Europe Autologous Stem Cell And Non Stem Cell Based Therapies Market

Market Size in USD Billion

USD

26.17 Billion

USD

4.24 Billion

2024

2032

USD

26.17 Billion

USD

4.24 Billion

2024

2032

| 2025 - 2032 | |

| USD 26.17 Billion | |

| USD 4.24 Billion | |

| % | |

|

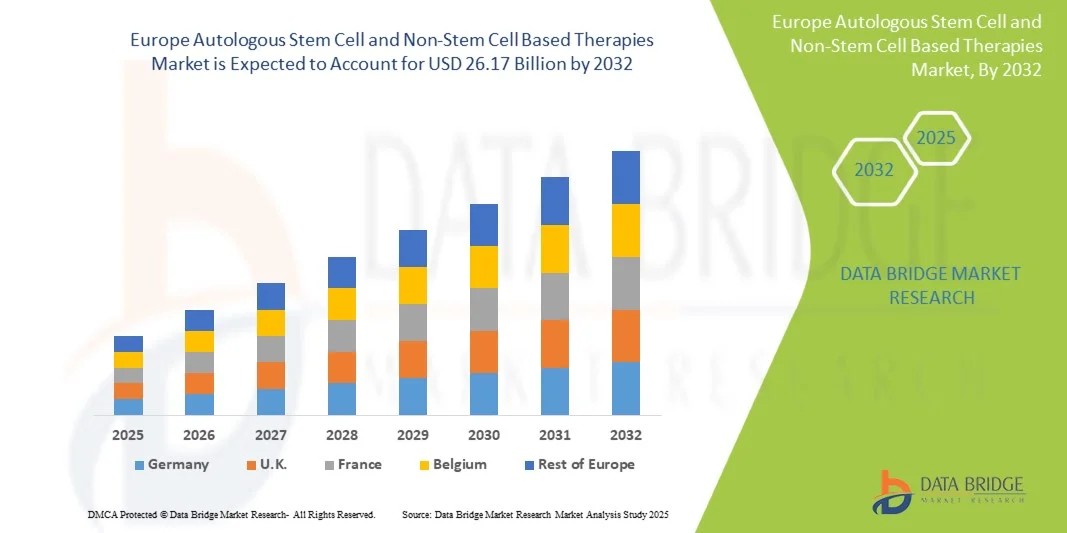

Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market Size

- The Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market size was valued at USD 4.24 billion in 2024 and is expected to reach USD 26.17 billion by 2032, at a CAGR of 13.90% during the forecast period

- The market growth is largely fueled by the increasing adoption and technological progress within regenerative medicine and advanced cellular therapies, leading to rising digitalization and innovation in both research and clinical settings

- Furthermore, rising patient demand for safe, personalized, and effective treatment options for chronic diseases, degenerative disorders, and cancer is establishing autologous stem cell and non-stem cell based therapies as a preferred solution in modern healthcare. These converging factors are accelerating the uptake of autologous stem cell and non-stem cell based therapies, thereby significantly boosting the industry's growth

Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market Analysis

- Autologous stem cell and non-stem cell based therapies are increasingly vital in regenerative medicine, offering personalized treatment approaches for conditions such as neurodegenerative disorders, cardiovascular diseases, orthopedic injuries, and certain types of cancers due to their ability to repair, regenerate, or replace damaged tissues

- The escalating demand for these therapies is primarily fueled by the rising prevalence of chronic diseases, increasing awareness of regenerative medicine, and advancements in stem cell processing and delivery technologies, alongside strong government and private funding in research and clinical applications

- Germany dominated the Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market with the largest revenue share of 34.8% in 2024, supported by its strong pharmaceutical and biotechnology sector, extensive clinical trial activity, and high adoption of advanced cell therapies in both hospitals and research institutions. The country’s well-established healthcare infrastructure and focus on innovation in regenerative medicine continue to strengthen its leadership position

- France is expected to be the fastest-growing country in the Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market during the forecast period, driven by rising investments in biotechnology, expansion of stem cell research programs, and government-backed initiatives to improve access to advanced therapies. Growing patient awareness and rapid adoption of novel treatment modalities in hospitals and research centers are accelerating France’s market growth

- The Blood Pressure (BP) Monitoring Devices segment dominated the Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market with 45.6% share in 2024, driven by its extensive use in both hospital and home-care settings to monitor cardiovascular health

Report Scope and Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market Segmentation

|

Attributes |

Autologous Stem Cell and Non-Stem Cell Based Therapies Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market Trends

Enhanced Advancements Through Personalized and Regenerative Therapies

- A significant and accelerating trend in the Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market is the growing focus on personalized regenerative medicine, where therapies are tailored to individual patient needs for more effective outcomes. This shift is enhancing patient care across conditions such as cardiovascular diseases, neurological disorders, orthopedic injuries, and oncology

- For instance, several European biotech companies and research institutions are advancing clinical trials in autologous stem cell therapies aimed at repairing damaged tissues, improving mobility, and restoring organ functions. Such progress is expected to drive strong adoption during the forecast period

- Continuous improvements in delivery devices, such as advanced insulin-like infusion systems and stem cell injectors, are allowing for greater precision, safety, and patient comfort. These innovations are also making therapies more accessible for both hospital settings and at-home administration

- The integration of regenerative therapies into mainstream healthcare systems across Europe is creating a unified approach to chronic disease management, as hospitals, universities, and research centers adopt cutting-edge techniques and infrastructure to support clinical applications

- This trend toward advanced, intuitive, and patient-focused therapies is fundamentally reshaping expectations within the healthcare sector. Consequently, leading European pharmaceutical and biotechnology companies are developing next-generation devices and therapies with improved usability, treatment outcomes, and accessibility

- The demand for autologous stem cell and non-stem cell based therapies that provide enhanced safety, effectiveness, and personalized treatment options is growing rapidly across both clinical and research applications, as patients and healthcare providers increasingly prioritize long-term health management and regenerative solutions

Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market Dynamics

Driver

Growing Need Due to Rising Prevalence of Chronic Diseases and Expanding Clinical Applications

- The increasing prevalence of chronic diseases such as cardiovascular disorders, diabetes, and neurodegenerative conditions, coupled with the growing adoption of regenerative medicine approaches, is a significant driver for the heightened demand for autologous stem cell and non-stem cell based therapies in Europe

- For instance, in April 2024, European research consortia announced advancements in stem cell–based therapies targeting osteoarthritis and spinal cord injury, highlighting the region’s strong focus on translating clinical research into accessible therapeutic solutions. Such strategies by key institutions and biotechnology companies are expected to drive market growth in the forecast period

- As patients and healthcare providers become more aware of the benefits of regenerative and cell-based therapies, these solutions are increasingly seen as offering advantages over conventional treatments, particularly for conditions with limited therapeutic options

- Furthermore, the growing popularity of clinical trials and collaborative research programs across Europe is making autologous and non-stem cell therapies an integral component of modern healthcare strategies, offering potential for tissue repair, disease modification, and long-term patient benefits

- The convenience of using patients’ own cells (in autologous therapies), reduced risks of immune rejection, and the ability to develop personalized treatment plans are key factors propelling adoption across hospitals, research centers, and specialty clinics. The trend towards expanding indications and wider clinical accessibility further contributes to market growth

Restraint/Challenge

Concerns Regarding High Costs and Regulatory Complexities

- Concerns surrounding the high costs of developing and administering autologous stem cell and non-stem cell based therapies pose a significant challenge to broader market penetration. As these therapies involve advanced technologies, specialized facilities, and stringent quality standards, treatment affordability remains a barrier for many patients

- For instance, several high-profile reports from European healthcare organizations indicate that reimbursement hurdles and cost-related restrictions limit patient access to stem cell therapies, slowing down their adoption across public healthcare systems

- Addressing these challenges through clear regulatory pathways, streamlined approval processes, and supportive reimbursement frameworks is crucial for building patient and provider confidence. Companies and research groups emphasize their efforts in conducting cost-effectiveness studies and engaging with health authorities to ease adoption barriers

- In addition, the relatively complex production and handling requirements of these therapies compared to conventional drugs can slow market expansion, particularly in regions with limited infrastructure or lower healthcare spending. While technological advancements are gradually improving efficiency, the perceived premium cost and logistical challenges can still hinder widespread availability

- Overcoming these challenges through collaborative clinical networks, supportive government initiatives, and innovations in cost-efficient manufacturing will be vital for sustained market growth in Europe’s autologous stem cell and non-stem cell based therapies sector

Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market Scope

The market is segmented on the basis of product, application, and end user.

• By Product

On the basis of product, the Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market is segmented into Blood Pressure (BP) Monitoring Devices, Pulmonary Pressure Monitoring Devices, and Intracranial Pressure (ICP) Monitoring Devices. The Blood Pressure (BP) Monitoring Devices segment dominated the market with 45.6% share in 2024, driven by its extensive use in both hospital and home-care settings to monitor cardiovascular health. The increasing prevalence of hypertension and cardiovascular complications across Europe has significantly boosted demand for these devices. Technological advancements such as wireless connectivity and wearable BP monitoring systems are further supporting their adoption. In addition, the affordability and easy availability of BP monitors have enhanced their penetration into home-care environments. Government awareness programs promoting early detection of cardiovascular risks also contribute to their dominance. The strong integration of BP monitoring into digital health ecosystems ensures continuous demand and growth.

The Pulmonary Pressure Monitoring Devices segment is expected to grow at the fastest CAGR of 20.4% from 2025 to 2032, supported by rising cases of chronic respiratory disorders such as COPD, asthma, and pulmonary hypertension. The growing geriatric population in Europe, particularly in Germany, Italy, and France, is further contributing to the need for pulmonary monitoring. The shift toward remote patient monitoring and telehealth integration enhances adoption of these devices. Pulmonary monitoring is gaining importance in post-COVID respiratory care, ensuring long-term demand. In addition, advanced implantable and minimally invasive sensors are being introduced by manufacturers, accelerating growth. The growing clinical trials and regulatory approvals for pulmonary monitoring innovations also expand the market opportunity. This segment is increasingly supported by healthcare digitization policies across the EU.

• By Application

On the basis of application, the Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market is segmented into neurodegenerative disorders, autoimmune diseases, cancer and tumours, and cardiovascular diseases. The cancer and tumours segment held the largest market share of 42.3% in 2024, owing to the rising incidence of cancer cases across Europe and the growing adoption of autologous stem cell therapies for oncology treatment. Stem cell-based therapies are increasingly being used alongside chemotherapy and radiation to restore hematopoietic function. European research institutes and biotech companies are actively investing in oncology-focused stem cell trials, further fueling growth. The availability of advanced cell processing facilities and supportive government funding in countries like Germany, the U.K., and France also enhance adoption. High patient demand for personalized therapies that minimize side effects is another growth driver. Partnerships between hospitals and biopharma companies are ensuring wider clinical accessibility.

The neurodegenerative disorders segment is projected to grow at the fastest CAGR of 19.8% during 2025–2032, driven by the increasing prevalence of conditions such as Alzheimer’s, Parkinson’s, and multiple sclerosis across Europe. Aging demographics are a major factor, particularly in countries with rapidly growing elderly populations. Stem cell therapies offer promising potential for neuronal repair and regeneration, driving heavy investment into R&D. Clinical trials in the U.K., Sweden, and Switzerland are accelerating innovation in this area. Regulatory flexibility for advanced therapy medicinal products (ATMPs) is creating opportunities for commercialization of neuro-focused stem cell solutions. The segment is also supported by rising healthcare expenditure and patient advocacy for innovative treatment alternatives.

• By End User

On the basis of end user, the Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market is segmented into hospitals and ambulatory surgical centres, and others. The Hospitals and Ambulatory Surgical Centres segment dominated the market with 68.5% share in 2024, as hospitals remain the primary centers for advanced stem cell therapy procedures, monitoring, and recovery. Large-scale infrastructure, availability of trained specialists, and the presence of stem cell banking units within hospitals support their market dominance. Hospitals are also heavily involved in clinical trials and collaborations with biotech firms, further expanding their role in this market. Increased government funding for public hospital research centers across Europe provides an additional boost. Patient preference for comprehensive, high-standard treatment facilities consolidates their dominant position.

The Others segment (including research institutes, academic centers, and specialized clinics) is expected to register the fastest CAGR of 17.6% between 2025 and 2032, supported by increasing investments in research-based therapy development. Research centers and academic institutes are playing a critical role in preclinical and translational studies, especially in Germany, Switzerland, and the U.K. Growing collaborations between biotech startups and universities are enabling new therapy innovations. Specialized clinics focusing on regenerative medicine are emerging across Europe, offering niche services. The segment also benefits from EU research grants supporting innovation in personalized medicine and stem cell applications.

Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market Regional Analysis

- The Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the rising prevalence of chronic diseases, expanding applications of regenerative medicine, and the growing number of clinical trials across the region

- Germany dominated the Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market with the largest revenue share of 34.8% in 2024, supported by its strong pharmaceutical and biotechnology sector, extensive clinical trial activity, and high adoption of advanced cell therapies in both hospitals and research institutions. The country’s well-established healthcare infrastructure and focus on innovation in regenerative medicine continue to strengthen its leadership position

- France is expected to be the fastest-growing country in the Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market during the forecast period, driven by rising investments in biotechnology, expansion of stem cell research programs, and government-backed initiatives to improve access to advanced therapies. Growing patient awareness and rapid adoption of novel treatment modalities in hospitals and research centers are accelerating France’s market growth

Germany Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market Insight

The Germany Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market is expected to expand at a considerable CAGR during the forecast period, driven by its strong pharmaceutical and biotechnology sector, extensive clinical trial activity, and high adoption of advanced cell therapies in hospitals and research institutions. Germany dominated the European Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market with the largest revenue share of 34.8% in 2024, supported by its well-established healthcare infrastructure and emphasis on innovation in regenerative medicine. The country’s leadership in advanced therapy development and robust investment in cell-based research continue to strengthen its dominant position within the European market.

France Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market Insight

The France Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market is expected to be the fastest-growing country in the European market during the forecast period, fueled by rising investments in biotechnology, the expansion of stem cell research programs, and supportive government policies aimed at enhancing access to advanced therapies. Growing patient awareness, coupled with the rapid adoption of novel treatment modalities in hospitals and research centers, is accelerating demand. Furthermore, the establishment of new clinical facilities and collaborations with international biotech firms are positioning France as a key growth hub within the European regenerative medicine landscape.

Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market Share

The autologous stem cell and non-stem cell based therapies industry is primarily led by well-established companies, including:

- Vericel Corporation (U.S.)

- BrainStorm Cell Limited (U.S.)

- Lisata Therapeutics, Inc. (U.S.)

- Holostem Terapie Avanzate S.r.l. (Italy)

- Takeda Pharmaceutical Company Limited (Japan)

- TiGenix NV (Belgium)

- Pharmicell Co., Ltd. (South Korea)

- ANTEROGEN CO., LTD. (South Korea)

- Cynata Therapeutics Limited (Australia)

- Cambium Bio Limited. (Australia)

- Pluri Biotech Ltd. (Israel)

- Mesoblast Limited (Australia)

- MEDIPOST Co., Ltd. (South Korea)

- Osiris Therapeutics, Inc. (U.S.)

- Cytori Therapeutics, Inc. (U.S.)

Latest Developments in Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market

- In May 2022, Novartis announced that Kymriah (tisagenlecleucel) received a new European Commission approval expanding its indication to include adult patients with relapsed or refractory follicular lymphoma, marking an important regulatory milestone for this autologous CAR-T therapy in Europe

- In June 2022, Gilead’s Kite unit announced that Yescarta (axicabtagene ciloleucel) was granted a European marketing authorization for the treatment of relapsed or refractory follicular lymphoma, expanding the use of this autologous CAR-T product in the EU

- In April 2022, Bristol Myers Squibb (BMS) announced that the European Commission approved Breyanzi (lisocabtagene maraleucel; liso-cel) for certain relapsed or refractory forms of large B-cell lymphoma in the EU, further broadening the availability of autologous CAR-T therapies in Europe

- In March 2022, the European Commission withdrew the marketing authorisation for Zynteglo (betibeglogene autotemcel), bluebird bio’s autologous gene therapy for transfusion-dependent β-thalassaemia, after the company requested discontinuation for commercial reasons; this is a notable commercial/regulatory development affecting autologous gene/cell therapies in Europe.

- In November 2024, Autolus announced that the U.S. FDA approved AUCATZYL (obecabtagene autoleucel, “obe-cel”) for adult patients with relapsed/refractory B-cell precursor acute lymphoblastic leukemia, and the company stated regulatory submissions/under-review status in the EU — a development that led to subsequent CHMP/EC activity in 2025

- In May 2025, the EMA’s CHMP issued a positive opinion recommending approval of obecabtagene autoleucel (obe-cel) for adult relapsed/refractory B-ALL — a key regulatory step prior to the European Commission decision

- In July 2025 the European Commission granted marketing authorisation for AUCATZYL (obecabtagene autoleucel) for adult patients with relapsed/refractory B-cell precursor acute lymphoblastic leukemia — the final EU approval following the CHMP positive opinion (included here because the CHMP opinion and company regulatory filings occurred in 2024–2025)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.