Asia Pacific Wind Turbine Pitch System Market

Market Size in USD Million

USD

384.48 Million

USD

563.73 Million

2024

2032

USD

384.48 Million

USD

563.73 Million

2024

2032

| 2025 - 2032 | |

| USD 384.48 Million | |

| USD 563.73 Million | |

| % | |

|

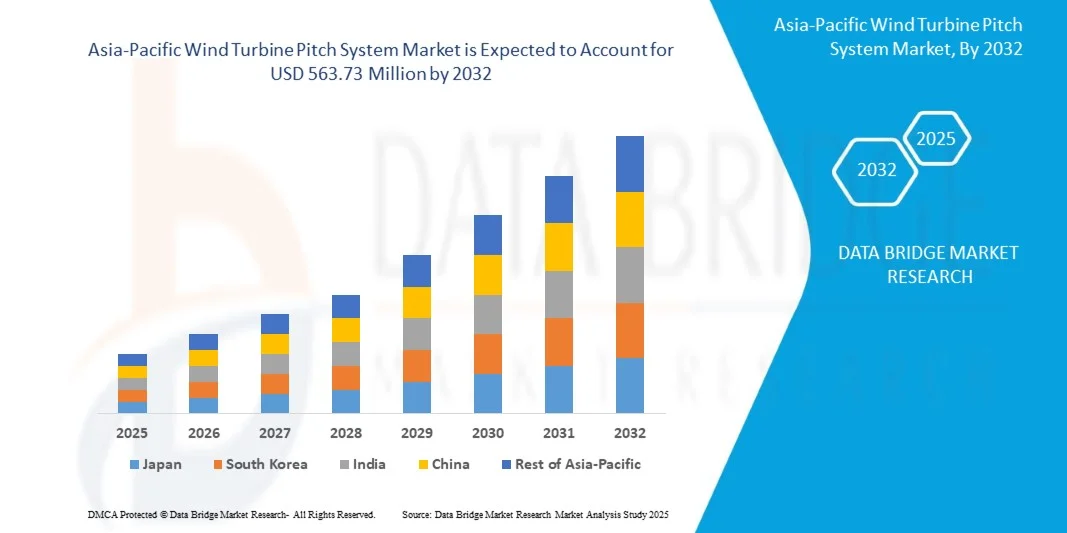

Asia-Pacific Wind Turbine Pitch System Market Size

- The Asia-Pacific Wind Turbine Pitch System Market size was valued at USD 384.48 million in 2024 and is expected to reach USD 563.73 million by 2032, at a CAGR of 4.9% during the forecast period

- The market growth is largely fueled by the increasing deployment of onshore and offshore wind turbines worldwide, driven by the push for renewable energy and carbon emission reduction. Technological advancements in pitch system components, such as motors, servo drives, and control systems, are enhancing turbine efficiency, reliability, and energy output

- Furthermore, rising investments in large-scale wind projects and the growing emphasis on predictive maintenance and smart monitoring systems are establishing advanced pitch systems as critical components for optimal turbine performance. These converging factors are accelerating the adoption of high-precision pitch solutions, thereby significantly boosting the industry’s growth

Asia-Pacific Wind Turbine Pitch System Market Analysis

- Wind turbine pitch systems are mechanisms that control the angle of turbine blades to optimize energy capture, reduce mechanical stress, and ensure operational safety. These systems include pitch motors, valves, servo drives, and monitoring solutions that integrate with turbine control platforms to enhance performance and longevity

- The escalating demand for wind turbine pitch systems is primarily fueled by the expansion of renewable energy infrastructure, increasing turbine sizes, and the need for high efficiency and reliability in both onshore and offshore installations. Continuous innovation in system design and automation further supports market growth

- China dominated the Asia-Pacific Wind Turbine Pitch System Market in 2024, due to its massive wind energy installations, government-backed renewable energy targets, and extensive investments in offshore and onshore projects

- India is expected to be the fastest growing country in the Asia-Pacific Wind Turbine Pitch System Market during the forecast period due to rapid wind farm installations, supportive government incentives, and aggressive renewable energy capacity targets

- Off-shore turbine segment dominated the market with a market share of 87.9% in 2024, due to deployment of large-scale turbines in wind farms that maximize energy generation. Offshore turbines require highly reliable pitch systems to withstand harsh marine environments and high wind loads. Advanced blade control ensures operational safety, optimal energy capture, and extended turbine lifespan. High investment in offshore wind infrastructure globally further drives this segment. Technological innovations in pitch systems support durability and efficiency

Report Scope and Asia-Pacific Wind Turbine Pitch System Market Segmentation

|

Attributes |

Asia-Pacific Wind Turbine Pitch System Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Asia-Pacific Wind Turbine Pitch System Market Trends

“Increasing Wind Energy Capacity”

- The Asia-Pacific Wind Turbine Pitch System Market is witnessing robust growth with the continuous expansion of wind energy projects, driven by the urgent need for renewable power generation. Pitch systems are essential in controlling the angle of turbine blades, ensuring maximum efficiency, safety, and output reliability across varying wind conditions

- For instance, companies such as Vestas and Siemens Gamesa have invested in advanced blade pitch systems that enhance turbine performance and reduce operational downtime. Their innovations underline the importance of pitch control technology in achieving higher capacity utilization factors in both onshore and offshore wind farms

- As global wind energy capacity continues to expand, pitch systems are playing a critical role in enabling larger turbine designs with higher efficiency. Advanced control systems ensure longer component lifespans and optimized power curves, enhancing the economics of wind projects

- Growing investments in offshore wind farms have further intensified the demand for reliable pitch control solutions. Offshore turbines, subject to harsher environmental conditions, rely on advanced hydraulic and electric pitch systems to withstand variability and improve resilience while maximizing electricity output

- Technological advancements in digitalization and predictive maintenance are being integrated into modern pitch systems, enabling real-time monitoring and fault detection. These innovations improve turbine reliability, reduce maintenance costs, and increase long-term operational efficiency for energy producers

- The increasing wind capacity highlights the pivotal role of pitch systems in ensuring safe, efficient, and profitable wind power generation. This trend will continue to reinforce their importance as renewable energy becomes central to power infrastructure strategies

Asia-Pacific Wind Turbine Pitch System Market Dynamics

Driver

“Favourable Government Policies”

- Favourable government policies supporting renewable energy development are a major driver of the Asia-Pacific Wind Turbine Pitch System Market, as incentives and regulatory frameworks encourage the expansion of wind energy infrastructure. Subsidies, tax credits, and renewable energy targets are promoting investments in new wind projects worldwide

- For instance, the U.S. government’s Production Tax Credit (PTC) and Europe’s Green Deal policies have accelerated the installation of wind power capacity. Global turbine players such as GE Renewable Energy and Nordex are expanding their pitch system offerings to meet demand generated by policy-driven projects

- Government initiatives often focus on long-term carbon neutrality goals, pushing utilities and developers to adopt larger turbines with innovative components such as advanced pitch systems. This ensures compliance with climate targets while improving efficiency and lowering the cost of renewable electricity

- In emerging economies, favourable renewable energy policies in countries such as India and China are fueling rapid expansion of wind installations. These programs directly boost the demand for pitch systems, as technology providers seek to support faster project deployment

- The alignment of global climate commitments, public funding support, and private sector investments ensures that government policies will remain a key driver for the widespread adoption of wind turbines and their associated pitch systems across markets

Restraint/Challenge

“High Initial Investment”

- A significant challenge in the Asia-Pacific Wind Turbine Pitch System Market is the high upfront capital involved in advanced pitch control technologies, which adds to the overall cost of wind turbine installation and project financing. This cost sensitivity is a deterrent for smaller developers and emerging markets

- For instance, many independent power producers in developing regions struggle to secure financing for projects requiring premium pitch systems from suppliers such as Siemens Gamesa and Vestas. The higher procurement and installation costs limit accessibility for price-sensitive operators despite long-term operational benefits

- Compared to conventional energy sources, wind projects already require heavy investments in turbine infrastructure, grid integration, and land acquisition. The additional costs associated with advanced blade pitch systems amplify the financial burden during early project phases

- The complexity of installation and maintenance further increases lifecycle costs, as advanced pitch systems require skilled technicians and periodic component replacement. This can create challenges for projects in remote or emerging regions with limited technical infrastructure

- Addressing the challenge of high initial costs will require innovative financing structures, partnerships, and cost-optimized pitch technologies that reduce expenditures without compromising efficiency. These solutions will be critical in ensuring broader adoption and long-term competitiveness of wind energy globally

Asia-Pacific Wind Turbine Pitch System Market Scope

The market is segmented on the basis of product type, function, diameter size, turbine power, services, system type, and application.

• By Product Type

On the basis of product type, the Asia-Pacific Wind Turbine Pitch System Market is segmented into pitch valves, pitch pumps, pitch motors, pitch servo drives, remote terminal solution, and others. The pitch motors segment dominated the largest market revenue share in 2024, driven by its pivotal role in precise blade angle control and maximizing energy capture. Pitch motors ensure smooth blade movement under variable wind conditions, enhancing operational efficiency and reducing mechanical stress. Their compatibility with turbine control systems and ability to support both onshore and offshore turbines further bolster adoption. Technological advancements are improving motor durability and reducing maintenance cycles, increasing reliability. Manufacturers prefer pitch motors for retrofit and new turbine installations due to these operational advantages.

The pitch servo drives segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by the rising demand for automation and highly responsive control systems. Servo drives enable precise adjustments to blade pitch in real-time, optimizing energy output while minimizing wear on turbine components. Their integration with advanced turbine control software and predictive maintenance systems enhances performance monitoring. The adoption of smart turbine solutions and Industry 4.0 technologies further accelerates growth. Rising investments in renewable energy infrastructure drive widespread deployment of these high-precision components.

• By Function

On the basis of function, the market is segmented into high bearing reliability, vibration control & monitoring, wind angle adjustments, condition monitoring system, and others. The wind angle adjustments segment dominated in 2024 due to its critical role in maximizing turbine efficiency. Accurate wind angle control ensures blades are optimally oriented to capture wind energy while reducing mechanical fatigue. It enhances turbine lifespan, improves energy output, and minimizes downtime. Both onshore and offshore turbines benefit from advanced wind angle systems that adapt to changing wind speeds and directions. Ongoing innovations in control algorithms and sensors further support precise adjustments.

The condition monitoring system segment is expected to witness the fastest growth rate from 2025 to 2032, driven by predictive maintenance and remote monitoring adoption. These systems provide real-time insights into turbine performance, detecting potential issues before failures occur. Monitoring reduces operational interruptions, lowers maintenance costs, and ensures safety. Integration with digital twin and IoT technologies enables proactive management of turbine fleets. Increasing investment in performance optimization and reliability solutions fuels growth in this segment.

• By Diameter Size

On the basis of diameter size, the market is segmented into less than 80 mts and more than 80 mts. The more than 80 mts segment dominated in 2024 due to large-scale offshore turbine deployment. Larger rotor diameters capture more wind energy, requiring advanced pitch systems for precise blade control. These systems reduce mechanical stress on blades and bearings, ensuring stable operation under high wind loads. Utility-scale projects prefer larger turbines for maximum energy efficiency. Technological improvements in motors and drives further support large-diameter turbine performance. The segment benefits from rising offshore wind farm installations globally.

The less than 80 mts segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by small- to mid-scale onshore projects. These turbines offer cost-effective solutions for distributed and localized power generation. Smaller diameter turbines require compact, efficient pitch systems that are easy to install and maintain. Growth in emerging economies and residential or industrial wind projects drives this segment. Flexibility in deployment and retrofitting older turbines also contributes to adoption.

• By Turbine Power

On the basis of turbine power, the market is segmented into more than 3 MW, 1 MW to 3 MW, and less than 1 MW. The more than 3 MW segment dominated in 2024 due to widespread deployment in utility-scale wind projects. High-capacity turbines require sophisticated pitch systems for precise blade control, load management, and energy optimization. Advanced pitch systems reduce mechanical stress and ensure long-term reliability. Technological innovations enhance performance, efficiency, and integration with smart turbine management solutions. Offshore wind farms primarily utilize turbines in this category for maximizing energy output. These systems are preferred for new installations in mature wind markets.

The 1 MW to 3 MW segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by adoption in small- to mid-scale commercial projects. Turbines in this range balance cost-efficiency and energy generation capacity. Reliable pitch systems are increasingly adopted for industrial and community-based renewable energy projects. Rising renewable energy adoption in emerging markets supports segment growth. Retrofit opportunities and expansion of mid-size turbine installations further accelerate demand.

• By Services

On the basis of services, the market is segmented into field services, engineering services, technical services, measurements & data logging, aftermarket services, and others. The aftermarket services segment dominated in 2024, driven by growing demand for maintenance, repairs, and replacement of pitch system components over the turbine lifecycle. Aftermarket services ensure operational continuity, extend turbine life, and minimize downtime. This segment is particularly crucial for offshore turbines, where maintenance costs are high. Increasing turbine fleet size globally drives aftermarket service adoption. Providers offering predictive and remote services gain competitive advantages in this segment.

The measurements & data logging segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by adoption of digital monitoring and performance optimization technologies. Accurate data collection enables predictive maintenance, energy yield optimization, and failure prevention. Integration with IoT, cloud analytics, and smart control systems enhances operational efficiency. Rising focus on turbine reliability, energy forecasting, and regulatory compliance accelerates growth. Continuous technological upgrades drive adoption of measurement solutions.

• By System Type

On the basis of system type, the market is segmented into electrical pitch system and hydraulic pitch system. The electrical pitch system segment dominated in 2024 due to its high efficiency, precision, and low maintenance requirements. Electrical systems allow seamless integration with turbine control software and predictive maintenance solutions. They provide reliable performance under variable wind conditions and reduce operational costs. Growing preference for smart turbine solutions in both onshore and offshore wind farms further supports adoption. Technological advancements in compact motor and drive design enhance reliability and energy efficiency.

The hydraulic pitch system segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by robustness under high load conditions and suitability for older turbine retrofits. Hydraulic systems can handle extreme torque and are favored in heavy-duty installations. Their reliability in harsh environmental conditions drives demand, particularly in offshore wind farms. Increasing maintenance and upgrade projects support segment growth. The system is increasingly adopted for large-scale turbines where precision and load management are critical.

• By Application

On the basis of application, the market is segmented into offshore turbines and onshore turbines. The offshore turbine segment dominated the market with a share of 87.9% in 2024 due to deployment of large-scale turbines in wind farms that maximize energy generation. Offshore turbines require highly reliable pitch systems to withstand harsh marine environments and high wind loads. Advanced blade control ensures operational safety, optimal energy capture, and extended turbine lifespan. High investment in offshore wind infrastructure globally further drives this segment. Technological innovations in pitch systems support durability and efficiency.

The onshore turbine segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by small- and medium-scale projects in emerging economies. Onshore installations benefit from cost-effective and easy-to-maintain pitch systems. Rising renewable energy adoption and government incentives drive segment growth. Flexibility in retrofitting older turbines and expanding distributed power generation supports adoption. Increasing deployment in remote or decentralized locations further accelerates demand.

Asia-Pacific Wind Turbine Pitch System Market Regional Analysis

- China dominated the Asia-Pacific Wind Turbine Pitch System Market with the largest revenue share in 2024, driven by its massive wind energy installations, government-backed renewable energy targets, and extensive investments in offshore and onshore projects

- Supportive policies promoting clean energy, coupled with rapid technological advancements in turbine components and large-scale manufacturing capabilities, reinforce China’s leadership in the regional market

- The presence of leading domestic wind equipment manufacturers, strategic collaborations with global players, and continuous expansion of offshore wind farms continue to consolidate China’s dominant position during the forecast period. Ongoing grid modernization and strong funding for renewable infrastructure further strengthen market penetration across coastal and inland regions

Japan Asia-Pacific Wind Turbine Pitch System Market Insight

The Japan market is anticipated to grow steadily from 2025 to 2032, supported by its increasing offshore wind developments and government initiatives to achieve carbon neutrality. Japanese energy companies are adopting advanced pitch control technologies to enhance turbine efficiency and reliability, reflecting the country’s focus on precision engineering and renewable integration. Rising investments in smart grid systems and digital monitoring solutions are creating opportunities for high-tech pitch systems. Continuous R&D in lightweight materials and system automation reinforces Japan’s steady market expansion. The nation’s emphasis on innovation and energy sustainability underpins its strong regional positioning.

India Asia-Pacific Wind Turbine Pitch System Market Insight

India is projected to register the fastest CAGR in the Asia Pacific Asia-Pacific Wind Turbine Pitch System Market during 2025–2032, fueled by rapid wind farm installations, supportive government incentives, and aggressive renewable energy capacity targets. Growing investments from both public and private sectors, along with favorable land availability for onshore projects, are accelerating adoption. The demand for cost-effective yet reliable pitch systems is particularly strong among new wind developers. Expanding domestic manufacturing capabilities, increasing foreign partnerships, and advancements in hybrid power solutions are enhancing market accessibility. Government policies focused on green energy transition and infrastructure upgrades ensure India’s emergence as the fastest-growing market in the region.

Asia-Pacific Wind Turbine Pitch System Market Share

The wind turbine pitch system industry is primarily led by well-established companies, including:

- Vestas (Denmark)

- Siemens Gamesa Renewable Energy (Spain)

- General Electric Renewable Energy (U.S.)

- Senvion (Germany)

- Nordex SE (Germany)

- Goldwind (China)

- Suzlon Energy (India)

- Envision Energy (China)

- Mingyang Smart Energy (China)

- Enercon (Germany)

- Acciona Energía (Spain)

- Mita-Teknik (Denmark)

- Moog Inc. (U.S.)

- Atech Antriebstechnik (Germany)

- Parker Hannifin Corporation (U.S.)

Latest Developments in Asia-Pacific Wind Turbine Pitch System Market

- In October 2021, General Electric launched its second 107-meter wind turbine blade mold at its Cherbourg facility in France, aimed at producing offshore wind turbine blades exceeding 100 meters for its Haliade-X turbines. This initiative underscores GE’s commitment to meeting the rising demand for high-capacity offshore wind solutions and reinforces its position as a key player in the offshore wind market. By expanding its blade production capabilities, GE is enhancing efficiency, supporting large-scale turbine deployment, and addressing the growing need for renewable energy generation worldwide

- In February 2021, KEB Automation reported a surge in demand for its drive controllers, brakes, and motors for onshore and offshore wind turbines, highlighting its critical role in supporting turbine efficiency and performance. This development emphasizes KEB’s ability to cater to the expanding wind energy sector, including low-cost off-grid electricity solutions. By providing reliable components for both utility-scale and decentralized energy projects, KEB is strengthening its market presence and capitalizing on the rapid growth of the renewable energy industry

- In February 2021, Hydroxycut introduced CUT Energy, a clean energy drink formulated for regular consumers, fitness enthusiasts, and individuals seeking weight management solutions. This product launch demonstrates Hydroxycut’s focus on tapping into the growing health-conscious and functional beverage market. By offering an innovative, clean energy solution, the company is expanding its brand presence, catering to evolving consumer preferences, and reinforcing its position in the competitive energy drink segment

- In January 2021, KEBA announced plans to expand its facilities at Technologiering in the municipalities to increase production capacity and workforce. This expansion highlights KEBA’s commitment to meeting rising demand for automation and control technologies while ensuring operational stability. By investing in infrastructure and talent, the company is strengthening its ability to serve industrial and renewable energy markets, enhancing competitiveness, and supporting sustainable growth in a rapidly evolving sector

- In March 2020, ABB announced measures to enhance offshore wind reliability, safety, and security to support stable power transmission to the German national grid. By implementing a comprehensive system encompassing IT infrastructure, OT security, plant-wide condition monitoring, SCADA, and remote access services for DolWin5 (Epsilon), ABB is reinforcing the efficiency and stability of Germany’s renewable energy network. This initiative underscores the company’s commitment to delivering clean, reliable power while supporting the country’s energy transition goals, further strengthening ABB’s position in the wind energy solutions market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Asia Pacific Wind Turbine Pitch System Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Asia Pacific Wind Turbine Pitch System Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Asia Pacific Wind Turbine Pitch System Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.