Europe Cardiac Computed Tomography Cct Market

Market Size in USD Million

USD

692.10 Million

USD

1,111.45 Million

2025

2033

USD

692.10 Million

USD

1,111.45 Million

2025

2033

| 2026 - 2033 | |

| USD 692.10 Million | |

| USD 1,111.45 Million | |

| % | |

|

Europe Cardiac Computed Tomography (CCT) Market Size

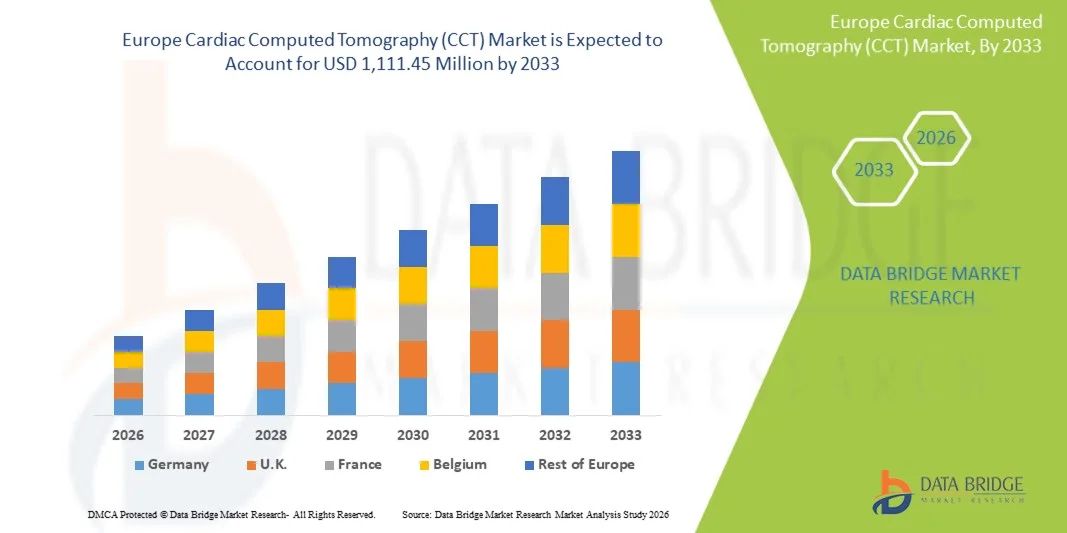

- The Europe Cardiac Computed Tomography (CCT) market size was valued at USD 692.10 million in 2025 and is expected to reach USD 1,111.45 million by 2033, at a CAGR of 6.10% during the forecast period

- The market growth is largely fueled by the rising prevalence of cardiovascular diseases, increasing adoption of non‑invasive imaging technologies such as coronary CT angiography, and continuous technological advancements in CT systems that improve image quality, diagnostic accuracy, and scanning speed

- Furthermore, growing healthcare infrastructure investments across Europe, heightened demand for early diagnosis of heart conditions, and the integration of advanced imaging workflows in clinical settings are driving strong uptake of cardiac CT solutions, positioning them as essential tools in modern cardiology diagnostics and significantly boosting the market’s expansion

Europe Cardiac Computed Tomography (CCT) Market Analysis

- Cardiac computed tomography (CCT), providing non-invasive imaging for coronary arteries and cardiac structures, is increasingly essential in modern cardiology diagnostics across both clinical and hospital settings due to its high accuracy, rapid scanning capabilities, and integration with advanced imaging workflows

- The escalating demand for cardiac CT is primarily fueled by the rising prevalence of cardiovascular diseases, growing adoption of non-invasive diagnostic technologies, and a preference for early detection of heart conditions to improve patient outcomes

- Germany dominated the Europe cardiac CT market with the largest revenue share of 28.5% in 2025, driven by well-established healthcare infrastructure, high adoption of advanced imaging technologies, and a strong presence of key industry players, with significant growth in CT installations particularly in tertiary care hospitals and specialized cardiac centers, supported by innovations in AI-assisted imaging and high-resolution scanners

- Poland is expected to be the fastest-growing country in the Europe cardiac CT market during the forecast period due to increasing investments in healthcare infrastructure, rising awareness of cardiovascular health, and expanding access to advanced imaging technologies

- Coronary CT angiography segment dominated the Europe cardiac CT market with a market share of 45.7% in 2025, driven by its established clinical utility for non-invasive assessment of coronary artery disease and growing adoption in routine cardiac evaluation protocols

Report Scope and Europe Cardiac Computed Tomography (CCT) Market Segmentation

|

Attributes |

Europe Cardiac Computed Tomography (CCT) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Cardiac Computed Tomography (CCT) Market Trends

“Advancements in AI-Assisted Imaging and Workflow Integration”

- A significant and accelerating trend in the Europe CCT market is the integration of artificial intelligence (AI) in imaging systems and workflow platforms, enhancing diagnostic accuracy, reducing scan times, and enabling automated post-processing for cardiologists

- For instance, Siemens Healthineers’ AI-Rad Companion Cardiovascular assists in automated segmentation and plaque quantification, helping clinicians streamline cardiac CT analysis and improve patient management decisions

- AI integration in CCT enables features such as predictive risk assessment, automated lesion detection, and enhanced image reconstruction, improving the overall clinical utility of scans. For instance, Canon Medical’s Advanced Intelligent Clear-IQ Engine (AiCE) uses AI to reduce noise while improving image clarity, assisting in precise coronary evaluation

- The seamless integration of CCT systems with hospital PACS and electronic health records allows cardiologists to efficiently combine imaging data with patient history, lab results, and prior scans, creating a centralized and automated diagnostic workflow

- This trend toward more intelligent, precise, and interconnected imaging solutions is fundamentally reshaping clinical expectations for cardiac diagnostics. Consequently, companies such as GE Healthcare are developing AI-enabled cardiac CT platforms that support automated coronary artery analysis and predictive modeling for patient risk stratification

- The demand for cardiac CT systems with AI-assisted imaging and workflow integration is growing rapidly across hospitals and specialized cardiac centers, as clinicians increasingly prioritize accurate, efficient, and data-driven cardiac evaluation

- Hybrid imaging solutions, combining CCT with other modalities such as PET or SPECT, are gaining traction, offering comprehensive cardiovascular assessment in a single workflow and further driving clinical adoption

Europe Cardiac Computed Tomography (CCT) Market Dynamics

Driver

“Rising Cardiovascular Disease Burden and Adoption of Non-Invasive Diagnostics”

- The increasing prevalence of cardiovascular diseases across Europe, coupled with the growing adoption of non-invasive diagnostic modalities, is a significant driver for the heightened demand for CCT systems

- For instance, in March 2025, Philips announced the expansion of its cardiac CT portfolio with AI-assisted solutions for coronary artery disease evaluation, aiming to improve early diagnosis and workflow efficiency in European hospitals

- As clinicians seek safer, faster, and more accurate alternatives to invasive procedures, CCT offers advanced capabilities such as coronary artery visualization, calcium scoring, and functional assessment, providing a compelling advantage over traditional diagnostic methods

- Furthermore, the growing adoption of advanced imaging platforms in cardiology and the need for integrated patient management systems are making cardiac CT an essential component of modern cardiac care, enabling streamlined workflow across departments

- The ability to perform rapid, high-resolution scans with minimal patient preparation, combined with features such as automated reporting and AI-assisted interpretation, is propelling the adoption of cardiac CT in both public and private healthcare facilities

- Government initiatives promoting early detection and preventive cardiology programs are encouraging hospitals to invest in advanced imaging technologies such as CCT, particularly for populations at high risk of cardiovascular diseases

- Collaborations between imaging device manufacturers and healthcare providers for clinical research and pilot studies are driving adoption, as hospitals can demonstrate the clinical and economic benefits of CCT before large-scale implementation

Restraint/Challenge

“High Equipment Cost and Regulatory Compliance Hurdles”

- The high capital cost of cardiac CT systems, along with ongoing maintenance and software update requirements, poses a significant challenge to broader market penetration, particularly in smaller hospitals or budget-constrained healthcare facilities

- For instance, hospitals in Eastern European countries may hesitate to invest in premium CT platforms despite their clinical benefits, due to budget limitations and competing priorities for healthcare spending

- Addressing these cost barriers through financing models, modular system upgrades, and scalable AI solutions is crucial for expanding adoption. Companies such as Canon Medical emphasize flexible purchasing options and software-based upgrades to make advanced cardiac CT systems more accessible

- In addition, stringent regulatory requirements for medical devices and compliance with EU MDR regulations create further hurdles, as manufacturers must ensure system safety, data protection, and clinical validation before deployment

- Overcoming these challenges through cost-effective solutions, regulatory support, and clinician education on the clinical value of CCT will be vital for sustained market growth across Europe

- Limited availability of trained radiologists and technicians for operating advanced cardiac CT systems in certain countries may delay adoption and integration of the technology in routine clinical workflows

- Data privacy concerns related to patient imaging data and the integration of AI-based analytics pose additional challenges, requiring robust cybersecurity protocols and compliance with GDPR regulations

Europe Cardiac Computed Tomography (CCT) Market Scope

The market is segmented on the basis of offerings, product type, application, end user, and distribution channel.

- By Offerings

On the basis of offerings, the Europe CCT market is segmented into system, service, and software. The system segment dominated the market with the largest revenue share in 2025, as hospitals and specialty cardiac centers prioritize investments in high-performance CT scanners for coronary and cardiac imaging. Systems offer comprehensive diagnostic capabilities, enabling coronary CT angiography, calcium scoring, and functional assessment in a single scan. Their integration with advanced software and AI-assisted tools enhances workflow efficiency, reduces scan time, and improves diagnostic accuracy. Furthermore, hospitals value turnkey systems for their reliability and long-term service support agreements, making system sales the backbone of CCT market revenue.

The software segment is expected to witness the fastest growth during the forecast period, fueled by increasing demand for AI-assisted image processing, cloud-based analysis, and post-processing tools that optimize diagnostic workflows. Software solutions enhance interpretation speed, automate plaque quantification, and integrate seamlessly with PACS and electronic health records. This enables cardiologists to access, analyze, and report imaging data more efficiently, making software adoption particularly attractive for smaller imaging centers and specialty clinics aiming to upgrade existing hardware.

- By Product Type

On the basis of product type, the market is segmented into single source CT, dual source cardiac CT, and spectral CT. The dual source cardiac CT segment dominated the market in 2025 due to its ability to produce high-resolution images at faster speeds, enabling accurate coronary artery assessment even in patients with high heart rates. Dual source CTs reduce motion artifacts and improve diagnostic confidence, making them a preferred choice in advanced hospitals and tertiary care centers. Their superior temporal resolution supports a wide range of cardiac applications, including calcium scoring and coronary CT angiography, establishing them as the industry standard for high-end cardiac imaging in Europe.

The spectral CT segment is expected to witness the fastest growth during the forecast period, driven by rising clinical adoption for functional cardiac imaging and plaque characterization. Spectral CT enables material differentiation, improved tissue contrast, and enhanced visualization of calcified plaques. Growing awareness among cardiologists of its diagnostic advantages, coupled with ongoing R&D and software integration, supports rapid uptake across specialty centers and high-volume hospitals.

- By Application

On the basis of application, the market is segmented into calcium scoring, coronary CT angiography (CCTA), device implantation, pulmonary vein isolation, and left atrial appendage occlusion. The coronary CT angiography (CCTA) segment dominated with the largest market revenue share of 45.7% in 2025, as it provides non-invasive, accurate assessment of coronary artery disease. Clinicians prefer CCTA for its ability to detect stenosis, assess plaque burden, and guide treatment planning without invasive catheterization. The segment benefits from strong guideline recommendations in Europe and increasing integration of AI tools for automated analysis, enhancing workflow and reproducibility.

The pulmonary vein isolation segment is expected to witness the fastest growth during the forecast period, fueled by the rising prevalence of atrial fibrillation and increasing adoption of cardiac CT for pre-procedural planning. Imaging for pulmonary vein isolation enables precise anatomical mapping, risk stratification, and improved outcomes for ablation procedures. Growing awareness among electrophysiologists and integration with navigation systems contribute to rapid market expansion in this application.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty centers, diagnostic & imaging centers, and others. The hospitals segment dominated with the largest market revenue share in 2025, as hospitals possess the infrastructure, budget, and patient volume to justify investment in advanced cardiac CT systems. Hospitals leverage CCT for a wide range of diagnostic and interventional planning applications, including coronary evaluation, device implantation, and pre-procedural assessment for atrial interventions. They also benefit from in-house radiology and cardiology expertise to maximize system utilization and ensure patient throughput.

The diagnostic & imaging centers segment is expected to witness the fastest growth during the forecast period, driven by the increasing number of outpatient imaging facilities offering advanced cardiac diagnostics. These centers adopt portable or smaller footprint CT systems and software solutions to provide accessible, cost-effective cardiac evaluation. The growing awareness among patients and collaborations with cardiologists to provide specialized services fuel this rapid adoption. Rising adoption of preventive cardiology programs and minimally invasive procedures also supports the rapid expansion of this segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and third-party distributor. The direct tender segment dominated the Europe CCT market in 2025, as hospitals and large specialty centers prefer procuring systems directly from manufacturers to secure service contracts, training, and long-term technical support. Direct tender allows healthcare providers to negotiate customized solutions, warranty extensions, and software bundles tailored to specific clinical needs. Manufacturers also benefit from direct engagement to strengthen client relationships and ensure adherence to regulatory standards.

The third-party distributor segment is expected to witness the fastest growth during the forecast period, driven by increasing adoption of CT systems and software by smaller imaging centers and specialty clinics. Distributors provide flexible financing, installation, and maintenance support, enabling smaller institutions to acquire advanced imaging solutions without upfront capital expenditure. The ease of access and post-sales support offered by distributors makes this channel particularly attractive in emerging European markets.

Europe Cardiac Computed Tomography (CCT) Market Regional Analysis

- Germany dominated the Europe cardiac CT market with the largest revenue share of 28.5% in 2025, driven by well-established healthcare infrastructure, high adoption of advanced imaging technologies, and a strong presence of key industry players

- Clinicians and hospitals in the country prioritize non-invasive diagnostic solutions such as coronary CT angiography and calcium scoring, valuing the accuracy, speed, and efficiency of cardiac CT in detecting and managing cardiovascular diseases

- This widespread adoption is further supported by government initiatives promoting early detection of heart conditions, high healthcare expenditure, and collaborations between hospitals and imaging device companies to integrate AI-assisted cardiac CT solutions

The Germany Cardiac Computed Tomography (CCT) Market Insight

The Germany CCT market captured the largest revenue share in Europe in 2025, driven by advanced healthcare infrastructure, high adoption of cutting-edge imaging technologies, and strong presence of key CT system manufacturers. Hospitals and specialty cardiac centers in Germany prioritize high-performance CT systems for coronary CT angiography, calcium scoring, and functional cardiac assessment. AI-assisted imaging and seamless integration with electronic health records further enhance the diagnostic utility of these systems. The country’s emphasis on innovation, preventive cardiology, and research collaborations supports rapid adoption. Increasing patient awareness and government-backed cardiovascular screening programs are also contributing to the market’s expansion.

France Cardiac Computed Tomography (CCT) Market Insight

The France CCT market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing prevalence of heart disease and the rising demand for non-invasive cardiac diagnostics. Hospitals and specialty centers are investing in advanced CT systems with AI-based post-processing and improved imaging accuracy. Government healthcare initiatives and reimbursement policies encouraging early diagnosis of cardiovascular conditions further stimulate market growth. In addition, the integration of cardiac CT with hospital information systems and PACS enhances workflow efficiency and adoption. Both new hospitals and existing centers undergoing upgrades are contributing to significant market expansion.

U.K. Cardiac Computed Tomography (CCT) Market Insight

The U.K. CCT market is expected to expand at a considerable CAGR, fueled by rising awareness of cardiovascular health, increasing hospital investments in advanced imaging systems, and the growing adoption of AI-assisted coronary CT angiography. The country’s robust healthcare infrastructure, combined with a focus on preventive cardiology, encourages widespread use of non-invasive cardiac diagnostics. Integration of CT systems with hospital networks and electronic health records facilitates efficient diagnosis and reporting. The U.K.’s hospitals and specialty centers continue to drive adoption in both new installations and technology upgrades for existing imaging systems.

Poland Cardiac Computed Tomography (CCT) Market Insight

The Poland CCT market is poised to grow at the fastest CAGR during the forecast period, driven by expanding healthcare infrastructure, government initiatives for preventive cardiac care, and rising patient awareness regarding heart disease. Specialty cardiac centers and diagnostic facilities are increasingly adopting cost-effective, high-resolution CT systems to meet growing demand. Investments in AI-enabled imaging solutions and remote analysis capabilities further accelerate adoption. The market growth is supported by expanding access to modern cardiac diagnostic technologies in both urban and semi-urban regions.

Europe Cardiac Computed Tomography (CCT) Market Share

The Europe Cardiac Computed Tomography (CCT) industry is primarily led by well-established companies, including:

- Siemens Healthineers AG (Germany)

- GE HealthCare (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Koninklijke Philips N.V. (Netherlands)

- Neusoft Medical Systems Co., Ltd. (China)

- United Imaging Healthcare (China)

- Shimadzu Corporation (Japan)

- Samsung Medison Co., Ltd. (South Korea)

- FUJIFILM Healthcare Corporation (Japan)

- Hitachi High-Tech Corporation (Japan)

- Mindray Medical International Limited (China)

- Shenzhen Anke High-Tech Co., Ltd. (China)

- Carestream Health (U.S.)

- Analogic Corporation (U.S.)

- NeuroLogica Corp. (U.S.)

- Agfa HealthCare (Belgium)

- Planmed Oy (Finland)

- Cybermed Inc. (South Korea)

- Unison Healthcare Group (Taiwan)

- Shanghai United Imaging Healthcare Co., Ltd. (China)

What are the Recent Developments in Europe Cardiac Computed Tomography (CCT) Market?

- In December 2025, Siemens Healthineers announced Syngo.CT Coronary Cockpit, a new software solution for cardiac CT at RSNA 2025. This AI‑driven software enhances automated plaque analysis, quantification, and visualization to support coronary artery disease management. Compatible with dual‑source and photon‑counting CT scanners, it helps clinicians use cardiac CT data for personalized therapeutic planning and reduces unnecessary invasive procedures a significant capability for European cardiac imaging workflows

- In December 2024, Siemens broadened its photon‑counting CT portfolio with new dual‑source and single‑source systems as part of the Naeotom Alpha class, showcased at RSNA 2024. These photon‑counting CT scanners with highly detailed spectral imaging and automation features are designed to enhance cardiovascular imaging. The portfolio expansion supports high resolution cardiac CT exams and makes advanced imaging more widely available across European tertiary care and outpatient settings

- In March 2024, Royal Philips launched the new AI‑enabled CT 5300 system aimed at cardiology imaging at the European Congress of Radiology (ECR 2024). The CT 5300 features advanced AI image reconstruction and automated workflow enhancements designed to improve coronary CT angiography (CCTA), streamline radiology department efficiency, and lower radiation doses. This scanner is intended to support both diagnosis and interventional planning, making advanced cardiac CT more accessible in European hospitals

- In December 2023, the COMBINE‑CT public‑private partnership received a €6.5 million grant to improve coronary CT diagnostics and care pathways across Europe. Coordinated by Philips with major European clinical partners, this initiative aims to develop vendor‑agnostic CCTA workflows that connect diagnosis, stratification, treatment planning, and follow‑up in coronary artery disease care. The multi‑center clinical trials will generate evidence to expand cardiac CT’s clinical utility across European healthcare systems

- In December 2023, cardiac CT imaging innovations were prominently featured at RSNA 2023, with multiple vendors introducing new systems targeting cardiovascular applications. Major CT manufacturers showcased four new CT scanners with enhanced capabilities for coronary CT angiography (CCTA) at this leading radiology conference, reflecting strong momentum behind cardiac CT adoption and technology innovation in Europe

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.