Asia Pacific Wound Closure Devices Market

Market Size in USD Billion

USD

753.50 Billion

USD

1,307.29 Billion

2025

2033

USD

753.50 Billion

USD

1,307.29 Billion

2025

2033

| 2026 - 2033 | |

| USD 753.50 Billion | |

| USD 1,307.29 Billion | |

| % | |

|

Wound Closure Devices Market Size

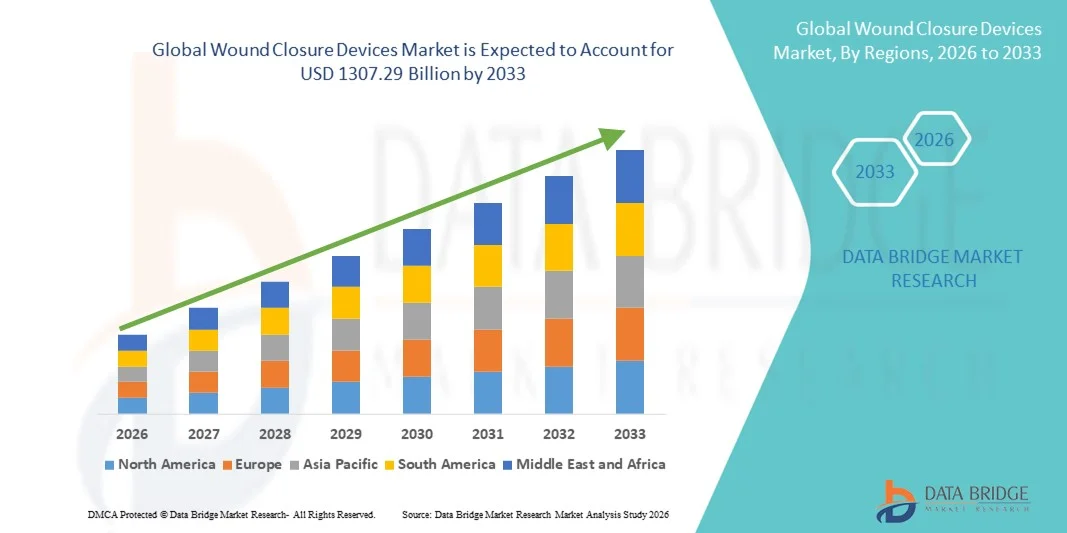

- The Asia-Pacific wound closure devices market size was valued at USD 753.50 billion in 2025 and is expected to reach USD 1307.29 billion by 2033, at a CAGR of 7.13% during the forecast period

- The market growth is largely fueled by the rising number of surgical procedures, increasing incidence of traumatic injuries, and growing prevalence of chronic wounds worldwide, leading to higher demand for effective and advanced wound closure solutions across hospitals and ambulatory surgical centers

- Furthermore, technological advancements in sutures, staples, adhesives, and hemostatic agents, along with the growing preference for minimally invasive surgeries and faster healing solutions, are establishing wound closure devices as essential components in modern surgical and emergency care. These converging factors are accelerating the uptake of Wound Closure Devices solutions, thereby significantly boosting the industry’s growth

Wound Closure Devices Market Analysis

- Wound closure devices, including sutures, staples, tissue adhesives, and hemostats, are essential components in surgical and trauma care settings due to their ability to promote faster healing, reduce infection risk, and improve cosmetic outcomes across a wide range of medical procedures

- The escalating demand for wound closure devices is primarily fueled by the increasing number of surgical procedures, rising incidence of traumatic injuries, growing prevalence of chronic wounds, and the expanding adoption of minimally invasive surgeries worldwide

- China dominated the wound closure devices market with the largest revenue share of 34.8% in 2025, driven by a high volume of surgical procedures, expanding hospital infrastructure, growing healthcare expenditure, and increasing adoption of advanced surgical products across public and private healthcare facilities

- India is expected to be the fastest-growing region in the wound closure devices market during the forecast period, expanding at a CAGR of 9.6% from 2026 to 2033, supported by improving access to surgical care, rising medical tourism, increasing awareness about advanced wound management, and government initiatives to strengthen healthcare infrastructure

- The acute wound segment held the largest market revenue share of 62.3% in 2025, owing to the high volume of surgical incisions, traumatic injuries, and lacerations worldwide

Report Scope and Wound Closure Devices Market Segmentation

|

Attributes |

Wound Closure Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Wound Closure Devices Market Trends

Advancements in Minimally Invasive and Biocompatible Wound Closure Technologies

- A significant and accelerating trend in the Asia-Pacific Wound Closure Devices market is the growing adoption of minimally invasive and biocompatible wound closure solutions designed to improve healing outcomes, reduce infection risk, and minimize scarring. Healthcare providers are increasingly preferring advanced sutures, surgical staples, tissue adhesives, and sealants that enhance procedural efficiency and patient recovery.

- For instance, in 2024, Ethicon (Johnson & Johnson MedTech) expanded its portfolio of absorbable sutures and advanced wound closure products across Asia-Pacific hospitals, supporting improved surgical precision and faster post-operative healing outcomes.

- The rising shift toward outpatient and minimally invasive surgeries is driving demand for advanced wound closure products that reduce operation time and support quicker patient discharge.

- Increasing integration of antimicrobial-coated sutures and bioengineered tissue adhesives is improving infection control and reducing post-surgical complications.

- Growing focus on cosmetic outcomes, particularly in plastic and reconstructive surgeries, is encouraging the adoption of advanced wound closure devices that minimize visible scarring and improve aesthetic results.

Wound Closure Devices Market Dynamics

Driver

Rising Surgical Procedures and Expanding Healthcare Infrastructure

- The increasing volume of surgical procedures, including cardiovascular, orthopedic, general, and cosmetic surgeries, is a major driver of the Wound Closure Devices market. Expanding hospital networks and growing access to surgical care are significantly contributing to market demand

- For instance, China dominated the Wound Closure Devices market with the largest revenue share of 34.8% in 2025, driven by a high volume of surgical procedures, expanding hospital infrastructure, growing healthcare expenditure, and increasing adoption of advanced surgical products across public and private healthcare facilities

- The growing prevalence of chronic diseases and trauma cases requiring surgical intervention is further accelerating the demand for effective wound closure solutions

- Increasing healthcare investments in emerging economies are enabling hospitals to adopt technologically advanced sutures, staples, and tissue sealants

- Rising awareness among surgeons regarding the benefits of advanced wound closure products, including reduced healing time and lower infection rates, is supporting broader clinical adoption

- In addition, India is expected to be the fastest-growing region in the Wound Closure Devices market during the forecast period, expanding at a CAGR of 9.6% from 2026 to 2033, supported by improving access to surgical care, rising medical tourism, increasing awareness about advanced wound management, and government initiatives to strengthen healthcare infrastructure

Restraint/Challenge

High Product Costs and Risk of Post-Surgical Complications

- The relatively high cost of advanced wound closure devices, particularly specialized sutures, stapling systems, and tissue adhesives, poses a challenge to adoption in cost-sensitive healthcare settings

- For instance, premium antimicrobial-coated sutures and powered surgical staplers from leading manufacturers can significantly increase procedural costs, limiting their use in smaller hospitals and rural healthcare facilities

- The risk of post-surgical complications such as wound infections, dehiscence, and allergic reactions to certain closure materials can affect product preference and clinical decisions

- Limited reimbursement coverage for advanced wound closure technologies in certain regions further restricts market penetration

- Variability in surgeon preference and the availability of traditional low-cost sutures in developing countries may slow the transition toward more advanced wound closure systems

- Overcoming these challenges will require cost-effective product innovations, improved reimbursement structures, enhanced clinical training, and greater awareness regarding the long-term benefits of advanced wound closure technologies

Wound Closure Devices Market Scope

The market is segmented on the basis of product type, wound type, application, and end user.

- By Product Type

On the basis of product type, the Wound Closure Devices market is segmented into adhesives, staples, sutures, sealants, and mechanical devices. The sutures segment dominated the largest market revenue share of 41.6% in 2025, driven by its widespread use across a broad range of surgical procedures globally. Sutures remain the standard method for wound closure due to their strong tensile strength, flexibility, and suitability for both internal and external wounds. Increasing number of surgical interventions, including orthopedic, cardiovascular, and general surgeries, significantly supports demand. Continuous advancements such as absorbable and antimicrobial-coated sutures enhance healing outcomes and reduce infection risks. Surgeons prefer sutures for precise wound approximation and reliable performance. Established clinical familiarity and cost-effectiveness further strengthen segment dominance. Growing hospital admissions and trauma cases globally also contribute to sustained revenue generation. Favorable reimbursement frameworks in developed markets support continued adoption. Expanding healthcare infrastructure in emerging economies further boosts utilization. Strong product innovation pipelines from key manufacturers enhance competitive positioning. The sutures segment is projected to grow at a CAGR of 7.9% from 2026 to 2033.

The adhesives segment is anticipated to witness the fastest CAGR of 10.8% from 2026 to 2033, driven by increasing preference for minimally invasive wound closure solutions. Adhesives offer faster application time, reduced scarring, and improved patient comfort compared to traditional sutures. Rising demand for cosmetic and outpatient procedures significantly supports growth. Technological advancements in cyanoacrylate-based and fibrin sealant products enhance bonding strength and flexibility. Growing adoption in pediatric and emergency care settings further accelerates expansion. Increased focus on reducing procedure time and improving aesthetic outcomes contributes to rapid segment penetration.

- By Wound Type

On the basis of wound type, the Wound Closure Devices market is segmented into acute wound and chronic wound. The acute wound segment held the largest market revenue share of 62.3% in 2025, owing to the high volume of surgical incisions, traumatic injuries, and lacerations worldwide. Acute wounds require immediate and effective closure to prevent infection and promote faster healing. Rising number of elective and emergency surgical procedures significantly drives demand. Increasing cases of road accidents and sports injuries further support growth. Hospitals rely heavily on advanced closure devices to minimize healing time and reduce complications. Technological improvements in absorbable sutures and mechanical staplers enhance clinical efficiency. Strong presence of surgical centers globally sustains consistent utilization. Favorable reimbursement coverage for surgical procedures further strengthens segment dominance. Growing healthcare expenditure across developing economies also contributes to expansion. The acute wound segment is projected to grow at a CAGR of 8.2% during the forecast period.

The chronic wound segment is expected to register the fastest CAGR of 11.5% from 2026 to 2033, driven by the increasing prevalence of diabetes, obesity, and vascular disorders. Chronic wounds such as diabetic foot ulcers and pressure ulcers require long-term management, increasing device utilization. Rising geriatric population significantly contributes to higher incidence rates. Growing awareness regarding advanced wound management solutions accelerates adoption. Expanding specialized wound care clinics further supports segment growth.

- By Application

On the basis of application, the Wound Closure Devices market is segmented into burns, ulcer, surgical wounds, pressure ulcers, diabetic ulcers, and arterial ulcers. The surgical wounds segment dominated the largest market revenue share of 36.8% in 2025, supported by the growing number of surgical procedures globally. Effective closure of surgical incisions is critical to reduce infection risk and improve recovery time. Increasing demand for minimally invasive and cosmetic surgeries further fuels adoption. Hospitals increasingly implement advanced closure technologies to enhance patient outcomes. Rising healthcare spending and improved surgical infrastructure strengthen market growth. Technological innovations such as antimicrobial sutures and bioactive sealants enhance healing efficiency. Strong clinical evidence supporting improved wound healing outcomes further boosts utilization. Expanding medical tourism in emerging economies also contributes to segment expansion. The segment is projected to grow at a CAGR of 8.4% from 2026 to 2033.

The diabetic ulcers segment is anticipated to witness the fastest CAGR of 12.1% from 2026 to 2033, driven by the rapidly growing diabetic population worldwide. Diabetic ulcers often lead to complications requiring advanced wound closure solutions. Rising awareness regarding early intervention and limb preservation strategies supports higher adoption. Increasing healthcare investments in chronic wound management further accelerate segment growth. Technological advancements in bioengineered skin substitutes and advanced dressings enhance healing outcomes.

- By End User

On the basis of end user, the Wound Closure Devices market is segmented into hospitals, community healthcare service providers, ambulatory surgical centers, and home care. The hospitals segment accounted for the largest revenue share of 54.7% in 2025, driven by high patient admissions and surgical procedure volumes. Hospitals remain primary centers for complex wound management and emergency trauma care. Availability of skilled surgeons and advanced medical infrastructure supports effective device utilization. Strong procurement contracts and reimbursement systems further strengthen segment leadership. Increasing number of specialized surgical departments globally sustains demand. Continuous adoption of advanced wound closure technologies enhances patient outcomes. Rising trauma and accident cases further contribute to growth. The segment is projected to grow at a CAGR of 7.8% during the forecast period.

The ambulatory surgical centers segment is expected to witness the fastest CAGR of 10.6% from 2026 to 2033, fueled by the growing preference for outpatient surgical procedures. Ambulatory centers offer cost-effective and efficient surgical care, reducing hospital burden. Increasing shift toward minimally invasive surgeries significantly supports segment expansion. Improved healthcare accessibility and shorter patient recovery times further enhance adoption. Rising patient preference for same-day discharge procedures further accelerates demand for efficient wound closure solutions in these settings. Ambulatory surgical centers are increasingly equipped with advanced surgical tools and skilled professionals, enabling safe and effective wound management. Lower procedural costs compared to hospital-based surgeries make these centers attractive for both patients and insurers. Favorable reimbursement policies for outpatient procedures in several developed countries also contribute to growth. Growing number of cosmetic, orthopedic, and ophthalmic surgeries performed in ambulatory centers boosts device utilization. Technological advancements in absorbable sutures, adhesives, and stapling devices enhance procedural efficiency. Increasing investments in expanding ambulatory care infrastructure further strengthen segment expansion. In addition, the rising focus on reducing hospital-acquired infections supports the continued shift toward outpatient surgical environments throughout the forecast period.

Wound Closure Devices Market Regional Analysis

- The Asia-Pacific wound closure devices market is projected to witness strong growth during the forecast period of 2026 to 2033, driven by the rising number of surgical procedures, expanding healthcare infrastructure, and increasing healthcare expenditure across developing economies

- Rapid urbanization and improving access to hospital care in countries such as China, Japan, and India are significantly contributing to market expansion. The growing burden of chronic diseases, trauma injuries, and elective surgical procedures is increasing demand for advanced wound closure products, including sutures, surgical staples, and tissue adhesives

- Government initiatives aimed at strengthening healthcare systems, expanding public hospital capacity, and promoting domestic medical device manufacturing are further supporting regional growth. In addition, the presence of global medical device manufacturers and improving distribution networks are enhancing the accessibility of advanced wound closure technologies across urban and semi-urban healthcare facilities

China Wound Closure Devices Market Insight

China wound closure devices market dominated the Asia-Pacific wound closure devices market with the largest revenue share of 34.8% in 2025, driven by a high volume of surgical procedures, expanding hospital infrastructure, growing healthcare expenditure, and increasing adoption of advanced surgical products across public and private healthcare facilities. The rapid expansion of tertiary hospitals and specialty surgical centers has significantly boosted demand for sutures, staples, and tissue adhesives. Rising prevalence of chronic diseases and increasing trauma cases further contribute to sustained product demand. Strong government investments in healthcare modernization and support for domestic medical device manufacturing are enhancing market penetration. Moreover, the growing availability of cost-competitive products from local manufacturers is expanding access across both metropolitan and secondary cities.

India Wound Closure Devices Market Insight

India wound closure devices market is expected to be the fastest-growing market in the Asia-Pacific wound closure devices sector, expanding at a CAGR of 9.6% from 2026 to 2033. Growth is supported by improving access to surgical care, rising medical tourism, increasing awareness about advanced wound management, and government initiatives aimed at strengthening healthcare infrastructure. The expansion of multi-specialty hospitals, growing private healthcare investments, and increasing surgical volumes are contributing to higher demand for wound closure products. In addition, the rising incidence of lifestyle-related diseases and trauma injuries is accelerating the adoption of advanced sutures and stapling devices. As healthcare facilities continue to modernize and adopt international treatment standards, demand for high-quality and cost-effective wound closure solutions is expected to increase significantly during the forecast period.

Wound Closure Devices Market Share

The Wound Closure Devices industry is primarily led by well-established companies, including:

- Johnson & Johnson (U.S.)

- Medtronic plc (Ireland)

- 3M Company (U.S.)

- B. Braun S.E. (Germany)

- Smith & Nephew plc (U.K.)

- Baxter International Inc. (U.S.)

- Ethicon, Inc. (U.S.)

- Integra LifeSciences Holdings Corporation (U.S.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Teleflex Incorporated (U.S.)

- ConvaTec Group plc (U.K.)

- Coloplast A/S (Denmark)

- Derma Sciences, Inc. (U.S.)

- DemeTECH Corporation (U.S.)

- Peters Surgical (France)

- Advanced Medical Solutions Group plc (U.K.)

- Medline Industries, LP (U.S.)

- Meril Life Sciences Pvt. Ltd. (India)

- Apollo Endosurgery, Inc. (U.S.)

- Kikgel S.A. (Poland)

Latest Developments in Asia-Pacific Wound Closure Devices Market

- In March 2021, Ethicon Endo-Surgery launched the ECHELON™+ Powered Stapler with GST Reloads, a new surgical stapling system designed to improve staple line security and uniform tissue compression in challenging procedures, helping reduce complications and improve surgical outcomes

- In August 2023, Healthium Medtech announced the launch of TRUMAS, a new range of sutures designed specifically for minimally invasive surgery applications, featuring optimized needle and suture combinations to improve handling and surgical efficiency

- In October 2024, Corza Medical launched its Onatec ophthalmic microsurgical sutures at the American Academy of Ophthalmology (AAO) Conference, introducing an advanced suture product designed for delicate eye surgery procedures

- In July 2024, Connexicon Medical’s Tissue Adhesive Skin Closure System received FDA approval, marking the introduction of a suture-free skin closure technology that aims to simplify wound closure and reduce procedure time for minor surgical wounds and lacerations

- In December 2024, H.B. Fuller Company announced the acquisition of GEM S.r.l. and Medifill Ltd, two medical adhesive technology firms, strengthening its wound closure adhesives portfolio and expanding its foothold in advanced closure technologies

- In January 2024, Stryker Corporation launched Zip® One, a non-invasive wound closure device that provides a suture-free option designed to reduce scarring and speed healing, reflecting the market trend toward patient-centric, minimally traumatic closure solutions

- In February 2025, Stryker received FDA approval for its new VELHOX Wound Closure System, a unique vacuum-assisted closure technology designed to improve wound healing outcomes and expand Stryker’s advanced wound care portfolio

- In January 2025, Cresilon received FDA approval for Traumagel, a novel plant-based hydrogel for severe bleeding control that supports closure and hemostasis as part of wound management strategies, reinforcing innovation beyond traditional sutures and staples

- In May 2025, Johnson & Johnson Services, Inc. announced the ECHELON LINEAR Cutter featuring 3D-Stapling Technology, a next-generation staple device designed to improve staple line security and enhance surgical precision in complex procedures

- In November 2025, Xtant Medical Holdings, Inc. launched CollagenX, a bovine collagen particulate product for surgical wound closure designed to promote healing and reduce infection risk — a notable late-2025 market entry in closure products

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.