Europe Hereditary Cancer Testing Market

Market Size in USD Billion

USD

3.02 Billion

USD

7.69 Billion

2025

2033

USD

3.02 Billion

USD

7.69 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.02 Billion | |

| USD 7.69 Billion | |

| % | |

|

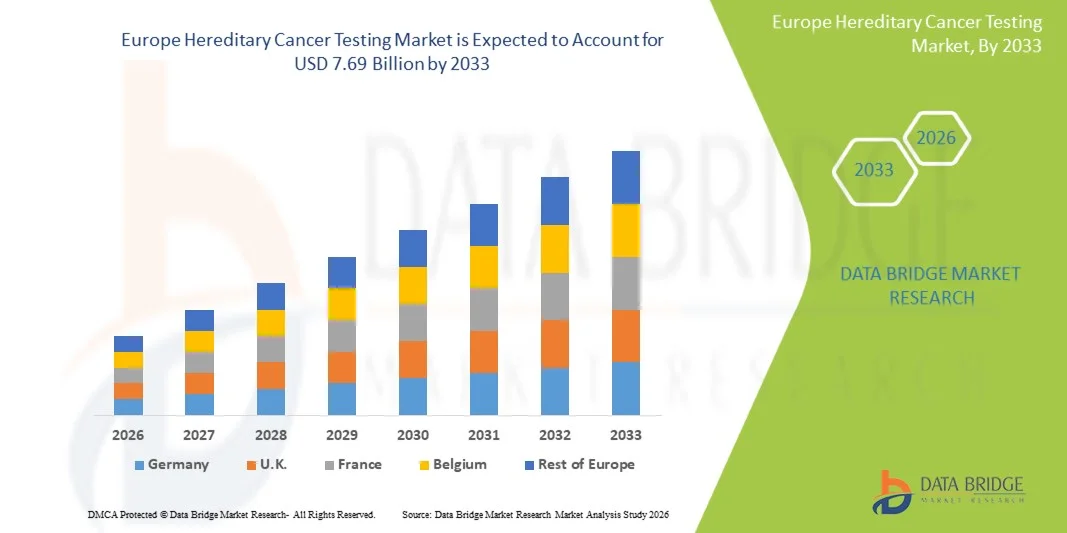

Europe Hereditary Cancer Testing Market Size

- The Europe Hereditary Cancer Testing Market size was valued at USD 3.02 billion in 2025 and is expected to reach USD 7.69 billion by 2033, at a CAGR of 12.40% during the forecast period

- The market growth is largely fueled by increasing advancements in genetic sequencing technologies and expanding adoption of precision medicine, enabling early detection and personalized risk assessment of hereditary cancers across global healthcare systems

- Furthermore, rising awareness regarding inherited genetic disorders, along with growing availability of genetic counseling and diagnostic services, is strengthening demand for Hereditary Cancer Testing solutions, thereby significantly boosting the industry's growth

Europe Hereditary Cancer Testing Market Analysis

- Smart genetic testing solutions, including hereditary cancer testing, are increasingly vital components of modern precision healthcare systems due to their ability to detect inherited cancer risks early, support personalized treatment decisions, and enable preventive healthcare strategies in both clinical and research settings

- The escalating demand for hereditary cancer testing is primarily fueled by rising awareness of genetic disorders, increasing adoption of precision medicine, and continuous advancements in genomic sequencing technologies

- The U.K. dominated the Europe Hereditary Cancer Testing Market with the largest revenue share of approximately 40.2% in 2025, characterized by advanced healthcare infrastructure, strong national screening programs, high awareness regarding genetic disorders, and early adoption of precision medicine, with the country witnessing substantial growth driven by expanding access to genetic testing and strong NHS-backed diagnostic initiatives

- Germany is expected to be the fastest growing country in the Europe Hereditary Cancer Testing Market during the forecast period, with a projected CAGR of around 9.1%, due to increasing investments in genomic research, rising adoption of precision medicine, strong healthcare reimbursement systems, and expanding use of advanced diagnostic technologies

- The multi panel set segment dominated the largest market revenue share of 58.3% in 2025, driven by its ability to screen multiple genes simultaneously for a wide range of hereditary cancers

Report Scope and Europe Hereditary Cancer Testing Market Segmentation

|

Attributes |

Hereditary Cancer Testing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Hereditary Cancer Testing Market Trends

“Enhanced Convenience Through AI and Digital Integration”

- A significant and accelerating trend in the Europe Hereditary Cancer Testing Market is the increasing integration of artificial intelligence (AI), advanced bioinformatics platforms, and digital health ecosystems to enhance testing accuracy, accessibility, and patient convenience. This integration is improving the speed and precision of genetic risk assessment and enabling more personalized healthcare decision-making

- For instance, AI-powered genomic analysis platforms are increasingly being used by diagnostic laboratories to rapidly interpret complex genetic variants associated with hereditary cancers such as BRCA1/BRCA2 mutations, reducing turnaround time and improving diagnostic efficiency

- AI integration in hereditary cancer testing enables advanced capabilities such as predictive risk modeling, identification of mutation patterns across large genomic datasets, and improved interpretation of variants of uncertain significance (VUS), thereby supporting more accurate clinical decision-making

- Furthermore, digital health integration allows hereditary cancer test results to be seamlessly shared with electronic health records (EHRs), enabling physicians to access patient genetic profiles in real time and design more targeted prevention or treatment strategies

- The growing adoption of telemedicine and digital genetic counseling platforms is also enhancing patient access to hereditary cancer testing services, particularly in remote or underserved areas across Europe

- This trend toward highly connected, data-driven, and AI-supported genomic diagnostics is fundamentally transforming hereditary cancer screening practices, with companies and laboratories increasingly investing in automation and intelligent analytics solutions

Europe Hereditary Cancer Testing Market Dynamics

Driver

“Rising Demand for Early Cancer Detection and Precision Medicine”

- The increasing burden of hereditary cancers and growing awareness regarding the importance of early genetic screening are key drivers fueling the Europe Hereditary Cancer Testing Market

- For instance, expanding national screening initiatives and research collaborations across Europe are encouraging the adoption of genetic testing for individuals with a family history of cancers such as breast, ovarian, and colorectal cancer

- As patients and healthcare providers increasingly prioritize preventive healthcare, hereditary cancer testing is becoming an essential tool for identifying high-risk individuals and enabling early intervention strategies

- Furthermore, advancements in next-generation sequencing (NGS) technologies have significantly improved test accuracy, scalability, and affordability, thereby expanding access to genetic testing services across clinical settings

- The rising adoption of precision medicine approaches, where treatment strategies are tailored based on genetic profiles, is further accelerating demand for hereditary cancer testing across oncology care pathways

Restraint/Challenge

“Data Privacy Concerns and High Cost of Genetic Testing”

- Concerns related to genetic data privacy and ethical handling of sensitive patient information represent a significant challenge for the widespread adoption of hereditary cancer testing in Europe

- Genetic testing involves highly sensitive personal and familial data, raising concerns regarding data security, consent management, and potential misuse of genetic information by third parties

- For instance, strict regulatory frameworks such as GDPR (General Data Protection Regulation) in Europe impose complex compliance requirements on genetic testing providers, increasing operational complexity and cost

- In addition, the relatively high cost of comprehensive hereditary cancer testing panels, particularly those based on advanced sequencing technologies, can limit accessibility for certain patient populations despite growing insurance coverage in some countries

- While costs are gradually declining due to technological advancements, affordability remains a barrier in broader population-level screening programs

- Addressing these challenges through stronger data protection frameworks, improved reimbursement policies, and cost-effective testing innovations will be critical for sustained market growth

Europe Hereditary Cancer Testing Market Scope

The market is segmented on the basis of test type, diagnosis type, technology, disease type, end user, and distribution channel.

• By Test Type

On the basis of test type, the Europe Hereditary Cancer Testing Market is segmented into multi panel set and single site genetic test. The multi panel set segment dominated the largest market revenue share of 58.3% in 2025, driven by its ability to screen multiple genes simultaneously for a wide range of hereditary cancers. These tests provide comprehensive risk assessment, enabling early detection and preventive care strategies. Rising awareness about genetic predisposition to cancer significantly boosts demand. Increasing adoption of advanced genomic technologies further supports growth. Growing preference for cost-effective and time-efficient testing enhances utilization. Expansion of personalized medicine strengthens adoption in clinical practice. Increasing availability of NGS-based panels improves diagnostic accuracy. Rising prevalence of hereditary cancer syndromes further fuels demand. Healthcare providers increasingly prefer multi-gene testing for better clinical outcomes. These factors collectively ensure dominance of the multi panel set segment.

The single site genetic test segment is expected to witness the fastest CAGR of 9.7% from 2026 to 2033, driven by increasing demand for targeted mutation testing in families with known genetic variants. These tests are highly accurate and cost-effective for specific gene analysis. Rising awareness among high-risk individuals supports growth. Expansion of genetic counseling services enhances adoption. Increasing insurance coverage for targeted testing further boosts demand. Growing use in confirmatory diagnostics strengthens the segment. Technological advancements improve test efficiency and turnaround time. These factors position single site genetic testing as the fastest-growing segment.

• By Diagnosis Type

On the basis of diagnosis type, the market is segmented into biopsy, imaging, and lab tests. The lab tests segment held the largest market revenue share of 49.6% in 2025, driven by the increasing use of blood and saliva-based genetic testing for cancer risk detection. Lab-based testing offers high accuracy and scalability, making it suitable for large population screening. Rising demand for early cancer detection supports growth. Increasing availability of advanced molecular diagnostic laboratories further drives adoption. Growing awareness about genetic screening programs enhances utilization. Expansion of hospital-based diagnostic services strengthens demand. Technological advancements in sequencing improve precision. Increasing integration of lab automation enhances efficiency. These factors ensure dominance of the lab tests segment.

The biopsy segment is expected to witness the fastest CAGR of 10.4% from 2026 to 2033, driven by its critical role in confirming cancer presence and genetic mutation analysis. Biopsy remains a gold standard for tissue-based diagnosis. Rising cancer incidence globally supports demand. Increasing use of minimally invasive biopsy techniques enhances adoption. Growing integration with genomic profiling strengthens clinical utility. Expansion of oncology centers boosts procedural volume. Technological improvements improve safety and accuracy. These factors position biopsy as the fastest-growing segment.

• By Technology

On the basis of technology, the market is segmented into sequencing, polymerase chain reaction (PCR), and microarray. The sequencing segment accounted for the largest market revenue share of 55.1% in 2025, driven by rapid advancements in next-generation sequencing (NGS) technologies. Sequencing enables comprehensive detection of genetic mutations associated with hereditary cancers. Increasing affordability of NGS platforms supports adoption. Rising demand for precision medicine boosts usage. Expanding genomic research initiatives further strengthens growth. High accuracy and deep genetic insights make sequencing highly preferred. Increasing clinical applications in oncology enhance demand. Growing integration into diagnostic workflows supports expansion. These factors ensure dominance of sequencing technology.

The PCR segment is expected to witness the fastest CAGR of 9.3% from 2026 to 2033, driven by its cost-effectiveness and wide accessibility in diagnostic laboratories. PCR is highly efficient for targeted gene amplification and mutation detection. Increasing use in early-stage screening supports growth. Rising demand for rapid diagnostic tools further boosts adoption. Expansion of decentralized testing facilities enhances accessibility. Technological improvements increase sensitivity and accuracy. Growing use in resource-limited settings strengthens demand. These factors position PCR as the fastest-growing technology segment.

• By Disease Type

On the basis of disease type, the market is segmented into hereditary breast & ovarian cancer syndrome, Cowden syndrome, Lynch syndrome, hereditary leukemia and hematologic malignancies syndromes, familial adenomatous polyposis (FAP), Li-Fraumeni syndrome, Von Hippel-Lindau disease, and multiple endocrine neoplasias (MEN) syndromes. The hereditary breast & ovarian cancer syndrome segment held the largest market revenue share of 32.8% in 2025, driven by high prevalence of BRCA1 and BRCA2 gene mutations. Increasing awareness of genetic breast cancer risk strongly supports testing demand. Rising incidence of breast and ovarian cancers globally further fuels growth. Expansion of screening programs enhances early detection. Strong availability of targeted therapies increases testing uptake. Growing adoption of preventive genetic testing among high-risk individuals supports demand. Healthcare initiatives promoting early diagnosis strengthen segment growth. These factors ensure dominance of this disease segment.

The Lynch syndrome segment is expected to witness the fastest CAGR of 10.8% from 2026 to 2033, driven by increasing recognition of hereditary colorectal cancer risks. Rising genetic screening programs support early identification. Growing awareness among physicians enhances diagnostic rates. Expansion of family-based testing improves detection efficiency. Increasing adoption of preventive oncology strategies boosts demand. Technological advancements in genomic testing enhance accuracy. These factors position Lynch syndrome as the fastest-growing disease segment.

• By End User

On the basis of end user, the market is segmented into hospitals, clinics, laboratories, radiology centers, diagnostic centers, and others. The diagnostic centers segment dominated the largest market revenue share of 41.7% in 2025, driven by increasing demand for specialized genetic testing services. Diagnostic centers offer advanced infrastructure and skilled professionals for accurate testing. Rising outsourcing of genetic testing from hospitals supports growth. Increasing awareness of early cancer detection boosts utilization. Expansion of private diagnostic chains strengthens accessibility. Technological advancements in testing platforms enhance efficiency. Growing availability of direct-to-consumer genetic testing further supports demand. These factors ensure dominance of diagnostic centers.

The laboratories segment is expected to witness the fastest CAGR of 9.9% from 2026 to 2033, driven by increasing investment in genomic research and testing infrastructure. Laboratories play a key role in high-throughput genetic analysis. Rising demand for large-scale cancer screening supports growth. Expansion of molecular diagnostic capabilities enhances efficiency. Increasing adoption of automation improves turnaround time. Growing collaboration with healthcare providers strengthens utilization. Technological advancements in sequencing platforms further boost demand. These factors position laboratories as the fastest-growing end user segment.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and retail sales. The direct tender segment held the largest market revenue share of 63.5% in 2025, driven by bulk procurement by hospitals, government programs, and large diagnostic organizations. Direct tenders ensure cost efficiency and standardized supply of genetic testing services. Increasing government screening initiatives support demand. Expansion of public healthcare infrastructure boosts procurement. Strong institutional partnerships enhance adoption. Rising focus on population-wide cancer screening programs further drives growth. These factors ensure dominance of direct tender distribution.

The retail sales segment is expected to witness the fastest CAGR of 8.6% from 2026 to 2033, driven by increasing demand for direct-to-consumer genetic testing kits. Growing awareness about hereditary cancer risk supports adoption. Expansion of online genetic testing platforms enhances accessibility. Rising preference for personalized health insights boosts demand. Increasing affordability of testing kits further supports growth. Technological advancements simplify sample collection and analysis. These factors position retail sales as the fastest-growing distribution channel.

Europe Hereditary Cancer Testing Market Regional Analysis

- The Europe Hereditary Cancer Testing Market is projected to expand at a substantial CAGR throughout the forecast period, driven by the increasing prevalence of hereditary cancer cases, rising awareness of early genetic screening, and the growing adoption of precision medicine across healthcare systems

- The region benefits from well-established healthcare infrastructure, strong regulatory frameworks, and expanding access to advanced genomic technologies. In addition, increasing investments in next-generation sequencing (NGS), coupled with growing integration of digital health platforms, is supporting widespread adoption of hereditary cancer testing

- The market is witnessing strong growth across hospitals, diagnostic laboratories, and research institutions, with increasing incorporation of genetic testing into routine oncology care pathways

U.K. Europe Hereditary Cancer Testing Market Insight

The U.K. Europe Hereditary Cancer Testing Market dominated Europe with the largest revenue share of approximately 40.2% in 2025, supported by advanced healthcare infrastructure, strong national screening programs, and high awareness regarding genetic disorders. The country has been an early adopter of precision medicine and genetic diagnostics, with the NHS playing a key role in expanding access to hereditary cancer testing services. In addition, ongoing government-backed genomic initiatives and expanding use of next-generation sequencing technologies are significantly driving market growth. Increasing demand for early cancer risk identification and preventive healthcare strategies continues to strengthen the U.K.’s leadership position in the European market.

Germany Europe Hereditary Cancer Testing Market Insight

The Germany Europe Hereditary Cancer Testing Market is expected to be the fastest growing in Europe during the forecast period, with a projected CAGR of around 9.1%, driven by rising investments in genomic research, increasing adoption of precision medicine, and strong healthcare reimbursement systems. Germany’s well-developed healthcare infrastructure and emphasis on technological innovation are supporting the rapid expansion of advanced genetic testing services. Furthermore, growing awareness of hereditary cancer risks and increasing integration of molecular diagnostics into clinical practice are accelerating market adoption. The country is also witnessing strong demand for advanced diagnostic technologies in both hospital and specialized laboratory settings, further supporting market expansion.

Europe Hereditary Cancer Testing Market Share

The Hereditary Cancer Testing industry is primarily led by well-established companies, including:

- Illumina (U.S.)

- Thermo Fisher Scientific (U.S.)

- Myriad Genetics (U.S.)

- Invitae Corporation (U.S.)

- Quest Diagnostics (U.S.)

- Labcorp (U.S.)

- Ambry Genetics (U.S.)

- F. Hoffmann-La Roche (Switzerland)

- Agilent Technologies (U.S.)

- Bio-Rad Laboratories (U.S.)

- BGI Genomics (China)

- Natera (U.S.)

- GeneDx (U.S.)

- Color Health (U.S.)

- Centogene (Germany)

- SOPHiA GENETICS (Switzerland)

- Guardant Health (U.S.)

- 23andMe (U.S.)

- ArcherDX (U.S.)

- Exact Sciences (U.S.)

Latest Developments in Europe Hereditary Cancer Testing Market

- In November 2023, the U.S. Food and Drug Administration (FDA) authorized the Invitae Common Hereditary Cancers Panel, a blood test that detects inherited genetic changes in 47 genes linked to hereditary cancer risk, marking a significant regulatory milestone in hereditary cancer diagnostics

- In March 2024, Exact Sciences launched the Riskguard hereditary cancer test, available to healthcare providers and covered by Medicare and many commercial insurance plans, expanding access to hereditary cancer risk assessment

- In February 2025, Foundation Medicine announced the launch of FoundationOneGermline and FoundationOneGermline More hereditary germline tests in the United States, offering expanded gene coverage for comprehensive hereditary cancer risk profiling

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.