Europe Corneal Transplant Market

Market Size in USD Million

USD

106.27 Million

USD

165.58 Million

2024

2032

USD

106.27 Million

USD

165.58 Million

2024

2032

| 2025 - 2032 | |

| USD 106.27 Million | |

| USD 165.58 Million | |

| % | |

|

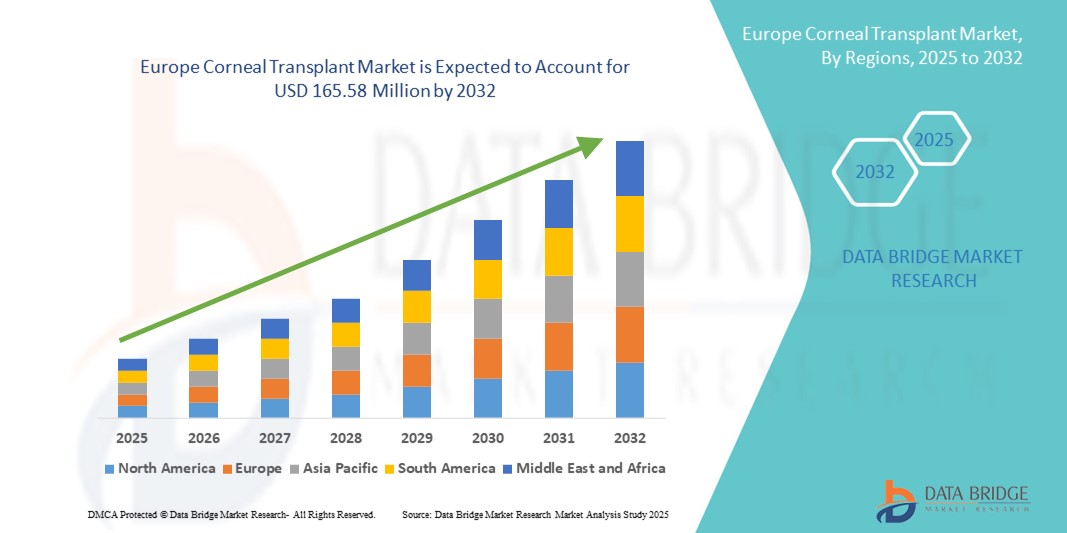

Europe Corneal Transplant Market Size

- The Europe corneal transplant market size was valued at USD 106.27 million in 2024 and is expected to reach USD 165.58 million by 2032, at a CAGR of 5.70% during the forecast period

- The market growth is primarily driven by the rising prevalence of corneal diseases such as keratoconus, Fuchs’ dystrophy, and infectious keratitis, coupled with increasing awareness and availability of advanced transplant techniques such as DMEK and DSAEK across the region

- In addition, growing investments in eye care infrastructure, expanding donor tissue availability, and favorable reimbursement policies are enhancing access to corneal transplant procedures. These factors collectively contribute to a positive growth trajectory for the Europe corneal transplant market over the coming years

Europe Corneal Transplant Market Analysis

- Corneal transplants, involving the replacement of damaged or diseased corneal tissue with healthy donor tissue, are essential procedures for restoring vision and improving quality of life, particularly in cases of corneal scarring, thinning, or dystrophies across both public and private healthcare settings

- The increasing demand for corneal transplants in Europe is primarily driven by the rising incidence of age-related and hereditary corneal disorders, advancements in surgical techniques such as lamellar keratoplasty, and improved post-operative outcomes

- Germany dominated the Europe corneal transplant market with the largest revenue share of 28.5% in 2024, supported by its advanced healthcare infrastructure, strong donor tissue availability through organized eye banks, and high volume of ophthalmic procedures performed annually

- Poland is expected to be the fastest growing country in the corneal transplant market during the forecast period due to ongoing improvements in healthcare delivery, rising awareness about corneal blindness, and expanding access to transplant services

- Penetrating keratoplasty (PK) segment dominated the corneal transplant market with a market share of 46.6% in 2024, attributed to its broad application in treating full-thickness corneal damage and continued preference among surgeons for complex corneal conditions

Report Scope and Europe Corneal Transplant Market Segmentation

|

Attributes |

Europe Corneal Transplant Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Corneal Transplant Market Trends

“Technological Advancements in Minimally Invasive Corneal Transplant Procedures”

- A major and accelerating trend in the Europe corneal transplant market is the shift toward advanced minimally invasive techniques such as Descemet Membrane Endothelial Keratoplasty (DMEK) and Descemet Stripping Automated Endothelial Keratoplasty (DSAEK), which offer faster recovery times, reduced complications, and improved visual outcomes compared to traditional methods

- For instance, the University Eye Hospital in Tübingen, Germany, has adopted DMEK as the preferred technique for endothelial disorders, reporting superior patient satisfaction and lower graft rejection rates. Similarly, Moorfields Eye Hospital in the U.K. is increasingly using DSAEK for specific patient groups due to its predictable outcomes and shorter learning curve for surgeons

- The growing availability of precut donor tissues through specialized eye banks has further facilitated the adoption of these techniques, making the procedures more accessible and efficient across healthcare systems. Advanced imaging technologies such as anterior segment OCT are also enhancing surgical precision and post-op evaluations

- As healthcare systems in Europe aim to improve efficiency and patient outcomes, hospitals and clinics are increasingly investing in training and infrastructure to support these modern techniques

- This trend toward less invasive and more targeted surgical approaches is redefining corneal transplantation standards and accelerating the transition from full-thickness transplants to selective lamellar procedures. Consequently, medical institutions and surgeons across Europe are prioritizing DMEK and DSAEK integration into routine ophthalmic care, driving demand for related instruments and donor tissue processing technologies

- The increasing preference for minimally invasive corneal transplant solutions reflects broader shifts in ophthalmic surgery and is such asly to fuel long-term market growth by improving patient outcomes and reducing healthcare costs

Europe Corneal Transplant Market Dynamics

Driver

“Rising Prevalence of Corneal Disorders and Expansion of Donor Tissue Programs”

- The growing burden of corneal diseases such as keratoconus, Fuchs’ endothelial dystrophy, and trauma-related scarring is a primary driver for the increasing demand for corneal transplants across Europe

- For instance, in 2024, the European Eye Bank Association (EEBA) reported a steady rise in both demand for and availability of donor corneas, particularly in countries such as Germany, Italy, and the Netherlands, due to increased awareness campaigns and improvements in corneal donation systems

- National programs aimed at improving eye donation rates, along with the implementation of centralized tissue distribution networks, are significantly enhancing the efficiency of corneal transplant services

- In addition, the aging population across Europe, which is more prone to degenerative eye conditions, is contributing to increased surgical volume

- The expansion of donor tissue availability and streamlined transplant coordination through digital platforms are strengthening healthcare systems' ability to respond promptly to corneal blindness cases. As a result, more patients are able to access timely and effective treatment, supporting continued market growth

Restraint/Challenge

“Skin Irritation Issues and Regulatory Compliance Hurdle”

- Despite advancements, disparities in access to corneal transplant procedures persist across Europe, particularly in Central and Eastern European countries where healthcare infrastructure and specialized ophthalmic surgical training are still developing

- For instance, in countries such as Romania and Bulgaria, access to high-quality donor tissue and advanced surgical techniques such as DMEK is still limited due to underfunded public health systems and a lack of trained corneal surgeons

- Moreover, logistical challenges related to cross-border tissue transport, varying regulations around tissue procurement and transplantation, and inconsistent reimbursement structures can hinder the efficiency and scalability of transplant programs

- These systemic issues can lead to longer patient wait times, suboptimal surgical outcomes, and reliance on older transplant methods such as full-thickness keratoplasty, which may carry higher complication rates

- Overcoming these barriers will require collaborative policy efforts, increased investment in training and infrastructure, and harmonization of tissue handling standards across European nations to ensure equitable access and better long-term outcomes

Europe Corneal Transplant Market Scope

The market is segmented on the basis of procedure type, type, donor type, graft type, surgery type, indication, gender, age group, and end user.

- By Procedure Type

On the basis of procedure type, the Europe corneal transplant market is segmented into endothelial keratoplasty, penetrating keratoplasty, Anterior Lamellar Keratoplasty (ALK), corneal limbal stem cell transplant, artificial cornea transplant, and others. The penetrating keratoplasty segment dominated the market with the largest revenue share of 46.6% in 2024 due to its continued application in full-thickness corneal diseases and the widespread surgical expertise available across European countries.

The Endothelial Keratoplasty segment is anticipated to witness the fastest growth rate from 2025 to 2032, supported by increasing adoption for treating endothelial disorders, reduced rejection rates, and faster post-operative recovery.

- By Type

On the basis of type, the Europe corneal transplant market is segmented into human cornea and synthetic. The human cornea segment held the largest market share in 2024, attributed to the high success rates of human donor transplants and the strong presence of eye donation programs in countries such as Germany, France, and Italy.

The synthetic segment is expected to register the fastest growth during forecast period, driven by technological advancements in artificial corneal materials and their use in patients with repeat graft failures or rejection risks.

- By Donor Type

On the basis of donor type, the market is segmented into autograft and allograft. The allograft segment dominated the market in 2024, as donor tissues from deceased individuals form the standard source for most corneal transplants across Europe.

The autograft segment is expected to witness fastest growth during forecast period, particularly in regenerative procedures and stem cell transplant applications where the patient’s own tissue is used to reduce immunological risks.

- By Graft Type

On the basis of graft type, the market is segmented into partial thickness grafts (lamellar) and full thickness grafts (penetrating). The Full Thickness Grafts (Penetrating) segment accounted for the largest revenue share in 2024 due to its routine use in severe or full-layer corneal damage cases.

The partial thickness grafts (Lamellar) segment is projected to witness the fastest CAGR from 2025 to 2032, supported by the growing preference for lamellar techniques such as DMEK and DSAEK, which offer improved clinical outcomes and fewer complications.

- By Surgery Type

On the basis of surgery type, the market is segmented into conventional surgery and laser-assisted surgery. The Conventional Surgery segment led the market in 2024, primarily due to its long-standing application, affordability, and broader accessibility in public hospitals across Europe.

The laser-assisted surgery segment is expected to grow at the highest rate during forecast period, driven by increasing investment in ophthalmic laser platforms, improved surgical accuracy, and shorter patient recovery times.

- By Indication

On the basis of indication, the Europe corneal transplant market is segmented into fuch's endothelial dystrophy, infectious keratitis, bullous keratopathy, keratoconus, regraft procedures, corneal scarring, corneal ulcers, and others. Fuch’s Endothelial Dystrophy held the largest share in 2024 due to its high prevalence in aging populations and the effectiveness of endothelial keratoplasty in treatment.

Keratoconus is anticipated to grow at the fastest rate during forecast period, owing to improved early diagnosis, rising awareness among younger patients, and increased use of anterior lamellar keratoplasty for its management.

- By Gender

On the basis of gender, the market is segmented into male and female. The Male segment dominated the market in 2024, influenced by higher reported rates of eye trauma and disease severity among men in several European regions.

The Female segment is expected to grow steadily, during forecast period due to increasing access to eye care services and awareness initiatives targeted at older women affected by corneal disorders.

- By Age Group

On the basis of age group, the market is segmented into geriatric, adult, and pediatric. The Geriatric segment held the largest share in 2024, as the elderly are more prone to corneal degeneration, dystrophies, and conditions requiring transplantation.

The Pediatric segment is projected to grow at a significant rate during forecast period, due to rising focus on congenital corneal diseases and improving surgical success rates in children.

- By End User

On the basis of end user, the Europe corneal transplant market is segmented into hospitals, eye clinics, ambulatory surgical centers, academic & research institutes, and others. Hospitals accounted for the largest revenue share in 2024 due to the availability of comprehensive eye care infrastructure, access to trained ophthalmologists, and higher volume of surgeries performed.

Eye Clinics are expected to grow at the fastest pace during forecast period, , supported by increasing privatization, outpatient surgical procedures, and adoption of advanced corneal imaging and laser systems in standalone facilities.

Europe Corneal Transplant Market Regional Analysis

- Germany dominated the Europe corneal transplant market with the largest revenue share of 28.5% in 2024, supported by its advanced healthcare infrastructure, strong donor tissue availability through organized eye banks, and high volume of ophthalmic procedures performed annually

- Patients and healthcare providers in the country benefit from early diagnosis, wide access to donor corneas, and the availability of advanced techniques such as DMEK and DSAEK, which contribute to better clinical outcomes and reduced recovery times

- This strong market presence is further supported by public health initiatives promoting organ and tissue donation, skilled corneal surgeons, and favorable reimbursement policies, making Germany a leading hub for corneal transplantation across both public and private healthcare facilities

The Germany Corneal Transplant Market Insight

The Germany corneal transplant market accounted for the largest revenue share in the Europe corneal transplant market in 2024, supported by a robust healthcare infrastructure, well-established eye banking networks, and widespread access to advanced surgical procedures such as DMEK and DSAEK. Public awareness campaigns and high surgical volumes contribute to Germany’s leading position. In addition, favorable reimbursement policies and investment in ophthalmic technologies are expected to further strengthen the market in the country.

France Corneal Transplant Market Insight

The France corneal transplant market is projected to grow significantly during the forecast period due to strong public health initiatives around organ donation and vision preservation. France benefits from centralized transplant coordination and wide accessibility to donor corneas. The adoption of modern surgical tools in both university hospitals and private eye clinics supports procedural innovation and patient safety.

Italy Corneal Transplant Market Insight

The Italy corneal transplant market is emerging as a key player in the corneal transplant market across Southern Europe, driven by active national eye donation programs and growing adoption of endothelial keratoplasty. Italian hospitals and transplant centers are increasingly investing in precision diagnostics and donor tissue processing, improving overall graft success rates. Enhanced collaboration with European eye banks is expected to further improve access and outcomes.

United Kingdom Corneal Transplant Market Insight

The U.K. corneal transplant market is anticipated to witness notable growth, supported by the NHS-organized donor systems and advanced corneal care capabilities in specialized hospitals such as Moorfields Eye Hospital. A growing elderly population and the presence of skilled ophthalmic surgeons are increasing transplant volumes. The country’s regulatory focus on safe tissue handling and innovation in outpatient surgeries are additional contributors to market expansion.

Spain Corneal Transplant Market Insight

The Spain corneal transplant market is witnessing increased demand for corneal transplants due to improved awareness of ocular diseases and consistent growth in donor availability, supported by its globally recognized organ donation framework. Spanish healthcare institutions are expanding their use of lamellar techniques, particularly in urban centers, and leveraging telemedicine to improve post-operative care access.

Poland Corneal Transplant Market Insight

The Poland corneal transplant market is expected to grow at the fastest CAGR in the Europe corneal transplant market during the forecast period, fueled by enhanced healthcare infrastructure, rising access to trained corneal surgeons, and government efforts to strengthen transplant services. Expanding use of DSAEK and DMEK techniques in tertiary care hospitals and increasing support from European healthcare programs are accelerating the market in Poland.

Europe Corneal Transplant Market Share

The Europe corneal transplant industry is primarily led by well-established companies, including:

- CorneaGen, Inc. (U.S.)

- KeraLink International (U.S.)

- Aurolab (India)

- AJL Ophthalmic S.A. (Spain)

- DIOPTEX GmbH (Austria)

- Geuder AG (Germany)

- HumanOptics AG (Germany)

- Presbia PLC (Ireland)

- Keramed, Inc. (U.S.)

- Alcon Inc. (Switzerland)

- Carl Zeiss Meditec AG (Germany)

- Bausch + Lomb Incorporated (Canada)

- Ziemer Ophthalmic Systems AG (Switzerland)

- Morcher GmbH (Germany)

- Ophtec BV (Netherlands)

- TearLab Corporation (U.S.)

- VSY Biotechnology GmbH (Germany)

- EyeYon Medical Ltd. (Israel)

- Mediphacos Ltd. (Brazil)

- LinkoCare Life Sciences AB (Sweden)

What are the Recent Developments in Europe Corneal Transplant Market?

- In May 2024, Germany’s University Eye Hospital in Tübingen announced the successful integration of AI-assisted surgical planning tools for DMEK procedures, aiming to enhance precision and patient outcomes in endothelial keratoplasty. This advancement reflects Germany’s ongoing leadership in adopting high-tech solutions in ophthalmology and its commitment to improving the success rates and recovery times associated with corneal transplants

- In April 2024, the U.K.-based Moorfields Eye Hospital launched a collaborative initiative with NHS Blood and Transplant to increase corneal tissue donation awareness across England. The campaign includes nationwide outreach programs and digital engagement tools designed to address donor shortages and streamline transplant wait times. This initiative underlines the importance of public education in expanding tissue availability for life-changing surgeries

- In March 2024, France’s Fondation Rothschild Hospital introduced femtosecond laser-assisted techniques in anterior lamellar keratoplasty (ALK), becoming one of the first centers in Western Europe to widely adopt this approach. The precision offered by this method has been associated with improved graft stability and reduced post-operative complications, enhancing France’s role in ophthalmic surgical innovation

- In February 2024, the Italian Society of Ophthalmology (SOI) partnered with leading eye banks in Milan and Rome to implement a centralized digital platform for donor cornea tracking and allocation. This platform enhances transparency, reduces tissue wastage, and ensures equitable distribution, showcasing Italy’s proactive steps toward digital transformation in transplant logistics

- In January 2024, Poland’s Ministry of Health allocated new funding to support specialized corneal transplant training programs in academic hospitals across Warsaw and Kraków. This investment aims to address the shortage of corneal surgeons and expand the reach of advanced procedures such as DSAEK and DMEK, positioning Poland as a fast-growing contributor in the European transplant landscape

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.