Europe Fluid Management Systems Market

Market Size in USD Billion

USD

3.27 Billion

USD

4.76 Billion

2024

2032

USD

3.27 Billion

USD

4.76 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.27 Billion | |

| USD 4.76 Billion | |

| % | |

|

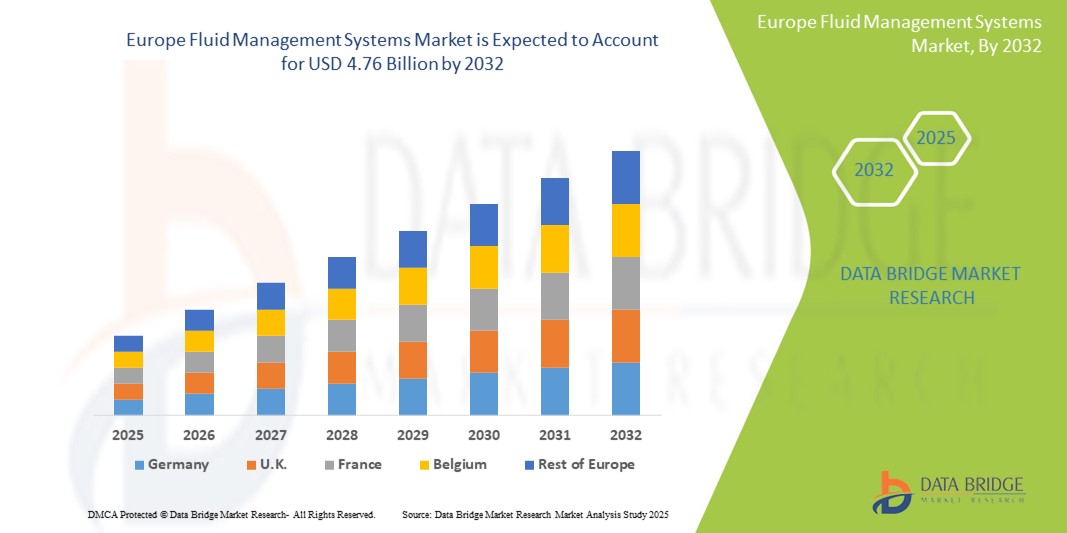

Fluid Management Systems Market Size

- The Europe Fluid Management Systems market size was valued at USD 3.27 billion in 2024 and is expected to reach USD 4.76 billion by 2032, at a CAGR of 4.8% during the forecast period

- The Europe Fluid Management Systems Market consists of a wide array of devices and systems designed to regulate fluid levels during surgical procedures, dialysis, and diagnostic interventions. These systems are essential for maintaining hemodynamic stability and optimizing patient outcomes across hospitals, ambulatory surgical centers, and specialty clinics.

- Key system types include suction and irrigation systems, fluid warming devices, fluid waste management systems, and dialyzers. Modern systems integrate features such as touch-screen interfaces, closed-loop automation, and real-time pressure and volume monitoring for enhanced efficiency and safety.

- There is growing adoption of advanced fluid management platforms offering high accuracy, reduced contamination risk, and improved surgical workflow efficiency, especially in urology, gynecology, and gastroenterology procedures.

Fluid Management Systems Market Analysis

- The Europe Fluid Management Systems market is driven by the increasing number of surgical procedures, growing preference for minimally invasive interventions, and the rising incidence of chronic conditions requiring fluid regulation, such as kidney disease and heart failure. Hospitals and surgical centers are increasingly adopting advanced fluid management solutions to improve surgical efficiency and reduce complications.

- Technological innovations—such as real-time flow monitoring, automated suction-irrigation systems, closed-loop fluid control, and integration with digital OR platforms—are transforming fluid management practices. These advancements enhance surgical precision, ensure patient safety, and streamline workflow across various specialties like urology, gynecology, and gastroenterology.

- Germany dominates the Fluid Management Systems market in Europe, holding the largest revenue share of 25.3% in 2025. This is attributed to its high surgical volume, robust hospital infrastructure, and strong adoption of OR automation technologies. The presence of leading medical device manufacturers and early uptake of digital fluid monitoring systems further support market leadership.

- Germany is projected to be the fastest-growing country in the Europe Fluid Management Systems market during the forecast period, fueled by national healthcare digitization efforts, rising investments in outpatient surgical facilities, and increased government funding for surgical safety and infection control technologies.

- Suction is expected to dominate the Europe Fluid Management Systems market with a market share of 38.4% in 2025 across Europe. These systems are widely used in laparoscopic and endoscopic surgeries for maintaining a clear surgical field. Their versatility, user-friendly operation, and critical role in maintaining intraoperative visibility drive consistent demand across surgical centers and hospitals.

Report Scope and Fluid Management Systems Market Segmentation

|

Attributes |

Fluid Management Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Fluid Management Systems Market Trends

“Shift Toward Integrated, Minimally Invasive, and Smart Surgical Solutions”

- A prominent trend in the Europe Fluid Management Systems Market is the integration of fluid management with minimally invasive surgical platforms, enhancing precision and safety during endoscopic and laparoscopic procedures.

- For instance, Stryker’s Neptune 3 Waste Management System enables closed fluid waste disposal and improved OR safety, minimizing exposure risks and enhancing workflow efficiency.

- Hospitals and surgical centers are adopting smart fluid control systems integrated with digital displays and automated pressure regulation for real-time fluid monitoring and improved surgical outcomes.

- Growing use of disposable, single-use fluid management components is reducing cross-contamination risks and aligning with infection control protocols.

- Increasing preference for outpatient procedures and ambulatory surgery centers is driving demand for compact, mobile, and user-friendly fluid management devices tailored to space-constrained environments.

- Enhanced integration with electronic health records (EHRs) and surgical planning tools enables better tracking of fluid usage, documentation accuracy, and postoperative care optimization

Fluid Management Systems Market Dynamics

Driver

“Rising Demand for Minimally Invasive Surgeries and Enhanced Surgical Precision”

- The growing shift toward minimally invasive surgical procedures across Europe is significantly driving the demand for advanced fluid management systems that offer superior control, visibility, and safety during surgeries

- For instance, laparoscopic and endoscopic procedures require efficient fluid irrigation and suction to maintain a clear surgical field and reduce complications.

- Rising patient preference for shorter recovery times, reduced surgical trauma, and fewer hospital stays is boosting the adoption of fluid management technologies in both public and private healthcare settings.

- Technological advancements in fluid regulation systems—such as real-time flow monitoring, automated suction control, and integrated waste management—are enhancing procedural outcomes.

- Increasing investments in ambulatory surgery centers and day-care hospitals are creating a need for compact, mobile, and easy-to-use fluid management devices that support a broad range of specialties.

- Surgeons and operating room staff are increasingly favoring smart systems that reduce manual workload, ensure hygienic fluid disposal, and enhance intraoperative efficiency

Restraint/Challenge

“High Capital Investment and Regulatory Compliance Burden”

- The high upfront cost of advanced fluid management systems—including integrated suction-irrigation units, waste disposal systems, and digital monitoring tools—poses a financial barrier for small and mid-sized healthcare facilities across Europe.

- For instance, state-of-the-art systems used in laparoscopic and endoscopic surgeries require significant capital investment, limiting adoption in cost-sensitive or rural settings.

- Complex regulatory requirements under the EU Medical Device Regulation (MDR) have extended approval timelines, increasing development costs for manufacturers and delaying product launches.

- Limited availability of skilled professionals trained in handling sophisticated fluid management technologies restricts efficient utilization in certain regions.

- Variability in regulatory interpretation across European countries and inconsistent reimbursement policies affect market penetration and investment decisions.

- Concerns over cross-contamination, infection control, and environmental waste disposal further complicate adoption, especially in facilities lacking standardized protocols or infrastructure

Fluid Management Systems Market Scope

The market is segmented on the basis product type, disposables and accessories, application, and end user.

- By Product type

On the basis of Product type, the Fluid Management Systems Market is into Integrated Fluid Management Systems and Standalone Fluid Management Systems. The Integrated systems segment is expected to dominate the market with the largest revenue share of 59.2% 2025, due to their ability to streamline surgical workflows by combining irrigation, suction, and waste management into a single unit. Their widespread adoption in minimally invasive surgeries enhances procedural safety and efficiency.

The Standalone systems segment is projected to witness the fastest CAGR from 2025 to 2032 while more cost-effective, are projected to witness steady growth, especially in smaller healthcare settings and ambulatory surgery centers requiring flexible, scalable solutions.

- By Disposables and Accessories

On the basis of Product, the Fluid Management Systems Market is into Visualization Systems, Pressure Transducers, Valves, Connectors and Fittings, Catheters, Bloodlines, Tubing Sets, Pressure Monitoring Lines, Suction Canisters, Cannulas, and Others. The Tubing sets and catheters segment is expected to dominate the market with the largest revenue share, owing to their routine usage and recurring demand across surgical specialties.

The visualization systems segment is projected to witness the fastest CAGR from 2025 to 2032, driven by increasing use of endoscopic procedures and high-definition imaging requirements.

- By Application

On the basis of application, the Fluid Management Systems market is segmented into Urology, Bronchoscopy, Arthroscopy, Cardiology, Neurology, Gastroenterology, Laparoscopy, Gynecology/Obstetrics, Otoscopy, Dentistry, Anesthesiology, and Others. The Laparoscopy held the largest market revenue share in 2025 due to the increasing volume of laparoscopic surgeries across Europe and demand for precise fluid regulation.

The Urology is expected to witness the fastest CAGR from 2025 to 2032, driven by the rising prevalence of kidney stones and urological cancers requiring minimally invasive interventions.

- By End users

On the basis of end users, the Fluid Management Systems market is segmented into Hospitals, Ambulatory Surgical Centers, Cosmetic Surgical Centers, and Others. The Hospitals segment accounted for the largest market revenue share in 2024, due to their high surgical case volumes, advanced infrastructure, and greater adoption of integrated fluid systems.

The Ambulatory surgical centers segment is expected to witness the fastest CAGR from 2025 to 2032, attributed to the growing trend of day-care surgeries, cost-efficiency, and the preference for minimally invasive procedures performed in outpatient settings.

Fluid Management Systems Market Regional Analysis

- Germany dominates the Europe Fluid Management Systems Market, accounting for the largest revenue share of 25.3% in 2025. This leadership is driven by Germany’s strong surgical infrastructure, high procedural volume in minimally invasive surgeries, and rapid adoption of integrated fluid management technologies in major hospitals across cities like Berlin, Munich, and Hamburg.

- The country’s emphasis on surgical precision and patient safety supports widespread use of advanced irrigation, suction, and waste management systems. In addition, Germany benefits from a strong presence of global and regional manufacturers, government initiatives for surgical care modernization, and robust investment in laparoscopic, arthroscopic, and urological procedures.

France Fluid Management Systems Market Insight

The France Fluid Management Systems Market is expected to experience stable growth throughout the forecast period, supported by increased investments in hospital automation, growing surgical volumes, and adoption of minimally invasive procedures. Healthcare facilities in Paris, Lyon, and Marseille are embracing fluid management solutions for specialties such as gynecology, urology, and gastroenterology to ensure efficient visualization and fluid control. Government-backed health reforms and funding under national healthcare infrastructure programs are aiding the replacement of outdated systems with smart, integrated fluid management platforms. Furthermore, the expansion of day-care surgical centers is fueling demand for portable, cost-effective systems tailored to short-stay procedures.

U.K. Fluid Management Systems Market Insight

The U.K. Fluid Management Systems Market is projected to register notable growth, driven by NHS-backed funding for surgical innovation, increasing adoption of endoscopic and minimally invasive surgeries, and the expansion of ambulatory care services. Major urban centers like London, Manchester, and Birmingham are witnessing strong uptake of fluid management systems integrated with high-definition visualization and automated suction systems. Despite post-Brexit regulatory transitions, the U.K. continues to attract international manufacturers and ensures high-quality standards through MHRA oversight. The increasing emphasis on reducing hospital stays, enhancing surgical outcomes, and enabling precision fluid control during procedures is shaping market dynamics. Additionally, the surge in elective and cosmetic surgeries post-pandemic is further contributing to the demand for reliable, compact fluid management systems.

Fluid Management Systems Market Share

The Fluid Management Systems industry is primarily led by well-established companies, including:

- Stryker Corporation (U.S.)

- Olympus Corporation (Japan)

- KARL STORZ SE & Co. KG (Germany)

- Baxter International Inc. (U.S.)

- Medtronic (Ireland)

- B. Braun Melsungen AG (Germany)

- Smith+Nephew (U.K.)

- Zimmer Biomet (U.S.)

- CONMED Corporation (U.S.)

- Hologic, Inc. (U.S.)

- Hager & Werken GmbH & Co. KG (Germany)

- Richard Wolf GmbH (Germany)

- Fresenius SE & Co. KGaA (Germany)

- Thermedx, LLC (U.S.)

- Nouvag AG (Switzerland)

Latest Developments in Europe Fluid Management Systems Market

- In March 2025, Stryker launched its next-generation integrated fluid management system across key European markets, featuring enhanced automation and real-time fluid monitoring to improve surgical precision and reduce operative time in minimally invasive procedures.

- In November 2024, Medtronic introduced the Advanced Fluid Control Suite with improved suction technology and smart waste management capabilities, deployed in major European hospitals to optimize fluid balance during complex surgeries.

- In August 2024, Olympus expanded its fluid management portfolio with the release of compact, portable irrigation and suction units tailored for outpatient and ambulatory surgical centers, addressing the rising demand for flexible and space-efficient solutions.

- In January 2024, Boston Scientific upgraded its fluid management disposables range, including advanced pressure transducers and tubing sets designed for enhanced safety and reduced risk of contamination during urological and cardiovascular procedures.

- In May 2023, CONMED introduced new visualization-compatible fluid management accessories aimed at improving workflow integration and ease of use in laparoscopic and arthroscopic surgeries across European healthcare facilities.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.