanced compression therapy systems. These innovations cater to the growing demand for minimally invasive, safe, and clinically validated interventions

- Increasing adoption of advanced venous treatment solutions in hospitals, specialty clinics, and ambulatory surgical centers is further accelerating market growth. These solutions are being recognized for their ability to enhance patient safety, reduce recovery times, and deliver long-term efficacy in chronic venous disease management

- Academic institutions, research centers, and government healthcare bodies in countries such as China, Japan, India, and Australia are conducting studies on novel venous therapies, clinical best practices, and treatment outcome optimization—leading to service enhancements backed by scientific evidence and tailored to region-specific patient needs

- As the Asia-Pacific region continues to emphasize healthcare quality, technological innovation, and patient-centered care, the Venous Diseases Treatment market is poised for sustained expansion—driven by regulatory rigor, technological advancements, and the increasing integration of clinical research with treatment delivery

Asia-Pacific Venous Diseases Treatment Market Dynamics

Driver

Rising Demand Driven by Healthcare Advancements, Pharmaceutical Growth, and Biotechnology Innovations

- The Asia-Pacific venous diseases treatment market is witnessing accelerated growth, driven by the expansion of advanced healthcare infrastructure, pharmaceutical manufacturing, and biotechnology research across key countries including China, India, Japan, South Korea, and Australia. Increasing investments in vascular therapies, minimally invasive procedures, and personalized treatment approaches are boosting the demand for high-quality venous disease treatment solutions that adhere to international safety and efficacy standards

- For instance, in March 2024, WuXi AppTec expanded its vascular treatment and analytical testing facilities in China, enhancing capabilities in bioanalytical services, device testing, and clinical support to enable faster regulatory approvals and support both domestic and global clients

- The rising prevalence of chronic venous disorders, coupled with a focus on improving patient outcomes and treatment safety, is encouraging hospitals and specialized clinics to adopt advanced venous treatment technologies, including endovenous laser therapy, radiofrequency ablation, and minimally invasive sclerotherapy procedures

- Government initiatives aimed at strengthening healthcare infrastructure, promoting local R&D in vascular medicine, and supporting clinical trial activities are further driving market expansion. Countries such as Singapore and South Korea are emerging as regional hubs for advanced venous treatment solutions, attracting international collaborations and investments

- The integration of digital health platforms, telemedicine, and advanced patient monitoring systems is enabling service providers to optimize treatment planning, improve procedural accuracy, and enhance follow-up care for patients with venous disorders

Restraint/Challenge

Challenges in Market Penetration Among Small-Scale Healthcare Facilities and Rural Regions

- Despite rapid urban healthcare development, the Asia-Pacific Venous Diseases Treatment market faces challenges in reaching small-scale clinics and rural healthcare facilities, particularly in Southeast Asia and parts of South Asia. High treatment costs, limited awareness of advanced venous therapies, and budgetary constraints often hinder adoption in these areas

- Infrastructure limitations, such as underdeveloped medical transport networks, lack of specialized equipment, and limited availability of trained vascular specialists, further restrict timely access to advanced treatments

- Many rural healthcare centers continue to rely on traditional or conservative venous care methods, which may not meet modern clinical standards, creating a disparity in treatment outcomes between urban and rural regions

- In addition, the uneven distribution of accredited vascular treatment centers forces patients in remote areas to travel long distances, increasing treatment delays and associated costs

- To address these challenges, leading market players are exploring mobile healthcare units, telemedicine-enabled consultations, and partnerships with local hospitals and clinics to improve accessibility. They are also introducing cost-effective treatment packages and training programs to enhance adoption in resource-limited settings while maintaining compliance with international medical standards

Asia-Pacific Venous Diseases Treatment Market Scope

The market is segmented into on the basis of product type, disease type, treatment type, end user, and distribution channel.

- By Product Type

On the basis of product type, the Asia-Pacific Venous Diseases Treatment market is segmented into sclerotherapy injection, ablation devices, venous closure products, venous stents, medication, and others. The ablation devices segment dominated the market with the largest revenue share of 26.4% in 2024, owing to its minimally invasive nature, high clinical efficacy, rapid recovery times, and widespread adoption across hospitals and outpatient centers. These devices are increasingly preferred by healthcare providers due to their ability to effectively treat a variety of venous disorders while minimizing patient discomfort and procedural risks.

The venous stents segment is projected to grow at the fastest CAGR of 10.5% from 2025 to 2032, driven by rising procedural volumes across hospitals and specialty clinics, increasing prevalence of complex venous obstructions, and ongoing technological advancements in stent design. Innovations that enhance stent durability, flexibility, and clinical performance are improving patient outcomes, encouraging wider adoption among vascular specialists. Growing awareness among clinicians and patients about minimally invasive stent procedures and long-term benefits is further fueling market expansion. In addition, training programs and procedural guidelines are helping physicians implement advanced stent solutions more effectively, supporting sustained segment growth.

- By Disease Type

On the basis of disease type, the market is segmented into deep vein thrombosis (DVT), chronic venous insufficiency (CVI), pulmonary embolism, superficial thrombophlebitis, varicose veins, and others. The Deep Vein Thrombosis (DVT) segment held the largest market share of 31.7% in 2024, driven by its high prevalence across the Asia-Pacific region and growing awareness of serious complications, including pulmonary embolism and post-thrombotic syndrome. Increased emphasis on early diagnosis, preventive interventions, and evidence-based treatment protocols is boosting the adoption of DVT-specific therapies. Expansion of diagnostic screening programs, clinician training initiatives, and public health awareness campaigns further support the segment’s growth.

Meanwhile, the Chronic Venous Insufficiency (CVI) segment is projected to register the fastest CAGR of 9.8% from 2025 to 2032, fueled by rising incidence rates, greater adoption of long-term management strategies, and a preference among patients for minimally invasive therapies that reduce hospital stays, recovery times, and treatment costs. Advancements in imaging technologies and interventional procedures are also encouraging clinicians to adopt CVI-targeted treatments more broadly.

- By Treatment Type

On the basis of treatment type, the market is segmented into sclerotherapy, radiofrequency ablation therapy, laser treatment, ambulatory phlebectomy, vein ligation and stripping, angioplasty or stenting, surgeries, compression therapy, venoactive medication, vena cava filter, and other therapies. The radiofrequency ablation therapy segment dominated with a revenue share of 29.3% in 2024, driven by its minimally invasive approach, high patient acceptance, and significant reduction in procedural risks and recovery times. Clinicians increasingly favor this therapy due to its precision, reproducibility, and ability to effectively target various venous disorders while minimizing post-procedure complications and hospital stays. Additionally, the use of advanced imaging guidance and monitoring during radiofrequency ablation enhances treatment safety and outcomes.

The laser treatment segment is anticipated to grow at the fastest CAGR of 10.1% from 2025 to 2032, supported by rapid technological innovations, increased adoption in both therapeutic and cosmetic procedures, and a rising trend toward outpatient-based interventions. Laser treatments provide patients with shorter treatment durations, improved comfort, and excellent clinical results, while healthcare providers benefit from efficient procedures and streamlined care delivery. The integration of real-time monitoring and image-guided systems further enhances the precision and safety of laser-based venous therapies, encouraging broader adoption across hospitals and outpatient clinics.

- By End User

On the basis of end user, the Asia-Pacific Venous Diseases Treatment market is segmented into hospitals, clinics, ambulatory surgical centers, and others. The hospitals segment dominated the market in 2024 with a revenue share of 45.6%, owing to their highly advanced infrastructure, extensive patient throughput, and the ability to perform complex and high-risk venous procedures. Hospitals are equipped with specialized vascular units, integrated care pathways, and multidisciplinary teams of vascular specialists, ensuring comprehensive patient management. They also provide access to advanced diagnostic imaging systems, image-guided treatment technologies, and state-of-the-art post-operative care facilities, making them the preferred choice for managing severe and complicated venous conditions.

The ambulatory surgical centers segment is projected to register the fastest CAGR of 9.7% from 2025 to 2032, fueled by the growing preference for outpatient care, minimally invasive procedures, and accelerated recovery protocols. Increasing patient inclination toward cost-effective, convenient, and time-efficient treatment outside traditional hospital settings, coupled with the expansion of specialized outpatient vascular clinics and telehealth-enabled follow-up care, is driving the growth of this segment, particularly for procedures that do not require prolonged hospital stays.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, retail sales, and others. The direct tender segment held the largest share of 47.2% in 2024, supported by bulk procurement by hospitals, government health programs, and large clinical facilities that seek consistent product availability, competitive pricing, and volume-based discounts. This channel is preferred due to its structured supply contracts, reliable logistics, and ability to maintain uninterrupted availability of critical venous disease treatment products.

The retail sales segment is projected to grow at the fastest CAGR of 8.9% from 2025 to 2032, driven by increasing demand from smaller clinics, private practices, ambulatory centers, and remote healthcare facilities that require flexible and readily accessible supply options. The rapid expansion of e-commerce platforms, specialized medical distributors, and telehealth-enabled procurement systems is further enhancing product accessibility, especially in regions with limited direct access to major healthcare networks, thereby improving patient access to advanced venous disease treatments across the Asia-Pacific region.

Asia-Pacific Venous Diseases Treatment Market Regional Analysis

- Asia-Pacific held a revenue share of 21% in the global venous diseases treatment market in 2024. The region’s strong position is driven by its large population base, rapid expansion of healthcare infrastructure, and growth of pharmaceutical and biotechnology sectors. Increasing outsourcing of testing, diagnostics, and treatment-related analytical services to specialized laboratories further supports market growth

- A rising emphasis on product quality, regulatory compliance, and safety testing across multiple industries—including medical research, environmental monitoring, and healthcare services—is boosting demand. The presence of advanced analytical facilities, a skilled workforce, and integrated hospital-based treatment centers enables the region to serve both domestic and international clients efficiently. Moreover, the expansion of contract research organizations (CROs), increased clinical trial activity, and adoption of digital laboratory management systems are reinforcing Asia-Pacific’s leading position in the Venous Diseases Treatment market

- Further growth is supported by public and private investments to strengthen laboratory infrastructure, expand healthcare facilities, and integrate advanced treatment technologies. Key contributors include the rising prevalence of venous diseases, growth in minimally invasive procedures, and adoption of personalized care models. Rapid urbanization, a growing middle-class population with increasing health awareness, and government-led R&D initiatives are collectively fueling market expansion. Strategic partnerships between regional healthcare providers and global players, alongside cross-border collaborations, are enhancing the region’s influence in the global market

China Asia-Pacific Venous Diseases Treatment Market Insight

The China venous diseases treatment market dominated the Asia-Pacific Venous Diseases Treatment market, accounting for the largest revenue share of 30.5% in 2024. The country’s leadership is supported by advanced healthcare infrastructure, increasing government initiatives to manage chronic venous diseases, a high patient volume, and rapid adoption of cutting-edge treatment technologies. Its well-established pharmaceutical and medical device manufacturing base ensures the availability of state-of-the-art therapies, while urbanization and regulatory support drive demand for quality treatment solutions.

India Asia-Pacific Venous Diseases Treatment Market Insight

The India venous diseases treatment market is projected to register the fastest CAGR in the Asia-Pacific Venous Diseases Treatment market from 2025 to 2032. This growth is fueled by expanding healthcare access, increasing adoption of minimally invasive procedures, development of specialty vascular centers, and rising patient awareness regarding treatment options. Government focus on improving rural and semi-urban healthcare facilities, coupled with investments in advanced medical technologies and partnerships with global players, is accelerating the market’s expansion in India.

Asia-Pacific Venous Diseases Treatment Market Share

The Asia-Pacific Venous Diseases Treatment industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Imricor (U.S.)

- Baylis Medical Company, Inc. (Canada)

- Theraclion (France)

- Sonablate (U.S.)

- plusmedica.de (Germany)

- Boston Scientific Corporation (U.S.)

- Olympus Corporation (Japan)

- Smith + Nephew (U.K.)

- Cook (U.S.)

- Scitech (Germany)

- Carl Zeiss Meditec AG (Germany)

- Teleflex Incorporated (U.S.)

- Alma Lasers (Israel)

- BD (U.S.)

- B.Braun SE (Germany)

- Medtronic (Ireland)

- Stryker (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Varian Medical Systems (U.S.)

- Candela Corporation (U.S.)

- Terumo Corporation (Japan)

- Angiodynamics (U.S.)

- optimed Medizinische Instrumente GmbH (Germany)

- Merit Medical Systems (U.S.)

- Bolitec Laser (Germany)

Latest Developments in Asia-Pacific Venous Diseases Treatment market

- In March 2024, BD initiated the AGILITY study, enrolling its first patient to evaluate the safety and effectiveness of the BD Vascular Covered Stent for treating Peripheral Arterial Disease (PAD). This global, multi-center clinical trial involves 315 patients across 40 sites in the U.S., Europe, Australia, and New Zealand. The study aims to address significant unmet needs in PAD treatment and could provide interventionalists with a new solution to improve patient outcomes over the next three years of follow-up

- In December 2023, Terumo India launched Ultimaster Nagomi, an advanced drug-eluting coronary stent system designed for complex percutaneous coronary interventions (PCI). The stent features an optimized delivery system, expanded size range, and increased overexpansion capability, allowing it to adapt to challenging anatomies. Ultimaster Nagomi aims to improve patient outcomes by enabling customized stent selection for small to large coronary arteries

- In March 2023, Haemonetics Corporation invested USD 32.2 million in Ireland-based Vivasure Medical, the company involved in developing a portfolio of fully absorbable, patch-based, large-bore percutaneous vessel closure devices. This investment underscores Haemonetics' commitment to advancing vascular closure technologies and expanding its product offerings in the Asia-Pacific region

- In February 2023, Servier, a global pharmaceutical group, highlighted its broad portfolio of high-quality treatments in cardiometabolism and venous diseases in its Sustainability Report. The report emphasizes Servier's commitment to addressing venous diseases through innovative therapies and sustainable practices, contributing to the advancement of venous disease treatments in the Asia-Pacific region

- In June 2022, the Asia-Pacific Varicose Vein Treatment Market was valued at USD 75.18 million in 2024, with expectations to grow at a CAGR of 6.9% from 2025 to 2033. This growth is attributed to the increasing prevalence of venous disorders, advancements in minimally invasive treatment technologies, and rising awareness about varicose vein treatments in the region

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.