Europe Hydrocephalus Market

Market Size in USD Billion

USD

411.87 Billion

USD

603.89 Billion

2025

2033

USD

411.87 Billion

USD

603.89 Billion

2025

2033

| 2026 - 2033 | |

| USD 411.87 Billion | |

| USD 603.89 Billion | |

| % | |

|

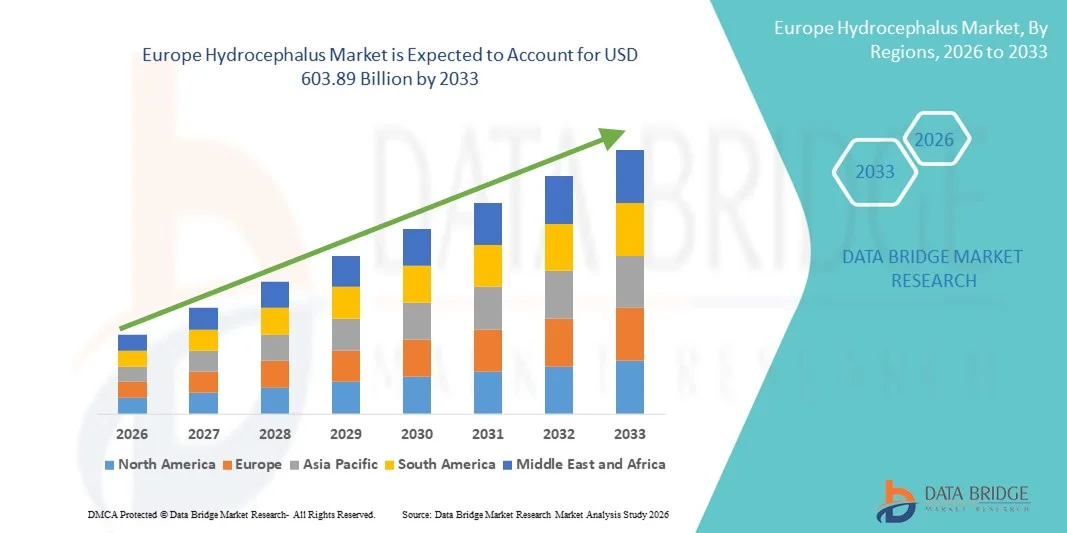

Europe Hydrocephalus Market Size

- The Europe hydrocephalus market size was valued at USD 411.87 billion in 2025 and is expected to reach USD 603.89 billion by 2033, at a CAGR of 4.90% during the forecast period

- The market growth is largely fueled by the growing prevalence of hydrocephalus cases worldwide, increasing geriatric population, and rising incidence of neurological disorders, which are driving demand for effective treatment and management solutions

- Furthermore, increasing healthcare expenditure, improved diagnostic capabilities, and growing adoption of advanced treatment options such as shunt systems and endoscopic third ventriculostomy (ETV) are establishing modern hydrocephalus treatments as the preferred choice for clinicians. These converging factors are accelerating the uptake of hydrocephalus solutions, thereby significantly boosting the industry’s growth

Europe Hydrocephalus Market Analysis

- Hydrocephalus is a neurological condition characterized by an abnormal accumulation of cerebrospinal fluid (CSF) in the brain’s ventricles, leading to increased intracranial pressure and potentially causing brain damage if untreated

- The market growth is primarily driven by rising prevalence of hydrocephalus cases globally, increasing geriatric population, and growing awareness about early diagnosis and effective treatment options such as shunt systems and endoscopic third ventriculostomy (ETV)

- U.K. dominated the Hydrocephalus market with the largest revenue share of approximately 42.8% in 2025, supported by advanced healthcare infrastructure, strong government funding for neurological care, high adoption of advanced neurosurgical treatments, and well-established patient support systems

- Germany is expected to be the fastest-growing country in the Hydrocephalus market during the forecast period, driven by increasing healthcare expenditure, rapid adoption of advanced neurosurgical technologies, expanding hospital infrastructure, and growing focus on improving patient outcomes

- The Treatment segment dominated the largest market revenue share of 63.7% in 2025, driven by increasing surgical procedures and rising demand for advanced treatment solutions. Surgical intervention, primarily shunt placement and endoscopic third ventriculostomy, remains the standard treatment for most hydrocephalus cases

Report Scope and Hydrocephalus Market Segmentation

|

Attributes |

Hydrocephalus Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Hydrocephalus Market Trends

Advancements in Endoscopic and Minimally Invasive Procedures

- A significant and accelerating trend in the global hydrocephalus market is the increasing adoption of endoscopic third ventriculostomy (ETV) and other minimally invasive surgical procedures, which reduce recovery time and postoperative complications compared to traditional shunt surgeries

- For instance, hospitals in Europe and North America are increasingly using ETV combined with choroid plexus cauterization (ETV/CPC) in pediatric hydrocephalus cases to improve long-term outcomes

- Minimally invasive approaches are also supported by advanced imaging technologies that enhance surgical precision and reduce risks

- This shift is driven by surgeon preference for procedures that reduce shunt dependency and long-term revision rates

- As a result, medical centers are investing in training and equipment to support endoscopic procedures, thereby driving market growth

- The trend toward minimally invasive surgery is expected to continue as clinical evidence supports better patient outcomes and lower complication rates

Europe Hydrocephalus Market Dynamics

Driver

Growing Need Due to Rising Incidence of Hydrocephalus and Improved Healthcare Access

- The increasing prevalence of hydrocephalus cases globally, including congenital and acquired forms, is a major driver for the hydrocephalus market

- For instance, in October 2022, the U.S. FDA approved the ReFlow Ventricular Catheter System (ReFlow System) to improve the management of shunt malfunctions in hydrocephalus patients, offering a new solution for treating shunt obstruction without surgery

- Rising geriatric population and increasing incidence of neurodegenerative disorders, brain injuries, and infections are contributing to higher hydrocephalus cases

- Improved access to healthcare facilities and better diagnostic imaging are increasing the number of diagnosed patients

- Increasing investments in neurosurgical infrastructure and advanced treatment centers are supporting market growth

- These factors are driving higher adoption of shunt systems, neuroendoscopic equipment, and monitoring devices globally

Restraint/Challenge

High Treatment Costs and Risk of Shunt Complications

- High treatment costs associated with hydrocephalus surgery, shunt implantation, and long-term follow-up pose a major challenge to market growth

- For instance, the high rate of shunt failure and complications such as infection and obstruction often require revision surgeries, increasing overall treatment costs and patient burden

- Shunt malfunction rates and long-term complications can lead to repeated hospitalizations and additional medical expenses

- Limited access to advanced treatment options in low-income regions may restrict market growth

- Insurance coverage limitations and high out-of-pocket expenses for patients can hinder adoption of advanced shunt systems

- Addressing these challenges through improved device reliability, better patient monitoring, and cost-effective treatment strategies is essential for sustained market growth

Europe Hydrocephalus Market Scope

The market is segmented on the basis of type, diagnostic & treatment, age group, and end users.

- By Type

On the basis of type, the Hydrocephalus market is segmented into Congenital Hydrocephalus, Acquired Hydrocephalus, Normal-Pressure Hydrocephalus, and Ex-Vacuo Hydrocephalus. The Congenital Hydrocephalus segment dominated the largest market revenue share of 42.1% in 2025, driven by early diagnosis and increasing neonatal screening programs. The segment is highly influenced by birth defects, genetic factors, and prenatal conditions leading to cerebrospinal fluid (CSF) accumulation. Growing awareness among healthcare professionals and parents about early signs of hydrocephalus supports early intervention. The availability of advanced imaging technologies, such as MRI and CT, facilitates early diagnosis. Congenital hydrocephalus often requires long-term management and surgical interventions, increasing market demand. Increasing healthcare expenditure in developed countries further strengthens the segment. Hospitals and pediatric centers remain key consumers due to high treatment volumes. Moreover, government initiatives for neonatal care and child health also support market growth. Therefore, congenital hydrocephalus remained dominant in 2025.

The Normal-Pressure Hydrocephalus segment is expected to witness the fastest CAGR of 10.8% from 2026 to 2033, driven by rising geriatric population and growing prevalence of neurodegenerative disorders. Normal-pressure hydrocephalus is often underdiagnosed due to symptom similarity with Alzheimer’s and Parkinson’s disease. Increasing awareness and improved diagnostic tools are expected to drive market growth. Advanced imaging techniques and improved clinical protocols are supporting early detection. Rising number of elderly patients requiring surgical management contributes to the segment’s growth. Increased research and clinical trials focused on NPH treatment further boost demand. Adoption of shunt and endoscopic third ventriculostomy (ETV) procedures is increasing. In addition, healthcare providers are increasingly investing in geriatric care infrastructure. Thus, NPH is expected to register the fastest growth rate.

- By Diagnostic & Treatment

On the basis of diagnostic & treatment, the Hydrocephalus market is segmented into Diagnostic and Treatment. The Treatment segment dominated the largest market revenue share of 63.7% in 2025, driven by increasing surgical procedures and rising demand for advanced treatment solutions. Surgical intervention, primarily shunt placement and endoscopic third ventriculostomy, remains the standard treatment for most hydrocephalus cases. The treatment segment benefits from technological advancements in shunt systems and minimally invasive surgical techniques. Rising adoption of programmable shunts and improved patient outcomes support segment growth. The growing number of hospitals performing neurosurgical procedures increases demand for treatment devices and services. In addition, increasing awareness about hydrocephalus treatment options drives early intervention. Government healthcare initiatives and insurance coverage further support treatment adoption. Overall, treatment remains the dominant segment due to high surgical volumes.

The Diagnostic segment is expected to witness the fastest CAGR of 11.5% from 2026 to 2033, driven by increasing utilization of advanced neuroimaging technologies such as MRI and CT scans. Early diagnosis is critical for improving patient outcomes and reducing long-term disability. Rising investments in diagnostic infrastructure and availability of advanced imaging equipment in hospitals and diagnostic centers boost growth. Increased awareness among clinicians regarding early detection of hydrocephalus is encouraging timely diagnosis. Technological advancements in imaging software and AI-based diagnostic tools also support segment expansion. Growth in screening programs for neonates and elderly patients further fuels diagnostic demand. Thus, diagnostic segment is expected to grow at the fastest rate.

- By Age Group

On the basis of age group, the Hydrocephalus market is segmented into Pediatric and Adult. The Pediatric segment dominated the largest market revenue share of 55.2% in 2025, driven by the high incidence of congenital hydrocephalus and pediatric neurological conditions. Early diagnosis through neonatal screening and advanced imaging supports timely treatment. Pediatric hydrocephalus often requires long-term management and repeated interventions, increasing market demand. The presence of specialized pediatric neurosurgery centers further supports segment dominance. Increasing healthcare spending on child health and neonatal care programs enhances market growth. In addition, rising awareness among parents and pediatricians about hydrocephalus symptoms contributes to early intervention. Therefore, pediatric patients remain the primary market for hydrocephalus treatment and management.

The Adult segment is expected to witness the fastest CAGR of 12.3% from 2026 to 2033, driven by increasing incidence of acquired hydrocephalus and normal-pressure hydrocephalus among elderly patients. Aging population and rising prevalence of neurodegenerative disorders contribute significantly to adult hydrocephalus cases. Increasing adoption of diagnostic screening for elderly patients is supporting early detection. Rising trauma cases and brain injuries also increase adult hydrocephalus incidence. Growing demand for minimally invasive treatment options and improved shunt technologies supports market growth. Therefore, the adult segment is expected to register the fastest growth rate.

- By End Users

On the basis of end users, the Hydrocephalus market is segmented into Hospitals, Clinics, Diagnostic Centers, and Academic Institutions & Research Organizations. The Hospitals segment dominated the largest market revenue share of 49.6% in 2025, driven by the high volume of neurosurgical procedures and availability of specialized treatment facilities. Hospitals offer comprehensive diagnosis and treatment services, including advanced imaging, shunt surgery, and postoperative care. The presence of skilled neurosurgeons and multidisciplinary teams supports better patient outcomes. Hospitals also benefit from higher reimbursement rates and strong infrastructure. Rising hospital investments in neurology departments further strengthen market dominance. In addition, hospitals conduct most hydrocephalus-related surgical interventions, leading to consistent demand for treatment devices and services. Therefore, hospitals remained the dominant end-user segment in 2025.

The Academic Institutions & Research Organizations segment is expected to witness the fastest CAGR of 13.0% from 2026 to 2033, driven by increasing research activities and clinical trials focused on hydrocephalus treatment innovations. Growing funding for neuroscience research and development of advanced treatment technologies contributes to market growth. Academic centers are increasingly collaborating with medical device manufacturers to develop improved shunt systems and diagnostic tools. The rise in scientific publications and clinical studies on hydrocephalus supports research expansion. In addition, increasing government grants and institutional support for neurological research further boost segment growth. Therefore, academic institutions and research organizations are expected to grow at the fastest rate.

Europe Hydrocephalus Market Regional Analysis

- The Europe hydrocephalus market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing prevalence of hydrocephalus, rising neurological disorder cases, and improving access to advanced neurosurgical treatments

- The region benefits from strong healthcare infrastructure, high adoption of innovative treatment options, and growing government support for neurological care. In addition, increasing awareness about early diagnosis and timely intervention is fueling market growth across both pediatric and adult patient segments

- Europe is witnessing an expansion in hydrocephalus treatment centers, advanced diagnostic facilities, and specialized neurosurgery departments, which is supporting wider patient access to effective treatment and postoperative care. The increasing number of clinical trials and research initiatives focused on improved shunt systems and minimally invasive procedures is also contributing to market expansion

U.K. Hydrocephalus Market Insight

The U.K. hydrocephalus market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by advanced healthcare infrastructure, strong government funding for neurological care, and a high adoption rate of advanced neurosurgical treatments. The U.K. has well-established patient support systems and specialized neurological centers that facilitate early diagnosis and effective management of hydrocephalus cases. In addition, the country’s focus on improving patient outcomes through adoption of innovative shunt systems, endoscopic third ventriculostomy (ETV), and continuous postoperative monitoring is driving market growth. Increasing public awareness, rising healthcare expenditure, and improved access to specialized treatment options further strengthen the U.K. market outlook.

Germany Hydrocephalus Market Insight

The Germany hydrocephalus market is expected to expand at a considerable CAGR during the forecast period, driven by increasing healthcare expenditure, rapid adoption of advanced neurosurgical technologies, and expanding hospital infrastructure. Germany’s strong focus on innovation and patient safety supports the integration of technologically advanced shunt systems and minimally invasive treatment approaches. The country’s growing emphasis on improving patient outcomes and enhancing neurological care services is also boosting market growth. Furthermore, Germany is witnessing an increase in research activities, clinical trials, and collaborations between medical device manufacturers and healthcare institutions, which is expected to accelerate the adoption of next-generation hydrocephalus treatment solutions

Europe Hydrocephalus Market Share

The Hydrocephalus industry is primarily led by well-established companies, including:

• Integra LifeSciences (U.S.)

• Stryker (U.S.)

• Sophysa (France)

• Aesculap (Germany)

• B. Braun S.E. (Germany)

• Spiegelberg (Germany)

• Natus Medical (U.S.)

• Boston Scientific (U.S.)

• Evoke Neuroscience (U.S.)

• Orbis Medical (U.K.)

• Chhabra Healthcare (India)

• HT Medical (South Korea)

• NuVasive (U.S.)

• Cerenovus (U.S.)

• Anspach (U.S.)

• Santron (Germany)

• Raumedic (Germany)

• Integra NeuroSciences (U.S.)

• Medtronic Neurosurgery (U.S.)

Latest Developments in Europe Hydrocephalus Market

- In April 2021, Medtronic launched the Strata™ II programmable valve for its hydrocephalus shunt system, designed to improve cerebrospinal fluid (CSF) flow control and reduce risks of over-drainage in patients with normal pressure and communicating hydrocephalus. The advanced valve allows clinicians to non-invasively adjust multiple pressure settings, helping tailor therapy to individual patient needs and potentially decreasing the frequency of revision surgeries. This launch reflects ongoing innovation in shunt technology aimed at improving patient outcomes and reducing complications

- In June 2023, CereVasc Inc. received Investigational Device Exemption (IDE) approval from the U.S. Food and Drug Administration (FDA) to begin the pivotal STRIDE study of its eShunt system for treating normal pressure hydrocephalus (NPH). The eShunt system offers a minimally invasive alternative to traditional ventriculoperitoneal shunts by enabling percutaneous transvenous-transdural implantation, potentially reducing surgical recovery time and long-term complications

- In September 2023, CereVasc partnered with LianMedical to introduce the eShunt system and related products in China, expanding clinical access to innovative hydrocephalus treatment technologies in the Asia-Pacific region. This strategic distribution agreement aims to broaden availability of next-generation hydrocephalus solutions in several major Chinese markets

- In September 2024, Integra LifeSciences received FDA approval for its innovative anti-siphon shunt system designed to reduce over-drainage complications by automatically adjusting cerebrospinal fluid flow based on patient positioning. The approval marked a significant advancement in shunt valve technology, offering neurosurgeons a tool to help decrease the need for revision procedures and improve patient comfort

- In July 2024, B. Braun Melsungen AG expanded its hydrocephalus product portfolio through the acquisition of a specialized shunt technology company, strengthening its presence in pediatric and adult hydrocephalus markets worldwide. The acquisition includes proprietary catheter and valve designs optimized for durability and clinical performance, reinforcing B. Braun’s neurosurgery offerings

- In May 2024, Sophysa Ltd. partnered with leading pediatric hospitals across Europe to conduct clinical trials for its smart shunt monitoring system, which provides real-time data on intracranial pressure and cerebrospinal fluid flow to support early detection of complications. The wireless-enabled monitoring device aims to improve long-term management and reduce emergency interventions in pediatric hydrocephalus patients

- In January 2024, Medtronic plc announced U.S. FDA approval of its new Strata II Hydrocephalus Shunt Valve, which offers improved flow control and reduces the risk of overdrainage, enhancing shunt therapy personalization and clinical performance. This regulatory milestone underscores continued innovation by major medtech players in hydrocephalus management technologies

- In April 2025, Integra LifeSciences Holdings Corporation announced the acquisition of NeuroVentures Dynamics, LLC, a privately held medical device company specializing in hydrocephalus shunt technologies, expanding Integra’s neurotechnology portfolio with new innovative platforms. This acquisition strengthens Integras position in the competitive neurotechnology market by integrating advanced shunt systems and supporting future product development

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.