Europe Bone Densitometer Devices Market

Market Size in USD Billion

USD

265.50 Billion

USD

374.68 Billion

2025

2033

USD

265.50 Billion

USD

374.68 Billion

2025

2033

| 2026 - 2033 | |

| USD 265.50 Billion | |

| USD 374.68 Billion | |

| % | |

|

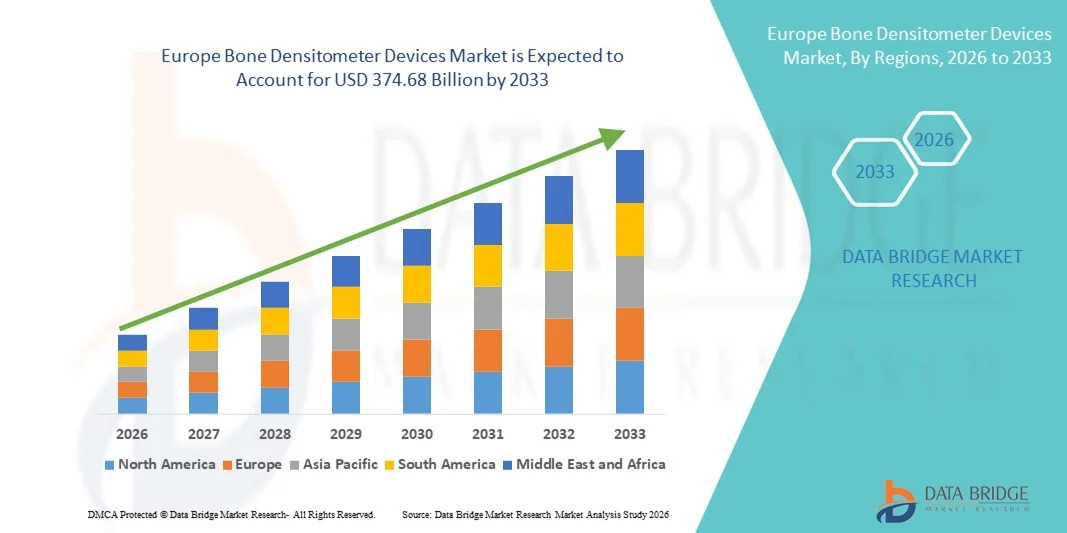

Europe Bone Densitometer Devices Market Size

- The Europe bone densitometer devices market size was valued at USD 265.5 billion in 2025 and is expected to reach USD 374.68 billion by 2033, at a CAGR of 4.40% during the forecast period

- The market growth is largely fueled by the rising prevalence of osteoporosis and other bone-related disorders, an aging global population, and increasing awareness of bone health, leading to higher adoption of bone densitometer devices across hospitals, diagnostic centers, and specialty clinics

- Furthermore, growing patient demand for early detection and preventive care, coupled with technological advancements such as dual-energy X-ray absorptiometry (DEXA) systems, portable bone densitometers, and AI-assisted analysis for more accurate assessments, is establishing bone densitometer devices as essential tools in modern healthcare. These converging factors are accelerating the uptake of Bone Densitometer Devices solutions, thereby significantly boosting overall market growth

Europe Bone Densitometer Devices Market Analysis

- Bone densitometer devices, including dual-energy X-ray absorptiometry (DEXA) systems and peripheral bone densitometers, are increasingly vital components of modern healthcare for assessing bone mineral density, diagnosing osteoporosis, and monitoring treatment efficacy across hospitals, diagnostic centers, and specialty clinics

- The escalating demand for bone densitometer devices is primarily fueled by the rising prevalence of osteoporosis and other bone-related disorders, an aging global population, increasing awareness of bone health, and technological advancements such as AI-assisted analysis and portable DEXA systems that improve diagnostic accuracy and patient convenience

- The U.K. dominated the bone densitometer devices market with the largest revenue share of 27.8% in 2025, characterized by advanced healthcare infrastructure, high awareness of osteoporosis screening programs, strong reimbursement policies, and the presence of specialized diagnostic centers adopting state-of-the-art densitometry technologies

- Germany is expected to be the fastest growing country in the bone densitometer devices market during the forecast period, driven by increasing geriatric population, rising incidence of bone-related disorders, growing adoption of portable and AI-assisted bone densitometers, and expanding healthcare expenditure on preventive diagnostics

- Osteoporosis & Osteopenia Diagnosis dominated the largest revenue share of 64.8% in 2025, due to the rising prevalence of osteoporosis globally, especially among the aging population

Report Scope and Bone Densitometer Devices Market Segmentation

|

Attributes |

Bone Densitometer Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Bone Densitometer Devices Market Trends

Rising Adoption of Advanced Imaging Technologies

- A key trend in the Europe Bone Densitometer Devices market is the increasing adoption of advanced imaging technologies, including dual-energy X-ray absorptiometry (DEXA), peripheral quantitative computed tomography (pQCT), and portable bone density systems

- These devices provide precise, non-invasive assessment of bone mineral density, supporting early diagnosis of osteoporosis and fracture risk management

- For instance, in 2024, Hologic launched its new Horizon A densitometer in Germany, which integrates low-dose imaging with advanced software for fracture risk assessment, demonstrating the shift toward high-precision diagnostic tools

- Healthcare providers are increasingly investing in compact and multi-functional densitometers that combine body composition analysis with bone density testing, improving workflow efficiency and patient throughput

- Integration of densitometry into routine preventive care, wellness checkups, and geriatric assessments is further enhancing its adoption across clinics, hospitals, and diagnostic centers

Europe Bone Densitometer Devices Market Dynamics

Driver

Growing Prevalence of Osteoporosis and Aging Population

- The rising incidence of osteoporosis, particularly among the aging European population, is a major driver of Bone Densitometer Devices market growth. Early detection and continuous monitoring of bone health are critical for reducing fracture-related morbidity and healthcare costs

- For instance, in the U.K., the National Osteoporosis Society has partnered with local hospitals to encourage annual bone density screening for women over 65, boosting demand for clinical densitometers

- Increasing awareness among clinicians and patients about the importance of bone density testing is driving routine adoption in hospitals, outpatient clinics, and private specialty centers

- Government and private healthcare reimbursement policies supporting preventive diagnostics, combined with technological improvements like faster scan times, automated reporting, and reduced radiation exposure, are further fueling market growth

- Moreover, growing demand for combined bone and body composition assessments in obesity management and metabolic disorder clinics is creating a broader application base for densitometer devices

Restraint/Challenge

High Costs and Limited Accessibility

- The relatively high acquisition and maintenance costs of advanced bone densitometer devices pose a barrier to adoption, especially for smaller clinics and budget-constrained healthcare facilities

- For instance, in rural regions of Germany and Eastern Europe, lack of modern diagnostic centers equipped with DEXA or pQCT machines limits patient access to routine bone health assessments

- While portable and compact densitometers are becoming more affordable, the perceived high upfront costs continue to challenge widespread adoption, particularly in developing or underserved areas

- Maintenance, calibration requirements, and the need for trained personnel to operate densitometer devices add additional operational expenses that can deter smaller facilities

- Overcoming these challenges through cost-effective devices, telemedicine-enabled diagnostics, mobile screening programs, and expanded healthcare infrastructure will be critical for sustained market growth

Europe Bone Densitometer Devices Market Scope

The market is segmented on the basis of type, technology, application, and end user.

- By Type

On the basis of type, the Bone Densitometer Devices market is segmented into Central Scan and Peripheral Scan. The Central Scan segment dominated the largest market revenue share of 56.4% in 2025, primarily due to its ability to provide accurate bone mineral density measurements at the spine and hip, which are critical sites for osteoporosis diagnosis. Central scan devices are widely adopted in hospitals, specialty clinics, and diagnostic centers for advanced screening and monitoring. They support dual-energy X-ray absorptiometry (DXA), which is considered the gold standard for bone health assessment. Hospitals and research institutions prefer central scanners due to their high precision, reproducibility, and ability to monitor treatment response over time. Integration with PACS systems and hospital IT infrastructure further strengthens adoption. Central scan devices also benefit from strong clinical validation, regulatory approvals, and insurance reimbursement frameworks in developed markets. Rising awareness of osteoporosis and aging populations in North America and Europe are driving consistent demand. Multi-functional capabilities, such as body composition analysis and vertebral fracture assessment, enhance utility. Their reliability and ability to support high patient throughput maintain dominance in the overall market.

The Peripheral Scan segment is expected to witness the fastest CAGR of 20.7% from 2026 to 2033, driven by the growing need for portable, cost-effective bone densitometry in clinics, rural areas, and home care settings. Peripheral scanners are lightweight, easier to operate, and suitable for screening the wrist, heel, and finger, providing initial diagnostic insights. Adoption is rising in outpatient clinics, wellness centers, and mobile diagnostic units where central scanners are unavailable. Increasing prevalence of osteoporosis screening programs in emerging markets fuels growth. Advancements in portable dual-energy and ultrasound-based devices enhance diagnostic reliability. Peripheral devices allow early intervention and preventive care, creating awareness-driven demand. Integration with cloud-based reporting systems and smartphone apps supports remote monitoring and telehealth initiatives. Rising geriatric population and patient preference for quick, non-invasive tests contribute to expansion. Affordable pricing and ease of transport further accelerate adoption. Ongoing innovations in compact design and improved detection accuracy strengthen growth prospects.

- By Technology

On the basis of technology, the market is segmented into Dual Energy X-ray Absorptiometry (DXA), Single X-Ray Absorptiometry (SXA), Radiographic Absorptiometry, Quantitative Computed Tomography (QCT), Ultrasound, and Other technologies. DXA dominated the largest revenue share of 61.5% in 2025, owing to its high accuracy, reproducibility, and widespread acceptance as the clinical gold standard for osteoporosis diagnosis. DXA is extensively used in hospitals, diagnostic centers, and research institutes for measuring bone mineral density at key fracture sites like the spine and hip. The technology allows assessment of body composition, vertebral fracture analysis, and treatment monitoring. Strong insurance reimbursement policies in developed countries encourage adoption. DXA devices integrate with hospital IT systems, enabling automated reporting and multi-site monitoring. Clinical guidelines globally recommend DXA for at-risk populations, reinforcing its dominance. Continuous technological advancements, including low-dose imaging and AI-assisted analysis, further improve efficiency. Developed healthcare systems prioritize DXA adoption for preventive bone health management. Patient and physician trust in its reliability sustains market leadership.

Ultrasound-based bone densitometers are expected to witness the fastest CAGR of 22.3% from 2026 to 2033, driven by their portability, low cost, and non-ionizing radiation, making them ideal for primary screening and mass health checkups. Ultrasound systems are widely adopted in wellness centers, peripheral clinics, and mobile screening units. The technology is gaining traction in emerging markets due to affordability and ease of use. Advancements in quantitative ultrasound devices are improving diagnostic accuracy. Growing awareness about early osteoporosis detection and preventive care enhances adoption. Integration with cloud-based reporting systems supports remote monitoring. Portable designs enable outreach in rural areas, workplaces, and community health programs. Increasing government initiatives for bone health screening drive adoption. Continuous product innovation, including multi-site measurement capabilities and compact form factors, supports rapid market growth.

- By Application

On the basis of application, the market is segmented into Osteoporosis & Osteopenia Diagnosis, Cystic Fibrosis Diagnosis, Body Composition Measurement, Rheumatoid Arthritis Diagnosis, and Others. Osteoporosis & Osteopenia Diagnosis dominated the largest revenue share of 64.8% in 2025, due to the rising prevalence of osteoporosis globally, especially among the aging population. Hospitals, diagnostic centers, and research institutions prefer bone densitometers for early detection and fracture risk assessment. Growing awareness campaigns and preventive healthcare programs in developed countries further boost adoption. Central scan devices and DXA technology are primarily used for this application, offering accurate monitoring and treatment evaluation. Regulatory guidelines recommend routine bone density testing in at-risk populations, reinforcing segment dominance. Integration with hospital PACS systems, automated reporting, and AI-assisted analytics enhance clinical workflow. Insurance coverage and favorable reimbursement policies support consistent market growth. Increasing urbanization and lifestyle-related bone health issues drive continuous demand. Hospitals and specialized clinics prefer this application for comprehensive care, ensuring segment leadership.

Body Composition Measurement is expected to witness the fastest CAGR of 21.1% from 2026 to 2033, driven by growing fitness awareness, preventive health trends, and adoption in wellness centers, gyms, and research facilities. Portable DXA and ultrasound devices are increasingly used for assessing lean mass, fat mass, and visceral fat. Rising interest in obesity management and metabolic disorder prevention supports adoption. Integration with health apps and cloud platforms enhances remote monitoring. The segment is expanding in corporate wellness programs and community health screenings. Affordable peripheral and ultrasound devices are further driving growth. Technological innovations, such as 3D body composition imaging and real-time analytics, enhance utility. Emerging markets are rapidly adopting body composition measurement for preventive health and sports performance tracking. Telehealth and homecare use cases also contribute to growth.

- By End User

On the basis of end user, the market is segmented into Hospitals, Clinics, Diagnostic Centres, Academic & Research Institutes, and Others. Hospitals dominated the largest revenue share of 52.6% in 2025, driven by high patient volumes, advanced imaging infrastructure, and the integration of bone densitometers in preventive care and diagnostic workflows. Hospitals prefer central scan devices for osteoporosis diagnosis, fracture risk assessment, and body composition analysis. Strong reimbursement frameworks, trained radiology staff, and PACS integration reinforce adoption. Hospitals also invest in advanced DXA systems with AI-assisted reporting for precise monitoring. Clinical guidelines globally support hospital-based bone health management. Rising prevalence of osteoporosis and geriatric population drives consistent demand. Hospitals also serve as training centers for technicians and researchers, strengthening market leadership.

Diagnostic Centres are expected to witness the fastest CAGR of 23.4% from 2026 to 2033, fueled by growing patient preference for outpatient testing, convenience, and accessibility. Diagnostic centers adopt portable DXA and ultrasound devices for cost-effective screening and body composition analysis. Expansion in urban and semi-urban areas, government screening initiatives, and preventive health programs support rapid growth. Increasing investments in private diagnostic infrastructure and telehealth integration accelerate adoption. Shorter turnaround time, easy appointment scheduling, and flexible service options make diagnostic centers attractive. Rising awareness about osteoporosis and lifestyle-related health issues drives utilization. Continuous innovation in compact, high-accuracy devices enhances segment growth. Expansion in emerging markets also contributes to strong CAGR.

Europe Bone Densitometer Devices Market Regional Analysis

- The Europe bone densitometer devices market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the rising prevalence of osteoporosis, an aging population, and increasing awareness of preventive bone health diagnostics

- The adoption of advanced densitometry technologies, including dual-energy X-ray absorptiometry (DEXA) and portable bone densitometers, is being supported by technological innovations, favorable reimbursement policies, and growing healthcare infrastructure across the region

- In addition, healthcare providers are increasingly focusing on integrating AI-assisted bone analysis systems for improved accuracy and early fracture risk detection, which is driving demand across hospitals, diagnostic centers, and specialty clinics. The region is witnessing notable growth across public and private healthcare facilities, with densitometer devices being incorporated into routine preventive checkups, geriatric care, and specialized osteoporosis management programs

U.K. Bone Densitometer Devices Market Insight

The U.K. bone densitometer devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by advanced healthcare infrastructure, high awareness of osteoporosis screening programs, and strong reimbursement frameworks that encourage early detection and monitoring of bone health. The presence of specialized diagnostic centers adopting state-of-the-art densitometry technologies, coupled with widespread preventive care initiatives, supports consistent device adoption. In addition, growing patient preference for non-invasive and accurate bone health assessments is further propelling the market. Initiatives such as government-supported osteoporosis screening campaigns in NHS hospitals and private clinics provide greater accessibility to densitometry services, stimulating demand in both urban and semi-urban regions. The U.K. dominated the Bone Densitometer Devices market with the largest revenue share of 27.8% in 2025, reflecting a combination of clinical expertise, healthcare investment, and patient awareness.

Germany Bone Densitometer Devices Market Insight

The Germany bone densitometer devices market is expected to expand at a considerable CAGR during the forecast period, fueled by rising geriatric populations, increasing incidence of bone-related disorders, and growing adoption of portable and AI-assisted bone densitometers in clinical practice. Germany’s well-developed healthcare infrastructure, emphasis on preventive diagnostics, and investments in AI-enabled imaging solutions promote the integration of advanced bone densitometry systems in hospitals and specialty clinics. Moreover, expanding healthcare expenditure and the country’s focus on digital health technologies are facilitating the deployment of densitometers in outpatient and community care centers. Germany is expected to be the fastest growing country in the Bone Densitometer Devices market during the forecast period, driven by a combination of technological adoption, rising demand for preventive care, and supportive policy frameworks for early detection and management of osteoporosis.

Europe Bone Densitometer Devices Market Share

The Bone Densitometer Devices industry is primarily led by well-established companies, including:

- Hologic, Inc. (U.S.)

- GE Healthcare Technologies Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Medtronic plc (Ireland)

- Canon Medical Systems Corporation (Japan)

- Furuno Electric Co., Ltd. (Japan)

- OsteoSys Co., Ltd. (South Korea)

- Norland at Swissray (U.S.)

- DMS Group (France)

- BeamMed Ltd. (Israel)

- Trivitron Healthcare Pvt. Ltd. (India)

- Alara, Inc. (U.S.)

- Carestream Health, Inc. (U.S.)

- Bio-Imaging Technologies (U.S.)

- OsteoDetector GmbH (Germany)

Latest Developments in Europe Bone Densitometer Devices Market

- In February 2023, Fujifilm introduced its FDX Visionary‑DR 2D‑Fan Beam bone densitometer, a high‑resolution system designed to deliver rapid and detailed bone mineral density assessments for diagnosing osteoporosis, morphometry, and whole‑body analysis. This launch enhanced capabilities for both orthopaedic diagnostics and patient screening across global markets

- In August 2024, OSTEOSYS Co., Ltd. announced that it had obtained certification under the European Union Medical Device Regulation (EU MDR) for its entire range of DXA bone densitometry systems, including models such as PRIMUS, EX CELLUS, and DEXXUM series. The MDR certification confirmed improved safety and compliance for distribution across Europe

- In September 2024, GE Healthcare launched the Lunar iDXA bone densitometer, featuring advanced imaging technology and enhanced diagnostic accuracy for evaluating bone mineral density, helping clinicians more precisely assess osteoporosis risk and fracture potential

- In January 2025, Xuzhou Pinyuan Electronic Technology released its Dual Screen Dual Probe Ultrasonic Bone Densitometer, a next‑generation device aimed at improving both precision and ease of use in bone density assessment through innovative dual‑probe ultrasound technology

- In June 2025, Echolight Medical LLC began commercial sales of its novel radiofrequency echographic multi spectrometry (REMS) bone densitometer, a radiation‑free, portable system that provides detailed profiling of bone health and offers a safer alternative to traditional DXA‑based devices, expanding options for outpatient and mobile diagnostics

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.