Europe Cell Counting Devices Market

Market Size in USD Billion

USD

3.72 Billion

USD

5.88 Billion

2024

2032

USD

3.72 Billion

USD

5.88 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.72 Billion | |

| USD 5.88 Billion | |

| % | |

|

Europe Cell Counting Devices Market Size

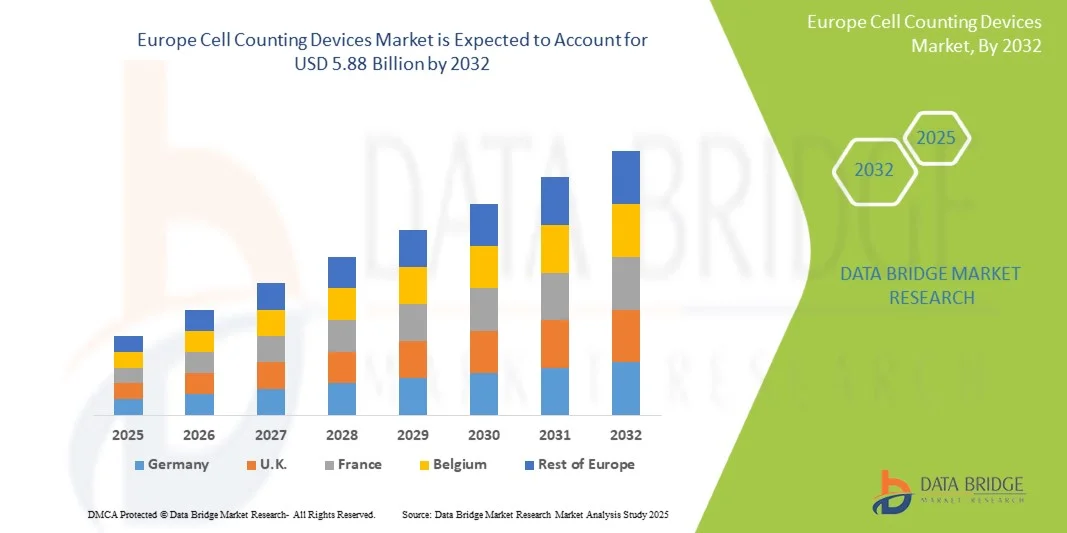

- The Europe Cell Counting Devices Market size was valued at USD 3.72 billion in 2024 and is expected to reach USD 5.88 billion by 2032, at a CAGR of 5.89% during the forecast period

- The market growth is largely fueled by the growing adoption and technological progress in automated laboratory technologies and digital cell analysis platforms, leading to increased efficiency in both research and clinical applications

- Furthermore, rising demand for accurate, user-friendly, and integrated solutions in life sciences and healthcare is establishing cell counting devices as a critical tool of choice. These converging factors are accelerating the uptake of cell counting devices solutions, thereby significantly boosting the industry's growth

Europe Cell Counting Devices Market Analysis

- Cell counting devices, which are essential tools for measuring cell concentration and viability in research, clinical diagnostics, and biopharmaceutical production, are increasingly being adopted across Europe due to the rising demand for precision medicine, cancer research, and regenerative therapies. Their ability to deliver high accuracy, automation, and time efficiency makes them indispensable in both academic and industrial laboratories

- The accelerating demand for cell counting devices is primarily fueled by the increasing prevalence of chronic diseases, advancements in stem cell and immunotherapy research, and growing investments in biopharmaceutical R&D across the region

- Germany dominated the Europe Cell Counting Devices Market in Europe with the largest revenue share of 34.6% in 2024, supported by its strong network of research universities, robust biopharmaceutical manufacturing industry, and widespread adoption of advanced laboratory automation technologies. The country’s emphasis on innovation and high healthcare expenditure further strengthen its leadership in the market

- France is expected to be the fastest-growing country in the European Europe Cell Counting Devices Market during the forecast period, driven by the expansion of cancer research programs, increasing government support for life sciences, and rapid adoption of automated and image-based cell counters in clinical laboratories and biopharmaceutical companies

- The consumables segment dominated the Europe Cell Counting Devices Market with the largest revenue share of 58.7% in 2024, primarily driven by the recurring demand for reagents, kits, and disposable accessories essential for consistent and reliable cell counting results

Report Scope and Europe Cell Counting Devices Market Segmentation

|

Attributes |

Europe Cell Counting Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Cell Counting Devices Market Trends

Enhanced Convenience Through Advanced Cell Analysis and Automation

- A significant and accelerating trend in the Europe Cell Counting Devices Market is the integration of advanced automation and intelligent analytical tools, which are improving precision, reliability, and user convenience in laboratories and clinical settings

- For instance, leading manufacturers have introduced automated benchtop instruments that enable rapid and consistent cell counting, minimizing manual intervention and ensuring reproducible results across large sample volumes. Such innovations are expected to drive the market forward during the forecast period

- Automation in cell counting devices enhances workflows by reducing operator dependency, providing error-free results, and significantly increasing throughput. This allows laboratories to efficiently manage growing test volumes without compromising accuracy

- Furthermore, the availability of compact and portable instruments is creating opportunities for decentralized testing, including point-of-care and field-based applications, thereby widening the scope of usage beyond traditional laboratories

- Advanced software integration now allows for real-time monitoring, data storage, and cloud connectivity, enabling seamless transfer of results and better decision-making in both research and clinical diagnostics

- The demand for devices offering high sensitivity, faster turnaround times, and compatibility with diverse cell types is rapidly increasing across pharmaceutical, biotechnology, and healthcare institutions

- The seamless combination of automation, digital connectivity, and high analytical performance is reshaping expectations in the market, as end-users increasingly look for solutions that deliver speed, precision, and ease of use

- Consequently, companies are focusing on developing next-generation cell counting technologies that support broader applications in research, drug development, and personalized medicine, further fueling growth across Europe

Europe Cell Counting Devices Market Dynamics

Driver

Growing Need Due to Rising Demand for Precision Medicine and Biopharmaceutical Research

- The increasing global focus on precision medicine, regenerative therapies, and advanced cancer research has significantly accelerated the adoption of cell counting devices in both clinical and research settings. Accurate measurement of cell concentration and viability is a critical step in drug development, stem cell research, and immunotherapy, driving sustained demand for these technologies

- For instance, in May 2023, Agilent Technologies launched its improved image-based cell analysis system, designed to deliver enhanced throughput and accuracy for pharmaceutical and biotechnology laboratories. Such advancements from leading companies are expected to drive the Cell Counting Devices industry growth during the forecast period

- As researchers and clinicians increasingly prioritize efficiency, accuracy, and reproducibility, cell counting devices provide superior performance compared to manual techniques. The ability to automate cell counting processes, generate reliable results, and reduce variability is fueling rapid adoption across hospitals, clinical laboratories, and biopharmaceutical companies

- Furthermore, the growing prevalence of chronic diseases, including cancer and cardiovascular disorders, is boosting demand for advanced diagnostic and therapeutic solutions. Cell counting devices are integral in supporting these workflows, ensuring consistent quality control and regulatory compliance in both research and manufacturing environments

- The rise of single-cell analysis and high-throughput screening platforms, combined with expanding investments in biotechnology infrastructure, is further propelling the Europe Cell Counting Devices Market. In addition, the trend toward miniaturized, user-friendly, and portable solutions is broadening accessibility for small-scale laboratories and point-of-care applications

Restraint/Challenge

High Cost of Advanced Technologies and Limited Accessibility in Developing Regions

- Despite their growing importance, the high cost of advanced cell counting devices, particularly image-based and automated counters, remains a significant challenge for widespread adoption. Many small and mid-sized laboratories in developing countries face budgetary constraints, limiting their ability to invest in high-end systems

- For instance, premium image-based counters with integrated AI analytics and multi-parameter detection capabilities often come with substantial upfront costs, making them less accessible for resource-constrained healthcare systems and academic institutions

- Addressing these concerns through cost optimization, increased affordability, and flexible financing models is critical to ensuring broader market penetration. Companies such as Thermo Fisher Scientific and Bio-Rad are increasingly focused on offering scalable solutions to bridge the affordability gap

- Another challenge lies in the technical expertise required to operate sophisticated devices. While automated systems reduce manual errors, they may still require specialized training and maintenance, which can be a barrier in regions with limited skilled personnel

- Overcoming these challenges through technological simplification, cost reduction, and targeted training programs will be essential for sustained global growth of the Europe Cell Counting Devices Market

Europe Cell Counting Devices Market Scope

The market is segmented on the basis of product type, application, and end user.

• By Product Type

On the basis of product type, the Europe Cell Counting Devices Market is segmented into consumables and instruments. The consumables segment dominated the market with the largest revenue share of 58.7% in 2024, primarily driven by the recurring demand for reagents, kits, and disposable accessories essential for consistent and reliable cell counting results. Their single-use nature minimizes contamination risks, aligns with stringent laboratory protocols, and ensures high reproducibility, making them indispensable in both clinical and research workflows. Ongoing innovation in assay reagents and increased adoption in diagnostics further strengthen this segment’s market leadership.

The instruments segment is projected to witness the fastest growth, registering a CAGR of 12.9% from 2025 to 2032. The growth is fueled by increasing demand for automation, high-throughput analysis, and AI-driven imaging technologies in laboratories. Instruments such as flow cytometers and automated image-based cell counters are enabling faster, more accurate results while reducing manual intervention. In addition, digital integration and the adoption of advanced counting platforms across biotechnology and clinical laboratories in Europe are accelerating the uptake of instruments.

• By Application

On the basis of application, the Europe Cell Counting Devices Market is segmented into research applications, clinical and diagnostic applications, and industrial applications. The research applications segment dominated with a revenue share of 46.5% in 2024, owing to the robust biotechnology and academic research infrastructure across Europe. Strong funding support from the EU for R&D in cell biology, cancer research, and regenerative medicine has boosted adoption of advanced cell counting systems. The demand for reproducibility and accuracy in preclinical and drug discovery workflows further solidifies this segment’s dominance.

The clinical and diagnostic applications segment is expected to register the fastest growth, with a CAGR of 13.6% from 2025 to 2032. Rising incidence of chronic and infectious diseases, combined with the demand for precision medicine, is fueling adoption of advanced cell counting technologies in pathology and diagnostic labs. Automation in clinical laboratories and integration of digital diagnostic solutions are improving efficiency, while widespread use in hematology and oncology diagnostics continues to expand this segment rapidly across the European healthcare landscape.

• By End User

On the basis of end user, the Europe Cell Counting Devices Market is segmented into research institutes, pharmaceutical and biotechnology companies, diagnostic centers, hospitals, clinical laboratories, and others. The research institutes segment accounted for the largest revenue share of 39.8% in 2024, supported by extensive academic and government-funded projects across the life sciences. These institutes heavily rely on accurate and efficient cell analysis for areas such as immunology, drug discovery, and stem cell research. Collaborations with industry and the growing number of biomedical research centers across Europe further strengthen this segment’s leading position.

The pharmaceutical and biotechnology companies segment is projected to grow at the fastest rate, registering a CAGR of 14.1% from 2025 to 2032. The surge in demand for biopharmaceuticals, cell-based therapies, and regenerative medicine is creating strong reliance on advanced cell counting solutions for quality control and R&D. Increasing clinical trials, strategic collaborations between biotech startups and pharma giants, and regulatory support for advanced therapies are further driving adoption. This segment’s rapid growth reflects the expanding role of cell counting devices in drug development and production pipelines.

Europe Cell Counting Devices Market Regional Analysis

- The Europe Cell Counting Devices Market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the rising prevalence of chronic diseases, expanding biotechnology and pharmaceutical research, and the growing demand for automated laboratory solutions

- Germany dominated the Europe Cell Counting Devices Market in Europe with the largest revenue share of 34.6% in 2024, supported by its strong network of research universities, robust biopharmaceutical manufacturing industry, and widespread adoption of advanced laboratory automation technologies. The country’s emphasis on innovation and high healthcare expenditure further strengthen its leadership in the market

- France is expected to be the fastest-growing country in the European Europe Cell Counting Devices Market during the forecast period, driven by the expansion of cancer research programs, increasing government support for life sciences, and rapid adoption of automated and image-based cell counters in clinical laboratories and biopharmaceutical companies

Germany Europe Cell Counting Devices Market Insight

The Germany Europe Cell Counting Devices Market is expected to expand at a considerable CAGR during the forecast period, supported by its strong network of research universities, robust biopharmaceutical manufacturing industry, and widespread adoption of advanced laboratory automation technologies. Germany dominated the Europe Cell Counting Devices Market in Europe with the largest revenue share of 34.6% in 2024, underscoring its leadership position. The country’s emphasis on innovation, high healthcare expenditure, and strong collaborations between academia and industry further enhance its role as a hub for advanced biomedical research and diagnostics.

France Europe Cell Counting Devices Market Insight

The France Europe Cell Counting Devices Market is expected to be the fastest-growing country in the European Europe Cell Counting Devices Market during the forecast period. Growth is primarily driven by the expansion of cancer research programs, increasing government support for life sciences, and the rapid adoption of automated and image-based cell counters in both clinical laboratories and biopharmaceutical companies. The country’s investments in precision medicine and partnerships between research institutions and healthcare providers are accelerating the deployment of cutting-edge cell counting solutions.

Europe Cell Counting Devices Market Share

The cell counting devices industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Danaher Corporation (U.S.)

- Sysmex Corporation (Japan)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Olympus Corporation (Japan)

- ChemoMetec (Denmark)

- Tip Biosystems (U.K.)

- Tecan Trading AG (Switzerland)

- BD (U.S.)

- Abbott (U.S.)

- DeNovix (U.S.)

Latest Developments in Europe Cell Counting Devices Market

- In September 2022, PerkinElmer, through its subsidiary Nexcelom Bioscience, launched the Cellaca PLX system. This instrument combines image-based cell counting, viability analysis, and multiple fluorescence detection into a single platform, offering researchers a more integrated solution. The Cellaca PLX is particularly relevant for cell and gene therapy research, an area where Europe has seen rapid expansion. The product was developed to meet increasing needs for reproducibility and high-throughput analysis in advanced therapeutic development and clinical manufacturing

- In February 2023, Agilent Technologies introduced enhanced automated solutions for cell analysis workflows.The company announced updates designed to improve throughput and efficiency in immuno-oncology, virology, and vaccine development research. These advancements in automation are directly applicable to laboratories across Europe, where demand for reliable and high-throughput cell counting and analysis platforms continues to rise. The move reinforced Agilent’s strategy to strengthen its position in cell analysis markets globally, including Europe, by supporting high-content workflows for both biopharma and academic users

- In March 2024, Revvity expanded commercialization of its Cellaca MX high-throughput cell counter. The company provided new technical documentation, workflow materials, and support infrastructure for the Cellaca MX system, emphasizing its use in multiparameter analysis. This system enables laboratories to process multiple samples quickly with consistent accuracy, a feature highly valued in European clinical and biopharmaceutical research facilities. The wider availability of the instrument underscored Revvity’s commitment to strengthening its presence in Europe’s fast-growing life sciences market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.