Europe Hernia Mesh Repair Devices Market

Market Size in USD Billion

USD

1.00 Billion

USD

1.24 Billion

2025

2033

USD

1.00 Billion

USD

1.24 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.00 Billion | |

| USD 1.24 Billion | |

| % | |

|

Europe Hernia Mesh Repair Devices Market Size

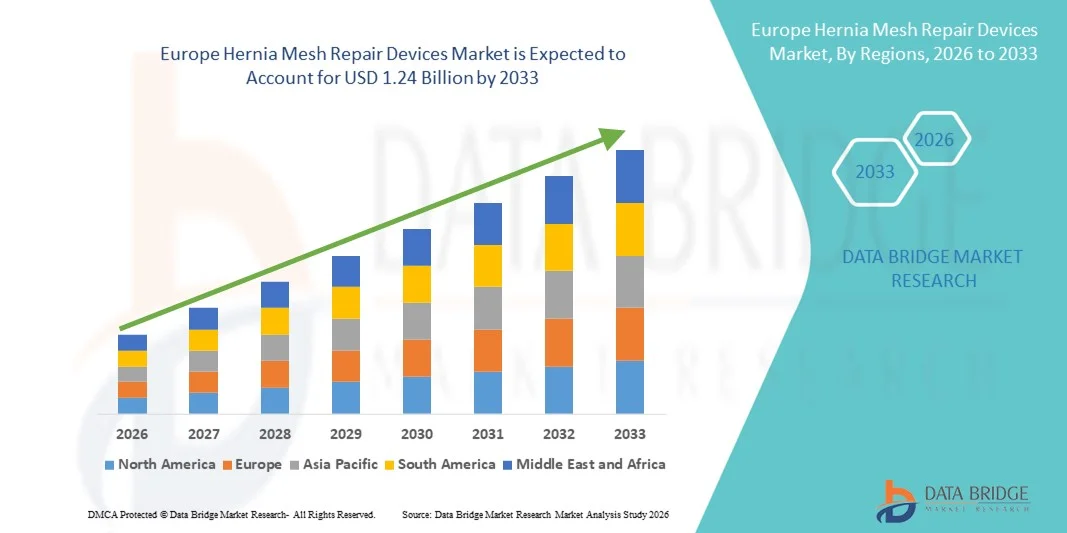

- The Europe hernia mesh repair devices market size was valued at USD 1.00 billion in 2025 and is expected to reach USD 1.24 billion by 2033, at a CAGR of 2.80% during the forecast period

- The market growth is largely fueled by increasing prevalence of hernia disorders, rising geriatric population, and growing awareness about minimally invasive surgical procedures across Europe, which are driving the demand for advanced hernia repair solutions

- Furthermore, technological advancements in mesh materials, such as lightweight, biocompatible, and absorbable meshes, along with rising preference for laparoscopic and robotic-assisted surgeries, are strengthening the adoption of hernia mesh devices. These factors, combined with favorable reimbursement policies in key European countries, are accelerating market expansion, thereby significantly boosting the industry's growth

Europe Hernia Mesh Repair Devices Market Analysis

- Hernia mesh repair devices, used for surgical correction of abdominal and other hernia types, are increasingly vital in modern healthcare due to their effectiveness in reducing recurrence rates, minimally invasive application, and improved patient recovery outcomes in both elective and emergency surgical procedures

- The escalating demand for hernia mesh devices is primarily fueled by the rising prevalence of hernia disorders, an aging population, growing awareness of minimally invasive surgical techniques, and technological advancements in mesh materials such as lightweight, absorbable, and biocompatible options

- Germany dominated the Europe hernia mesh repair devices market with the largest revenue share of 28.5% in 2025, characterized by a well-established healthcare infrastructure, high surgical procedure volumes, and the presence of key industry players, with hospitals and surgical centers increasingly adopting advanced laparoscopic and robotic-assisted mesh implantation techniques

- France is expected to be the fastest-growing country during the forecast period due to increasing healthcare spending, expanding hospital networks, and rising patient awareness about hernia repair solutions

- Meshes segment dominated the Europe hernia mesh repair devices market with a market share of 46.7% in 2025, driven by its proven long-term performance, broad clinical acceptance, and versatility for both open and laparoscopic hernia repair procedures

Report Scope and Europe Hernia Mesh Repair Devices Market Segmentation

|

Attributes |

Europe Hernia Mesh Repair Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Hernia Mesh Repair Devices Market Trends

Advancements in Minimally Invasive and Biocompatible Mesh Technologies

- A significant and accelerating trend in the Europe hernia mesh repair devices market is the adoption of minimally invasive surgical techniques, including laparoscopic and robotic-assisted procedures, combined with advanced biocompatible and lightweight mesh materials, enhancing patient recovery and reducing post-operative complications

- For instance, the TiMesh Light mesh allows surgeons to perform laparoscopic hernia repairs with reduced tissue irritation and faster recovery times, while maintaining the required strength for long-term outcomes

- Advanced mesh materials enable features such as absorbable coatings to minimize inflammation, improved structural flexibility for patient comfort, and antimicrobial properties to reduce post-surgical infections. For instance, Parietex™ Composite mesh offers dual-surface technology to reduce adhesion formation and optimize tissue integration

- The integration of advanced imaging, navigation, and robotic assistance in hernia repair surgeries facilitates precise placement of mesh and reduces operative time, improving overall surgical outcomes. Through a single surgical procedure, surgeons can address multiple hernia sites with enhanced accuracy and safety

- This trend towards more intelligent, patient-friendly, and clinically effective mesh solutions is fundamentally reshaping surgeon and patient expectations for hernia repair. Consequently, companies such as Medtronic are developing advanced meshes with enhanced biocompatibility, absorbable coatings, and ergonomic designs for laparoscopic application

- The demand for hernia mesh devices that offer improved surgical outcomes, reduced complications, and minimally invasive applicability is growing rapidly across both public and private healthcare settings, as hospitals increasingly prioritize patient safety and efficiency

- Regulatory approvals for next-generation meshes with innovative coatings and materials are facilitating market growth, as clinicians gain access to safer and more versatile surgical options

Europe Hernia Mesh Repair Devices Market Dynamics

Driver

Rising Hernia Prevalence and Increasing Surgical Interventions

- The increasing prevalence of abdominal and groin hernias among aging populations, coupled with the rising volume of elective and emergency surgical procedures, is a significant driver for the heightened demand for hernia mesh repair devices

- For instance, in March 2025, Ethicon introduced a new lightweight polypropylene mesh designed for laparoscopic hernia repair, aiming to improve patient outcomes and reduce recurrence rates. Such strategies by key companies are expected to drive market growth in the forecast period

- As healthcare providers focus on improving post-surgical recovery and minimizing complications, advanced mesh devices offer enhanced durability, reduced recurrence, and compatibility with minimally invasive techniques, providing a compelling advantage over traditional suturing methods

- Furthermore, growing awareness among surgeons and patients regarding mesh options and procedural advancements is making hernia mesh devices an essential component of modern hernia repair strategies, integrated into hospital procurement programs

- The ability to perform laparoscopic and robotic-assisted hernia repairs efficiently, with shorter hospital stays and faster return to normal activities, are key factors propelling the adoption of hernia mesh devices in both public and private healthcare facilities. The trend towards patient-centered care and hospital efficiency further contributes to market growth

- Rising investments in healthcare infrastructure across Europe, particularly in surgical theaters and minimally invasive procedure facilities, are increasing accessibility to advanced hernia mesh devices

- Expansion of training programs for surgeons in advanced mesh implantation techniques is improving procedural outcomes, enhancing trust in new mesh technologies, and supporting faster market adoption

Restraint/Challenge

Post-Surgical Complications and Regulatory Compliance Hurdles

- Concerns surrounding mesh-related post-surgical complications, including chronic pain, mesh migration, and infection risks, pose a significant challenge to broader market penetration. As hernia mesh devices are surgically implanted, adverse outcomes can raise hesitancy among surgeons and patients

- For instance, reports of mesh-related complications in laparoscopic procedures have made some patients and clinicians cautious in adopting newer mesh products

- Addressing these clinical concerns through rigorous preclinical testing, long-term follow-up studies, and adherence to stringent European regulatory standards such as MDR 2017/745 is crucial for building surgeon and patient confidence. Companies such as C.R. Bard emphasize clinical validation and post-market surveillance in their product documentation to reassure healthcare providers. Additionally, high costs of advanced mesh products compared to conventional options can limit adoption, particularly in smaller hospitals or budget-constrained healthcare systems. While some mid-range meshes are available, premium features such as antimicrobial coating and robotic-assisted compatibility often come at a higher price

- While reimbursement and hospital support are improving, perceived premium pricing for advanced hernia meshes can still hinder widespread adoption, especially in countries with constrained healthcare budgets or limited surgical infrastructure

- Overcoming these challenges through enhanced clinical validation, surgeon education, and development of cost-effective mesh solutions will be vital for sustained growth in the Europe hernia mesh repair devices market

- Negative publicity from litigation or adverse patient outcomes in certain countries can temporarily impact adoption rates and slow market momentum for newer mesh products

- Variability in regulatory approvals and post-market monitoring requirements across European countries can delay product launches and limit uniform market expansion for hernia mesh devices

Europe Hernia Mesh Repair Devices Market Scope

The market is segmented on the basis of product, surgery type, hernia type, and end user.

- By Product

On the basis of product, the Europe hernia mesh repair devices market is segmented into fixation devices, meshes, and surgical instruments. The meshes segment dominated the market with the largest market revenue share of 46.7% in 2025, driven by their critical role in reducing hernia recurrence and supporting tissue repair. Meshes are preferred for both open and minimally invasive procedures due to their proven long-term performance and versatility across hernia types. Hospitals and surgical centers prioritize advanced synthetic and composite meshes because of their biocompatibility and structural strength. Growing awareness among surgeons about lightweight and absorbable meshes further reinforces their dominance. The adoption of laparoscopic and robotic-assisted surgeries has also increased the demand for specialized meshes that are easier to manipulate and implant. Leading manufacturers, such as Ethicon and Medtronic, are continuously innovating in this segment to improve patient outcomes and reduce post-surgical complications.

The fixation devices segment is anticipated to witness the fastest growth rate of 12.8% from 2026 to 2033, fueled by increasing adoption in laparoscopic surgeries. Fixation devices such as tacks, sutures, and glue ensure proper mesh placement and reduce post-operative complications such as migration or folding. Minimally invasive procedures require advanced fixation tools for accurate placement, driving demand in both hospitals and ambulatory surgery centers. Technological innovations such as absorbable tacks and ergonomic applicators enhance procedural efficiency. Surgeons increasingly prefer fixation devices that reduce operating time and improve recovery outcomes. The trend toward robotic-assisted surgeries also supports growth, as precise fixation is critical in these procedures.

- By Surgery Type

On the basis of surgery type, the market is segmented into open tension-free repair surgery and laparoscopic surgery. The laparoscopic surgery segment dominated the Europe hernia mesh repair devices market with 52% market share in 2025, driven by its minimally invasive nature, faster patient recovery, and reduced post-operative pain. Hospitals increasingly prefer laparoscopic procedures for both primary and recurrent hernias because they enable shorter hospital stays and lower complication rates. Advanced laparoscopic meshes and fixation devices are in high demand due to their compatibility with robotic-assisted systems. The segment is further supported by increasing surgeon training programs and reimbursement policies in key European countries. The ability to treat multiple hernia sites through small incisions also enhances patient satisfaction, contributing to market growth. Laparoscopic surgery is particularly favored in Germany, France, and the UK, where hospital infrastructure and skilled workforce are well-established.

The open tension-free repair surgery segment is expected to witness the fastest CAGR of 10.5% from 2026 to 2033, primarily driven by the high prevalence of incisional and complex hernias requiring traditional open repair. Open surgery remains preferred in cases where laparoscopic intervention is not feasible, including large or recurrent hernias. Technological improvements in sutures, meshes, and fixation tools are making open procedures safer and more efficient. Many ambulatory surgery centers still perform open repairs, especially for older patients or those with comorbidities. The segment benefits from cost-effectiveness and familiarity among surgeons, particularly in Italy and Spain, where laparoscopic adoption is still growing. Patient awareness and training in enhanced surgical techniques are further supporting this segment’s growth.

- By Hernia Type

On the basis of hernia type, the market is segmented into incisional hernia, umbilical hernia, inguinal hernia, and femoral hernia. The inguinal hernia segment dominated the market with 38% market share in 2025, due to its high prevalence across Europe, particularly among adult males. Inguinal hernia repair is the most commonly performed hernia surgery, fueling demand for advanced meshes and fixation devices. Hospitals and ambulatory centers prioritize lightweight and absorbable meshes to reduce recurrence and post-surgical complications. Minimally invasive laparoscopic procedures for inguinal hernia are also increasing, driving demand for specialized surgical instruments. The segment is supported by awareness campaigns promoting early detection and timely surgical intervention. Surgeons in Germany and France prefer mesh-based inguinal hernia repair for long-term durability and patient comfort.

The incisional hernia segment is expected to witness the fastest growth rate of 13.1% from 2026 to 2033, driven by the increasing number of abdominal surgeries and associated post-operative hernia complications. Incisional hernias often require complex repair with specialized meshes and fixation devices, boosting market demand. Robotic-assisted and laparoscopic approaches for incisional hernia repair are gaining traction in advanced healthcare facilities. Growing patient awareness regarding minimally invasive options and faster recovery is also fueling adoption. Key players are developing composite meshes and advanced fixation systems to address these complex hernias. Rising surgical infrastructure and skilled workforce in the UK and Spain are further supporting segment growth.

- By End User

On the basis of end user, the market is segmented into hospitals and ambulatory surgery centers (ASCs). The hospitals segment dominated the Europe hernia mesh repair devices market with 67% market share in 2025, driven by higher surgical volumes, access to advanced infrastructure, and ability to perform both open and laparoscopic procedures. Hospitals are the primary buyers of meshes, fixation devices, and surgical instruments due to the need for standardized procedures and long-term patient follow-up. Hospitals in Germany, France, and the UK increasingly adopt robotic-assisted surgeries, which require high-quality mesh and fixation products. The segment also benefits from reimbursement policies and insurance coverage, which encourage the use of advanced surgical devices. Hospitals serve as training centers for surgeons, further strengthening adoption of new hernia repair technologies.

The ambulatory surgery centers segment is expected to witness the fastest CAGR of 11.7% from 2026 to 2033, due to the growing trend of outpatient minimally invasive hernia repair procedures. ASCs provide cost-effective care, shorter hospital stays, and convenient access for patients undergoing laparoscopic or open surgeries. Increasing patient preference for outpatient procedures and improved post-surgical care protocols are driving demand in this segment. ASCs are also investing in advanced meshes and fixation devices compatible with minimally invasive techniques. Technological innovations and portable surgical instruments are making these centers more capable of handling complex procedures efficiently. Rising awareness among patients about outpatient hernia repair benefits is further boosting growth in this segment.

Europe Hernia Mesh Repair Devices Market Regional Analysis

- Germany dominated the Europe hernia mesh repair devices market with the largest revenue share of 28.5% in 2025, characterized by a well-established healthcare infrastructure, high surgical procedure volumes, and the presence of key industry players

- Patients and surgeons in the region highly value advanced mesh materials, enhanced fixation devices, and minimally invasive approaches that reduce post-operative complications, accelerate recovery, and improve long-term outcomes

- This widespread adoption is further supported by favorable reimbursement policies, increasing healthcare spending, well-trained surgical workforce, and the presence of leading hernia mesh manufacturers such as Ethicon and Medtronic, establishing Germany as a hub for advanced hernia repair procedures

The U.K. Hernia Mesh Repair Devices Market Insight

The U.K. hernia mesh repair devices market captured a significant revenue share in 2025, fueled by increasing prevalence of hernia disorders and growing adoption of minimally invasive laparoscopic procedures. Surgeons and hospitals are prioritizing advanced meshes and fixation devices to reduce post-operative complications and recurrence rates. The growing trend of outpatient and ambulatory surgeries is also supporting market expansion. Additionally, rising patient awareness and the demand for faster recovery times are encouraging hospitals to adopt advanced mesh technologies. The integration of robotic-assisted hernia repair techniques is further enhancing precision and improving patient outcomes, which is contributing to the overall market growth in the country.

Germany Hernia Mesh Repair Devices Market Insight

The Germany hernia mesh repair devices market accounted for the largest share in Europe in 2025, driven by the country’s well-established healthcare infrastructure and high surgical volumes. Hospitals and specialized surgical centers emphasize minimally invasive and robotic-assisted hernia repairs, which require high-quality meshes and fixation devices. Surgeons increasingly prefer lightweight and biocompatible meshes due to better patient outcomes and reduced post-operative complications. Rising government initiatives for advanced surgical technologies and reimbursement policies support broader adoption. Germany’s focus on innovation and continuous medical training ensures that hospitals remain early adopters of advanced hernia repair solutions. The strong presence of key market players such as Ethicon and Medtronic further strengthens the market’s dominance in Germany.

France Hernia Mesh Repair Devices Market Insight

The France hernia mesh repair devices market is projected to grow at a substantial CAGR during the forecast period, primarily driven by increasing surgical interventions and rising awareness about minimally invasive procedures. Hospitals are investing in advanced meshes and fixation devices for laparoscopic and open surgeries. The country also sees growing adoption of robotic-assisted hernia repair systems, improving precision and patient recovery. French patients increasingly demand faster recovery, reduced post-operative pain, and lower recurrence rates, supporting mesh adoption. Government healthcare spending and favorable reimbursement policies facilitate the use of advanced surgical devices. Hospitals and ambulatory surgery centers are adopting these technologies in both new facilities and renovations.

Italy Hernia Mesh Repair Devices Market Insight

The Italy hernia mesh repair devices market is anticipated to expand at a considerable CAGR during the forecast period, fueled by increasing prevalence of abdominal hernias and rising demand for minimally invasive surgeries. Hospitals and surgical centers are focusing on patient-centric care, which includes faster recovery and reduced complications. Advanced meshes and fixation devices are increasingly preferred due to their durability and improved clinical outcomes. Technological adoption in robotic-assisted procedures is gaining momentum, especially in metropolitan hospitals. Patient awareness and demand for outpatient hernia repair procedures are contributing to growth. The market is further strengthened by collaborations between device manufacturers and surgical training centers.

Europe Hernia Mesh Repair Devices Market Share

The Europe Hernia Mesh Repair Devices industry is primarily led by well-established companies, including:

- Boston Scientific Corporation (U.S.)

- Cook (U.S.)

- TELA Bio, Inc. (U.S.)

- Integra LifeSciences Corporation (U.S.)

- BD (U.S.)

- Ethicon Inc. (U.S.)

- C.R. Bard, Inc. (U.S.)

- Medtronic (Ireland)

- W. L. Gore & Associates, Inc. (U.S.)

- Zimmer Biomet. (U.S.)

- Smith+Nephew plc (U.K.)

- Stryker (U.S.)

- Olympus Corporation (Japan)

- Karl Storz SE & Co. KG (Germany)

- Getinge AB (Sweden)

- Medline Industries, LP (U.S.)

- Cardinal Health, Inc. (U.S.)

- Teleflex Incorporated (U.S.)

- CONMED Corporation (U.S.)

- Arthrex, Inc. (U.S.)

What are the Recent Developments in Europe Hernia Mesh Repair Devices Market?

- In January 2026, BD announced a key milestone with the first prophylactic use of CE‑marked Phasix™ Mesh in Greece following expanded indications in Europe, and the launch of three new mesh sizes in 2025, marking a shift toward not just repair but hernia prevention strategies in high‑risk abdominal surgeries

- In June 2025, TELA Bio, Inc. announced the European commercial launch of OviTex® Inguinal Reinforced Tissue Matrix, a next‑generation soft‑tissue mesh engineered specifically for laparoscopic and robotic‑assisted inguinal hernia repair. This product launch provides European surgeons with additional biologic‑reinforced options that aim to optimize clinical performance and patient outcomes in minimally invasive hernia procedures

- In April 2025, W. L. Gore & Associates launched GORE® SYNECOR Preperitoneal Biomaterial across Europe, a hybrid synthetic mesh designed for both minimally invasive and open hernia repair that offers enhanced handling, conformability, and permanent strength to support complex repairs and help reduce recurrence. This regional rollout follows CE‑mark approval and expands Gore’s hernia repair portfolio within European surgical practices

- In February 2024, GORE® SYNECOR Preperitoneal Biomaterial received CE‑Mark approval and was launched in Europe, offering a hybrid synthetic mesh option for preperitoneal hernia reinforcement in both laparoscopic and open surgeries, addressing complex hernia cases with permanent strength and enhanced tissue support

- In February 2021, W. L. Gore & Associates launched GORE® SYNECOR Intraperitoneal Biomaterial in Europe, the Middle East, and South Africa a tri‑layer hybrid mesh designed to support complex hernia repairs with improved handling and tissue integration, expanding available options for surgeons treating ventral/incisional hernias

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.