Europe Electrosurgery Market

Market Size in USD Billion

USD

4.58 Billion

USD

6.42 Billion

2024

2032

USD

4.58 Billion

USD

6.42 Billion

2024

2032

| 2025 - 2032 | |

| USD 4.58 Billion | |

| USD 6.42 Billion | |

| % | |

|

Electrosurgery Market Size

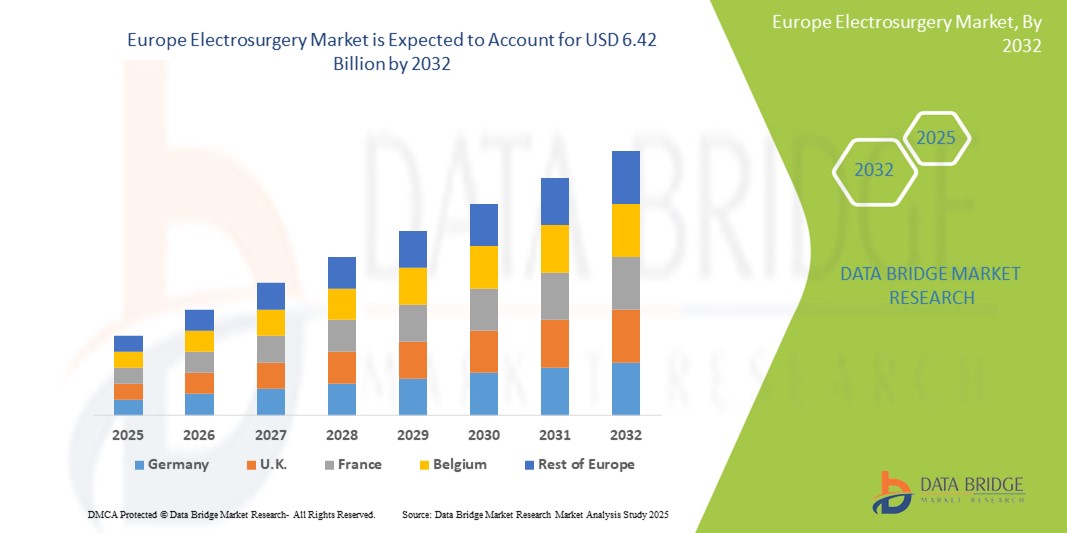

- The Europe Electrosurgery market size was valued at USD 4.58 billion in 2024 and is expected to reach USD 6.42 billion by 2032, at a CAGR of 4.3% during the forecast period

- The market growth is largely fueled by the rising prevalence of chronic diseases necessitating surgical interventions, the increasing aging population, and the growing demand for minimally invasive surgeries.

- Furthermore, technological advancements in electrosurgical instruments, such as improved precision, safety features, and integration with advanced imaging and robotic systems, are driving market expansion. These converging factors are accelerating the uptake of electrosurgery solutions, thereby significantly boosting the industry's growth.

Electrosurgery Market Analysis

- Electrosurgery encompasses a wide array of medical devices that utilize high-frequency electrical current to cut, coagulate, desiccate, and fulgurate tissues during surgical procedures. This market includes electrosurgical generators, active electrodes, and various accessories. Electrosurgery is a fundamental technique employed across numerous surgical specialties, offering benefits such as precise tissue cutting, reduced blood loss, and improved hemostasis. The market is driven by the increasing volume of surgical procedures, the growing demand for minimally invasive techniques, and continuous technological advancements in electrosurgical systems.

- The escalating demand for electrosurgery is primarily fueled by the increasing number of general, gynecological, urological, orthopedic, and cosmetic surgeries, the growing adoption of outpatient procedures, and the rising focus on improving surgical outcomes and patient safety.

- Germany dominates the Electrosurgery market in Europe, holding the largest revenue share of 26.7% in 2025, supported by advanced surgical infrastructure, high procedure volumes, and early adoption of cutting-edge electrosurgical technologies. Factors such as a well-established hospital network, skilled surgical professionals, and rising demand for minimally invasive procedures contribute significantly to the market's strong performance.

- Germany is projected to be the fastest-growing country in the European Electrosurgery market during the forecast period, growth is fueled by the rising prevalence of chronic conditions requiring surgical intervention, such as cancer and cardiovascular diseases, increasing outpatient surgical procedures, and continuous innovation by key industry players in devices offering better precision, safety, and ease of use.

- Electrosurgery Instruments and Accessories segment is expected to dominate the Electrosurgery market with a market share of 41.62% in 2025, due to their versatility, cost-effectiveness, and widespread use in general surgeries, gynecology, and urology. These devices offer effective tissue dissection and coagulation, making them a mainstay in both hospital operating rooms and ambulatory surgical centers.

Report Scope and Electrosurgery Market Segmentation

|

Attributes |

Electrosurgery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Electrosurgery Market Trends

“Growing preference for minimally invasive surgeries (MIS)”

- Increasing Demand for Minimally Invasive Surgery (MIS) and Technological Advancements: A significant and accelerating trend in the Europe electrosurgery market is the increasing demand for minimally invasive surgical (MIS) procedures, which heavily rely on advanced electrosurgical instruments. This trend is coupled with continuous technological innovations that enhance the precision, safety, and efficiency of electrosurgical units.

- For instance, modern electrosurgical generators integrate smart feedback and monitoring systems, such as those from Valleylab FT10 (by Medtronic) and ESG-400 (by Bovie Medical). These systems automatically adjust power delivery based on real-time tissue impedance, minimizing the risk of thermal injury to surrounding tissues and providing safer outcomes, especially in delicate surgeries like neurosurgery or laparoscopic procedures.

- The market is also witnessing the development of innovative electrode designs with improved precision and control, contributing to market expansion. Furthermore, the integration of robotic-assisted surgery and AI-based feedback systems is improving the precision, safety, and efficiency of electrosurgical procedures.

- This trend towards more precise, safer, and technologically advanced electrosurgical solutions is fundamentally reshaping surgical practices. Consequently, companies are investing heavily in R&D to develop next-generation instruments with enhanced features and connectivity.

- The demand for electrosurgical devices that offer seamless integration with digital workflows and advanced safety features is growing rapidly across hospitals and ambulatory surgical centers, as healthcare providers prioritize improved patient outcomes and operational efficiency.

Electrosurgery Market Dynamics

Driver

“Rising prevalence of chronic diseases”

- Growing Prevalence of Chronic Diseases and Increasing Surgical Procedures: The rising incidence of chronic diseases, such as cardiovascular diseases, cancer, and neurological disorders, which often necessitate surgical interventions, is a significant driver for the heightened demand for electrosurgery devices

- For instance, the increasing prevalence of age-related conditions like cardiac arrhythmias and cancerous tumors drives up the demand for electrosurgical procedures in hospitals, clinics, and ablation centers. Electrosurgery is crucial in these surgeries as it provides high-precision cutting, coagulation, and tissue removal capabilities

- The increasing aging population is more susceptible to various health conditions requiring surgical treatments, further boosting the demand for electrosurgical instruments.

- The shift towards outpatient surgeries and ambulatory surgical centers (ASCs) is also propelling the adoption of advanced, portable electrosurgical units due to their cost-effectiveness and shorter patient recovery times.

- Additionally, increasing healthcare expenditures and investments in upgrading surgical facilities contribute to the market's expansion

Restraint/Challenge

“High initial cost of advanced equipment”

- Concerns Regarding Procedural Risks and High Equipment Costs: Concerns surrounding the potential for complications, such as toxic fumes produced during surgical procedures and electromagnetic interference-related risks, along with the high cost of advanced electrosurgical systems, present significant challenges to widespread market adoption.

- For instance, surgical smoke, emerging from the thermal breakdown of tissue during electrosurgery, can pose health risks to operating room staff. While smoke evacuation systems are being developed, addressing these concerns requires continuous innovation and adherence to stringent safety protocols.

- The initial investment for purchasing sophisticated electrosurgical generators and instruments can be substantial, particularly for smaller healthcare facilities or those with budget constraints. This high cost can limit widespread adoption despite the clinical benefits.

- Furthermore, stringent regulatory frameworks and the need for continuous training of surgeons and operating room staff to operate sophisticated electrosurgical technologies add to the operational burden and can impede market growth

Electrosurgery Market Scope

The market is segmented on the basis product, type of surgery and end user.

- By Product

On the basis of Product, the Electrosurgery market is segmented into Electrosurgical Generators, Electrosurgical Instruments and Accessories, and Argon and Smoke Management Systems. The Electrosurgical Instruments and Accessories segment dominates the largest market revenue share of 41.62% in 2025, driven by their central role in regulating electrical energy for various surgical procedures. These generators enable precise control of current intensity and waveform, making them essential across a wide range of surgical specialties. Technological advancements, such as intelligent energy delivery and integration with robotic systems, are further enhancing their performance and adoption.

The Argon and Smoke Management Systems segment is anticipated to witness the fastest growth rate of 5.8% from 2025 to 2032 owing to the rising awareness of surgical smoke hazards and increasing emphasis on operating room safety. The use of argon gas for controlled coagulation and the need to improve visibility during minimally invasive procedures are accelerating the adoption of advanced smoke evacuation solutions.

- By Type of Surgery

On the basis of application, the Electrosurgery market is segmented into General Surgery, Gynecological Surgery, Urologic Surgery, Orthopedic Surgery, Cardiovascular Surgery, Cosmetic Surgery, Neurosurgery, and Other Surgeries. The General Surgery held the largest market revenue share in 2025, due to the broad application of electrosurgical devices in procedures such as appendectomies, hernia repairs, and gastrointestinal operations. The versatility and efficiency of electrosurgical techniques in cutting and coagulation drive their widespread use in this segment.

The Cosmetic Surgery is expected to witness the fastest CAGR from 2025 to 2032, driven by the increasing demand for aesthetic procedures such as skin resurfacing, body contouring, and blepharoplasty. Electrosurgery offers benefits like minimal bleeding, improved precision, and faster recovery, which align with the preferences of cosmetic surgery patients.

- By End users

On the basis of end users, the Electrosurgery market is segmented into Hospitals, Clinics & Ablation Centers, Ambulatory Surgical Centers (ASCs), and Research Laboratories & Academic Institutes. The Hospitals, Clinics & Ablation Centers segment accounted for the largest market revenue share in 2025 as they are primary centers for both inpatient and outpatient surgeries. The availability of comprehensive surgical infrastructure and skilled professionals supports high adoption of electrosurgical technologies in these settings.

The Ambulatory Surgical Centers (ASCs) segment is expected to witness the fastest CAGR from 2025 to 2032, due to the shift toward minimally invasive, same-day procedures. ASCs benefit from lower costs, quicker patient turnover, and increasing availability of portable and user-friendly electrosurgical equipment.

Electrosurgery Market Regional Analysis

- Germany dominates the Europe Electrosurgery Market, accounting for the largest revenue share of 26.7% in 2025, driven by the country’s advanced healthcare infrastructure, rising prevalence of chronic diseases, and rapid adoption of digital and remote patient monitoring technologies. Factors such as aging population, increasing hospitalization rates, and strong integration of telehealth solutions continue to propel market demand.

- Germany’s market benefits from favorable reimbursement policies, a growing focus on value-based care, and the presence of major industry players such as GE Healthcare, Medtronic, and Philips. These companies are continuously introducing innovative monitoring solutions, including wearable and wireless technologies that support real-time data tracking and early detection of critical health events.

- Additionally, the surge in remote and home-based care, especially following the COVID-19 pandemic, has accelerated the deployment of multi-parameter monitoring systems across outpatient settings, long-term care facilities, and home environments. Government support for remote health management and digital health tools further contributes to the sustained growth.

France Electrosurgery Market Insight

The France Electrosurgery market is expected to witness steady growth over the forecast period, driven by increasing demand for chronic disease management, rising healthcare digitization, and federal efforts to reduce hospital readmissions. National initiatives to strengthen telemedicine and digital health infrastructure—such as France Health Infoway—have encouraged widespread adoption of connected patient monitoring technologies, particularly in rural and underserved communities. The country's publicly funded healthcare system also supports equitable access to diagnostic and monitoring tools, contributing to a more standardized rollout of patient monitoring devices.

U.K. Electrosurgery Market Insight

The U.K. Electrosurgery market is poised for robust growth, propelled by improvements in healthcare infrastructure, expanding access to medical technologies, and rising awareness about early disease detection and management. The U.K. government's ongoing healthcare reform and national programs to reduce non-communicable diseases (such as diabetes and hypertension) are driving the adoption of monitoring devices in both urban and semi-urban settings. Public health campaigns and investments in hospital modernization are also boosting demand for ICU and bedside monitoring systems.

Electrosurgery Market Share

The Electrosurgery industry is primarily led by well-established companies, including:

- Medtronic plc (Ireland)

- Olympus Corporation (Japan)

- Johnson & Johnson (Ethicon) (U.S.)

- B. Braun Melsungen AG (Germany)

- CONMED Corporation (U.S.)

- Erbe Elektromedizin GmbH (Germany)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Bovie Medical Corporation (now Apyx Medical) (U.S.)

- KLS Martin Group (Germany)

- Smith & Nephew plc (U.K.)

Latest Developments in Europe Electrosurgery Market

- In April 2024, Integra LifeSciences Holdings Corporation acquired Acclarent, Inc., broadening Integra's product range and enhancing its market presence in ENT surgical solutions.

- In March 2024, Medical Device Business Services (a subsidiary of Johnson & Johnson) collaborated with NVIDIA Corporation to enhance real-time analysis and make AI algorithms more widely accessible in operating rooms globally, improving surgeon decision-making and patient outcomes.

- In November 2023, Erbe Elektromedizin GmbH launched TriSect rapide, a tool designed for bipolar coagulation, division, and sealing of vessels and tissue bundles, suitable for various open, minimally invasive, and endoscopically assisted procedures.

- In August 2023, Erbe Elektromedizin GmbH launched HYBRIDknife flex, an innovative device combining needle-free, high-pressure hydrodissection and novel electrosurgical waveforms, streamlining endoscopic submucosal dissection (ESD) procedures.

- In June 2023, Olympus Corporation launched an advanced electrosurgical generator called ESG-410, designed to support options and efficiencies in the treatment of bladder cancer and enlarged prostate.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.