Europe Ehealth Market

Market Size in USD Billion

USD

14.80 Billion

USD

81.13 Billion

2025

2033

USD

14.80 Billion

USD

81.13 Billion

2025

2033

| 2026 - 2033 | |

| USD 14.80 Billion | |

| USD 81.13 Billion | |

| % | |

|

Europe eHealth Market Overview

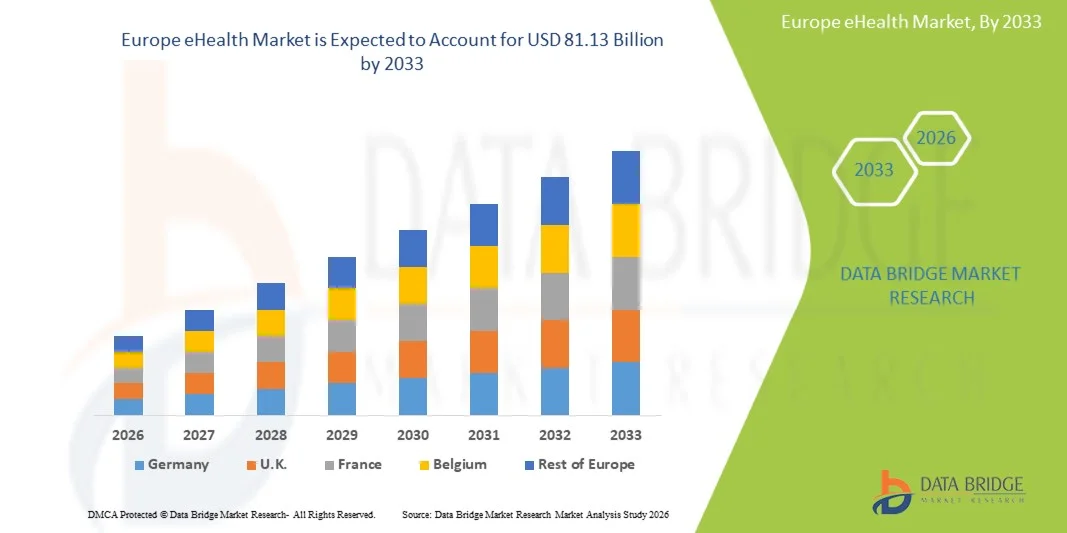

The Europe eHealth market was valued at USD 14.80 billion in 2025 and is projected to reach USD 81.13 billion by 2033, growing at a CAGR of 23.7% from 2026 to 2033. The market is experiencing strong growth driven by increasing digitalization of healthcare systems, rising adoption of telemedicine and remote patient monitoring solutions, and expanding government initiatives supporting interoperable electronic health records and connected care infrastructure.

The growing prevalence of chronic diseases, aging populations, and increasing pressure on healthcare providers to improve efficiency and reduce costs are encouraging hospitals, clinics, and public health agencies to invest in advanced eHealth technologies. Digital health platforms, mobile health applications, AI-powered clinical decision support systems, and cloud-based healthcare management solutions are transforming care delivery across the region, enabling improved patient outcomes, enhanced accessibility, and data-driven healthcare decision-making.

Key Market Trends & Insights

- Germany dominated the Europe eHealth market with the largest revenue share of 21.68% in 2025, supported by strong healthcare digitization initiatives, widespread adoption of electronic health records, and significant investments in digital health infrastructure.

- The Solutions segment led the market with a 67.48% share in 2025, driven by the widespread deployment of electronic health records, telehealth platforms, healthcare analytics, and clinical workflow management systems across hospitals and healthcare networks.

- Poland is expected to be the fastest-growing country at a CAGR of 26.4% from 2026 to 2033, fueled by healthcare modernization programs, expanding telehealth services, and increasing public and private investments in digital healthcare technologies.

- Services are the fastest-growing offering type, projected to register a CAGR of 25.9%, reflecting the surge in demand for implementation, integration, consulting, maintenance, and managed services.

- The Cloud segment dominated the deployment category with a 57.84% revenue share in 2025, led by scalability, cost-efficiency, and ability to support real-time access to healthcare information across multiple care settings.

- Large Enterprises accounted for 64.31% of the market, preferred by the substantial investments in digital transformation and advanced healthcare IT infrastructure.

- The Video Sessions segment is the fastest-growing functionality category, with a CAGR of 28.1%, driven by the rapid expansion of telemedicine and virtual healthcare consultations.

Market Size & Forecast

- Global Market Value (2025): USD 14.80 Billion

- Expected Market Value (2033): USD 81.13 Billion

- Forecast CAGR (2026–2033): 23.7%

- Leading Country in 2025: Germany

- Fastest Growing Country: Poland

Report Scope and Europe eHealth Market Segmentation

|

Attributes |

Europe eHealth Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe |

|

Key Market Players |

· Dedalus Group (Italy) · CompuGroup Medical SE & Co. KGaA (Germany) · Nexus AG (Germany) · Cegedim (France) · EMIS Group Plc (U.K.) · System C Healthcare Ltd (U.K.) · TPP (U.K.) · Orion Health (New Zealand) · MEDITECH (U.S.) · InterSystems Corporation (U.S.) · Epic Systems Corporation (U.S.) · Oracle Health (U.S.) · Sectra AB (Sweden) · Cambio Healthcare Systems (Sweden) · Tunstall Healthcare Group (U.K.) · Siemens Healthineers AG (Germany) · Philips (Netherlands) · Doctolib (France) · KRY International AB (Sweden) · CGM Clinical Europe GmbH (Germany) |

|

Market Opportunities |

· Expansion of cross-border digital health services within the European Union · Growing adoption of remote patient monitoring for aging populations · Integration of artificial intelligence into clinical workflows and diagnostics |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe eHealth Market Trends

Trend: Expansion of AI-Powered Digital Health Platforms

Healthcare providers across Europe are increasingly adopting AI-powered eHealth platforms to improve clinical decision-making, automate administrative workflows, and enhance patient engagement without increasing operational burden. The integration of predictive analytics, digital therapeutics, and intelligent virtual assistants enables more personalized care delivery and proactive disease management. Hospitals and healthcare networks are similarly leveraging digital platforms to optimize resource allocation through standardized, data-driven healthcare processes, while cloud-based technologies create connected ecosystems that closely support real-world clinical and patient-care requirements. For instance, in March 2025, the European Commission expanded support for AI-driven healthcare initiatives under the European Health Data Space framework, encouraging broader adoption of intelligent digital health solutions across member states.

Europe eHealth Market Dynamics

Key Market Driver: Growing Adoption of Digital Healthcare and Remote Patient Monitoring

The rapid expansion of telehealth services and remote patient monitoring programs has created substantial demand for advanced eHealth solutions that can support continuous patient engagement, real-time health tracking, and integrated care delivery across diverse healthcare settings. Hospitals, healthcare providers, and public health organizations are deploying digital health platforms as a core component of their care strategies, reducing operational costs, improving access to healthcare services, and enhancing patient outcomes through data-driven interventions and personalized treatment approaches. For instance, in January 2025, NHS England expanded digital monitoring initiatives for long-term conditions, reinforcing the role of connected healthcare technologies in improving patient management and healthcare efficiency.

Key Restraint/Challenge: Data Privacy Concerns and Interoperability Complexities

A significant restraint in the Europe eHealth market is the complexity of maintaining data privacy, cybersecurity compliance, and interoperability across diverse healthcare systems. Modern eHealth platforms integrate electronic health records, cloud infrastructure, connected medical devices, and patient applications, requiring substantial investment in security frameworks, regulatory compliance, and system integration. The operational burden extends to data governance requirements, cross-border information exchange standards, and continuous technology upgrades, making implementation challenging for smaller healthcare providers and resource-constrained organizations.

For instance, in 2025, several European healthcare organizations increased investments in GDPR-compliant digital infrastructure and cybersecurity modernization programs to address growing concerns regarding healthcare data protection and interoperability requirements.

Key Market Opportunity: Expansion of Cross-Border Health Data Exchange Ecosystems

The expansion of cross-border digital health ecosystems presents a significant market opportunity. Interoperable eHealth platforms can enable seamless patient record sharing, improve care coordination, and support data-driven healthcare decision-making across multiple jurisdictions. The development of cloud-enabled health information exchanges and AI-assisted clinical support tools is further accelerating digital transformation, opening growth opportunities across hospitals, healthcare networks, and public health systems throughout Europe. For instance, in March 2025, the European Health Data Space implementation efforts advanced across member countries, supporting secure health data exchange and fostering broader adoption of interoperable eHealth solutions.

Europe eHealth Market Scope

The Europe eHealth market is segmented on the basis of offering, deployment, enterprise size, functionality, technology, and end user.

- By Offering

On the basis of offering, the Europe eHealth market is segmented into solutions and services. The Solutions segment dominated the market with a 67.48% share in 2025, owing to the widespread deployment of electronic health records, telehealth platforms, healthcare analytics, and clinical workflow management systems across hospitals and healthcare networks. Healthcare organizations are prioritizing digital infrastructure investments to improve patient outcomes and operational efficiency. The increasing need for interoperable healthcare data systems is further driving solution adoption. Government-led healthcare digitization initiatives are supporting large-scale implementation across the region. Continuous innovation in AI-enabled healthcare platforms is strengthening the segment’s position. The segment benefits from long-term investments in healthcare IT modernization and connected care ecosystems.

The Services segment is projected to register the fastest growth at a CAGR of 25.9% from 2026 to 2033, driven by rising demand for implementation, integration, consulting, maintenance, and managed services. As healthcare providers deploy increasingly complex digital health platforms, the need for specialized technical support continues to expand. Regulatory compliance requirements are also encouraging organizations to seek external expertise. Cloud migration and interoperability projects are generating substantial service opportunities. Growing adoption of AI and advanced analytics solutions is further increasing demand for professional services. The segment is also benefiting from healthcare workforce shortages and the need for outsourced digital transformation support.

- By Deployment

On the basis of deployment, the Europe eHealth market is segmented into cloud and on-premises. The Cloud segment dominated the market with a 57.24% share in 2025, owing to its scalability, cost-efficiency, and ability to support real-time access to healthcare information across multiple care settings. Healthcare organizations increasingly prefer cloud-based systems for managing patient records, telehealth applications, and clinical workflows. The model enables faster deployment and easier integration with emerging digital health technologies. Continuous improvements in cloud security and compliance capabilities are supporting adoption. The growing demand for remote healthcare delivery is also accelerating cloud utilization. The segment remains central to Europe’s healthcare digitalization initiatives.

The On-Premises segment is projected to register the fastest growth at a CAGR of 25.8% from 2026 to 2033, driven by increasing concerns regarding patient data privacy, cybersecurity, and regulatory compliance. Many hospitals, government healthcare institutions, and large healthcare networks continue to prefer on-premises infrastructure for greater control over sensitive health information. These systems offer enhanced data governance and customization capabilities tailored to specific organizational requirements. Growing investments in healthcare cybersecurity and national health data sovereignty initiatives are further supporting adoption. Large healthcare providers are increasingly upgrading legacy systems with advanced on-premises solutions. The segment is also benefiting from stringent European data protection regulations and the need for secure clinical data management.

- By Enterprise Size

On the basis of enterprise size, the Europe eHealth market is segmented into large enterprises and small and medium enterprises. The Large Enterprises segment dominated the market with a 64.31% share in 2025, driven by substantial investments in digital transformation and advanced healthcare IT infrastructure. Large hospital networks and healthcare systems possess the financial resources necessary for large-scale eHealth deployments. These organizations are leading adopters of AI-powered analytics, telehealth platforms, and integrated patient management systems. Regulatory compliance requirements further encourage investments in sophisticated digital solutions. The segment benefits from strong partnerships with technology providers and healthcare innovators. Extensive patient populations also increase the need for comprehensive digital healthcare platforms.

The Small and Medium Enterprises (SMEs) segment is projected to register the fastest growth at a CAGR of 26.7% from 2026 to 2033, fueled by increasing accessibility of cloud-based healthcare technologies and subscription-based software models. SMEs are increasingly adopting digital health solutions to improve operational efficiency and patient engagement. Lower implementation costs are making advanced healthcare technologies more attainable. Government incentives for healthcare digitization are further supporting adoption among smaller organizations. Growing awareness of data-driven healthcare benefits is encouraging investments. The segment is also benefiting from simplified deployment models and managed service offerings.

- By Functionality

On the basis of functionality, the Europe eHealth market is segmented into content management system, group messaging, dashboard, video sessions, social support, and others. The Dashboard segment dominated the market with a 26.84% share in 2025, owing to its critical role in delivering real-time clinical insights, patient monitoring data, and healthcare performance metrics. Healthcare providers increasingly rely on dashboards for informed decision-making and workflow optimization. These solutions improve visibility across clinical and administrative operations. Integration with electronic health records enhances their value within healthcare settings. Growing emphasis on population health management is further supporting adoption. The segment remains essential for data-driven healthcare delivery.

The Video Sessions segment is projected to witness the fastest growth at a CAGR of 28.1% from 2026 to 2033, driven by the rapid expansion of telemedicine and virtual healthcare consultations. Patients and healthcare providers increasingly prefer remote care models for convenience and accessibility. Advances in video communication technologies are improving the quality of virtual consultations. Healthcare systems are integrating video capabilities into broader digital health ecosystems. Rising demand for specialist consultations and chronic disease management is accelerating adoption. The segment is also benefiting from evolving reimbursement policies supporting telehealth services.

- By Technology

On the basis of technology, the Europe eHealth market is segmented into Internet of Things (IoT), chatbots, artificial intelligence, block chain and big data, and others. The Internet of Things (IoT) segment dominated the market with a 31.46% share in 2025, driven by extensive adoption of connected medical devices, wearable health monitors, and remote patient monitoring systems. IoT technologies enable continuous health tracking and real-time clinical data collection. Healthcare providers are increasingly utilizing connected devices to improve patient outcomes and care coordination. Growing prevalence of chronic diseases is supporting adoption of remote monitoring solutions. Technological advancements in sensor technologies are further enhancing capabilities. The segment benefits from strong demand for proactive and preventive healthcare approaches.

The Artificial Intelligence segment is expected to register the fastest growth at a CAGR of 29.3% from 2026 to 2033, fueled by increasing demand for predictive analytics, clinical decision support, and intelligent automation tools. AI is transforming healthcare operations by improving diagnostic accuracy and treatment planning. Healthcare providers are leveraging machine learning algorithms to optimize resource allocation and patient management. Growing healthcare data volumes are creating strong demand for advanced analytical capabilities. Investments in precision medicine and personalized healthcare are accelerating adoption. The segment is also benefiting from continuous innovation in generative AI and healthcare-specific models.

- By End User

On the basis of end user, the Europe eHealth market is segmented into healthcare providers, payers, healthcare consumers, pharmacies, and others. The Healthcare Providers segment dominated the market with a 44.37% share in 2025, owing to widespread adoption of electronic health records, telemedicine platforms, and clinical management systems. Hospitals and clinics are increasingly investing in digital health technologies to improve efficiency and patient outcomes. Regulatory requirements for healthcare digitization are further supporting adoption. Integration of AI and analytics tools is enhancing operational performance. The segment benefits from continuous investments in connected care infrastructure. Healthcare providers remain the primary users of eHealth solutions across Europe.

The Healthcare Consumers segment is projected to witness the fastest growth at a CAGR of 27.8% from 2026 to 2033, driven by increasing adoption of mobile health applications, wearable devices, and patient engagement platforms. Consumers are becoming more proactive in managing their health through digital tools and remote care services. Growing awareness of preventive healthcare is encouraging technology adoption. Improved access to digital health information is enhancing patient participation in care decisions. Expansion of telehealth and home-based care services is further supporting growth. The segment is benefiting from rising demand for personalized and convenient healthcare experiences.

Europe eHealth Market Regional Analysis

Germany dominated the Europe eHealth market with the largest revenue share of 21.68% in 2025, supported by strong healthcare digitization initiatives, widespread adoption of electronic health records, and significant investments in digital health infrastructure. The country also benefits from comprehensive electronic health record initiatives, high adoption of telehealth and remote monitoring platforms, and growing utilization of eHealth solutions across hospitals, clinics, and outpatient care settings. Increasing focus on interoperable healthcare systems and AI-enabled clinical decision support technologies continues to strengthen Germany’s leadership position in the European eHealth market.

The Germany eHealth Market Insight

The Germany eHealth market is witnessing strong growth due to rising investments in healthcare digitalization programs, electronic health records, and telemedicine technologies. The country’s advanced healthcare infrastructure, along with increasing adoption of AI-powered analytics, remote patient monitoring, and connected care platforms, is driving demand across hospitals, clinics, and healthcare networks. In addition, growing emphasis on improving healthcare efficiency, enhancing patient outcomes, and expanding access to digital health services is accelerating eHealth adoption across Germany.

U.K. eHealth Market Insight

The U.K. eHealth market is experiencing steady growth, supported by rising adoption of digital healthcare technologies, virtual care services, and connected health platforms. Increasing investments in healthcare IT infrastructure and growing demand for cost-effective, accessible healthcare delivery models are contributing to market growth. Furthermore, integration of artificial intelligence, cloud computing, and advanced data analytics technologies is improving healthcare efficiency and patient engagement, positioning the U.K. as a key innovation hub in the eHealth industry.

France eHealth Market Insight

The France eHealth market is expanding steadily due to increasing government support for healthcare digitization, growing telemedicine adoption, and rising investments in digital health infrastructure. Healthcare providers are increasingly implementing electronic health records, patient engagement platforms, and remote monitoring solutions to improve care quality and operational performance. Moreover, growing demand for integrated healthcare services and data-driven clinical decision-making is supporting market expansion across the country.

Poland eHealth Market Insight

The Poland eHealth market is growing rapidly, driven by increasing healthcare modernization initiatives, expanding digital infrastructure, and rising government focus on healthcare accessibility and efficiency. Growing adoption of telemedicine, electronic health records, and cloud-based healthcare platforms across hospitals and healthcare facilities is significantly boosting market demand. In addition, rising investments in healthcare IT, increasing awareness regarding digital health benefits, and ongoing technological advancements are positioning Poland as one of the fastest-growing eHealth markets in Europe.

Europe eHealth Market Share

The Europe eHealth industry is primarily led by well-established companies, including:

- Dedalus Group (Italy)

- CompuGroup Medical SE & Co. KGaA (Germany)

- Nexus AG (Germany)

- Cegedim (France)

- EMIS Group Plc (U.K.)

- System C Healthcare Ltd (U.K.)

- TPP (U.K.)

- Orion Health (New Zealand)

- MEDITECH (U.S.)

- InterSystems Corporation (U.S.)

- Epic Systems Corporation (U.S.)

- Oracle Health (U.S.)

- Sectra AB (Sweden)

- Cambio Healthcare Systems (Sweden)

- Tunstall Healthcare Group (U.K.)

- Siemens Healthineers AG (Germany)

- Philips (Netherlands)

- Doctolib (France)

- KRY International AB (Sweden)

- CGM Clinical Europe GmbH (Germany)

Latest Developments in Europe eHealth Market

- In March 2025, the European Commission, together with the Polish Presidency of the Council of the EU, hosted the high-level event “The European Health Data Space (EHDS) – Unlocking Europe's Health Data Future Together” following the adoption of the EHDS Regulation. The initiative is designed to establish a secure framework for sharing electronic health data across EU member states, improve interoperability, and support innovation in digital healthcare. This development marks a major step toward a unified European digital health ecosystem

- In January 2025, the Council of the European Union adopted the European Health Data Space (EHDS) Regulation, creating a new legal framework to improve cross-border access to electronic health data and enable secure data sharing for research and healthcare innovation. The regulation also strengthens patient control over health information while promoting interoperability among electronic health record systems across Europe. This milestone significantly advances healthcare digitalization within the European Union

- In May 2024, Philips expanded its AI-enabled healthcare informatics and remote patient monitoring capabilities across Europe through enhancements to its connected care portfolio. The development focused on strengthening clinical decision support, hospital workflow optimization, and virtual care delivery. The expansion reflects the growing adoption of digital health technologies among European healthcare providers seeking improved patient outcomes and operational efficiency

- In December 2023, Oracle Health continued the integration and expansion of former Cerner healthcare technologies across European healthcare systems, strengthening cloud-based electronic health record capabilities and healthcare data interoperability solutions. The initiative supports healthcare organizations seeking modern digital infrastructures capable of managing growing volumes of clinical data

- In March 2022, the European Commission proposed the creation of the European Health Data Space (EHDS), introducing the first EU-wide framework for secure access, exchange, and reuse of electronic health data. The proposal aimed to empower citizens with greater control over their health information while enabling healthcare providers, researchers, and policymakers to utilize health data more effectively. The initiative laid the foundation for Europe's future digital health ecosystem

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.